Key Insights

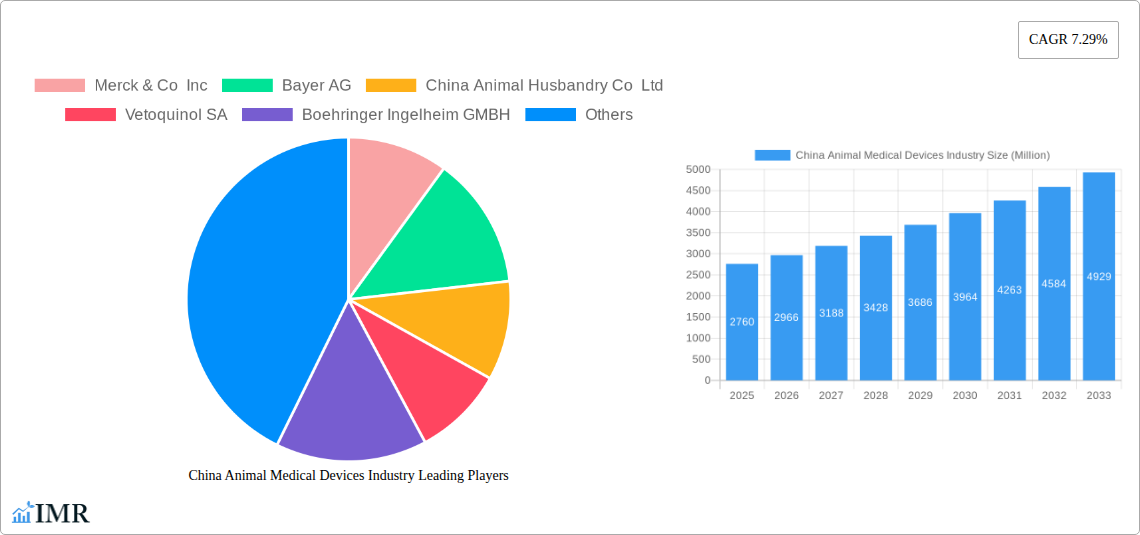

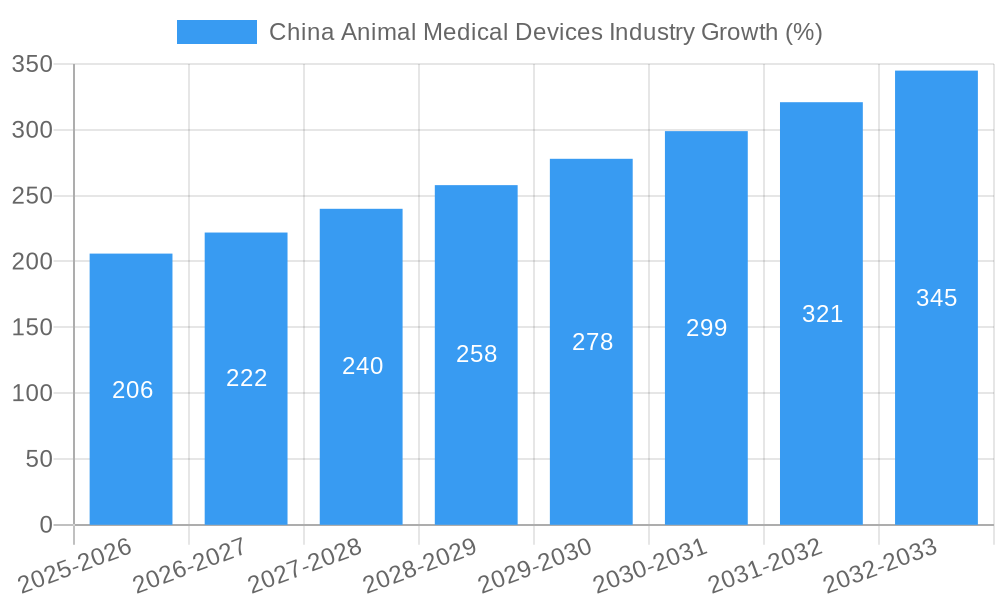

The China animal medical devices market, valued at approximately $2.76 billion in 2025, exhibits robust growth potential, projected to expand at a compound annual growth rate (CAGR) of 7.29% from 2025 to 2033. This expansion is fueled by several key drivers. Increasing pet ownership, particularly in urban areas, coupled with rising pet humanization trends, is significantly boosting demand for advanced diagnostic and therapeutic devices. Furthermore, the government's increasing focus on animal health and disease prevention, along with improvements in veterinary infrastructure and expertise, contributes to market growth. The market is segmented by product type (therapeutics, diagnostics, other) and animal type (dogs and cats, horses, ruminants, swine, poultry, other), with dogs and cats currently dominating the market share due to higher pet ownership rates and increased willingness to spend on their healthcare. While the market faces challenges such as stringent regulatory approvals and regional disparities in veterinary infrastructure, the overall outlook remains positive, driven by the expanding middle class and rising disposable incomes within China.

Competition in the market is intense, with both domestic and international players vying for market share. Major players like Merck & Co Inc, Bayer AG, Zoetis Inc, and others are actively engaged in research and development, introducing innovative products and expanding their distribution networks. The market's growth trajectory is also influenced by government initiatives promoting sustainable agricultural practices and improved animal welfare. This creates opportunities for specialized animal medical device companies offering solutions for specific livestock health challenges. Growth in the swine and poultry segments is projected to be particularly strong due to China's significant agricultural sector and focus on improving animal health for increased productivity. Therefore, continued investment in research, product innovation, and strategic partnerships will be key for companies aiming to succeed in this dynamic and expanding market.

China Animal Medical Devices Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the burgeoning China animal medical devices industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report leverages extensive data and expert analysis to illuminate growth trends, market segmentation, competitive landscapes, and future opportunities within this dynamic sector. The report meticulously examines the parent market (Animal Health) and child markets (Therapeutics, Diagnostics, etc.) to provide a holistic understanding. Market values are presented in Million units.

China Animal Medical Devices Industry Market Dynamics & Structure

This section analyzes the structural dynamics of the Chinese animal medical devices market, considering market concentration, technological advancements, regulatory landscapes, competitive substitution, end-user demographics, and mergers & acquisitions (M&A) activity.

Market Concentration: The market exhibits a moderately concentrated structure, with a handful of multinational corporations and a growing number of domestic players vying for market share. Multinationals like Zoetis and Boehringer Ingelheim hold significant market positions due to their established brands and extensive product portfolios. However, domestic companies are increasingly challenging this dominance through localized innovation and competitive pricing. We estimate the top 5 players hold approximately xx% of the market share in 2025.

Technological Innovation: Technological innovation plays a crucial role, with advancements in diagnostics (e.g., point-of-care diagnostics) and therapeutics (e.g., targeted drug delivery) driving market expansion. However, barriers to innovation include stringent regulatory approval processes and high R&D costs.

Regulatory Framework: The regulatory environment is constantly evolving, impacting market entry and product approvals. Stringent quality control and safety standards necessitate substantial investment and compliance efforts from companies.

Competitive Product Substitutes: The presence of traditional veterinary practices and alternative therapies poses a level of competition. However, the increasing demand for advanced diagnostics and effective therapeutics continues to fuel growth within the medical device sector.

End-User Demographics: The expanding pet-owning population and increasing pet healthcare spending are driving demand, particularly within the companion animal (dogs and cats) segment. Meanwhile, the livestock sector presents opportunities for growth, especially in areas with intensive farming practices.

M&A Trends: The industry has witnessed an increase in M&A activity, with both strategic acquisitions and collaborations aimed at expanding market reach, enhancing product portfolios, and accelerating innovation. The acquisition of an equity stake by Boehringer Ingelheim in New Ruipeng Group in 2020 exemplifies such strategic moves. The total value of M&A deals in 2024 is estimated at xx Million units.

- Market Share of Top 5 Players (2025): xx%

- Number of M&A Deals (2019-2024): xx

- Average Deal Value (2019-2024): xx Million units

China Animal Medical Devices Industry Growth Trends & Insights

The China animal medical devices market experienced substantial growth during the historical period (2019-2024), driven by factors such as increasing pet ownership, rising disposable incomes, and growing awareness of animal healthcare. The market size expanded from xx Million units in 2019 to xx Million units in 2024, registering a Compound Annual Growth Rate (CAGR) of xx%. This positive trend is expected to continue throughout the forecast period (2025-2033), with the market projected to reach xx Million units by 2033. The adoption rate of advanced diagnostic tools and therapeutic devices is also increasing, fueled by technological advancements and the rise of specialized veterinary clinics. Consumer behavior is shifting towards a preference for premium products and sophisticated veterinary services. Furthermore, government initiatives promoting animal welfare and the modernization of livestock farming are creating significant growth opportunities.

Dominant Regions, Countries, or Segments in China Animal Medical Devices Industry

The coastal regions of China, including Guangdong, Jiangsu, and Zhejiang, are leading the market in terms of both market size and growth rate. These areas boast higher disposable incomes, a higher concentration of veterinary clinics, and a greater awareness of animal healthcare. Within the product segments, Therapeutics holds the largest market share, followed by Diagnostics. The companion animal segment (Dogs and Cats) is currently the dominant animal type, driven by the expanding pet-owning population and their willingness to invest in their pets' health. However, significant growth potential exists within the livestock sector (Ruminants, Swine, Poultry), particularly as farmers adopt improved disease management strategies and prioritize animal health for improved productivity.

- Key Drivers for Coastal Regions: Higher disposable incomes, increased pet ownership, advanced veterinary infrastructure.

- Key Drivers for Therapeutics Segment: Increasing prevalence of animal diseases, rising demand for effective treatments.

- Key Drivers for Companion Animal Segment: Growing pet ownership, rising pet humanization trends.

- Growth Potential in Livestock Sector: Improved disease management strategies, increased demand for enhanced productivity.

China Animal Medical Devices Industry Product Landscape

The product landscape is characterized by a diverse range of devices, including diagnostic imaging equipment (e.g., ultrasound, X-ray), in-vitro diagnostic tests, surgical instruments, and therapeutic devices. Recent innovations include the development of portable diagnostic devices for on-site testing, minimally invasive surgical instruments, and advanced drug delivery systems. These advancements are enhancing the efficiency and effectiveness of veterinary care, contributing to improved animal health outcomes and reducing the costs associated with treatment. Many products emphasize ease of use, portability, and accuracy to cater to the specific needs of different animal types and veterinary practices.

Key Drivers, Barriers & Challenges in China Animal Medical Devices Industry

Key Drivers: Rising pet ownership and increasing pet expenditure, growing awareness of animal welfare, technological advancements in diagnostics and therapeutics, government support for agricultural modernization and animal health initiatives. The growing demand for efficient and effective animal healthcare solutions in both companion animals and livestock is a significant catalyst for market growth.

Key Barriers & Challenges: Stringent regulatory approvals causing delays in product launches, high R&D costs hindering innovation by smaller domestic players, uneven distribution infrastructure leading to regional disparities in access to advanced medical devices, and fierce competition from both domestic and multinational companies. Supply chain disruptions, particularly during recent global events, also posed significant challenges. These factors collectively contribute to the complexities of operating within this dynamic market.

Emerging Opportunities in China Animal Medical Devices Industry

Untapped opportunities exist in the rural areas with expanding veterinary care access, leveraging telemedicine for remote diagnostics, development of cost-effective diagnostic tools for resource-limited settings, specialized devices for unique animal types, and tapping into the growing demand for personalized medicine in animal healthcare. The increasing interest in preventative healthcare and the development of innovative solutions to tackle emerging diseases are also paving the way for exciting prospects.

Growth Accelerators in the China Animal Medical Devices Industry

Long-term growth will be propelled by strategic partnerships between domestic and international companies, government initiatives to support the modernization of the animal health sector, investments in research and development leading to advancements in diagnostic and therapeutic technologies. Expansion into underserved regions and the development of innovative business models to improve access to veterinary care will further accelerate growth.

Key Players Shaping the China Animal Medical Devices Industry Market

- Merck & Co Inc

- Bayer AG

- China Animal Husbandry Co Ltd

- Vetoquinol SA

- Boehringer Ingelheim GMBH

- Virbac Corporation

- BioChek BV

- Ceva Sante Animale

- Elanco Animal Health Incorporated

- Zoetis Inc

Notable Milestones in China Animal Medical Devices Industry Sector

- May 2021: Boehringer Ingelheim launched GastroGard (omeprazole oral paste) in China, becoming the first imported equine drug approved.

- September 2020: Boehringer Ingelheim acquired an equity stake in New Ruipeng Group, expanding its reach in the Chinese animal health market.

In-Depth China Animal Medical Devices Industry Market Outlook

The future of the China animal medical devices market is bright, with continued growth driven by technological innovation, increasing pet ownership, and expanding veterinary care access across the country. Strategic investments in R&D, strategic partnerships, and expanding distribution networks are crucial for players to capitalize on the significant market opportunities presented by this dynamic sector. The focus will shift towards personalized medicine, preventative care, and technologically advanced solutions. The increasing collaboration between domestic and multinational companies will also shape the industry's future landscape.

China Animal Medical Devices Industry Segmentation

-

1. Product

-

1.1. By Therapeutics

- 1.1.1. Vaccines

- 1.1.2. Parasiticides

- 1.1.3. Anti-infectives

- 1.1.4. Medical Feed Additives

- 1.1.5. Other Therapeutics

-

1.2. By Diagnostics

- 1.2.1. Immunodiagnostic Tests

- 1.2.2. Molecular Diagnostics

- 1.2.3. Diagnostic Imaging

- 1.2.4. Clinical Chemistry

- 1.2.5. Other Diagnostics

-

1.1. By Therapeutics

-

2. Animal Type

- 2.1. Dogs and Cats

- 2.2. Horses

- 2.3. Ruminants

- 2.4. Swine

- 2.5. Poultry

- 2.6. Other Animals

China Animal Medical Devices Industry Segmentation By Geography

- 1. China

China Animal Medical Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.29% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Pet Adoption; Advanced Technology in Animal Healthcare; Rise in the number of Initiatives by Governments and Animal Welfare Associations

- 3.3. Market Restrains

- 3.3.1. Use of Counterfeit Medicines; Increasing Costs of Animal Testing and Veterinary Care

- 3.4. Market Trends

- 3.4.1. The Dogs and Cats Segment Dominates the China Veterinary Healthcare Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Animal Medical Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. By Therapeutics

- 5.1.1.1. Vaccines

- 5.1.1.2. Parasiticides

- 5.1.1.3. Anti-infectives

- 5.1.1.4. Medical Feed Additives

- 5.1.1.5. Other Therapeutics

- 5.1.2. By Diagnostics

- 5.1.2.1. Immunodiagnostic Tests

- 5.1.2.2. Molecular Diagnostics

- 5.1.2.3. Diagnostic Imaging

- 5.1.2.4. Clinical Chemistry

- 5.1.2.5. Other Diagnostics

- 5.1.1. By Therapeutics

- 5.2. Market Analysis, Insights and Forecast - by Animal Type

- 5.2.1. Dogs and Cats

- 5.2.2. Horses

- 5.2.3. Ruminants

- 5.2.4. Swine

- 5.2.5. Poultry

- 5.2.6. Other Animals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Merck & Co Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Bayer AG

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 China Animal Husbandry Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Vetoquinol SA

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Boehringer Ingelheim GMBH

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Virbac Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 BioChek BV

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Ceva Sante Animale

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Elanco Animal Health Incorporated

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Zoetis Inc

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Merck & Co Inc

List of Figures

- Figure 1: China Animal Medical Devices Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Animal Medical Devices Industry Share (%) by Company 2024

List of Tables

- Table 1: China Animal Medical Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Animal Medical Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: China Animal Medical Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 4: China Animal Medical Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 5: China Animal Medical Devices Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 6: China Animal Medical Devices Industry Volume K Unit Forecast, by Animal Type 2019 & 2032

- Table 7: China Animal Medical Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: China Animal Medical Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: China Animal Medical Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: China Animal Medical Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: China Animal Medical Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 12: China Animal Medical Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 13: China Animal Medical Devices Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 14: China Animal Medical Devices Industry Volume K Unit Forecast, by Animal Type 2019 & 2032

- Table 15: China Animal Medical Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: China Animal Medical Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Animal Medical Devices Industry?

The projected CAGR is approximately 7.29%.

2. Which companies are prominent players in the China Animal Medical Devices Industry?

Key companies in the market include Merck & Co Inc, Bayer AG, China Animal Husbandry Co Ltd, Vetoquinol SA, Boehringer Ingelheim GMBH, Virbac Corporation, BioChek BV, Ceva Sante Animale, Elanco Animal Health Incorporated, Zoetis Inc.

3. What are the main segments of the China Animal Medical Devices Industry?

The market segments include Product, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.76 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Pet Adoption; Advanced Technology in Animal Healthcare; Rise in the number of Initiatives by Governments and Animal Welfare Associations.

6. What are the notable trends driving market growth?

The Dogs and Cats Segment Dominates the China Veterinary Healthcare Market.

7. Are there any restraints impacting market growth?

Use of Counterfeit Medicines; Increasing Costs of Animal Testing and Veterinary Care.

8. Can you provide examples of recent developments in the market?

In May 2021, Boehringer Ingelheim has launched GastroGard(omeprazole oral paste) in the Chinese market, has been granted by the Registration Certificate of Imported Veterinary Drug by the Ministry of Agriculture and Rural Affairs of China, making it the first equine drug approved to be imported into the China market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Animal Medical Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Animal Medical Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Animal Medical Devices Industry?

To stay informed about further developments, trends, and reports in the China Animal Medical Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence