Key Insights

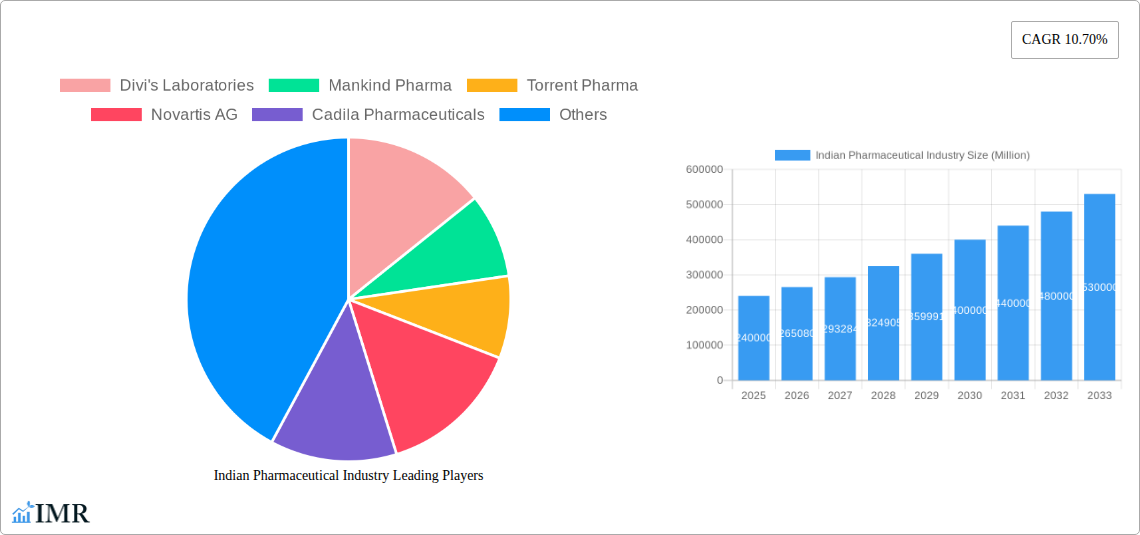

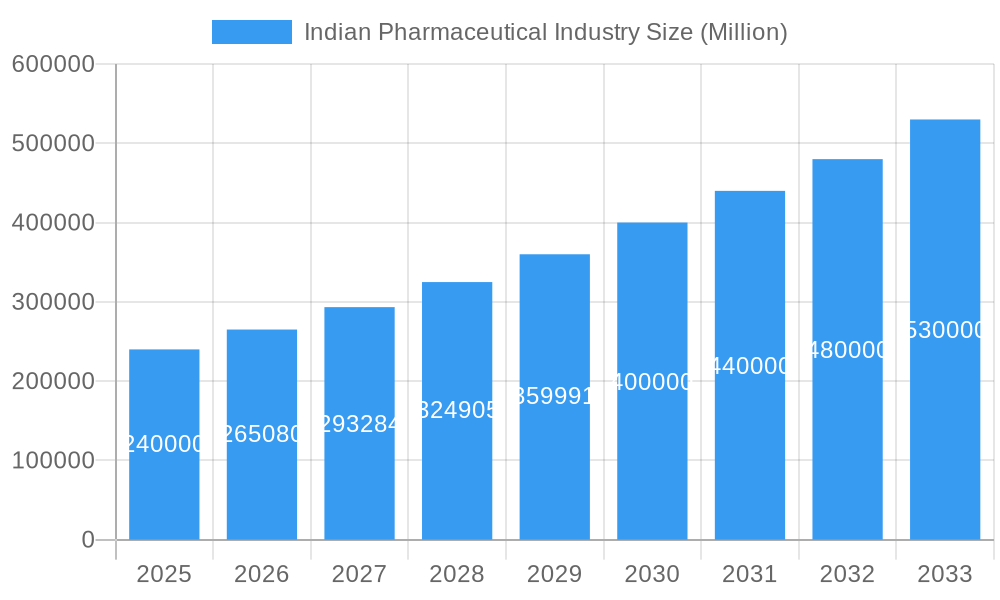

The Indian pharmaceutical market, valued at approximately ₹2 trillion (USD 240 billion) in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 10.70% from 2025 to 2033. This expansion is fueled by several key drivers: a burgeoning population with increasing healthcare needs, rising prevalence of chronic diseases like diabetes and cardiovascular ailments, growing government initiatives promoting affordable healthcare access (Ayushman Bharat, for example), and a robust generic drug manufacturing base. Furthermore, increasing investments in research and development, coupled with a favorable regulatory environment, are further accelerating market growth. However, challenges such as stringent regulatory approvals, price controls on essential medicines, and increasing competition from international players pose potential restraints. The market is segmented by drug type (prescription, OTC, generic) and therapeutic category (anti-infectives, cardiovascular, gastrointestinal, anti-diabetic, respiratory, dermatologicals, musculoskeletal, nervous system, and others). Major players like Sun Pharma, Cipla, Dr. Reddy's, and Aurobindo Pharma dominate the landscape, alongside multinational giants like Novartis and Pfizer, competing intensely across various segments.

Indian Pharmaceutical Industry Market Size (In Billion)

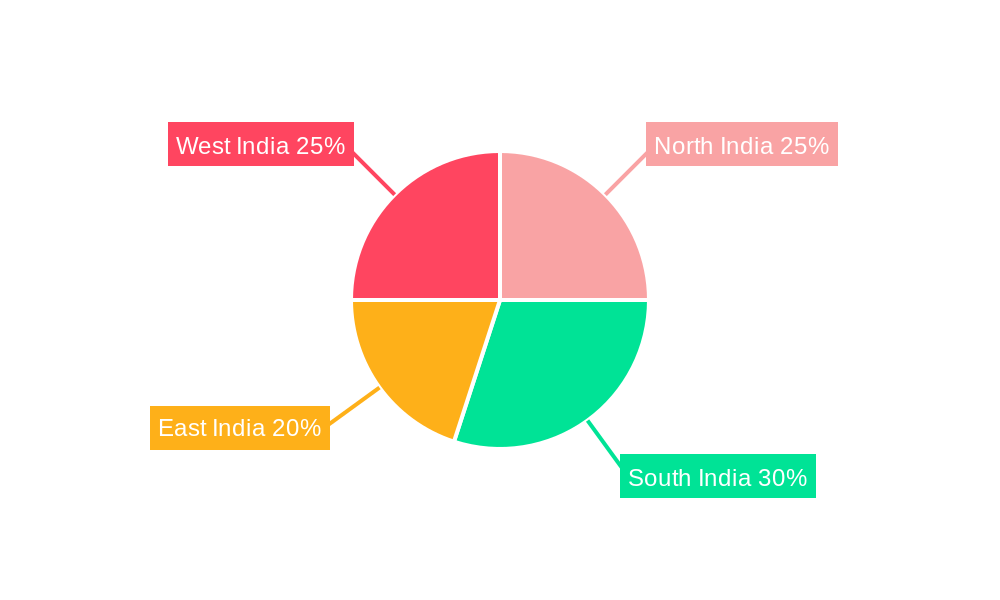

The regional distribution demonstrates significant variations across India. While precise figures are not provided, it's reasonable to assume that states like Maharashtra, Gujarat, and Andhra Pradesh, being prominent pharmaceutical manufacturing hubs, contribute a larger share to the overall market. The growth will likely be driven by increased access to healthcare in less developed regions, leading to a more even distribution of market share across North, South, East, and West India over the forecast period. Further expansion is anticipated through the increasing adoption of innovative delivery systems, biosimilars, and focus on specialized therapeutic areas such as oncology and immunology. The continuous improvement in healthcare infrastructure and the rise of telemedicine also contribute to the positive outlook. However, maintaining price competitiveness while adhering to stringent quality standards will remain crucial for sustained success in this dynamic market.

Indian Pharmaceutical Industry Company Market Share

Indian Pharmaceutical Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Indian pharmaceutical industry, encompassing market dynamics, growth trends, key players, and future outlook. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report leverages extensive data analysis and expert insights to deliver actionable intelligence for industry professionals. This report is crucial for investors, pharmaceutical companies, and regulatory bodies seeking a deep understanding of this rapidly evolving market. The report segments the market by drug type (Prescription Drugs, OTC Drugs, Generic Drugs) and therapeutic category (Anti-Infectives, Cardiovascular, Gastrointestinal, Anti-Diabetic, Respiratory, Dermatologicals, Musculo-Skeletal System, Nervous System, Others).

Indian Pharmaceutical Industry Market Dynamics & Structure

The Indian pharmaceutical industry is characterized by a complex interplay of factors influencing its growth and structure. Market concentration is moderate, with a few large players dominating certain segments alongside numerous smaller companies specializing in niche areas. Technological innovation, particularly in generics and biosimilars, is a significant driver, while regulatory frameworks, including those governing drug approvals and pricing, play a crucial role. The market faces competition from both domestic and international players, with pricing pressure and the availability of substitute therapies influencing market dynamics. End-user demographics, driven by India's large and growing population, are a significant factor, although access remains a challenge in certain areas. M&A activity is robust, with larger companies acquiring smaller ones to expand their product portfolios and market reach.

- Market Concentration: Moderate, with top 10 players holding xx% market share in 2024.

- Technological Innovation: Focus on generics, biosimilars, and API manufacturing.

- Regulatory Framework: Stringent regulations impacting drug approvals and pricing.

- Competitive Substitutes: Availability of generic and biosimilar alternatives influencing pricing.

- End-User Demographics: Large and growing population driving demand, but access remains a challenge.

- M&A Activity: Significant M&A activity (xx deals valued at xx Million USD in 2024).

Indian Pharmaceutical Industry Growth Trends & Insights

The Indian pharmaceutical market has exhibited robust growth over the past years, driven by factors such as increasing healthcare expenditure, rising prevalence of chronic diseases, and a growing demand for affordable medicines. The market size is projected to reach xx Million units by 2025, expanding at a CAGR of xx% during the forecast period (2025-2033). This growth is influenced by rising adoption rates of innovative therapies, technological disruptions leading to improved manufacturing processes and drug delivery systems, and changing consumer behavior favoring greater self-medication and reliance on over-the-counter drugs. The increasing affordability and accessibility of healthcare, particularly in rural areas, will significantly impact the market’s growth trajectory. However, challenges such as regulatory hurdles and pricing pressures persist.

Dominant Regions, Countries, or Segments in Indian Pharmaceutical Industry

The Indian pharmaceutical market exhibits significant geographic diversity, with varying growth trajectories and market share contributions across its regions. While the industry's reach is widespread, specific states boasting well-developed healthcare infrastructure command a dominant share of the market. Among drug types, Generic Drugs continue to lead, underpinned by their inherent affordability and widespread accessibility. Similarly, key therapeutic categories such as Anti-Infectives and Cardiovascular drugs are major contributors to market share, driven by the high prevalence of associated conditions and ongoing advancements in treatment development.

-

Key Growth Drivers:

- Escalating healthcare expenditure and increased health insurance penetration.

- The growing burden of chronic diseases, including Diabetes and Cardiovascular conditions.

- Supportive government policies and initiatives fostering domestic manufacturing capabilities.

- A strong and expanding export market fueled by global demand for high-quality, cost-effective generic medicines.

-

Dominant Segments:

- Drug Type: Generic Drugs are the leading segment, representing approximately 65-70% of the market share in 2024.

- Therapeutic Category: Anti-Infectives (estimated 20-25% market share in 2024) and Cardiovascular drugs (estimated 15-20% market share in 2024) are the dominant therapeutic areas.

Indian Pharmaceutical Industry Product Landscape

The Indian pharmaceutical industry offers a broad spectrum of products ranging from generic drugs to innovative biologics. Continuous innovation is focused on improving drug efficacy, reducing side effects, and developing novel drug delivery systems. Unique selling propositions often emphasize cost-effectiveness, efficacy, and improved patient compliance. Technological advancements, such as AI-driven drug discovery and personalized medicine approaches, are driving further innovation.

Key Drivers, Barriers & Challenges in Indian Pharmaceutical Industry

Key Drivers:

- Rising healthcare expenditure and insurance coverage.

- Growing prevalence of chronic diseases.

- Government initiatives promoting domestic manufacturing.

- Strong export market for generic drugs and APIs.

Key Challenges:

- Stringent regulatory requirements leading to longer approval times.

- Price controls and intense competition impacting profitability.

- Supply chain disruptions and dependence on raw material imports.

- Intellectual property rights concerns and counterfeit drug issues.

Emerging Opportunities in Indian Pharmaceutical Industry

- Expanding access to healthcare in rural areas.

- Growing demand for biosimilars and biologics.

- Focus on personalized medicine and targeted therapies.

- Increasing adoption of digital health technologies.

Growth Accelerators in the Indian Pharmaceutical Industry

The Indian pharmaceutical industry's growth is set to be significantly amplified by cutting-edge technological advancements. Innovations like Artificial Intelligence (AI) in drug discovery and the burgeoning field of personalized medicine are poised to revolutionize how treatments are developed and delivered. Furthermore, strategic collaborations between Indian and international pharmaceutical companies are expected to foster a synergistic environment, driving innovation and expanding market reach. The exploration of new therapeutic frontiers and the penetration of previously untapped markets will also play a crucial role in accelerating the industry's upward trajectory.

Key Players Shaping the Indian Pharmaceutical Industry Market

Notable Milestones in Indian Pharmaceutical Industry Sector

- February 2022: Dr. Reddy's Laboratories Ltd. secured crucial approval from the Drug Controller General of India (DCGI) for its Sputnik Light vaccine, bolstering India's COVID-19 vaccination efforts.

- November 2021: Cipla Limited obtained Emergency Use Authorization (EUA) for Molnupiravir, an oral antiviral medication, contributing significantly to the treatment landscape for COVID-19 patients.

In-Depth Indian Pharmaceutical Industry Market Outlook

The Indian pharmaceutical industry is strategically positioned for sustained and robust growth in the coming years. This positive outlook is underpinned by a confluence of factors, including rapid technological advancements, a consistent increase in healthcare expenditure, and a widening access to essential healthcare services across the nation. Key to achieving continued success will be the formation of strategic alliances, a concentrated effort on developing treatments for emerging therapeutic areas, and the effective utilization of digital health technologies. While the market presents substantial opportunities for both established domestic companies and international entrants, navigating the intricate landscape of regulatory frameworks and intense market competition will remain paramount for achieving long-term prosperity.

Indian Pharmaceutical Industry Segmentation

-

1. Therapeutic Category

- 1.1. Anti-Infectives

- 1.2. Cardiovascular

- 1.3. Gastrointestinal

- 1.4. Anti Diabetic

- 1.5. Respiratory

- 1.6. Dermatologicals

- 1.7. Musculo-Skeletal System

- 1.8. Nervous System

- 1.9. Others

-

2. Drug Type

-

2.1. Prescription Drug

- 2.1.1. Branded Drugs

- 2.1.2. Generic Drugs

- 2.2. OTC Drugs

-

2.1. Prescription Drug

Indian Pharmaceutical Industry Segmentation By Geography

- 1. India

Indian Pharmaceutical Industry Regional Market Share

Geographic Coverage of Indian Pharmaceutical Industry

Indian Pharmaceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 5.1.1. Anti-Infectives

- 5.1.2. Cardiovascular

- 5.1.3. Gastrointestinal

- 5.1.4. Anti Diabetic

- 5.1.5. Respiratory

- 5.1.6. Dermatologicals

- 5.1.7. Musculo-Skeletal System

- 5.1.8. Nervous System

- 5.1.9. Others

- 5.2. Market Analysis, Insights and Forecast - by Drug Type

- 5.2.1. Prescription Drug

- 5.2.1.1. Branded Drugs

- 5.2.1.2. Generic Drugs

- 5.2.2. OTC Drugs

- 5.2.1. Prescription Drug

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 6. Indian Pharmaceutical Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 6.1.1. Anti-Infectives

- 6.1.2. Cardiovascular

- 6.1.3. Gastrointestinal

- 6.1.4. Anti Diabetic

- 6.1.5. Respiratory

- 6.1.6. Dermatologicals

- 6.1.7. Musculo-Skeletal System

- 6.1.8. Nervous System

- 6.1.9. Others

- 6.2. Market Analysis, Insights and Forecast - by Drug Type

- 6.2.1. Prescription Drug

- 6.2.1.1. Branded Drugs

- 6.2.1.2. Generic Drugs

- 6.2.2. OTC Drugs

- 6.2.1. Prescription Drug

- 6.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Divi's Laboratories

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mankind Pharma

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Torrent Pharma

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Novartis AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cadila Pharmaceuticals

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Aurobindo Pharma Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Merck & Co Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sun Pharmaceutical Industries Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Cipla Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Lupin Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Biocon Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 GlaxoSmithKline plc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Dr Reddy's Laboratories Ltd

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Abbott

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Pfizer Inc

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Divi's Laboratories

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indian Pharmaceutical Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Indian Pharmaceutical Industry Share (%) by Company 2025

List of Tables

- Table 1: Indian Pharmaceutical Industry Revenue Million Forecast, by Therapeutic Category 2020 & 2033

- Table 2: Indian Pharmaceutical Industry Revenue Million Forecast, by Drug Type 2020 & 2033

- Table 3: Indian Pharmaceutical Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Indian Pharmaceutical Industry Revenue Million Forecast, by Therapeutic Category 2020 & 2033

- Table 5: Indian Pharmaceutical Industry Revenue Million Forecast, by Drug Type 2020 & 2033

- Table 6: Indian Pharmaceutical Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Pharmaceutical Industry?

The projected CAGR is approximately 10.70%.

2. Which companies are prominent players in the Indian Pharmaceutical Industry?

Key companies in the market include Divi's Laboratories, Mankind Pharma, Torrent Pharma, Novartis AG, Cadila Pharmaceuticals, Aurobindo Pharma Limited, Merck & Co Inc, Sun Pharmaceutical Industries Ltd, Cipla Inc, Lupin Limited, Biocon Limited, GlaxoSmithKline plc, Dr Reddy's Laboratories Ltd, Abbott, Pfizer Inc.

3. What are the main segments of the Indian Pharmaceutical Industry?

The market segments include Therapeutic Category, Drug Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Low Cost of Production and Increased R&D Activities; Increased Expenditure on Healthcare and Medicine.

6. What are the notable trends driving market growth?

The Respiratory Therapeutic Category Segment is Expected to Show Healthy Market Growth in the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of a Stable Pricing and Policy Environment; Lack in Development of Innovative Drugs.

8. Can you provide examples of recent developments in the market?

In February 2022, Dr. Reddy's Laboratories Ltd. announced that the Drugs Controller General of India (DCGI) had approved the single-shot Sputnik Light vaccine for restricted use in an emergency in India.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Pharmaceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Pharmaceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Pharmaceutical Industry?

To stay informed about further developments, trends, and reports in the Indian Pharmaceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence