Key Insights

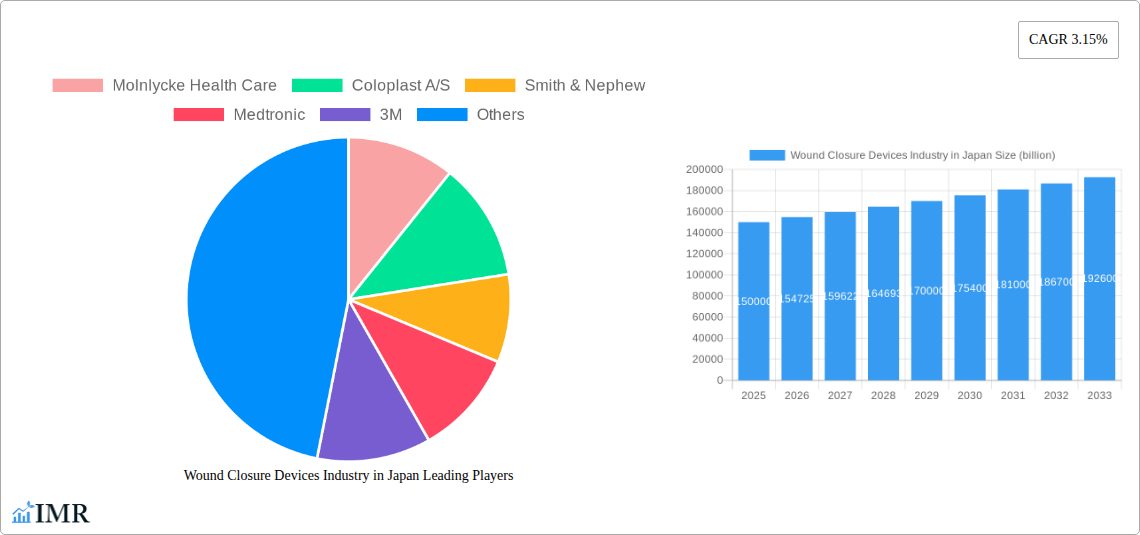

The Japanese wound closure devices market, valued at approximately ¥150 billion (estimated based on comparable global markets and regional economic indicators) in 2025, is projected to experience steady growth, driven by a rising geriatric population predisposed to chronic wounds, increasing prevalence of diabetes, and advancements in minimally invasive surgical procedures. The market's Compound Annual Growth Rate (CAGR) of 3.15% over the forecast period (2025-2033) indicates a consistent demand for innovative and effective wound closure solutions. The segment dominated by acute wound closures (e.g., surgical incisions) is expected to maintain its significant share, while the chronic wound segment (diabetic ulcers, pressure ulcers) will experience comparatively higher growth, driven by the increasing incidence of these conditions. Hospitals and trauma centers constitute the largest end-user segment, reflecting the high volume of surgical procedures and trauma cases. Key players like Molnlycke Health Care, Smith & Nephew, and 3M are expected to maintain their market leadership through product innovation, strategic partnerships, and expansion of their distribution networks within Japan's diverse regional markets (Kanto, Kansai, Chubu, Kyushu, Tohoku). However, increasing healthcare costs and stringent regulatory approvals might pose challenges to market expansion. The market’s growth is further influenced by the adoption of advanced wound closure techniques, such as tissue adhesives and mechanical devices, alongside traditional methods like sutures and staples.

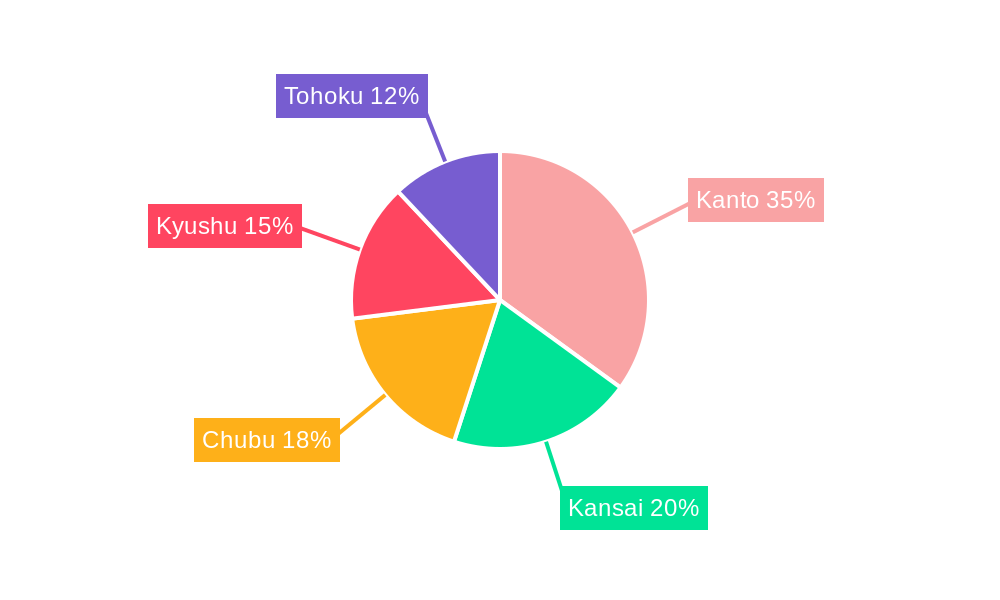

The regional distribution across Japan reflects varying healthcare infrastructure and population density. While the Kanto region (including Tokyo) is expected to hold the largest market share, other regions will see growth proportionate to their demographics and healthcare investments. The competitive landscape is marked by both global and domestic players, with a focus on developing products tailored to the specific needs of the Japanese market, particularly concerning patient preferences and healthcare system requirements. Future growth opportunities lie in the development of biocompatible and biodegradable materials, minimally invasive wound closure devices, and improved wound management solutions for chronic wounds. Further research into advanced wound healing technologies and personalized medicine approaches will significantly shape the market's trajectory in the coming years.

Wound Closure Devices Industry in Japan: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Wound Closure Devices market in Japan, encompassing market size, growth trends, competitive landscape, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report segments the market by product type (adhesives, staples, sutures, strips, sealants, mechanical wound closure devices), wound type (acute wounds, chronic wounds), and end-user (hospitals, clinics, trauma centers, others), offering a granular understanding of this vital healthcare sector. The total market size in 2025 is estimated at XX billion USD and is projected to reach XX billion USD by 2033.

Wound Closure Devices Industry in Japan Market Dynamics & Structure

The Japanese wound closure devices market is characterized by a moderately concentrated landscape with key players such as Molnlycke Health Care, Coloplast A/S, Smith & Nephew, Medtronic, 3M, ConvaTec Group PLC, Cardinal Health Inc, Paul Hartmann AG, B Braun SE, and Integra Lifesciences competing for market share. The market's dynamics are shaped by several factors:

- Market Concentration: The market exhibits a moderate level of concentration, with the top five players holding approximately XX% of the market share in 2025.

- Technological Innovation: Advancements in biocompatible materials, minimally invasive techniques, and smart wound closure devices are driving growth. However, high R&D costs and regulatory hurdles pose significant challenges.

- Regulatory Framework: Stringent regulatory approvals from the Japanese Ministry of Health, Labour and Welfare (MHLW) influence market entry and product availability.

- Competitive Product Substitutes: Traditional suturing techniques continue to compete with advanced wound closure devices, impacting market penetration.

- End-User Demographics: An aging population and rising prevalence of chronic diseases contribute to increased demand for wound closure devices.

- M&A Trends: Consolidation through mergers and acquisitions is expected to increase in the forecast period, with an estimated XX M&A deals anticipated between 2025 and 2033.

Wound Closure Devices Industry in Japan Growth Trends & Insights

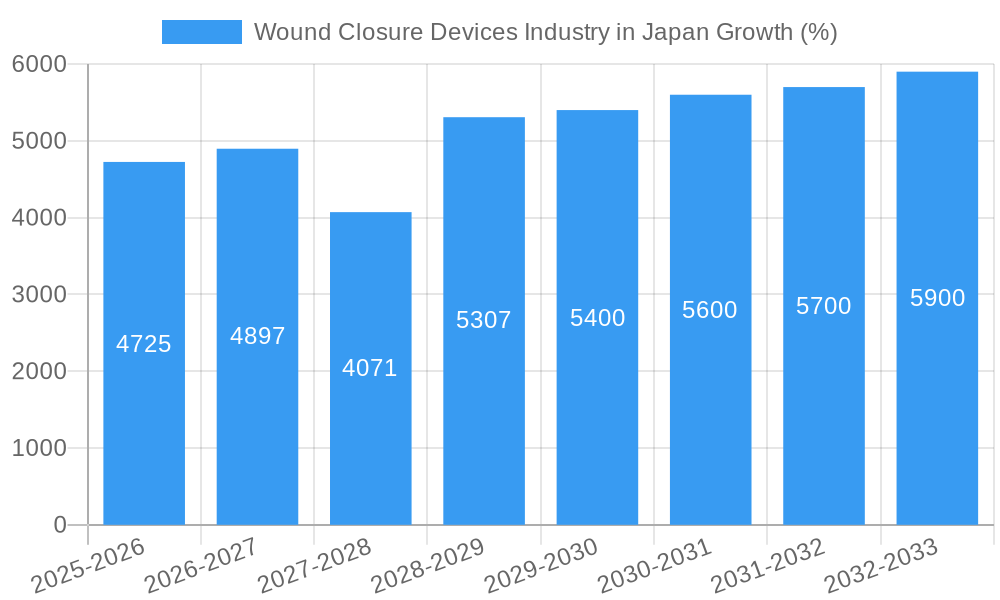

The Japanese wound closure devices market experienced a CAGR of XX% during the historical period (2019-2024). This growth is projected to continue, with an estimated CAGR of XX% during the forecast period (2025-2033), reaching a market value of XX billion USD by 2033. This growth is driven by factors such as the rising prevalence of chronic wounds, increasing demand for minimally invasive procedures, and advancements in wound closure technologies. The market penetration rate for advanced wound closure devices is currently at approximately XX%, with significant potential for further growth, particularly in rural areas and smaller clinics. Technological disruptions, such as the introduction of bio-absorbable materials and smart wound monitoring systems, are accelerating market expansion. Consumer behavior shifts, including increased preference for less invasive and faster recovery methods, are also influencing market trends. Market growth is further accelerated by increasing healthcare expenditure and government initiatives to improve healthcare infrastructure.

Dominant Regions, Countries, or Segments in Wound Closure Devices Industry in Japan

The Kanto region, encompassing Tokyo and its surrounding prefectures, is currently the dominant market segment due to high concentration of hospitals and medical facilities. However, other regions are witnessing significant growth due to improvements in healthcare infrastructure and access.

Dominant Segments:

- Product Type: Sutures and staples currently dominate the market, holding approximately XX% of the total market share in 2025. However, adhesives and sealants are experiencing faster growth due to their minimally invasive nature and ease of use.

- Wound Type: Chronic wounds, including diabetic ulcers and pressure ulcers, account for a significant portion of the market due to their high prevalence and longer treatment durations.

- End-User: Hospitals remain the largest end-user segment, driven by a high volume of surgical procedures and trauma cases. However, clinics and trauma centers are emerging as significant growth drivers.

Key Drivers:

- Favorable government policies supporting healthcare infrastructure development.

- Increased healthcare expenditure.

- Growing awareness among healthcare professionals regarding the benefits of advanced wound closure devices.

Wound Closure Devices Industry in Japan Product Landscape

The Japanese market showcases a diverse range of wound closure devices, from traditional sutures and staples to advanced bio-absorbable materials and innovative sealant technologies. Recent innovations focus on improving biocompatibility, reducing infection risk, and enhancing patient comfort. Products are increasingly incorporating features like antimicrobial properties and enhanced tissue integration capabilities to improve healing outcomes. These technological advancements are directly correlated to improving patient recovery times and reducing the overall cost of care.

Key Drivers, Barriers & Challenges in Wound Closure Devices Industry in Japan

Key Drivers:

- The aging population and rising incidence of chronic diseases fuel the demand for efficient wound management solutions.

- Technological advancements in materials science and medical device engineering are continuously improving the effectiveness and safety of wound closure devices.

- Government initiatives promoting advanced medical technologies and better healthcare infrastructure facilitate market expansion.

Key Challenges:

- High regulatory hurdles and stringent approval processes for new devices create market entry barriers and slow down innovation.

- The high cost of advanced wound closure devices limits affordability for some healthcare facilities. This results in a reliance on cost-effective traditional methods.

- Competition from existing and new players intensifies pricing pressures and creates a dynamic competitive landscape.

Emerging Opportunities in Wound Closure Devices Industry in Japan

Untapped market potential exists in smaller clinics and rural areas. Furthermore, there's significant growth opportunity in developing specialized wound closure devices for specific wound types, such as diabetic foot ulcers, which necessitate tailored solutions. The increasing focus on minimally invasive procedures creates a promising opportunity for innovative devices that reduce complications and improve patient outcomes.

Growth Accelerators in the Wound Closure Devices Industry in Japan Industry

Strategic partnerships between device manufacturers and healthcare providers will propel market growth. Technological breakthroughs in bio-engineered materials and smart wound care systems will further enhance device capabilities and attract wider adoption. Market expansion initiatives targeting underserved areas, coupled with focused marketing campaigns for specific demographics, will increase market penetration.

Key Players Shaping the Wound Closure Devices Industry in Japan Market

- Molnlycke Health Care

- Coloplast A/S

- Smith & Nephew

- Medtronic

- 3M

- ConvaTec Group PLC

- Cardinal Health Inc

- Paul Hartmann AG

- B Braun SE

- Integra Lifesciences

Notable Milestones in Wound Closure Devices Industry in Japan Sector

- January 2023: MiMedx Group, Inc. secured an exclusive distribution agreement with GUNZE MEDICAL LIMITED for EPIFIX sales in Japan, significantly expanding the market reach of this chronic wound treatment.

- April 2023: Gunze Medical expanded its wound care sales channel, directly selling artificial dermis (PELNAC), wound dressings, and other related medical devices, potentially altering the distribution dynamics and competitive landscape.

In-Depth Wound Closure Devices Industry in Japan Market Outlook

The Japanese wound closure devices market is poised for robust growth, driven by an aging population, rising chronic disease prevalence, and ongoing technological innovation. Strategic investments in R&D, collaborations to expand distribution channels, and a focus on addressing the unique needs of different wound types will create lucrative opportunities for both established players and new entrants. The continued focus on minimally invasive and improved patient-centric solutions will remain central to the future success in this market.

Wound Closure Devices Industry in Japan Segmentation

-

1. Product

-

1.1. Wound Care

- 1.1.1. Dressings

- 1.1.2. Bandages

- 1.1.3. Other Wound Care Products

-

1.2. Wound Closure

- 1.2.1. Suture

- 1.2.2. Surgical Staplers

- 1.2.3. Other Wound Closure Products

-

1.1. Wound Care

-

2. Wound Type

-

2.1. Chronic Wound

- 2.1.1. Diabetic Foot Ulcer

- 2.1.2. Pressure Ulcer

- 2.1.3. Other Chronic Wounds

-

2.2. Acute Wound

- 2.2.1. Surgical Wounds

- 2.2.2. Burns

- 2.2.3. Other Acute Wounds

-

2.1. Chronic Wound

Wound Closure Devices Industry in Japan Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wound Closure Devices Industry in Japan REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.15% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increase in the Aging Population in Japan; Increasing Incidences of Chronic Wounds

- 3.2.2 Ulcers and Diabetic Ulcers; Increase in Volume of Surgical Procedures

- 3.3. Market Restrains

- 3.3.1. High Treatment Costs

- 3.4. Market Trends

- 3.4.1. Diabetic Foot Ulcer Under Chronic Wound Segment is Expected to Have a Significant Share in the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Wound Care

- 5.1.1.1. Dressings

- 5.1.1.2. Bandages

- 5.1.1.3. Other Wound Care Products

- 5.1.2. Wound Closure

- 5.1.2.1. Suture

- 5.1.2.2. Surgical Staplers

- 5.1.2.3. Other Wound Closure Products

- 5.1.1. Wound Care

- 5.2. Market Analysis, Insights and Forecast - by Wound Type

- 5.2.1. Chronic Wound

- 5.2.1.1. Diabetic Foot Ulcer

- 5.2.1.2. Pressure Ulcer

- 5.2.1.3. Other Chronic Wounds

- 5.2.2. Acute Wound

- 5.2.2.1. Surgical Wounds

- 5.2.2.2. Burns

- 5.2.2.3. Other Acute Wounds

- 5.2.1. Chronic Wound

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Wound Care

- 6.1.1.1. Dressings

- 6.1.1.2. Bandages

- 6.1.1.3. Other Wound Care Products

- 6.1.2. Wound Closure

- 6.1.2.1. Suture

- 6.1.2.2. Surgical Staplers

- 6.1.2.3. Other Wound Closure Products

- 6.1.1. Wound Care

- 6.2. Market Analysis, Insights and Forecast - by Wound Type

- 6.2.1. Chronic Wound

- 6.2.1.1. Diabetic Foot Ulcer

- 6.2.1.2. Pressure Ulcer

- 6.2.1.3. Other Chronic Wounds

- 6.2.2. Acute Wound

- 6.2.2.1. Surgical Wounds

- 6.2.2.2. Burns

- 6.2.2.3. Other Acute Wounds

- 6.2.1. Chronic Wound

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. South America Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Wound Care

- 7.1.1.1. Dressings

- 7.1.1.2. Bandages

- 7.1.1.3. Other Wound Care Products

- 7.1.2. Wound Closure

- 7.1.2.1. Suture

- 7.1.2.2. Surgical Staplers

- 7.1.2.3. Other Wound Closure Products

- 7.1.1. Wound Care

- 7.2. Market Analysis, Insights and Forecast - by Wound Type

- 7.2.1. Chronic Wound

- 7.2.1.1. Diabetic Foot Ulcer

- 7.2.1.2. Pressure Ulcer

- 7.2.1.3. Other Chronic Wounds

- 7.2.2. Acute Wound

- 7.2.2.1. Surgical Wounds

- 7.2.2.2. Burns

- 7.2.2.3. Other Acute Wounds

- 7.2.1. Chronic Wound

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Wound Care

- 8.1.1.1. Dressings

- 8.1.1.2. Bandages

- 8.1.1.3. Other Wound Care Products

- 8.1.2. Wound Closure

- 8.1.2.1. Suture

- 8.1.2.2. Surgical Staplers

- 8.1.2.3. Other Wound Closure Products

- 8.1.1. Wound Care

- 8.2. Market Analysis, Insights and Forecast - by Wound Type

- 8.2.1. Chronic Wound

- 8.2.1.1. Diabetic Foot Ulcer

- 8.2.1.2. Pressure Ulcer

- 8.2.1.3. Other Chronic Wounds

- 8.2.2. Acute Wound

- 8.2.2.1. Surgical Wounds

- 8.2.2.2. Burns

- 8.2.2.3. Other Acute Wounds

- 8.2.1. Chronic Wound

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Middle East & Africa Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Wound Care

- 9.1.1.1. Dressings

- 9.1.1.2. Bandages

- 9.1.1.3. Other Wound Care Products

- 9.1.2. Wound Closure

- 9.1.2.1. Suture

- 9.1.2.2. Surgical Staplers

- 9.1.2.3. Other Wound Closure Products

- 9.1.1. Wound Care

- 9.2. Market Analysis, Insights and Forecast - by Wound Type

- 9.2.1. Chronic Wound

- 9.2.1.1. Diabetic Foot Ulcer

- 9.2.1.2. Pressure Ulcer

- 9.2.1.3. Other Chronic Wounds

- 9.2.2. Acute Wound

- 9.2.2.1. Surgical Wounds

- 9.2.2.2. Burns

- 9.2.2.3. Other Acute Wounds

- 9.2.1. Chronic Wound

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Asia Pacific Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Wound Care

- 10.1.1.1. Dressings

- 10.1.1.2. Bandages

- 10.1.1.3. Other Wound Care Products

- 10.1.2. Wound Closure

- 10.1.2.1. Suture

- 10.1.2.2. Surgical Staplers

- 10.1.2.3. Other Wound Closure Products

- 10.1.1. Wound Care

- 10.2. Market Analysis, Insights and Forecast - by Wound Type

- 10.2.1. Chronic Wound

- 10.2.1.1. Diabetic Foot Ulcer

- 10.2.1.2. Pressure Ulcer

- 10.2.1.3. Other Chronic Wounds

- 10.2.2. Acute Wound

- 10.2.2.1. Surgical Wounds

- 10.2.2.2. Burns

- 10.2.2.3. Other Acute Wounds

- 10.2.1. Chronic Wound

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Kanto Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 12. Kansai Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 13. Chubu Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 14. Kyushu Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 15. Tohoku Wound Closure Devices Industry in Japan Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Molnlycke Health Care

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Coloplast A/S

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Smith & Nephew

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Medtronic

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 3M

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 ConvaTec Group PLC

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Cardinal Health Inc

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Paul Hartmann AG

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 B Braun SE

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Integra Lifesciences

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Molnlycke Health Care

List of Figures

- Figure 1: Global Wound Closure Devices Industry in Japan Revenue Breakdown (billion, %) by Region 2024 & 2032

- Figure 2: Japan Wound Closure Devices Industry in Japan Revenue (billion), by Country 2024 & 2032

- Figure 3: Japan Wound Closure Devices Industry in Japan Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America Wound Closure Devices Industry in Japan Revenue (billion), by Product 2024 & 2032

- Figure 5: North America Wound Closure Devices Industry in Japan Revenue Share (%), by Product 2024 & 2032

- Figure 6: North America Wound Closure Devices Industry in Japan Revenue (billion), by Wound Type 2024 & 2032

- Figure 7: North America Wound Closure Devices Industry in Japan Revenue Share (%), by Wound Type 2024 & 2032

- Figure 8: North America Wound Closure Devices Industry in Japan Revenue (billion), by Country 2024 & 2032

- Figure 9: North America Wound Closure Devices Industry in Japan Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Wound Closure Devices Industry in Japan Revenue (billion), by Product 2024 & 2032

- Figure 11: South America Wound Closure Devices Industry in Japan Revenue Share (%), by Product 2024 & 2032

- Figure 12: South America Wound Closure Devices Industry in Japan Revenue (billion), by Wound Type 2024 & 2032

- Figure 13: South America Wound Closure Devices Industry in Japan Revenue Share (%), by Wound Type 2024 & 2032

- Figure 14: South America Wound Closure Devices Industry in Japan Revenue (billion), by Country 2024 & 2032

- Figure 15: South America Wound Closure Devices Industry in Japan Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Wound Closure Devices Industry in Japan Revenue (billion), by Product 2024 & 2032

- Figure 17: Europe Wound Closure Devices Industry in Japan Revenue Share (%), by Product 2024 & 2032

- Figure 18: Europe Wound Closure Devices Industry in Japan Revenue (billion), by Wound Type 2024 & 2032

- Figure 19: Europe Wound Closure Devices Industry in Japan Revenue Share (%), by Wound Type 2024 & 2032

- Figure 20: Europe Wound Closure Devices Industry in Japan Revenue (billion), by Country 2024 & 2032

- Figure 21: Europe Wound Closure Devices Industry in Japan Revenue Share (%), by Country 2024 & 2032

- Figure 22: Middle East & Africa Wound Closure Devices Industry in Japan Revenue (billion), by Product 2024 & 2032

- Figure 23: Middle East & Africa Wound Closure Devices Industry in Japan Revenue Share (%), by Product 2024 & 2032

- Figure 24: Middle East & Africa Wound Closure Devices Industry in Japan Revenue (billion), by Wound Type 2024 & 2032

- Figure 25: Middle East & Africa Wound Closure Devices Industry in Japan Revenue Share (%), by Wound Type 2024 & 2032

- Figure 26: Middle East & Africa Wound Closure Devices Industry in Japan Revenue (billion), by Country 2024 & 2032

- Figure 27: Middle East & Africa Wound Closure Devices Industry in Japan Revenue Share (%), by Country 2024 & 2032

- Figure 28: Asia Pacific Wound Closure Devices Industry in Japan Revenue (billion), by Product 2024 & 2032

- Figure 29: Asia Pacific Wound Closure Devices Industry in Japan Revenue Share (%), by Product 2024 & 2032

- Figure 30: Asia Pacific Wound Closure Devices Industry in Japan Revenue (billion), by Wound Type 2024 & 2032

- Figure 31: Asia Pacific Wound Closure Devices Industry in Japan Revenue Share (%), by Wound Type 2024 & 2032

- Figure 32: Asia Pacific Wound Closure Devices Industry in Japan Revenue (billion), by Country 2024 & 2032

- Figure 33: Asia Pacific Wound Closure Devices Industry in Japan Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Region 2019 & 2032

- Table 2: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Product 2019 & 2032

- Table 3: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Wound Type 2019 & 2032

- Table 4: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Region 2019 & 2032

- Table 5: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Country 2019 & 2032

- Table 6: Kanto Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 7: Kansai Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 8: Chubu Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 9: Kyushu Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 10: Tohoku Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 11: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Product 2019 & 2032

- Table 12: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Wound Type 2019 & 2032

- Table 13: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Country 2019 & 2032

- Table 14: United States Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 15: Canada Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 16: Mexico Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 17: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Product 2019 & 2032

- Table 18: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Wound Type 2019 & 2032

- Table 19: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Country 2019 & 2032

- Table 20: Brazil Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 21: Argentina Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 22: Rest of South America Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 23: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Product 2019 & 2032

- Table 24: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Wound Type 2019 & 2032

- Table 25: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Country 2019 & 2032

- Table 26: United Kingdom Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 27: Germany Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 28: France Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 29: Italy Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 30: Spain Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 31: Russia Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 32: Benelux Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 33: Nordics Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 34: Rest of Europe Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 35: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Product 2019 & 2032

- Table 36: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Wound Type 2019 & 2032

- Table 37: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Country 2019 & 2032

- Table 38: Turkey Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 39: Israel Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 40: GCC Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 41: North Africa Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 42: South Africa Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 43: Rest of Middle East & Africa Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 44: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Product 2019 & 2032

- Table 45: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Wound Type 2019 & 2032

- Table 46: Global Wound Closure Devices Industry in Japan Revenue billion Forecast, by Country 2019 & 2032

- Table 47: China Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 48: India Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 49: Japan Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 50: South Korea Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 51: ASEAN Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 52: Oceania Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

- Table 53: Rest of Asia Pacific Wound Closure Devices Industry in Japan Revenue (billion) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wound Closure Devices Industry in Japan?

The projected CAGR is approximately 3.15%.

2. Which companies are prominent players in the Wound Closure Devices Industry in Japan?

Key companies in the market include Molnlycke Health Care, Coloplast A/S, Smith & Nephew, Medtronic, 3M, ConvaTec Group PLC, Cardinal Health Inc, Paul Hartmann AG, B Braun SE, Integra Lifesciences.

3. What are the main segments of the Wound Closure Devices Industry in Japan?

The market segments include Product, Wound Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in the Aging Population in Japan; Increasing Incidences of Chronic Wounds. Ulcers and Diabetic Ulcers; Increase in Volume of Surgical Procedures.

6. What are the notable trends driving market growth?

Diabetic Foot Ulcer Under Chronic Wound Segment is Expected to Have a Significant Share in the Market.

7. Are there any restraints impacting market growth?

High Treatment Costs.

8. Can you provide examples of recent developments in the market?

April 2023: Gunze Medical, a comprehensive medical device manufacturer that handles everything from research to sales, strengthened its wound care sales channel in Japan. With this, Gunze started directly selling artificial dermis as PELNAC, wound dressings (fiber pads for debridement), and other medical devices for wound care in Japan.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wound Closure Devices Industry in Japan," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wound Closure Devices Industry in Japan report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wound Closure Devices Industry in Japan?

To stay informed about further developments, trends, and reports in the Wound Closure Devices Industry in Japan, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence