Key Insights

The graphics processor (GPU) market is experiencing robust growth, driven by the increasing demand for high-performance computing across diverse sectors. The market, currently valued in the billions (the exact figure is unavailable but inferred to be substantial based on a CAGR of 33.35% and a "million" value unit), is projected to continue its rapid expansion through 2033. Key drivers include the proliferation of high-resolution displays, the rise of artificial intelligence (AI) and machine learning (ML) applications, advancements in gaming technology, and the expanding automotive industry's reliance on advanced driver-assistance systems (ADAS) and autonomous driving technologies. The significant penetration of smartphones, tablets, and notebooks further fuels demand for integrated and dedicated GPUs, while the growth of cloud computing increases demand for cloud-based GPU solutions. Segmentation by type reveals a dynamic landscape, with dedicated graphics cards retaining a significant share but facing competition from integrated and hybrid solutions that offer cost-effective performance. Market segmentation by deployment reflects the ongoing shift towards cloud-based solutions, though on-premise deployments remain substantial, particularly in high-performance computing applications.

The market's growth trajectory is influenced by several factors. While technological advancements and increasing computing power are primary drivers, challenges such as supply chain disruptions and the high cost of advanced GPUs can act as restraints. However, the consistent innovation in GPU architecture, the integration of GPUs into various applications, and the continuous expansion of the global digital economy are expected to outweigh these challenges. Major players such as NVIDIA, AMD, Intel, and Qualcomm are actively involved in research and development, striving to enhance performance, efficiency, and power consumption. Regional analysis indicates a strong presence across North America, Europe, and Asia Pacific, with the latter expected to experience particularly rapid growth due to increasing smartphone adoption and technological advancements. The competitive landscape is dynamic, with established players facing increasing competition from emerging companies specializing in niche applications and technologies.

Graphic Processor Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Graphic Processor (GPU) industry, encompassing market dynamics, growth trends, regional dominance, product landscape, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. The report segments the market by type (Dedicated Graphics Card, Integrated Graphics Solutions, Hybrid Solutions), deployment (On-premise, Cloud), and application (Smartphones, Tablets & Notebooks, Workstations, Gaming PCs, Media & Entertainment, Automotives), offering a granular view of this rapidly evolving sector. The report projects a market size of xx Million units by 2033.

Graphic Processor Industry Market Dynamics & Structure

The graphic processor market is characterized by high competition among established players and emerging entrants. Market concentration is moderate, with a few dominant players holding significant market share, while numerous smaller companies cater to niche segments. Technological innovation is a primary driver, with continuous advancements in GPU architecture, memory technology, and processing power shaping market trends. Regulatory frameworks concerning data privacy and security play a significant role, especially in applications like automotive and cloud computing. Competitive product substitutes, primarily CPUs with integrated graphics, exist but are often less powerful for demanding applications. End-user demographics are diverse, ranging from individual gamers and consumers to large enterprises and data centers. M&A activity is relatively frequent, with larger players acquiring smaller companies to expand their product portfolios and technological capabilities.

- Market Concentration: Moderate, with top 5 players holding approximately xx% market share in 2025.

- Technological Innovation: Key drivers include advancements in AI, machine learning, and high-performance computing.

- Regulatory Frameworks: Compliance with data privacy regulations (e.g., GDPR) impacts cloud-based deployments.

- Competitive Substitutes: Integrated graphics solutions offer a cost-effective alternative but lack performance in high-demand scenarios.

- End-User Demographics: Diverse, encompassing consumers, businesses, and government organizations.

- M&A Trends: Consolidation is expected to continue, with larger players acquiring smaller companies to gain technological advantages and market share. Estimated xx M&A deals in the forecast period.

Graphic Processor Industry Growth Trends & Insights

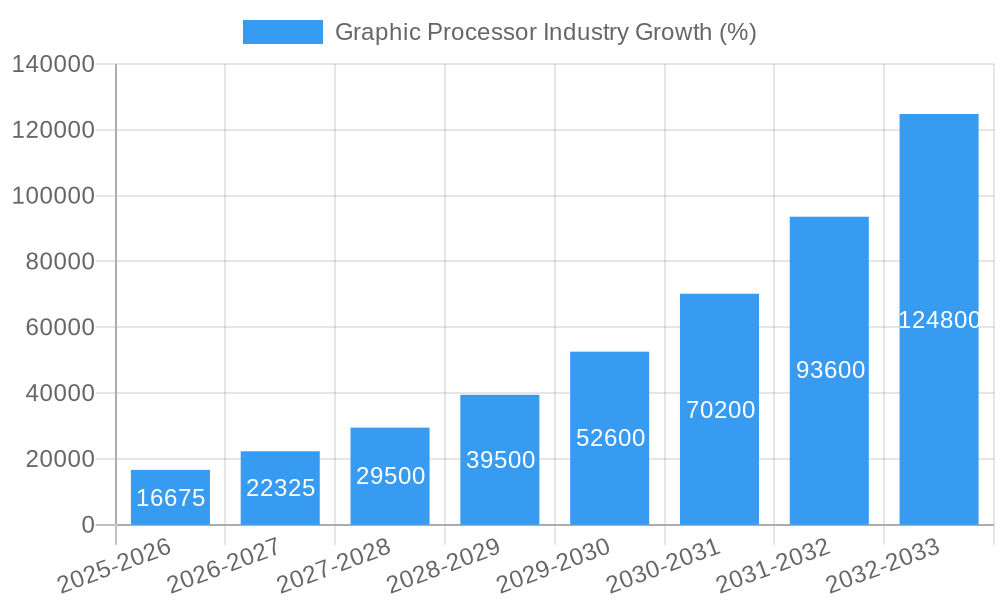

The global graphic processor market exhibits strong growth momentum, fueled by increasing demand across various applications. The historical period (2019-2024) witnessed a Compound Annual Growth Rate (CAGR) of xx%, driven by factors such as the rising adoption of gaming PCs, smartphones with advanced graphical capabilities, and the proliferation of data centers. Technological disruptions, particularly the advancement of AI and machine learning, are further accelerating market expansion. The market penetration of high-end GPUs in specific segments, such as high-performance computing and automotive, is significantly increasing. Shifting consumer behavior toward immersive gaming experiences and high-quality media consumption also contributes to market growth. We predict a CAGR of xx% for the forecast period (2025-2033), reaching a projected xx Million units by 2033.

Dominant Regions, Countries, or Segments in Graphic Processor Industry

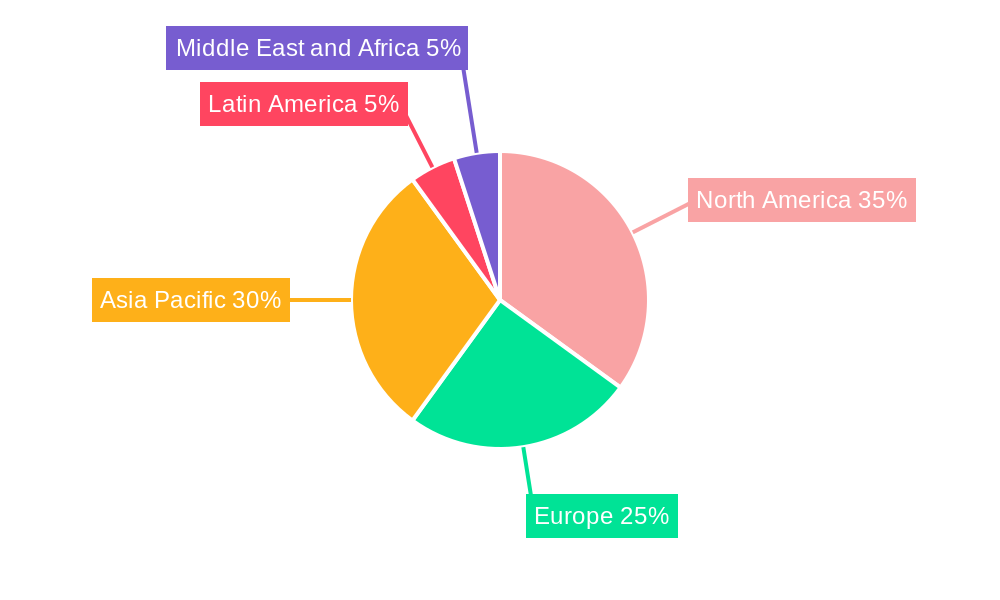

North America and Asia-Pacific are the dominant regions in the graphic processor market. Within these regions, the United States and China, respectively, are leading countries due to robust technological innovation, high consumer spending on electronics, and significant investments in data center infrastructure.

By Type: Dedicated graphics cards dominate the market due to their superior performance, catering to demanding applications like gaming and professional workstations. However, integrated graphics solutions witness significant growth, driven by increasing adoption in budget-friendly laptops and smartphones.

By Deployment: On-premise deployments remain dominant, particularly in high-performance computing and professional applications. However, cloud-based deployments are rapidly expanding, fueled by the increasing demand for scalable and cost-effective computing solutions.

By Application: Smartphones and gaming PCs are the largest application segments, driven by high consumer demand for enhanced visual experiences. The automotive segment shows promising growth potential due to the increasing integration of advanced driver-assistance systems (ADAS).

- North America: Strong technological innovation, high consumer spending.

- Asia-Pacific: Rapid economic growth, increasing smartphone penetration.

- Europe: Stable growth, driven by demand from various sectors.

- Dedicated Graphics Cards: High performance drives market dominance.

- On-Premise Deployments: Maintaining dominance but facing challenges from cloud deployments.

- Smartphones & Gaming PCs: Largest application segments.

Graphic Processor Industry Product Landscape

The graphic processor market features a wide range of products, from entry-level integrated graphics solutions to high-end dedicated graphics cards with advanced features like ray tracing and AI acceleration. Key innovations include advancements in GPU architecture (e.g., increased cores, higher clock speeds), memory technologies (GDDR6X), and power efficiency improvements. Unique selling propositions (USPs) focus on enhanced performance, low power consumption, and specialized features tailored to specific applications. For example, GPUs designed for AI inference tasks excel in specific algorithms.

Key Drivers, Barriers & Challenges in Graphic Processor Industry

Key Drivers:

- Technological advancements in GPU architecture and memory technologies.

- Rising demand for high-performance computing in various sectors (AI, data centers, gaming).

- Growing adoption of smartphones and gaming PCs with advanced graphics capabilities.

Key Challenges:

- Supply chain disruptions affecting the availability of key components (e.g., semiconductors). This has a quantifiable impact, delaying product launches and increasing costs by an estimated xx%.

- High development costs and long lead times for new GPU designs.

- Intense competition among major players, leading to price pressures.

Emerging Opportunities in Graphic Processor Industry

- Expansion into untapped markets such as augmented reality (AR) and virtual reality (VR).

- Development of specialized GPUs for emerging applications, such as autonomous driving and edge computing.

- Growing demand for high-performance computing in cloud-based environments.

Growth Accelerators in the Graphic Processor Industry

Technological breakthroughs, particularly in areas like high-bandwidth memory and advanced rendering techniques, are key growth catalysts. Strategic partnerships between GPU manufacturers and software developers are creating synergistic opportunities. Expanding market penetration into emerging applications, such as the metaverse, is another key accelerator.

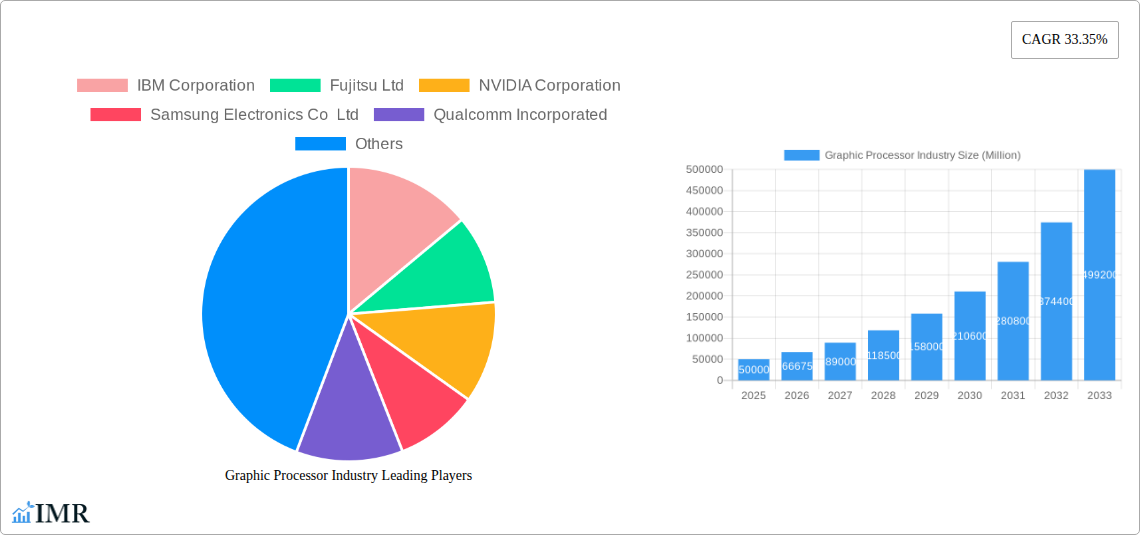

Key Players Shaping the Graphic Processor Industry Market

- IBM Corporation

- Fujitsu Ltd

- NVIDIA Corporation

- Samsung Electronics Co Ltd

- Qualcomm Incorporated

- Advanced Micro Devices Inc

- Taiwan Semiconductor Manufacturing Company Ltd

- Intel Corporation

- Sony Corporation

- Apple Inc *List Not Exhaustive

Notable Milestones in Graphic Processor Industry Sector

- July 2022: Samsung Electronics launched the first 16-gigabit (Gb) GDDR6 DRAM with processing speeds of 24 Gbps, significantly improving graphics performance for next-generation devices.

- November 2022: Qualcomm launched the Snapdragon 8 Gen 2 mobile platform with enhanced Snapdragon Elite Gaming capabilities, including real-time hardware-accelerated ray tracing.

In-Depth Graphic Processor Industry Market Outlook

The graphic processor market is poised for sustained growth, driven by continued technological advancements and increasing demand across diverse applications. Future market potential lies in emerging areas such as artificial intelligence, high-performance computing, and the metaverse. Strategic opportunities include developing specialized GPUs for niche applications and fostering strategic partnerships to expand market reach and accelerate innovation. The market is expected to witness significant expansion in the coming years, providing lucrative opportunities for both established players and new entrants.

Graphic Processor Industry Segmentation

-

1. Type

- 1.1. Dedicated Graphics Card

- 1.2. Integrated Graphics Solutions

- 1.3. Hybrid Solutions

-

2. Deployement

- 2.1. On-premise

- 2.2. Cloud

-

3. Applications

- 3.1. Smartphones

- 3.2. Tablets and Notebooks

- 3.3. Workstations

- 3.4. Gaming PC

- 3.5. Media and Entertainment

- 3.6. Automotives

Graphic Processor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Graphic Processor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 33.35% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Graphic Applications; Rise of Geographic Information Systems (GIS) and Immersive Multimedia

- 3.3. Market Restrains

- 3.3.1. Declining Workstation Sales

- 3.4. Market Trends

- 3.4.1. Gaming Industry to Augment Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Dedicated Graphics Card

- 5.1.2. Integrated Graphics Solutions

- 5.1.3. Hybrid Solutions

- 5.2. Market Analysis, Insights and Forecast - by Deployement

- 5.2.1. On-premise

- 5.2.2. Cloud

- 5.3. Market Analysis, Insights and Forecast - by Applications

- 5.3.1. Smartphones

- 5.3.2. Tablets and Notebooks

- 5.3.3. Workstations

- 5.3.4. Gaming PC

- 5.3.5. Media and Entertainment

- 5.3.6. Automotives

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Dedicated Graphics Card

- 6.1.2. Integrated Graphics Solutions

- 6.1.3. Hybrid Solutions

- 6.2. Market Analysis, Insights and Forecast - by Deployement

- 6.2.1. On-premise

- 6.2.2. Cloud

- 6.3. Market Analysis, Insights and Forecast - by Applications

- 6.3.1. Smartphones

- 6.3.2. Tablets and Notebooks

- 6.3.3. Workstations

- 6.3.4. Gaming PC

- 6.3.5. Media and Entertainment

- 6.3.6. Automotives

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Dedicated Graphics Card

- 7.1.2. Integrated Graphics Solutions

- 7.1.3. Hybrid Solutions

- 7.2. Market Analysis, Insights and Forecast - by Deployement

- 7.2.1. On-premise

- 7.2.2. Cloud

- 7.3. Market Analysis, Insights and Forecast - by Applications

- 7.3.1. Smartphones

- 7.3.2. Tablets and Notebooks

- 7.3.3. Workstations

- 7.3.4. Gaming PC

- 7.3.5. Media and Entertainment

- 7.3.6. Automotives

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Dedicated Graphics Card

- 8.1.2. Integrated Graphics Solutions

- 8.1.3. Hybrid Solutions

- 8.2. Market Analysis, Insights and Forecast - by Deployement

- 8.2.1. On-premise

- 8.2.2. Cloud

- 8.3. Market Analysis, Insights and Forecast - by Applications

- 8.3.1. Smartphones

- 8.3.2. Tablets and Notebooks

- 8.3.3. Workstations

- 8.3.4. Gaming PC

- 8.3.5. Media and Entertainment

- 8.3.6. Automotives

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Latin America Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Dedicated Graphics Card

- 9.1.2. Integrated Graphics Solutions

- 9.1.3. Hybrid Solutions

- 9.2. Market Analysis, Insights and Forecast - by Deployement

- 9.2.1. On-premise

- 9.2.2. Cloud

- 9.3. Market Analysis, Insights and Forecast - by Applications

- 9.3.1. Smartphones

- 9.3.2. Tablets and Notebooks

- 9.3.3. Workstations

- 9.3.4. Gaming PC

- 9.3.5. Media and Entertainment

- 9.3.6. Automotives

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Dedicated Graphics Card

- 10.1.2. Integrated Graphics Solutions

- 10.1.3. Hybrid Solutions

- 10.2. Market Analysis, Insights and Forecast - by Deployement

- 10.2.1. On-premise

- 10.2.2. Cloud

- 10.3. Market Analysis, Insights and Forecast - by Applications

- 10.3.1. Smartphones

- 10.3.2. Tablets and Notebooks

- 10.3.3. Workstations

- 10.3.4. Gaming PC

- 10.3.5. Media and Entertainment

- 10.3.6. Automotives

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. North America Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Asia Pacific Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Latin America Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Middle East and Africa Graphic Processor Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 IBM Corporation

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Fujitsu Ltd

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 NVIDIA Corporation

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Samsung Electronics Co Ltd

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Qualcomm Incorporated

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Advanced Micro Devices Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Taiwan Semiconductor Manufacturing Company Ltd

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Intel Corporation

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Sony Corporation

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Apple Inc *List Not Exhaustive

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 IBM Corporation

List of Figures

- Figure 1: Global Graphic Processor Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Graphic Processor Industry Revenue (Million), by Type 2024 & 2032

- Figure 13: North America Graphic Processor Industry Revenue Share (%), by Type 2024 & 2032

- Figure 14: North America Graphic Processor Industry Revenue (Million), by Deployement 2024 & 2032

- Figure 15: North America Graphic Processor Industry Revenue Share (%), by Deployement 2024 & 2032

- Figure 16: North America Graphic Processor Industry Revenue (Million), by Applications 2024 & 2032

- Figure 17: North America Graphic Processor Industry Revenue Share (%), by Applications 2024 & 2032

- Figure 18: North America Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: North America Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Europe Graphic Processor Industry Revenue (Million), by Type 2024 & 2032

- Figure 21: Europe Graphic Processor Industry Revenue Share (%), by Type 2024 & 2032

- Figure 22: Europe Graphic Processor Industry Revenue (Million), by Deployement 2024 & 2032

- Figure 23: Europe Graphic Processor Industry Revenue Share (%), by Deployement 2024 & 2032

- Figure 24: Europe Graphic Processor Industry Revenue (Million), by Applications 2024 & 2032

- Figure 25: Europe Graphic Processor Industry Revenue Share (%), by Applications 2024 & 2032

- Figure 26: Europe Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Europe Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Asia Pacific Graphic Processor Industry Revenue (Million), by Type 2024 & 2032

- Figure 29: Asia Pacific Graphic Processor Industry Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Graphic Processor Industry Revenue (Million), by Deployement 2024 & 2032

- Figure 31: Asia Pacific Graphic Processor Industry Revenue Share (%), by Deployement 2024 & 2032

- Figure 32: Asia Pacific Graphic Processor Industry Revenue (Million), by Applications 2024 & 2032

- Figure 33: Asia Pacific Graphic Processor Industry Revenue Share (%), by Applications 2024 & 2032

- Figure 34: Asia Pacific Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Asia Pacific Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Latin America Graphic Processor Industry Revenue (Million), by Type 2024 & 2032

- Figure 37: Latin America Graphic Processor Industry Revenue Share (%), by Type 2024 & 2032

- Figure 38: Latin America Graphic Processor Industry Revenue (Million), by Deployement 2024 & 2032

- Figure 39: Latin America Graphic Processor Industry Revenue Share (%), by Deployement 2024 & 2032

- Figure 40: Latin America Graphic Processor Industry Revenue (Million), by Applications 2024 & 2032

- Figure 41: Latin America Graphic Processor Industry Revenue Share (%), by Applications 2024 & 2032

- Figure 42: Latin America Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 43: Latin America Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 44: Middle East and Africa Graphic Processor Industry Revenue (Million), by Type 2024 & 2032

- Figure 45: Middle East and Africa Graphic Processor Industry Revenue Share (%), by Type 2024 & 2032

- Figure 46: Middle East and Africa Graphic Processor Industry Revenue (Million), by Deployement 2024 & 2032

- Figure 47: Middle East and Africa Graphic Processor Industry Revenue Share (%), by Deployement 2024 & 2032

- Figure 48: Middle East and Africa Graphic Processor Industry Revenue (Million), by Applications 2024 & 2032

- Figure 49: Middle East and Africa Graphic Processor Industry Revenue Share (%), by Applications 2024 & 2032

- Figure 50: Middle East and Africa Graphic Processor Industry Revenue (Million), by Country 2024 & 2032

- Figure 51: Middle East and Africa Graphic Processor Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Graphic Processor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Graphic Processor Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Global Graphic Processor Industry Revenue Million Forecast, by Deployement 2019 & 2032

- Table 4: Global Graphic Processor Industry Revenue Million Forecast, by Applications 2019 & 2032

- Table 5: Global Graphic Processor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Graphic Processor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Graphic Processor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Graphic Processor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: Graphic Processor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: Graphic Processor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Graphic Processor Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 17: Global Graphic Processor Industry Revenue Million Forecast, by Deployement 2019 & 2032

- Table 18: Global Graphic Processor Industry Revenue Million Forecast, by Applications 2019 & 2032

- Table 19: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Global Graphic Processor Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 21: Global Graphic Processor Industry Revenue Million Forecast, by Deployement 2019 & 2032

- Table 22: Global Graphic Processor Industry Revenue Million Forecast, by Applications 2019 & 2032

- Table 23: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Global Graphic Processor Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 25: Global Graphic Processor Industry Revenue Million Forecast, by Deployement 2019 & 2032

- Table 26: Global Graphic Processor Industry Revenue Million Forecast, by Applications 2019 & 2032

- Table 27: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Global Graphic Processor Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 29: Global Graphic Processor Industry Revenue Million Forecast, by Deployement 2019 & 2032

- Table 30: Global Graphic Processor Industry Revenue Million Forecast, by Applications 2019 & 2032

- Table 31: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: Global Graphic Processor Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 33: Global Graphic Processor Industry Revenue Million Forecast, by Deployement 2019 & 2032

- Table 34: Global Graphic Processor Industry Revenue Million Forecast, by Applications 2019 & 2032

- Table 35: Global Graphic Processor Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Graphic Processor Industry?

The projected CAGR is approximately 33.35%.

2. Which companies are prominent players in the Graphic Processor Industry?

Key companies in the market include IBM Corporation, Fujitsu Ltd, NVIDIA Corporation, Samsung Electronics Co Ltd, Qualcomm Incorporated, Advanced Micro Devices Inc, Taiwan Semiconductor Manufacturing Company Ltd, Intel Corporation, Sony Corporation, Apple Inc *List Not Exhaustive.

3. What are the main segments of the Graphic Processor Industry?

The market segments include Type, Deployement, Applications.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Graphic Applications; Rise of Geographic Information Systems (GIS) and Immersive Multimedia.

6. What are the notable trends driving market growth?

Gaming Industry to Augment Market Growth.

7. Are there any restraints impacting market growth?

Declining Workstation Sales.

8. Can you provide examples of recent developments in the market?

July 2022: The first 16-gigabit (Gb) Graphics Double Data Rate 6 (GDDR6) DRAM with processing speeds of 24 gigabits per second (Gbps) was launched by Samsung Electronics. The new memory, which is built using extreme ultraviolet (EUV) technology and Samsung's third-generation 10-nanometer-class (1z) process, is intended to significantly improve graphics performance for next-generation graphics cards (Video Graphics Arrays), laptops, game consoles, artificial intelligence-based applications, and high-performance computing (HPC) systems.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Graphic Processor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Graphic Processor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Graphic Processor Industry?

To stay informed about further developments, trends, and reports in the Graphic Processor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence