Key Insights

The North American real and compound chocolate market, valued at approximately $XX million in 2025, is projected to experience steady growth, driven by increasing consumer demand for premium chocolate products and innovative flavor profiles. The market's Compound Annual Growth Rate (CAGR) of 2.91% from 2019 to 2024 suggests a continued expansion through 2033. Key growth drivers include the rising popularity of chocolate in various applications, such as confectionery, bakery, and ice cream, alongside the increasing adoption of convenient, ready-to-eat products. The diverse product segment, encompassing chocolate chips, slabs, coatings, and other forms, caters to a wide range of consumer preferences. While the market faces challenges such as fluctuating cocoa prices and concerns about sugar consumption, the ongoing innovation in flavor combinations (e.g., dark, milk, white, and other specialty flavors) and the expansion of product offerings are expected to mitigate these constraints. The North American market, particularly the United States, holds a significant share of this market, fueled by high per capita chocolate consumption and a strong established food manufacturing sector.

Within the North American market, the segments exhibiting the strongest growth are projected to be premium dark chocolate and specialty chocolate applications in high-growth confectionery segments like artisanal chocolates and premium ice cream. The increasing availability of vegan and organic chocolate options caters to evolving consumer demands. Leading companies like Cargill, Lindt & Sprüngli, and Barry Callebaut are leveraging their established brands and distribution networks to capitalize on these trends. However, competition remains intense, with smaller, niche players focusing on sustainable sourcing and unique flavor profiles to gain market share. Future growth will be influenced by factors such as economic conditions, health and wellness trends, and consumer preferences, with companies likely to focus on product innovation and strategic partnerships to maintain competitiveness within this dynamic market.

North America Real and Compound Chocolate Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North American real and compound chocolate industry, covering market dynamics, growth trends, key players, and future outlook. With a focus on both the parent market (chocolate) and child markets (compound chocolate, specific product types, and applications), this report offers invaluable insights for industry professionals, investors, and strategic decision-makers. The study period spans from 2019 to 2033, with 2025 as the base and estimated year.

Study Period: 2019-2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025-2033 Historical Period: 2019-2024

North America Real and Compound Chocolate Industry Market Dynamics & Structure

This section analyzes the market structure, competitive landscape, and key influencing factors within the North American real and compound chocolate industry. The market is characterized by a blend of large multinational corporations and smaller specialized players. Technological advancements, particularly in ingredient sourcing and processing, are driving innovation and efficiency gains. Stringent food safety regulations and evolving consumer preferences, such as increasing demand for organic and plant-based options, significantly shape the industry's trajectory. Mergers and acquisitions (M&A) activity has been notable, with larger players consolidating market share and expanding their product portfolios.

- Market Concentration: Moderately concentrated, with a few dominant players controlling a significant share. xx% market share held by top 5 players (2024).

- Technological Innovation: Focus on sustainable sourcing, automation in production, and novel flavor/formulation development.

- Regulatory Framework: Stringent food safety regulations and labeling requirements.

- Competitive Substitutes: Sugar confectionery, other desserts, and plant-based alternatives.

- End-User Demographics: Growing demand from health-conscious consumers and expanding millennial/Gen Z populations influence product development.

- M&A Trends: Consolidation among major players, with xx major M&A deals in the last 5 years, focused on expanding product lines and geographical reach.

North America Real and Compound Chocolate Industry Growth Trends & Insights

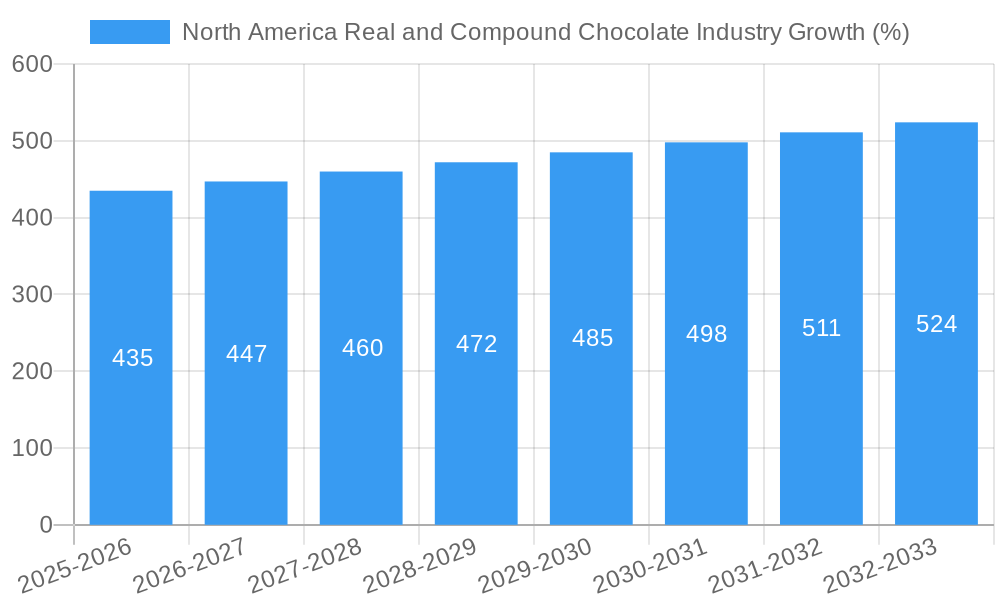

The North American real and compound chocolate market exhibits steady growth driven by several factors. The market size has experienced a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024), reaching a value of $xx Million in 2024. This growth is fueled by rising disposable incomes, changing consumer preferences (e.g., premiumization, indulgence), and increasing product diversification within the sector. Technological advancements in processing and sustainable sourcing contribute to improving production efficiencies and product quality. Market penetration for specific product segments (e.g., dairy-free chocolate) is increasing significantly, reflecting evolving consumer demands. The forecast period (2025-2033) projects a CAGR of xx%, driven by continued consumer demand and innovation.

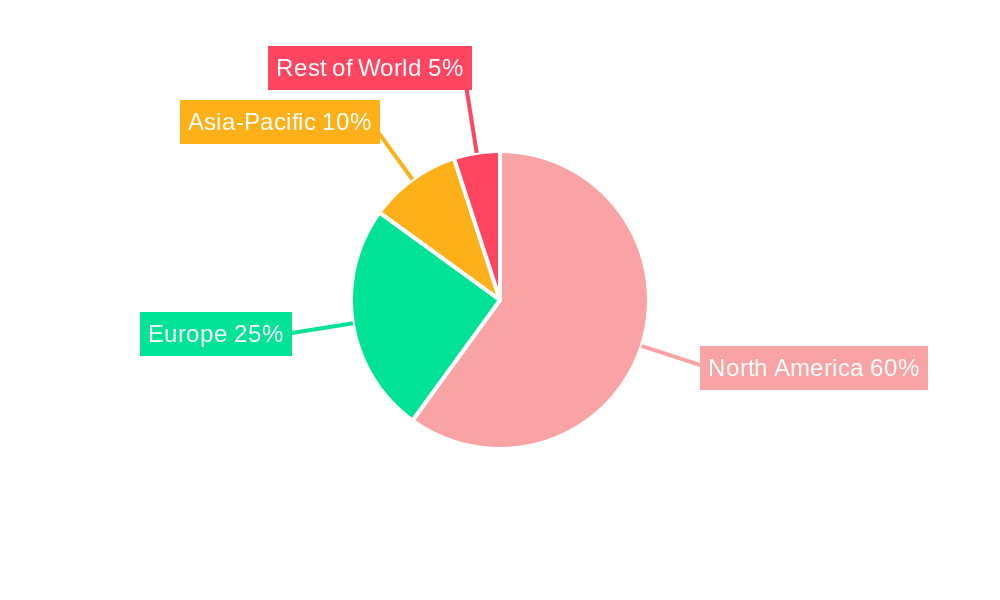

Dominant Regions, Countries, or Segments in North America Real and Compound Chocolate Industry

The US dominates the North American real and compound chocolate market, accounting for xx% of the total market value in 2024. Canada holds a significant portion, representing xx% of the market. Within product segments, milk chocolate maintains the largest share, followed by dark and white chocolate. The confectionery application sector leads in terms of consumption, with increasing demand from the bakery and ice cream sectors.

- Key Drivers (US): Strong economic growth, high chocolate consumption per capita, established distribution networks.

- Key Drivers (Canada): Rising disposable income, increasing popularity of premium chocolate.

- Dominant Flavor Segment: Milk Chocolate, driven by its broad appeal across age groups.

- Dominant Product Segment: Chocolate Chips/Drops/Chunks, owing to its versatility and widespread use in various applications.

- Dominant Application Segment: Confectionery, followed by bakery products.

North America Real and Compound Chocolate Industry Product Landscape

The North American market showcases a diverse range of chocolate products, including chocolate chips, slabs, coatings, and specialized compound chocolates. Product innovation focuses on unique flavors, textures, and functional ingredients catering to specific dietary needs (e.g., vegan, sugar-free). Advancements in processing techniques lead to improved product consistency and shelf life. Sustainability initiatives and ethical sourcing are increasingly influencing consumer choices, driving the growth of organic and fair-trade options.

Key Drivers, Barriers & Challenges in North America Real and Compound Chocolate Industry

Key Drivers:

- Rising disposable incomes and increased spending on premium products.

- Growing demand for convenient and on-the-go snack options.

- Expanding e-commerce channels and online sales.

Challenges:

- Fluctuations in raw material prices (cocoa, sugar, dairy). The price volatility of cocoa beans has resulted in a xx% increase in production costs during 2023 (estimated).

- Stringent regulatory compliance requirements.

- Intense competition from both domestic and international players.

Emerging Opportunities in North America Real and Compound Chocolate Industry

- Growing demand for functional chocolates incorporating health-beneficial ingredients.

- Expansion into new niche markets, such as vegan and organic chocolate.

- Development of innovative product formats and packaging.

- Increased focus on sustainability and ethical sourcing.

Growth Accelerators in the North America Real and Compound Chocolate Industry

Technological breakthroughs in chocolate processing and ingredient sourcing are key growth accelerators. Strategic partnerships between chocolate manufacturers and food retailers enhance distribution and market reach. Expansion into emerging consumer segments (e.g., health-conscious individuals) and innovative marketing strategies are crucial for sustained growth.

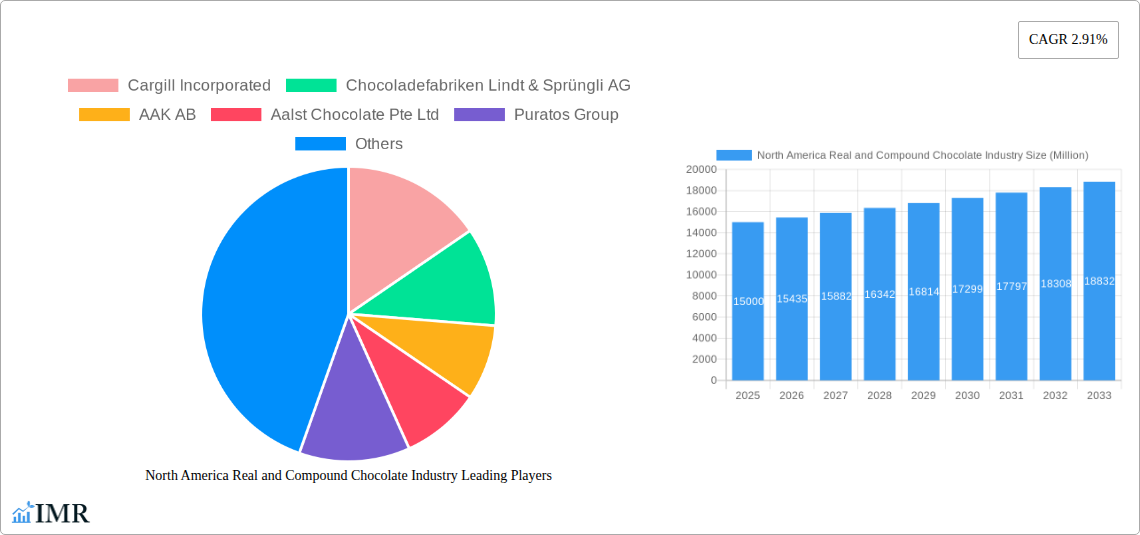

Key Players Shaping the North America Real and Compound Chocolate Industry Market

- Cargill Incorporated

- Chocoladefabriken Lindt & Sprüngli AG

- AAK AB

- Aalst Chocolate Pte Ltd

- Puratos Group

- Sephra

- Fuji Oil Holdings

- Santa Barbara Chocolate

- Natra SA

- The Barry Callebaut Group

- Clasen Quality Chocolate

- Stover & Company

Notable Milestones in North America Real and Compound Chocolate Industry Sector

- September 2021: The Hershey Company and Barry Callebaut extended their strategic supply partnership, strengthening their presence in the North American market.

- November 2021: Barry Callebaut launched a complete portfolio of dairy-free chocolate compounds, capitalizing on the growing plant-based market.

- April 2022: Grupo Bimbo SAB de CV and Barry Callebaut renewed their long-term supply agreement, expanding distribution across North and Central America.

In-Depth North America Real and Compound Chocolate Industry Market Outlook

The North American real and compound chocolate market presents significant growth potential driven by sustained consumer demand, product innovation, and strategic partnerships. Continued focus on sustainability, ethical sourcing, and functional ingredients will shape the industry's future. Expanding into new markets and leveraging e-commerce platforms will be critical for long-term success. The market is expected to experience robust growth, reaching a value of $xx Million by 2033.

North America Real and Compound Chocolate Industry Segmentation

-

1. Flavor

- 1.1. Dark

- 1.2. Milk

- 1.3. White

- 1.4. Other Flavors

-

2. Product

- 2.1. Chocolate Chips/Drops/Chunks

- 2.2. Chocolate Slab

- 2.3. Chocolate Coatings

- 2.4. Other Products

-

3. Application

- 3.1. Compound Chocolates

- 3.2. Bakery

- 3.3. Confectionery

- 3.4. Ice Cream and Frozen Desserts

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Mexico

- 4.4. Rest of North America

North America Real and Compound Chocolate Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

North America Real and Compound Chocolate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.91% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Wide Applications and Functionality; Demand For Gluten-Free Products

- 3.3. Market Restrains

- 3.3.1. Easy Availability of Economically Feasible Alternatives

- 3.4. Market Trends

- 3.4.1. Economical and Desirable Substitute of Cocoa Butter

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Flavor

- 5.1.1. Dark

- 5.1.2. Milk

- 5.1.3. White

- 5.1.4. Other Flavors

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Chocolate Chips/Drops/Chunks

- 5.2.2. Chocolate Slab

- 5.2.3. Chocolate Coatings

- 5.2.4. Other Products

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Compound Chocolates

- 5.3.2. Bakery

- 5.3.3. Confectionery

- 5.3.4. Ice Cream and Frozen Desserts

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.4.4. Rest of North America

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.5.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Flavor

- 6. United States North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Flavor

- 6.1.1. Dark

- 6.1.2. Milk

- 6.1.3. White

- 6.1.4. Other Flavors

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Chocolate Chips/Drops/Chunks

- 6.2.2. Chocolate Slab

- 6.2.3. Chocolate Coatings

- 6.2.4. Other Products

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Compound Chocolates

- 6.3.2. Bakery

- 6.3.3. Confectionery

- 6.3.4. Ice Cream and Frozen Desserts

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Mexico

- 6.4.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Flavor

- 7. Canada North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Flavor

- 7.1.1. Dark

- 7.1.2. Milk

- 7.1.3. White

- 7.1.4. Other Flavors

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Chocolate Chips/Drops/Chunks

- 7.2.2. Chocolate Slab

- 7.2.3. Chocolate Coatings

- 7.2.4. Other Products

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Compound Chocolates

- 7.3.2. Bakery

- 7.3.3. Confectionery

- 7.3.4. Ice Cream and Frozen Desserts

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Mexico

- 7.4.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Flavor

- 8. Mexico North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Flavor

- 8.1.1. Dark

- 8.1.2. Milk

- 8.1.3. White

- 8.1.4. Other Flavors

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Chocolate Chips/Drops/Chunks

- 8.2.2. Chocolate Slab

- 8.2.3. Chocolate Coatings

- 8.2.4. Other Products

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Compound Chocolates

- 8.3.2. Bakery

- 8.3.3. Confectionery

- 8.3.4. Ice Cream and Frozen Desserts

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Mexico

- 8.4.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Flavor

- 9. Rest of North America North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Flavor

- 9.1.1. Dark

- 9.1.2. Milk

- 9.1.3. White

- 9.1.4. Other Flavors

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Chocolate Chips/Drops/Chunks

- 9.2.2. Chocolate Slab

- 9.2.3. Chocolate Coatings

- 9.2.4. Other Products

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Compound Chocolates

- 9.3.2. Bakery

- 9.3.3. Confectionery

- 9.3.4. Ice Cream and Frozen Desserts

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. United States

- 9.4.2. Canada

- 9.4.3. Mexico

- 9.4.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Flavor

- 10. United States North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 11. Canada North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 12. Mexico North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 13. Rest of North America North America Real and Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 14. Competitive Analysis

- 14.1. Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 Cargill Incorporated

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Chocoladefabriken Lindt & Sprüngli AG

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 AAK AB

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Aalst Chocolate Pte Ltd

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Puratos Group

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Sephra

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Fuji Oil Holdings

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Santa Barbara Chocolate*List Not Exhaustive

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Natra SA

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 The Barry Callebaut Group

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.11 Clasen Quality Chocolate

- 14.2.11.1. Overview

- 14.2.11.2. Products

- 14.2.11.3. SWOT Analysis

- 14.2.11.4. Recent Developments

- 14.2.11.5. Financials (Based on Availability)

- 14.2.12 Stover & Company

- 14.2.12.1. Overview

- 14.2.12.2. Products

- 14.2.12.3. SWOT Analysis

- 14.2.12.4. Recent Developments

- 14.2.12.5. Financials (Based on Availability)

- 14.2.1 Cargill Incorporated

List of Figures

- Figure 1: North America Real and Compound Chocolate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Real and Compound Chocolate Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Flavor 2019 & 2032

- Table 3: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 4: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 5: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 6: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United States North America Real and Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada North America Real and Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Mexico North America Real and Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Rest of North America North America Real and Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Flavor 2019 & 2032

- Table 13: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 14: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 15: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 16: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Flavor 2019 & 2032

- Table 18: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 19: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 20: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 21: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Flavor 2019 & 2032

- Table 23: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 24: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 25: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Flavor 2019 & 2032

- Table 28: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 29: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 30: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 31: North America Real and Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Real and Compound Chocolate Industry?

The projected CAGR is approximately 2.91%.

2. Which companies are prominent players in the North America Real and Compound Chocolate Industry?

Key companies in the market include Cargill Incorporated, Chocoladefabriken Lindt & Sprüngli AG, AAK AB, Aalst Chocolate Pte Ltd, Puratos Group, Sephra, Fuji Oil Holdings, Santa Barbara Chocolate*List Not Exhaustive, Natra SA, The Barry Callebaut Group, Clasen Quality Chocolate, Stover & Company.

3. What are the main segments of the North America Real and Compound Chocolate Industry?

The market segments include Flavor, Product, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Wide Applications and Functionality; Demand For Gluten-Free Products.

6. What are the notable trends driving market growth?

Economical and Desirable Substitute of Cocoa Butter.

7. Are there any restraints impacting market growth?

Easy Availability of Economically Feasible Alternatives.

8. Can you provide examples of recent developments in the market?

April 2022: Grupo Bimbo SAB de CV and Barry Callebaut renewed their long-term supply agreement, which was first signed in 2012. Under the terms of the agreement, Barry Callebaut will continue to supply chocolate and compound to Grupo Bimbo's domestic market in Mexico and distribution to several countries in Central America, the United States, Canada, and Uruguay.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Real and Compound Chocolate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Real and Compound Chocolate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Real and Compound Chocolate Industry?

To stay informed about further developments, trends, and reports in the North America Real and Compound Chocolate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence