Key Insights

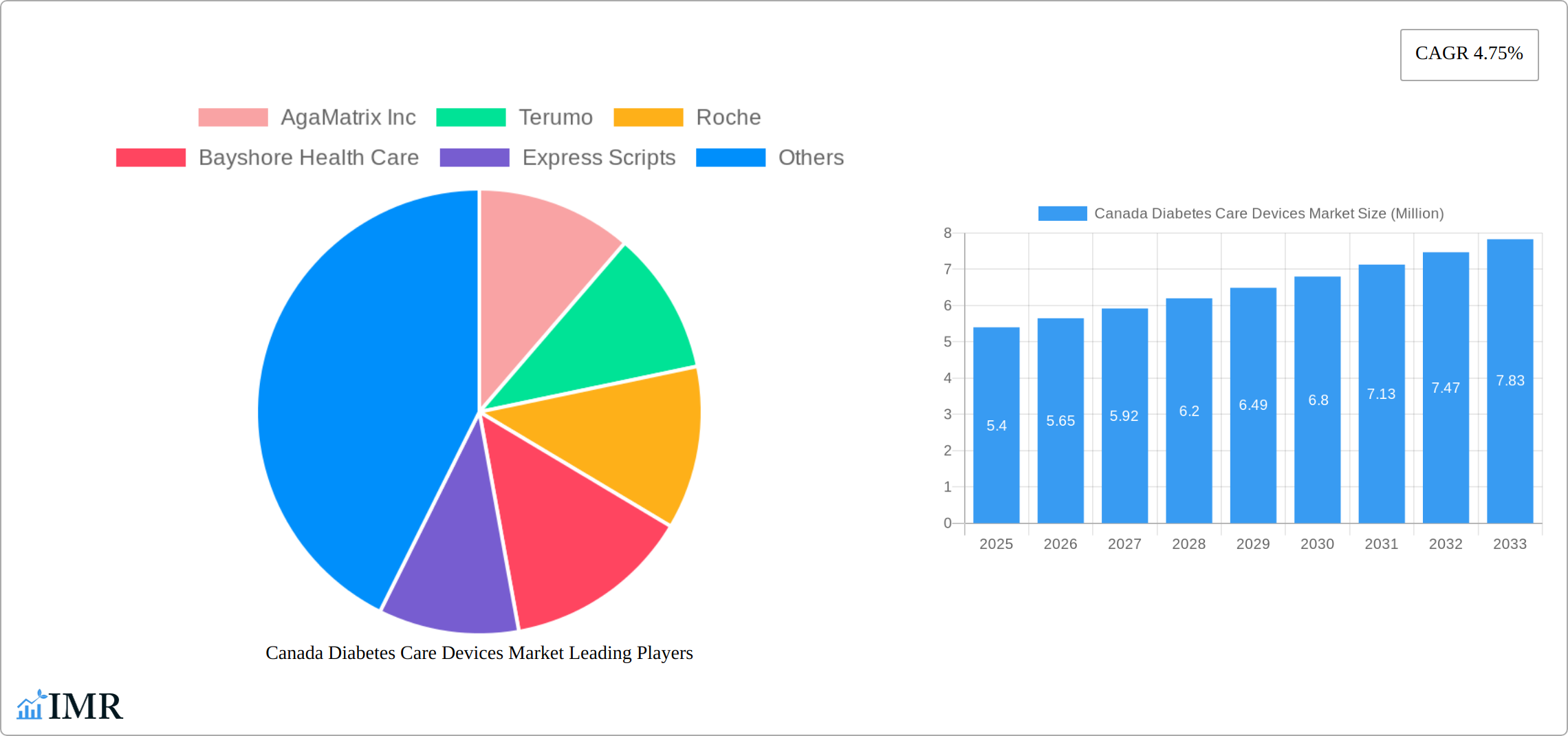

The Canada diabetes care devices market, valued at $5.40 million in 2025, is projected to experience robust growth, driven by a rising prevalence of diabetes, an aging population, and increasing adoption of advanced technologies for disease management. The market's Compound Annual Growth Rate (CAGR) of 4.75% from 2025 to 2033 indicates a steady expansion, fueled by several key factors. Increased awareness of the benefits of continuous glucose monitoring (CGM) systems and insulin pumps is driving demand for sophisticated devices. Furthermore, government initiatives promoting early diagnosis and better diabetes management contribute significantly to market growth. The market is segmented into various device types, including glucose monitoring systems (CGMs, self-monitoring blood glucose devices), insulin delivery systems (insulin pumps, pens), and other related supplies. The high cost of advanced devices, however, remains a significant restraint, particularly for patients without comprehensive insurance coverage. Competition among established players like Medtronic, Abbott, and Novo Nordisk, alongside emerging companies focusing on innovative technologies, will shape the market landscape. Regional variations in access to healthcare and technological adoption across Eastern, Western, and Central Canada also influence market dynamics. The increasing focus on telehealth and remote patient monitoring will likely drive the demand for connected devices and related services in the coming years.

The increasing prevalence of Type 1 and Type 2 diabetes in Canada is a primary driver of market growth. This is further amplified by the rising incidence of comorbidities associated with diabetes, such as cardiovascular disease and neuropathy, leading to increased demand for effective management tools. The market is witnessing a shift toward technologically advanced devices like CGM systems offering real-time glucose monitoring and improved data management. These systems not only improve glycemic control but also enhance patient convenience and compliance. Further growth can be attributed to the growing number of diabetes education programs and initiatives aimed at promoting self-management techniques and empowering patients to take control of their health. While pricing remains a barrier, the long-term benefits of better diabetes management through advanced technology ultimately outweigh the initial costs for many patients, contributing to the market's positive growth trajectory.

Canada Diabetes Care Devices Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Canada Diabetes Care Devices Market, encompassing market dynamics, growth trends, dominant segments, and key players. With a focus on the parent market of diabetes care and the child market of devices, this report offers invaluable insights for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with 2025 as the base year and a forecast period of 2025-2033. The market size is presented in million units.

Canada Diabetes Care Devices Market Market Dynamics & Structure

The Canadian diabetes care devices market is characterized by a moderately concentrated landscape, with key players like Medtronic, Abbott, and Novo Nordisk A/S holding significant market share (xx%). Technological innovation, particularly in continuous glucose monitoring (CGM) and insulin pump technology, is a major driver. Stringent regulatory frameworks by Health Canada influence product approvals and market entry. The market faces competition from alternative therapies, including lifestyle modifications and non-device-based treatments. The aging population and increasing prevalence of diabetes contribute significantly to market growth. M&A activity within the sector remains moderate, with xx major deals recorded in the past five years.

- Market Concentration: Moderately concentrated, with top players holding xx% market share.

- Technological Innovation: CGM and advanced insulin delivery systems are key drivers.

- Regulatory Framework: Health Canada approvals are crucial for market entry.

- Competitive Substitutes: Lifestyle changes and alternative therapies pose competition.

- End-User Demographics: Aging population and rising diabetes prevalence fuel demand.

- M&A Trends: Moderate M&A activity, with xx deals in the past five years.

- Innovation Barriers: High R&D costs, stringent regulatory pathways, and intellectual property protection.

Canada Diabetes Care Devices Market Growth Trends & Insights

The Canadian diabetes care devices market experienced a CAGR of xx% during 2019-2024 and is projected to grow at a CAGR of xx% from 2025-2033, reaching a market size of xx million units by 2033. This growth is driven by increasing diabetes prevalence, rising healthcare expenditure, and technological advancements leading to improved patient outcomes and convenience. The adoption rate of CGM systems is steadily increasing, while the market for insulin pumps continues to mature. Consumer behavior is shifting towards preference for user-friendly, connected devices, and remote monitoring capabilities. The market penetration of advanced devices remains relatively low but is expected to rise significantly during the forecast period.

Dominant Regions, Countries, or Segments in Canada Diabetes Care Devices Market

Ontario and Quebec represent the largest segments of the Canadian diabetes care devices market, driven by higher population density and greater prevalence of diabetes. Within the product categories, the segments of insulin pumps (xx million units) and continuous glucose monitoring (xx million units) are experiencing the highest growth rates. The strong performance of basal or long-acting insulins like Lantus and Tresiba, along with the increasing popularity of GLP-1 receptor agonists (like Victoza and Trulicity) and SGLT-2 inhibitors (Invokana, Jardiance), is further driving market expansion. The significant market share of these segments is attributed to the increasing prevalence of type 2 diabetes and the growing adoption of more effective and convenient treatment options. Government initiatives promoting diabetes management and insurance coverage for these advanced therapies also contribute to their dominance.

- Key Drivers: Higher diabetes prevalence in Ontario and Quebec, government initiatives supporting diabetes care.

- Dominant Segments: Insulin pumps, Continuous Glucose Monitoring (CGM) Systems, GLP-1 receptor agonists, SGLT-2 inhibitors and Basal or Long Acting insulins.

- Market Share: xx% for Ontario and Quebec combined. xx% for insulin pumps and CGM.

Canada Diabetes Care Devices Market Product Landscape

The Canadian diabetes care devices market showcases a diverse range of products, from traditional blood glucose meters and insulin syringes to advanced CGM systems and sophisticated insulin pumps. Recent innovations focus on improving accuracy, ease of use, and connectivity. Many devices now integrate with mobile apps for data tracking and remote monitoring, enhancing patient convenience and empowering self-management. This trend towards integration and data-driven insights is expected to continue driving market growth. Unique selling propositions include smaller device sizes, longer battery life, and enhanced data analytics capabilities.

Key Drivers, Barriers & Challenges in Canada Diabetes Care Devices Market

Key Drivers:

- Increasing prevalence of diabetes

- Rising healthcare expenditure

- Technological advancements in device design and functionality

- Government initiatives promoting diabetes management

Challenges and Restraints:

- High cost of advanced devices and therapies, limiting accessibility for some patients.

- Stringent regulatory requirements for new product approvals leading to longer time to market.

- Competition from alternative therapies and lifestyle interventions.

- Supply chain disruptions impacting device availability. This resulted in xx% increase in device price in 2022.

Emerging Opportunities in Canada Diabetes Care Devices Market

- Expansion of telehealth and remote patient monitoring solutions.

- Growth in demand for integrated diabetes management platforms.

- Increasing adoption of artificial intelligence (AI) in diabetes management.

- Growing focus on personalized diabetes care and treatment strategies.

Growth Accelerators in the Canada Diabetes Care Devices Market Industry

The long-term growth of the Canadian diabetes care devices market will be significantly fueled by continued technological innovation, specifically in areas such as closed-loop insulin delivery systems, non-invasive glucose monitoring, and AI-driven predictive analytics. Strategic partnerships between device manufacturers, pharmaceutical companies, and healthcare providers are also expected to accelerate market expansion. This collaboration will enhance the integration of devices and therapies to deliver comprehensive diabetes care solutions. Furthermore, expansion into underserved populations and regions, through targeted outreach programs and education initiatives will boost market growth.

Key Players Shaping the Canada Diabetes Care Devices Market Market

- AgaMatrix Inc

- Terumo

- Roche

- Bayshore Health Care

- Express Scripts

- One Drop

- Eli Lilly

- LMC Diabetes and Endocrinology

- Medtronic

- Ypsomed Holding AG

- Telus Health

- AstraZeneca

- Sanofi Aventis

- Becton Dickinson

- Johnson and Johnson (Lifescan)

- Abbott

- Bristol Myers Squibb

- Novo Nordisk A/S

- Arkray

- Boehringer Ingelheim

- Dexcom

- Ascensia Diabetes Care

Notable Milestones in Canada Diabetes Care Devices Market Sector

- July 2023: Dexcom, Inc. receives Health Canada approval for its Dexcom G7 Continuous Glucose Monitoring System.

- July 2022: NuGen Medical Devices Inc. receives Health Canada approval for its needle-free insulin delivery system, InsuJet.

In-Depth Canada Diabetes Care Devices Market Market Outlook

The future of the Canadian diabetes care devices market is bright, driven by sustained technological advancements, expanding access to innovative therapies, and a growing focus on patient empowerment and improved health outcomes. Strategic partnerships and collaborations will play a crucial role in accelerating market growth, while addressing challenges related to affordability and accessibility. The market is poised for significant expansion, with a continued shift towards personalized and connected care solutions.

Canada Diabetes Care Devices Market Segmentation

-

1. Product Type

- 1.1. Monitoring Devices

- 1.2. Management Devices

-

2. End-Use

- 2.1. Hospitals

- 2.2. Clinics

- 2.3. Home Healthcare

-

3. Geography

- 3.1. Ontario

- 3.2. Quebec

- 3.3. British Columbia

- 3.4. Alberta

- 3.5. Manitoba

- 3.6. Saskatchewan

- 3.7. Nova Scotia

- 3.8. New Brunswick

- 3.9. Newfoundland and Labrador

- 3.10. Prince Edward Island

Canada Diabetes Care Devices Market Segmentation By Geography

- 1. Canada

Canada Diabetes Care Devices Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.75% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies

- 3.3. Market Restrains

- 3.3.1 ; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures

- 3.3.2 Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products

- 3.4. Market Trends

- 3.4.1. The Continuous Glucose Monitoring Devices Segment is Growing at a Significant Pace

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Diabetes Care Devices Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Monitoring Devices

- 5.1.2. Management Devices

- 5.2. Market Analysis, Insights and Forecast - by End-Use

- 5.2.1. Hospitals

- 5.2.2. Clinics

- 5.2.3. Home Healthcare

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Ontario

- 5.3.2. Quebec

- 5.3.3. British Columbia

- 5.3.4. Alberta

- 5.3.5. Manitoba

- 5.3.6. Saskatchewan

- 5.3.7. Nova Scotia

- 5.3.8. New Brunswick

- 5.3.9. Newfoundland and Labrador

- 5.3.10. Prince Edward Island

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Eastern Canada Canada Diabetes Care Devices Market Analysis, Insights and Forecast, 2019-2031

- 7. Western Canada Canada Diabetes Care Devices Market Analysis, Insights and Forecast, 2019-2031

- 8. Central Canada Canada Diabetes Care Devices Market Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 AgaMatrix Inc

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 Terumo

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Roche

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 Bayshore Health Care

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 Express Scripts

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 One Drop

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 Eli Lilly

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 LMC Diabetes and Endocrinology

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Medtronic

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 Ypsomed Holding AG

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.11 Telus Health

- 9.2.11.1. Overview

- 9.2.11.2. Products

- 9.2.11.3. SWOT Analysis

- 9.2.11.4. Recent Developments

- 9.2.11.5. Financials (Based on Availability)

- 9.2.12 AstraZeneca

- 9.2.12.1. Overview

- 9.2.12.2. Products

- 9.2.12.3. SWOT Analysis

- 9.2.12.4. Recent Developments

- 9.2.12.5. Financials (Based on Availability)

- 9.2.13 Sanofi Aventis

- 9.2.13.1. Overview

- 9.2.13.2. Products

- 9.2.13.3. SWOT Analysis

- 9.2.13.4. Recent Developments

- 9.2.13.5. Financials (Based on Availability)

- 9.2.14 Becton Dickinson

- 9.2.14.1. Overview

- 9.2.14.2. Products

- 9.2.14.3. SWOT Analysis

- 9.2.14.4. Recent Developments

- 9.2.14.5. Financials (Based on Availability)

- 9.2.15 Johnson and Johnson (Lifescan)

- 9.2.15.1. Overview

- 9.2.15.2. Products

- 9.2.15.3. SWOT Analysis

- 9.2.15.4. Recent Developments

- 9.2.15.5. Financials (Based on Availability)

- 9.2.16 Abbott

- 9.2.16.1. Overview

- 9.2.16.2. Products

- 9.2.16.3. SWOT Analysis

- 9.2.16.4. Recent Developments

- 9.2.16.5. Financials (Based on Availability)

- 9.2.17 Bristol Myers Squibb

- 9.2.17.1. Overview

- 9.2.17.2. Products

- 9.2.17.3. SWOT Analysis

- 9.2.17.4. Recent Developments

- 9.2.17.5. Financials (Based on Availability)

- 9.2.18 Novo Nordisk A/S

- 9.2.18.1. Overview

- 9.2.18.2. Products

- 9.2.18.3. SWOT Analysis

- 9.2.18.4. Recent Developments

- 9.2.18.5. Financials (Based on Availability)

- 9.2.19 Arkray

- 9.2.19.1. Overview

- 9.2.19.2. Products

- 9.2.19.3. SWOT Analysis

- 9.2.19.4. Recent Developments

- 9.2.19.5. Financials (Based on Availability)

- 9.2.20 Boehringer Ingelheim

- 9.2.20.1. Overview

- 9.2.20.2. Products

- 9.2.20.3. SWOT Analysis

- 9.2.20.4. Recent Developments

- 9.2.20.5. Financials (Based on Availability)

- 9.2.21 Dexcom

- 9.2.21.1. Overview

- 9.2.21.2. Products

- 9.2.21.3. SWOT Analysis

- 9.2.21.4. Recent Developments

- 9.2.21.5. Financials (Based on Availability)

- 9.2.22 Ascensia Diabetes Care

- 9.2.22.1. Overview

- 9.2.22.2. Products

- 9.2.22.3. SWOT Analysis

- 9.2.22.4. Recent Developments

- 9.2.22.5. Financials (Based on Availability)

- 9.2.1 AgaMatrix Inc

List of Figures

- Figure 1: Canada Diabetes Care Devices Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Canada Diabetes Care Devices Market Share (%) by Company 2024

List of Tables

- Table 1: Canada Diabetes Care Devices Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Canada Diabetes Care Devices Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 5: Canada Diabetes Care Devices Market Revenue Million Forecast, by End-Use 2019 & 2032

- Table 6: Canada Diabetes Care Devices Market Volume K Unit Forecast, by End-Use 2019 & 2032

- Table 7: Canada Diabetes Care Devices Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Geography 2019 & 2032

- Table 9: Canada Diabetes Care Devices Market Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 11: Canada Diabetes Care Devices Market Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: Eastern Canada Canada Diabetes Care Devices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Eastern Canada Canada Diabetes Care Devices Market Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: Western Canada Canada Diabetes Care Devices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Western Canada Canada Diabetes Care Devices Market Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: Central Canada Canada Diabetes Care Devices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Central Canada Canada Diabetes Care Devices Market Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: Canada Diabetes Care Devices Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 20: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 21: Canada Diabetes Care Devices Market Revenue Million Forecast, by End-Use 2019 & 2032

- Table 22: Canada Diabetes Care Devices Market Volume K Unit Forecast, by End-Use 2019 & 2032

- Table 23: Canada Diabetes Care Devices Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 24: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Geography 2019 & 2032

- Table 25: Canada Diabetes Care Devices Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Canada Diabetes Care Devices Market Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Diabetes Care Devices Market?

The projected CAGR is approximately 4.75%.

2. Which companies are prominent players in the Canada Diabetes Care Devices Market?

Key companies in the market include AgaMatrix Inc, Terumo, Roche, Bayshore Health Care, Express Scripts, One Drop, Eli Lilly, LMC Diabetes and Endocrinology, Medtronic, Ypsomed Holding AG, Telus Health, AstraZeneca, Sanofi Aventis, Becton Dickinson, Johnson and Johnson (Lifescan), Abbott, Bristol Myers Squibb, Novo Nordisk A/S, Arkray, Boehringer Ingelheim, Dexcom, Ascensia Diabetes Care.

3. What are the main segments of the Canada Diabetes Care Devices Market?

The market segments include Product Type, End-Use, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.40 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

The Continuous Glucose Monitoring Devices Segment is Growing at a Significant Pace.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

July 2023: Dexcom, Inc. has received approval from Health Canada for their latest Dexcom G7 Continuous Glucose Monitoring System. This advanced system is designed for individuals with diabetes of all types, aged two years and above. Dexcom, Inc. specializes in manufacturing reliable continuous glucose monitoring solutions for people living with diabetes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Diabetes Care Devices Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Diabetes Care Devices Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Diabetes Care Devices Market?

To stay informed about further developments, trends, and reports in the Canada Diabetes Care Devices Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence