Key Insights

The ferroalloys market, encompassing crucial materials like ferrosilicon, ferromanganese, and ferrochrome, experienced robust growth between 2019 and 2024, driven primarily by the burgeoning steel industry. Steel production, a major consumer of ferroalloys, witnessed significant expansion globally during this period, fueled by infrastructure development, particularly in emerging economies. The rising demand for high-strength, low-alloy steels in automotive and construction sectors further amplified the ferroalloys market's trajectory. While precise market size figures for past years are not provided, considering the typical growth rates observed in related industrial sectors, a conservative estimate would place the market size around $50 billion in 2024. This growth is anticipated to continue, albeit at a moderated pace, through 2033.

Looking ahead, the market's growth from 2025 to 2033 will be influenced by several factors. Government initiatives promoting infrastructure development and sustainable construction practices in regions like Asia-Pacific and the Middle East will continue to stimulate demand. However, fluctuating raw material prices, especially for key components like manganese ore and chromium, pose a significant challenge. Furthermore, environmental regulations aimed at reducing carbon emissions from steel production could impact the production methods and costs associated with ferroalloys manufacturing. Therefore, while growth is projected, a realistic CAGR of 4% – 5% seems appropriate for the forecast period, leading to a market size of approximately $70 billion by 2033. Technological advancements leading to more efficient production processes and the exploration of alternative raw materials could also influence this growth trajectory.

Ferroalloys Industry Market Report: 2019-2033

This comprehensive report provides a deep dive into the global ferroalloys industry, analyzing market dynamics, growth trends, key players, and future prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for industry professionals, investors, and strategists seeking to understand and capitalize on the opportunities within this dynamic sector. The report covers parent markets like metals and mining and child markets such as steel, stainless steel, and the renewable energy sector.

Ferroalloys Industry Market Dynamics & Structure

The ferroalloys market is characterized by moderate concentration, with several large players holding significant market share. Technological innovation, driven by demand for higher-quality alloys and sustainable production methods, is a key driver. Stringent environmental regulations impact production processes and necessitate investment in cleaner technologies. The market faces competition from alternative materials and increasing prices of raw materials. End-user demographics are heavily influenced by the construction and automotive industries, along with the burgeoning renewable energy sector. M&A activity is moderate, driven by consolidation efforts and the pursuit of strategic advantages.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2024.

- Technological Innovation: Focus on improving alloy quality, reducing energy consumption, and enhancing environmental sustainability.

- Regulatory Framework: Stringent environmental regulations, varying by region, drive investment in cleaner technologies.

- Competitive Product Substitutes: Alternative materials are emerging, particularly in niche applications, posing a competitive threat.

- End-User Demographics: Primarily driven by steel, stainless steel, and increasingly renewable energy sectors.

- M&A Trends: Moderate activity, driven by vertical integration and expansion into new markets. Approximately xx M&A deals were recorded between 2019 and 2024, with a total value of xx Million.

Ferroalloys Industry Growth Trends & Insights

The ferroalloys market witnessed a compound annual growth rate (CAGR) of xx% during the historical period (2019-2024), reaching a market size of xx Million in 2024. This growth is primarily driven by increasing global steel production, particularly in developing economies. Technological advancements, including the use of advanced alloys in high-strength steels and the growing demand for ferroalloys in the renewable energy sector (solar and wind power), further accelerate market expansion. Shifting consumer preferences towards lightweight and high-performance materials in the automotive and aerospace sectors also contribute to market growth. The market penetration rate of advanced ferroalloys is expected to increase significantly by 2033. We project a CAGR of xx% from 2025-2033, with the market size reaching xx Million by 2033.

Dominant Regions, Countries, or Segments in Ferroalloys Industry

China continues to dominate the global ferroalloys market, holding the largest market share due to its vast steel production capacity and robust infrastructure. Other key regions include India, the European Union, and North America. Growth in these regions is driven by factors like economic expansion, infrastructural development, and government policies promoting industrial growth. However, the renewable energy sector is a rapidly growing segment driving demand for specific types of ferroalloys, especially in regions with ambitious climate targets.

- China: Dominant market share due to extensive steel production and robust infrastructure.

- India: Rapid economic growth and increasing steel demand fuel market expansion.

- European Union: Stringent environmental regulations drive innovation in sustainable ferroalloy production.

- North America: Significant demand from the automotive and construction sectors.

- Renewable Energy Sector: A rapidly growing segment driving demand for specialized ferroalloys.

Ferroalloys Industry Product Landscape

The ferroalloys market offers a diverse range of products, including ferrosilicon, ferromanganese, ferrochromium, and silicomanganese, each with unique applications and performance characteristics. Recent product innovations focus on enhancing alloy properties, such as improved strength, corrosion resistance, and weldability. These advancements cater to the growing demand for high-performance materials in various industries. Unique selling propositions often focus on customized alloy compositions to meet specific customer requirements and advanced production techniques that ensure high quality and consistency.

Key Drivers, Barriers & Challenges in Ferroalloys Industry

Key Drivers:

- Increasing global steel production.

- Growth of the renewable energy sector.

- Demand for high-performance materials in automotive and aerospace industries.

- Government support for infrastructure development.

Key Challenges & Restraints:

- Fluctuations in raw material prices (e.g., manganese ore, chromium ore).

- Stringent environmental regulations and the cost of compliance.

- Competition from alternative materials.

- Supply chain disruptions and geopolitical uncertainties. The impact of these disruptions on 2024 production is estimated to be around xx Million units.

Emerging Opportunities in Ferroalloys Industry

Emerging opportunities lie in the growing demand for ferroalloys in advanced applications, such as electric vehicles, energy storage systems, and high-speed rail. Untapped markets in developing economies and the increasing focus on sustainable production methods present further growth opportunities. Moreover, the development of innovative alloys with enhanced properties and tailored compositions will unlock new market segments.

Growth Accelerators in the Ferroalloys Industry

Long-term growth in the ferroalloys industry will be accelerated by technological breakthroughs in alloy production, leading to higher efficiency and lower costs. Strategic partnerships between ferroalloy producers and end-users will facilitate the development of specialized alloys tailored to specific applications. Expansion into new markets, particularly in developing economies, will further fuel market growth.

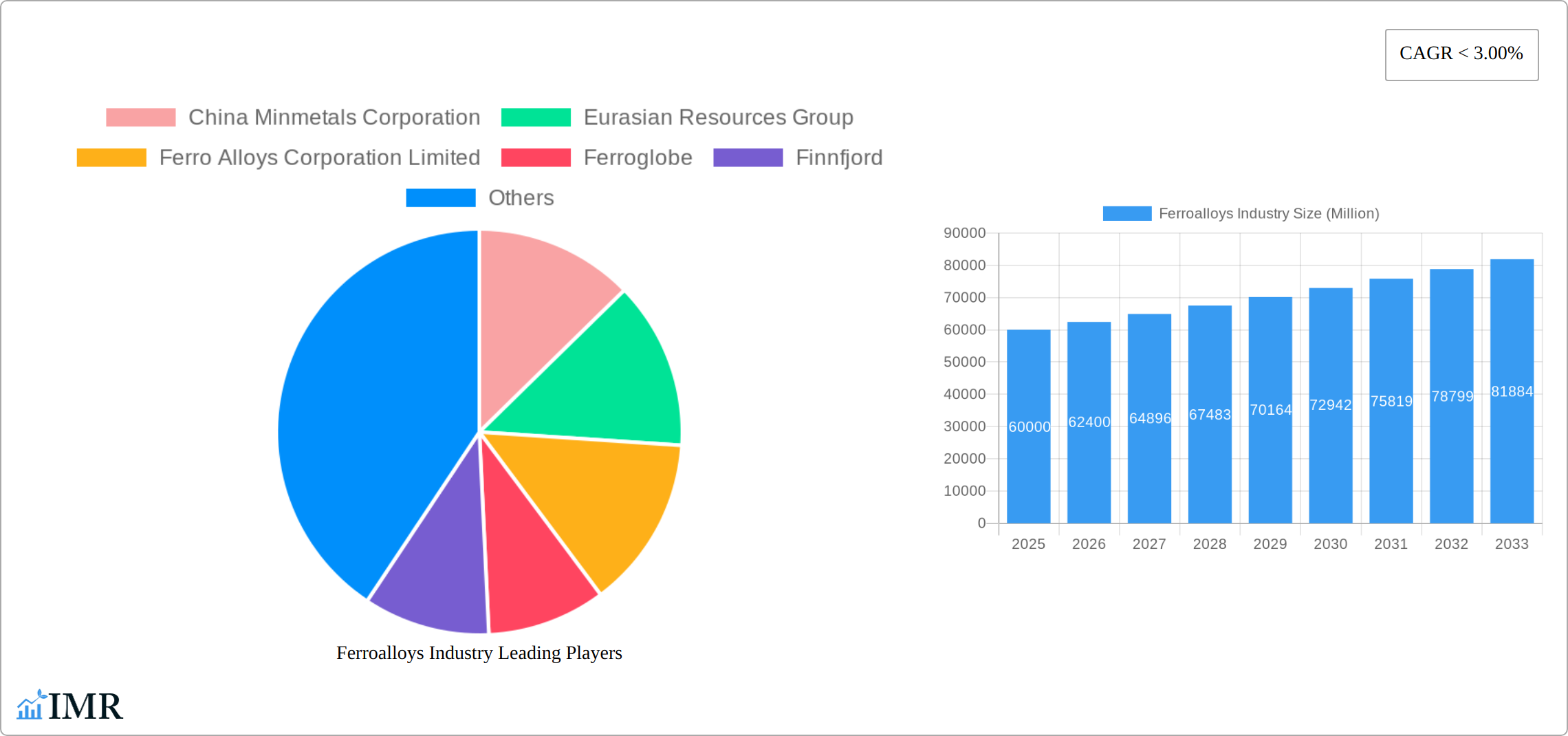

Key Players Shaping the Ferroalloys Industry Market

- China Minmetals Corporation

- Eurasian Resources Group

- Ferro Alloys Corporation Limited

- Ferroglobe

- Finnfjord

- Mechel

- OM Holdings Ltd

- Shanghai Shenjia Ferroalloys Co Ltd

- SKP Group

- Tashi Group

Notable Milestones in Ferroalloys Industry Sector

- July 2022: Ferroglobe PLC achieves high-purity (up to 99.995%) silicon metal powder production for batteries and advanced technologies. This signals a significant advancement in material science for energy storage solutions.

- June 2022: Ferroglobe PLC and REC Silicon sign an MOU to establish a low-carbon, traceable U.S.-based solar supply chain, signifying a move towards sustainable practices within the industry.

In-Depth Ferroalloys Industry Market Outlook

The ferroalloys market is poised for continued growth, driven by sustained demand from traditional sectors and the emergence of new applications in the renewable energy and advanced materials sectors. Strategic investments in research and development, coupled with sustainable production practices, will be crucial for long-term success. Opportunities for market expansion exist in developing economies and through strategic partnerships that enable the development of specialized alloys for niche applications. The market presents considerable potential for innovation and growth in the coming decade.

Ferroalloys Industry Segmentation

-

1. Application

- 1.1. Metallurgy

- 1.2. Semiconductors

- 1.3. Photovoltaic Solar Energy

- 1.4. Chemical Processing

- 1.5. Other Applications

Ferroalloys Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Ferroalloys Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of < 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries

- 3.3. Market Restrains

- 3.3.1. Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries

- 3.4. Market Trends

- 3.4.1. Growing Demand from Metallurgy Industry

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ferroalloys Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Metallurgy

- 5.1.2. Semiconductors

- 5.1.3. Photovoltaic Solar Energy

- 5.1.4. Chemical Processing

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.2.2. North America

- 5.2.3. Europe

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Asia Pacific Ferroalloys Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Metallurgy

- 6.1.2. Semiconductors

- 6.1.3. Photovoltaic Solar Energy

- 6.1.4. Chemical Processing

- 6.1.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Ferroalloys Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Metallurgy

- 7.1.2. Semiconductors

- 7.1.3. Photovoltaic Solar Energy

- 7.1.4. Chemical Processing

- 7.1.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ferroalloys Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Metallurgy

- 8.1.2. Semiconductors

- 8.1.3. Photovoltaic Solar Energy

- 8.1.4. Chemical Processing

- 8.1.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. South America Ferroalloys Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Metallurgy

- 9.1.2. Semiconductors

- 9.1.3. Photovoltaic Solar Energy

- 9.1.4. Chemical Processing

- 9.1.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East and Africa Ferroalloys Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Metallurgy

- 10.1.2. Semiconductors

- 10.1.3. Photovoltaic Solar Energy

- 10.1.4. Chemical Processing

- 10.1.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 China Minmetals Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Eurasian Resources Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Ferro Alloys Corporation Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Ferroglobe

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Finnfjord

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Mechel

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 OM Holdings Ltd

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Shanghai Shenjia Ferroalloys Co Ltd

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 SKP Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tashi Group*List Not Exhaustive

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 China Minmetals Corporation

List of Figures

- Figure 1: Global Ferroalloys Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Asia Pacific Ferroalloys Industry Revenue (Million), by Application 2024 & 2032

- Figure 3: Asia Pacific Ferroalloys Industry Revenue Share (%), by Application 2024 & 2032

- Figure 4: Asia Pacific Ferroalloys Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Asia Pacific Ferroalloys Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: North America Ferroalloys Industry Revenue (Million), by Application 2024 & 2032

- Figure 7: North America Ferroalloys Industry Revenue Share (%), by Application 2024 & 2032

- Figure 8: North America Ferroalloys Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: North America Ferroalloys Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Europe Ferroalloys Industry Revenue (Million), by Application 2024 & 2032

- Figure 11: Europe Ferroalloys Industry Revenue Share (%), by Application 2024 & 2032

- Figure 12: Europe Ferroalloys Industry Revenue (Million), by Country 2024 & 2032

- Figure 13: Europe Ferroalloys Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: South America Ferroalloys Industry Revenue (Million), by Application 2024 & 2032

- Figure 15: South America Ferroalloys Industry Revenue Share (%), by Application 2024 & 2032

- Figure 16: South America Ferroalloys Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: South America Ferroalloys Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Middle East and Africa Ferroalloys Industry Revenue (Million), by Application 2024 & 2032

- Figure 19: Middle East and Africa Ferroalloys Industry Revenue Share (%), by Application 2024 & 2032

- Figure 20: Middle East and Africa Ferroalloys Industry Revenue (Million), by Country 2024 & 2032

- Figure 21: Middle East and Africa Ferroalloys Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Ferroalloys Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Ferroalloys Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 3: Global Ferroalloys Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global Ferroalloys Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 5: Global Ferroalloys Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: China Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: India Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Japan Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: South Korea Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of Asia Pacific Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Ferroalloys Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 12: Global Ferroalloys Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: United States Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Mexico Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Ferroalloys Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 17: Global Ferroalloys Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Germany Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: United Kingdom Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Italy Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Europe Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Ferroalloys Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 24: Global Ferroalloys Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 25: Brazil Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Argentina Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Rest of South America Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Global Ferroalloys Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 29: Global Ferroalloys Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Saudi Arabia Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: South Africa Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Rest of Middle East and Africa Ferroalloys Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ferroalloys Industry?

The projected CAGR is approximately < 3.00%.

2. Which companies are prominent players in the Ferroalloys Industry?

Key companies in the market include China Minmetals Corporation, Eurasian Resources Group, Ferro Alloys Corporation Limited, Ferroglobe, Finnfjord, Mechel, OM Holdings Ltd, Shanghai Shenjia Ferroalloys Co Ltd, SKP Group, Tashi Group*List Not Exhaustive.

3. What are the main segments of the Ferroalloys Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries.

6. What are the notable trends driving market growth?

Growing Demand from Metallurgy Industry.

7. Are there any restraints impacting market growth?

Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries.

8. Can you provide examples of recent developments in the market?

July 2022: Ferroglobe PLC entered a new phase in its silicon metal powder project for batteries and other advanced technologies, reaching a high purity production (up to 99.995%) in micrometer and sub-micrometer size.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ferroalloys Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ferroalloys Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ferroalloys Industry?

To stay informed about further developments, trends, and reports in the Ferroalloys Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence