Key Insights

The Canada data center construction market is experiencing robust growth, driven by increasing digitalization, the expanding adoption of cloud computing, and the burgeoning need for robust IT infrastructure across various sectors. The market's Compound Annual Growth Rate (CAGR) of 8.94% from 2019 to 2024 suggests a significant expansion, projected to continue through 2033. Key drivers include the growing demand for data storage and processing capabilities from sectors like IT & Telecommunications, BFSI (Banking, Financial Services, and Insurance), and the government. Furthermore, the increasing reliance on edge computing and the need for geographically dispersed data centers to reduce latency are fueling market expansion. While specific market size data for 2025 isn't provided, estimating from the CAGR and assuming a base year of 2024, we can project a substantial market value in the hundreds of millions of Canadian dollars for 2025. The market is segmented by infrastructure type (electrical, mechanical, and other) and end-user sectors, allowing for tailored investment strategies and business development within specific niches. Challenges could include the high initial capital investment required for data center construction, stringent regulatory compliance, and the need for skilled labor. Nevertheless, the long-term prospects remain positive, given Canada's growing economy and strategic location for North American data center operations.

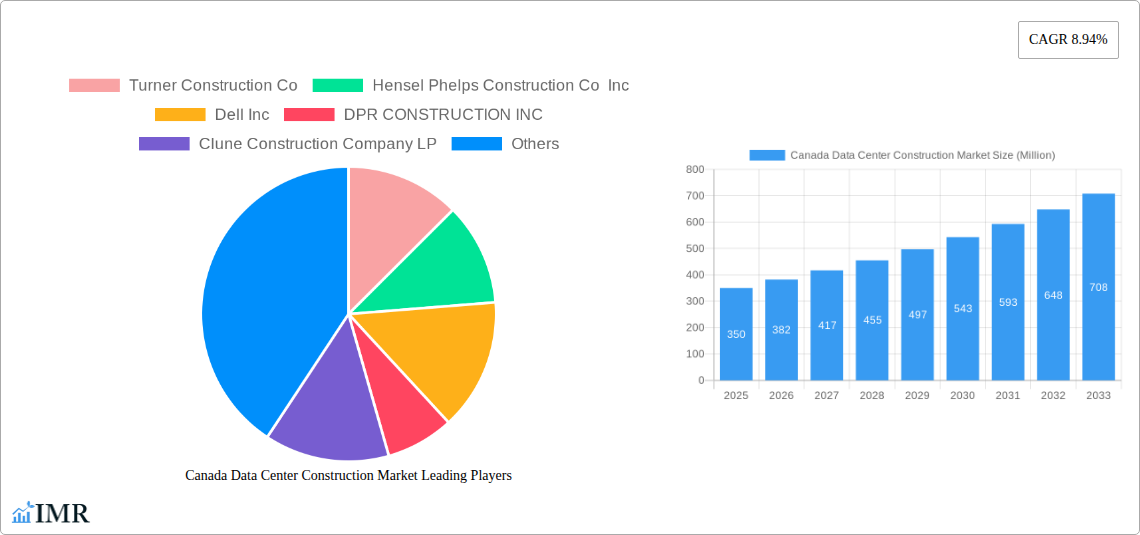

The competitive landscape is characterized by a mix of large multinational corporations, such as IBM, Dell, and Schneider Electric, alongside regional construction firms like Turner Construction and Hensel Phelps. These companies are actively engaged in securing projects and developing innovative data center solutions. Regional variations exist within Canada, with Eastern, Western, and Central Canada all contributing to the overall market growth. However, the distribution of market share among these regions might be influenced by factors such as population density, economic activity, and existing infrastructure development. The forecast period of 2025-2033 presents significant opportunities for market players, particularly those capable of offering sustainable and energy-efficient data center designs in response to growing environmental concerns. Further research into specific regional demands and technological advancements will be crucial to accurately predict the future market trajectory.

Canada Data Center Construction Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Canada data center construction market, encompassing market dynamics, growth trends, key players, and future outlook. With a focus on both parent and child markets (infrastructure and end-user segments), this report is essential for investors, industry professionals, and anyone seeking to understand this rapidly evolving sector. The study period covers 2019-2033, with 2025 as the base and estimated year.

Canada Data Center Construction Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory influences, and market trends within the Canadian data center construction market. The market is characterized by a moderately concentrated structure, with several major players holding significant market share. However, smaller, specialized firms also play a vital role, particularly in niche areas.

Market Concentration: The top five players (Turner Construction Co, Hensel Phelps Construction Co Inc, DPR CONSTRUCTION INC, AECOM, and IBM Corporation) account for approximately xx% of the market share in 2024. This indicates a competitive, yet not overly consolidated market.

Technological Innovation: Drivers include the increasing adoption of sustainable technologies (e.g., green data centers), advanced cooling systems, and prefabricated modular data center solutions. Barriers include high initial investment costs for new technologies and the need for skilled labor.

Regulatory Framework: Government policies promoting digital infrastructure development and investments in renewable energy significantly impact market growth. However, navigating complex building codes and environmental regulations can present challenges.

Competitive Substitutes: The main competitive substitute is the use of cloud services, which reduces the demand for on-premises data centers. However, specific industry requirements often necessitate on-premise solutions.

End-User Demographics: The IT & Telecommunication sector is the largest end-user segment, followed by BFSI and Government, exhibiting steady growth.

M&A Trends: The number of M&A deals in the Canadian data center construction market averaged xx per year between 2019 and 2024, indicating a moderate level of consolidation. These deals primarily focus on expanding service offerings and geographical reach.

Canada Data Center Construction Market Growth Trends & Insights

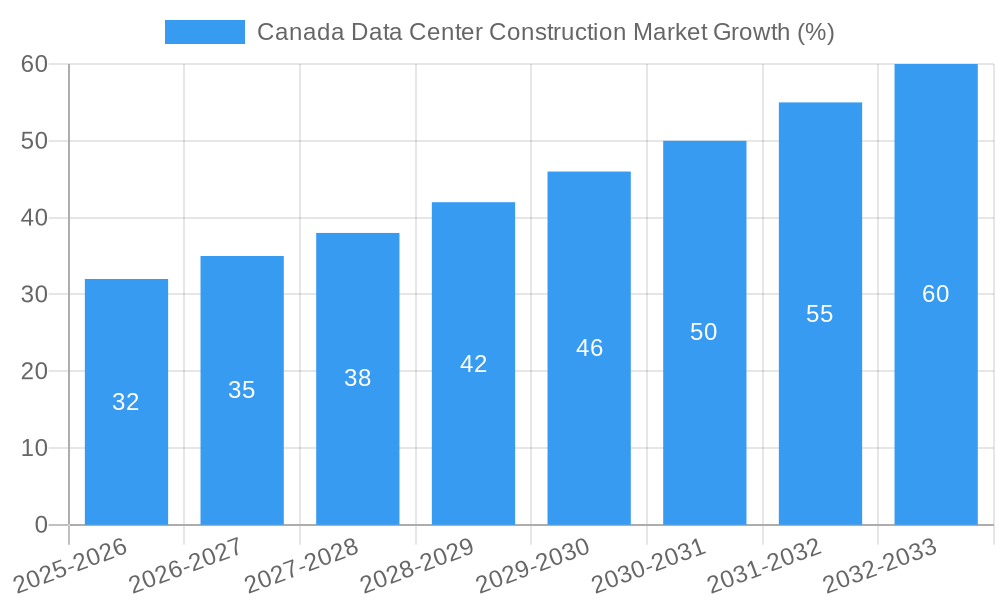

The Canada data center construction market witnessed significant growth between 2019 and 2024, driven primarily by increasing data consumption, the expansion of cloud computing services, and government initiatives to enhance digital infrastructure. The market size expanded from xx Million in 2019 to xx Million in 2024, achieving a CAGR of xx%. This growth trajectory is projected to continue throughout the forecast period (2025-2033), with the market expected to reach xx Million by 2033, driven by factors such as the rising adoption of 5G technology, the growing demand for edge computing, and the increasing need for robust cybersecurity infrastructure. Technological disruptions, such as the widespread adoption of AI and IoT, are further fueling the demand for advanced data center facilities. Furthermore, shifts in consumer behavior towards digital services are driving the expansion of e-commerce and streaming platforms, consequently boosting the demand for data center capacity. Market penetration of advanced technologies like AI-powered monitoring systems is expected to increase from xx% in 2024 to xx% by 2033.

Dominant Regions, Countries, or Segments in Canada Data Center Construction Market

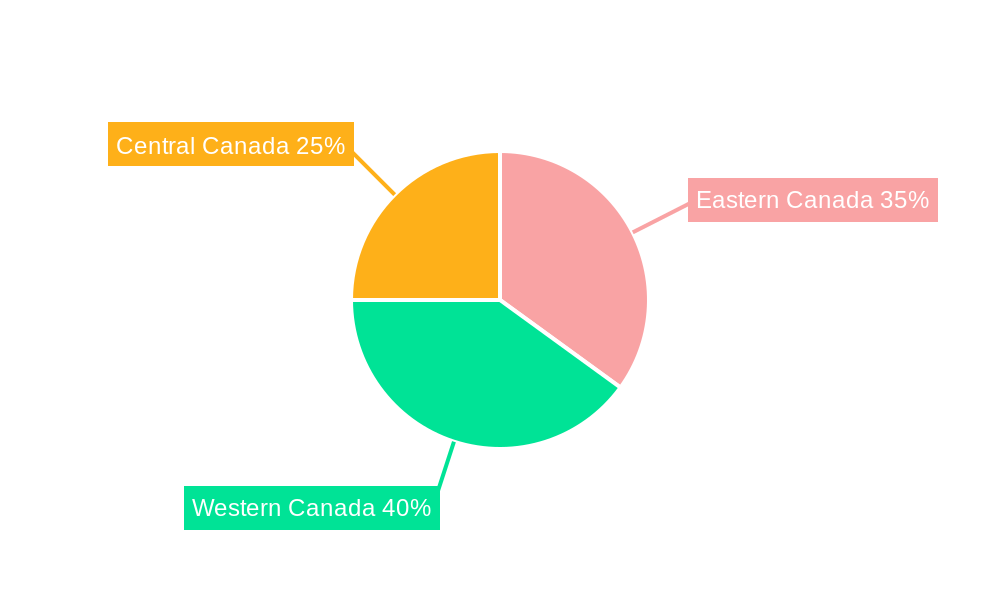

The Ontario and Quebec regions are currently dominating the Canadian data center construction market, driven by high concentrations of IT companies and robust digital infrastructure investments. Within infrastructure segments, Electrical Infrastructure consistently holds the largest market share due to the significant energy requirements of data centers. The IT & Telecommunication sector remains the most significant end-user segment, exhibiting a substantial market share and growth potential.

Key Drivers:

- Strong Government Support: Federal and provincial government initiatives promoting digital transformation and investment in advanced technologies.

- Robust IT Sector: A thriving IT sector, particularly in Ontario and Quebec, driving demand for data center capacity.

- Strategic Location: Canada’s geographical location provides benefits for connectivity and low latency to key markets.

- Favorable Regulatory Environment: Relatively streamlined regulatory processes for data center development compared to some other jurisdictions.

Dominance Factors:

- High Concentration of IT Companies: Major data centers are often co-located with significant IT and telecommunication companies.

- Existing Infrastructure: Existing fiber optic networks and power infrastructure reduce the costs associated with establishing new data centers.

- Skilled Workforce: Availability of a skilled workforce in the IT and construction sectors.

Canada Data Center Construction Market Product Landscape

The Canadian data center construction market showcases a diverse range of products, encompassing various building designs, cooling solutions, and power systems. Innovations focus on modular designs, prefabrication techniques, and energy-efficient technologies to reduce costs, construction time, and environmental impact. Key performance metrics include power usage effectiveness (PUE), mean time between failures (MTBF), and uptime. Unique selling propositions include features like enhanced security, flexible scalability, and sustainable design elements.

Key Drivers, Barriers & Challenges in Canada Data Center Construction Market

Key Drivers:

The escalating demand for data storage and processing capabilities, fueled by the expanding cloud computing and digital transformation initiatives, is the primary driver. Government incentives aimed at fostering technological advancements and investments in digital infrastructure further accelerate the growth. The need for robust cybersecurity measures and reliable infrastructure to support critical national services also propels market expansion.

Key Challenges & Restraints:

- Supply Chain Disruptions: Global supply chain disruptions impacting the timely procurement of essential components and materials for data center construction, leading to delays and increased costs. This resulted in a xx% increase in project completion times in 2024.

- Skilled Labor Shortages: A shortage of skilled labor in the construction and IT sectors hindering the timely completion of data center projects.

- High Energy Costs: High energy costs, particularly in certain provinces, pose a significant challenge to the profitability of data center operations.

- Regulatory Complexity: Navigating intricate building codes and environmental regulations adds to project complexity and delays.

Emerging Opportunities in Canada Data Center Construction Market

The rise of edge computing presents a significant opportunity. This involves building smaller data centers closer to end-users to reduce latency and improve performance for applications like IoT and 5G. There's also growing demand for sustainable data centers, leading to opportunities for green building technologies and renewable energy solutions.

Growth Accelerators in the Canada Data Center Construction Market Industry

Strategic partnerships between technology providers and construction companies, combined with technological breakthroughs in energy-efficient cooling and prefabricated modular data centers, are fueling growth. Expansion into underserved regions and increased investment in cybersecurity measures are also key accelerators.

Key Players Shaping the Canada Data Center Construction Market Market

- Turner Construction Co

- Hensel Phelps Construction Co Inc

- Dell Inc

- DPR CONSTRUCTION INC

- Clune Construction Company LP

- IBM Corporation

- Holder Construction Company

- Nabholz Construction Corporation

- Rittal GMBH & Co KG

- AECOM

- HITT Contrating Inc

- Hewlett Packard Enterprise (HPE)

- Fortis ConstructionInc

- Schneider Electric SE

Notable Milestones in Canada Data Center Construction Market Sector

- June 2022: Cologix partners with Console Connect, expanding interconnection capabilities in Toronto.

- May 2022: NetIX and eStruxture collaborate to offer enhanced global connectivity solutions in Canada.

In-Depth Canada Data Center Construction Market Market Outlook

The Canada data center construction market is poised for sustained growth, driven by ongoing digital transformation, government support, and the adoption of new technologies. Strategic investments in sustainable and resilient infrastructure will be crucial for long-term success. Companies that can adapt to evolving technological demands and overcome supply chain challenges will be best positioned to capture significant market share.

Canada Data Center Construction Market Segmentation

-

1. Infrastructure

-

1.1. By Electrical Infrastructure

-

1.1.1. Power Distribution Solution

- 1.1.1.1. PDU - Ba

-

1.1.1.2. Transfer Switches

- 1.1.1.2.1. Static

- 1.1.1.2.2. Automatic (ATS)

-

1.1.1.3. Switchgear

- 1.1.1.3.1. Low-voltage

- 1.1.1.3.2. Medium-voltage

- 1.1.1.4. Power Panels and Components

- 1.1.1.5. Others

-

1.1.2. Power Back-up Solutions

- 1.1.2.1. UPS

- 1.1.2.2. Generators

- 1.1.3. Service

-

1.1.1. Power Distribution Solution

-

1.2. By Mechanical Infrastructure

-

1.2.1. Cooling Systems

- 1.2.1.1. Immersion Cooling

- 1.2.1.2. Direct-to-Chip Cooling

- 1.2.1.3. Rear Door Heat Exchanger

- 1.2.1.4. In-row and In-rack Cooling

- 1.2.2. Racks

- 1.2.3. Other Mechanical Infrastructure

-

1.2.1. Cooling Systems

- 1.3. General Construction

-

1.1. By Electrical Infrastructure

-

2. Tier Type

- 2.1. Tier 1 and 2

- 2.2. Tier 3

- 2.3. Tier 4

-

3. End User

- 3.1. Banking, Financial Services, and Insurance

- 3.2. IT and Telecommunications

- 3.3. Government and Defense

- 3.4. Healthcare

- 3.5. Other End Users

Canada Data Center Construction Market Segmentation By Geography

- 1. Canada

Canada Data Center Construction Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.94% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 9.1 Growing Cloud Applications

- 3.2.2 AI

- 3.2.3 and Big Data9.2 Growing Adoption of Hyperscale Data Centers in Large Enterprises9.3 Advent Green Data Center

- 3.3. Market Restrains

- 3.3.1 10.1 High CaPex

- 3.3.2 OpEx & TCO for building Data Center

- 3.4. Market Trends

- 3.4.1. BFSI to hold major market share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Data Center Construction Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Infrastructure

- 5.1.1. By Electrical Infrastructure

- 5.1.1.1. Power Distribution Solution

- 5.1.1.1.1. PDU - Ba

- 5.1.1.1.2. Transfer Switches

- 5.1.1.1.2.1. Static

- 5.1.1.1.2.2. Automatic (ATS)

- 5.1.1.1.3. Switchgear

- 5.1.1.1.3.1. Low-voltage

- 5.1.1.1.3.2. Medium-voltage

- 5.1.1.1.4. Power Panels and Components

- 5.1.1.1.5. Others

- 5.1.1.2. Power Back-up Solutions

- 5.1.1.2.1. UPS

- 5.1.1.2.2. Generators

- 5.1.1.3. Service

- 5.1.1.1. Power Distribution Solution

- 5.1.2. By Mechanical Infrastructure

- 5.1.2.1. Cooling Systems

- 5.1.2.1.1. Immersion Cooling

- 5.1.2.1.2. Direct-to-Chip Cooling

- 5.1.2.1.3. Rear Door Heat Exchanger

- 5.1.2.1.4. In-row and In-rack Cooling

- 5.1.2.2. Racks

- 5.1.2.3. Other Mechanical Infrastructure

- 5.1.2.1. Cooling Systems

- 5.1.3. General Construction

- 5.1.1. By Electrical Infrastructure

- 5.2. Market Analysis, Insights and Forecast - by Tier Type

- 5.2.1. Tier 1 and 2

- 5.2.2. Tier 3

- 5.2.3. Tier 4

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Banking, Financial Services, and Insurance

- 5.3.2. IT and Telecommunications

- 5.3.3. Government and Defense

- 5.3.4. Healthcare

- 5.3.5. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Infrastructure

- 6. Eastern Canada Canada Data Center Construction Market Analysis, Insights and Forecast, 2019-2031

- 7. Western Canada Canada Data Center Construction Market Analysis, Insights and Forecast, 2019-2031

- 8. Central Canada Canada Data Center Construction Market Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 Turner Construction Co

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 Hensel Phelps Construction Co Inc

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Dell Inc

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 DPR CONSTRUCTION INC

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 Clune Construction Company LP

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 IBM Corporation

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 Holder Construction Company

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Nabholz Construction Corporation

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Rittal GMBH & Co KG

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 AECOM

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.11 HITT Contrating Inc

- 9.2.11.1. Overview

- 9.2.11.2. Products

- 9.2.11.3. SWOT Analysis

- 9.2.11.4. Recent Developments

- 9.2.11.5. Financials (Based on Availability)

- 9.2.12 Hewlett Packard Enterprise (HPE)

- 9.2.12.1. Overview

- 9.2.12.2. Products

- 9.2.12.3. SWOT Analysis

- 9.2.12.4. Recent Developments

- 9.2.12.5. Financials (Based on Availability)

- 9.2.13 Fortis ConstructionInc

- 9.2.13.1. Overview

- 9.2.13.2. Products

- 9.2.13.3. SWOT Analysis

- 9.2.13.4. Recent Developments

- 9.2.13.5. Financials (Based on Availability)

- 9.2.14 Schneider Electric SE

- 9.2.14.1. Overview

- 9.2.14.2. Products

- 9.2.14.3. SWOT Analysis

- 9.2.14.4. Recent Developments

- 9.2.14.5. Financials (Based on Availability)

- 9.2.1 Turner Construction Co

List of Figures

- Figure 1: Canada Data Center Construction Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Canada Data Center Construction Market Share (%) by Company 2024

List of Tables

- Table 1: Canada Data Center Construction Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Canada Data Center Construction Market Revenue Million Forecast, by Infrastructure 2019 & 2032

- Table 3: Canada Data Center Construction Market Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 4: Canada Data Center Construction Market Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Canada Data Center Construction Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Canada Data Center Construction Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Eastern Canada Canada Data Center Construction Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Western Canada Canada Data Center Construction Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Central Canada Canada Data Center Construction Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Canada Data Center Construction Market Revenue Million Forecast, by Infrastructure 2019 & 2032

- Table 11: Canada Data Center Construction Market Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 12: Canada Data Center Construction Market Revenue Million Forecast, by End User 2019 & 2032

- Table 13: Canada Data Center Construction Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Data Center Construction Market?

The projected CAGR is approximately 8.94%.

2. Which companies are prominent players in the Canada Data Center Construction Market?

Key companies in the market include Turner Construction Co, Hensel Phelps Construction Co Inc, Dell Inc, DPR CONSTRUCTION INC, Clune Construction Company LP, IBM Corporation, Holder Construction Company, Nabholz Construction Corporation, Rittal GMBH & Co KG, AECOM, HITT Contrating Inc, Hewlett Packard Enterprise (HPE), Fortis ConstructionInc, Schneider Electric SE.

3. What are the main segments of the Canada Data Center Construction Market?

The market segments include Infrastructure, Tier Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

9.1 Growing Cloud Applications. AI. and Big Data9.2 Growing Adoption of Hyperscale Data Centers in Large Enterprises9.3 Advent Green Data Center.

6. What are the notable trends driving market growth?

BFSI to hold major market share.

7. Are there any restraints impacting market growth?

10.1 High CaPex. OpEx & TCO for building Data Center.

8. Can you provide examples of recent developments in the market?

June 2022: Cologix announced its continued strategic partnership with Console Connect by PCCW Global by deploying the Console Connect Software-Defined Interconnection platform at Cologix's TOR1 data center in Toronto-this marked Console Connect's second PoP within Cologix's Canadian market and interconnection ecosystem. The first was available in December 2021 at Cologix's MTL7 data center in Montréal.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Data Center Construction Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Data Center Construction Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Data Center Construction Market?

To stay informed about further developments, trends, and reports in the Canada Data Center Construction Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence