Key Insights

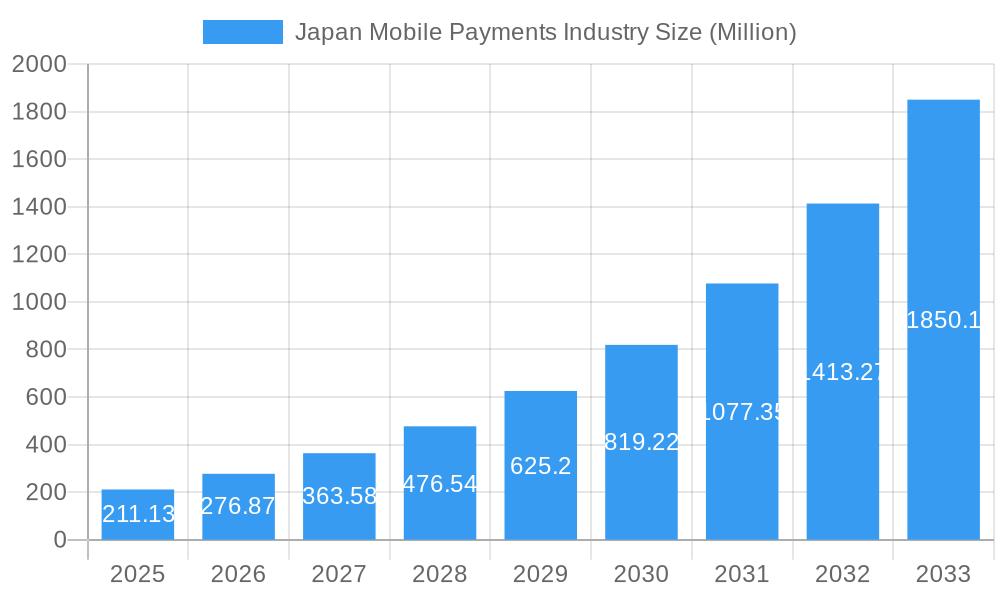

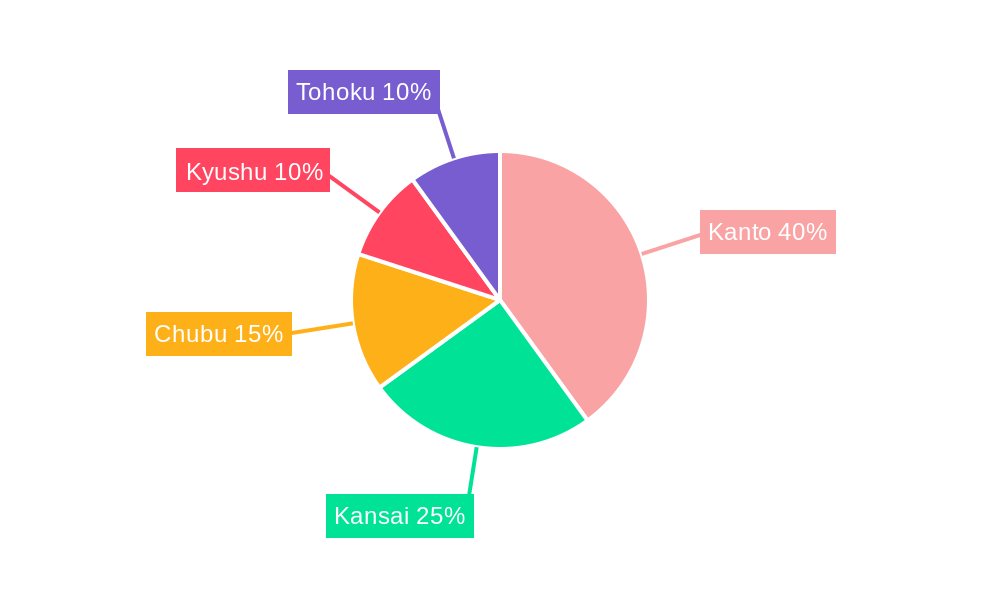

The Japan mobile payments market, valued at $211.13 million in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 31.04% from 2025 to 2033. This surge is driven by several key factors. Firstly, increasing smartphone penetration and digital literacy amongst the Japanese population are creating a fertile ground for mobile payment adoption. Secondly, government initiatives promoting cashless transactions and a growing preference for contactless payment methods are accelerating market expansion. The rise of e-commerce and the increasing popularity of online services across retail, entertainment, healthcare, and hospitality sectors are further fueling demand. Furthermore, the presence of established players like PayPay, Visa, Mastercard, and Rakuten, alongside domestic financial institutions like Mitsubishi UFJ Financial Group and Credit Saison, fosters competition and innovation within the ecosystem. The market is segmented by payment mode (Point of Sale and Online Sale) and end-user industry, with retail and entertainment likely leading the adoption curve. Regional variations exist, with the Kanto and Kansai regions expected to dominate due to higher population density and economic activity.

Japan Mobile Payments Industry Market Size (In Million)

However, the market's growth isn't without challenges. While security concerns surrounding mobile payments are being addressed through robust security protocols, consumer trust and apprehension regarding data privacy remain a significant factor. Furthermore, the existing robust cash-based infrastructure in Japan presents a gradual transition challenge for widespread mobile payments adoption. Despite these restraints, the long-term outlook for the Japan mobile payments market remains exceptionally positive, fueled by continuous technological advancements and a steadily shifting consumer preference toward convenient and digital payment solutions. The market's projected growth signifies a significant shift in Japan's financial landscape, promising a future increasingly dominated by mobile payment solutions.

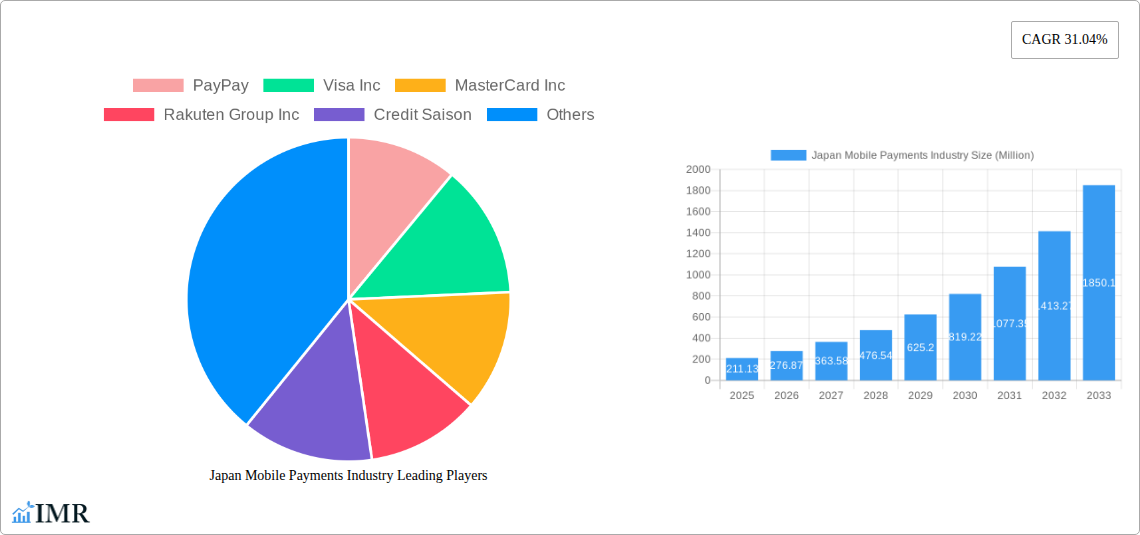

Japan Mobile Payments Industry Company Market Share

Japan Mobile Payments Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Japan mobile payments industry, covering market dynamics, growth trends, key players, and future outlook. With a focus on the parent market (mobile payments) and its child markets (Point of Sale, Online Sale, Retail, Entertainment, Healthcare, Hospitality etc.), this report is an essential resource for industry professionals, investors, and strategic decision-makers. The study period spans 2019-2033, with 2025 as the base and estimated year, and a forecast period of 2025-2033. The historical period covered is 2019-2024. Expected market value in Million units is provided wherever available.

Japan Mobile Payments Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory environment, and market trends within the Japanese mobile payments industry. We delve into market concentration, examining the market share held by key players like PayPay, Visa Inc, MasterCard Inc, Rakuten Group Inc, and others. The analysis also incorporates the influence of technological innovation, regulatory frameworks (including their impact on market entry and competition), the presence of competitive substitute payment methods, and prevailing end-user demographics. Further, the report explores the impact of mergers and acquisitions (M&A) activities on market consolidation and innovation.

- Market Concentration: PayPay holds a significant market share (xx%), followed by Visa Inc (xx%), MasterCard Inc (xx%), and Rakuten Group Inc (xx%). The remaining market share is distributed among numerous smaller players.

- Technological Innovation Drivers: The rapid adoption of smartphones and advancements in NFC technology are key drivers. However, challenges remain in overcoming consumer resistance to adopting new technologies and ensuring seamless integration across different platforms.

- Regulatory Framework: The Japanese government's focus on promoting digitalization and fintech has created a supportive regulatory environment, while simultaneously imposing stringent data privacy regulations.

- Competitive Product Substitutes: Traditional cash payments and credit cards continue to compete, but mobile payments are gradually gaining traction.

- End-User Demographics: Younger generations show higher adoption rates of mobile payments compared to older demographics.

- M&A Trends: The past five years have seen xx M&A deals in the Japanese mobile payments sector, mostly focused on smaller players being acquired by larger companies.

Japan Mobile Payments Industry Growth Trends & Insights

The Japanese mobile payments market is experiencing a dynamic evolution, driven by increasing smartphone penetration, evolving consumer behavior, and the integration of innovative technologies. This section delves into the market's trajectory, examining its size, adoption rates, and the fundamental shifts in how consumers conduct transactions. Through a combination of robust quantitative data and qualitative insights, we uncover key trends such as the projected Compound Annual Growth Rate (CAGR), widespread market penetration, and the significant impact of advancements like biometric authentication. Furthermore, we explore how changing consumer preferences and spending habits are actively shaping the industry's future. The market is anticipated to reach approximately [Insert specific number] million units by 2025, with an estimated CAGR of [Insert specific percentage]% for the period of 2025-2033.

(Note: This section would contain a detailed 600-word analysis based on the referenced XXX data source, detailing market size evolution, adoption rates, technological disruptions, and consumer behavior shifts, supported by specific metrics (e.g., CAGR, market penetration).)

Dominant Regions, Countries, or Segments in Japan Mobile Payments Industry

This section pinpoints the leading geographical regions, specific countries within Japan, and key segments that are propelling the growth of the mobile payments industry. We dissect the contributing factors behind their dominance, including supportive economic policies, advancements in digital infrastructure, and the ingrained preferences of Japanese consumers. The analysis also scrutinizes current market share and forecasts future growth potential across these dominant areas.

- By Mode of Payment: While Point-of-Sale (POS) payments currently hold a significant market share of [Insert specific percentage]%, online payment solutions are exhibiting rapid growth, capturing [Insert specific percentage]% of the market. This indicates a strong shift towards digital transactions for both in-person and remote purchases.

- By End-user Industry: The retail sector remains the largest contributor to mobile payment adoption, accounting for [Insert specific percentage]% of the market. The entertainment and hospitality sectors follow closely, representing [Insert specific percentage]% and [Insert specific percentage]% respectively. Promising growth potential is also identified within the healthcare sector and other emerging end-user industries as digital payment integration becomes more prevalent.

- Key Drivers: The widespread adoption of mobile payments in Japan is significantly fueled by proactive government initiatives aimed at promoting digital transactions, coupled with an exceptionally high smartphone penetration rate. Furthermore, a growing consumer inclination towards convenient and contactless transaction methods is a crucial catalyst for sustained market expansion. (This section will include detailed explanations of the above bullet points)

Japan Mobile Payments Industry Product Landscape

The Japanese mobile payment ecosystem is characterized by a rich and diverse array of products, each offering a unique blend of features and functionalities designed to cater to varied user needs. Core offerings include seamless contactless payment capabilities powered by Near Field Communication (NFC) technology, efficient QR code scanning for quick transactions, and an increasing integration of advanced biometric authentication methods such as fingerprint and facial recognition for enhanced security. Leading providers are in a constant cycle of innovation, introducing value-added features like integrated loyalty programs, attractive cashback incentives, and robust security enhancements to elevate the user experience and broaden their customer base. This competitive environment not only fosters continuous innovation but also drives significant improvements in transaction speed, security protocols, and the overall intuitiveness of the user interface across all payment platforms.

Key Drivers, Barriers & Challenges in Japan Mobile Payments Industry

Several factors are propelling the growth of the Japanese mobile payments market, including government support for digitalization, increasing smartphone penetration, and consumer demand for convenience. However, challenges remain, including security concerns, a preference for cash among older generations, and the need for wider acceptance across various merchants. Addressing these challenges through robust security measures, educational campaigns, and improved merchant adoption programs is crucial for sustained market growth.

Key Drivers: Technological advancements, government initiatives (e.g., cashless society promotion), rising smartphone penetration.

Key Challenges: Security concerns, overcoming cash preference, ensuring merchant adoption, data privacy regulations.

Emerging Opportunities in Japan Mobile Payments Industry

Untapped opportunities exist in expanding mobile payment adoption in less-penetrated segments, such as rural areas and older demographics. Furthermore, the integration of mobile payments with other services, such as loyalty programs and transportation, presents significant opportunities. The development of innovative applications, such as personalized payment solutions and enhanced security features using biometric authentication and blockchain technology, will further shape the future of the market.

Growth Accelerators in the Japan Mobile Payments Industry

Several factors will accelerate long-term growth, including continued technological advancements in mobile payment technologies, strategic partnerships between financial institutions and technology companies, and expansion into new markets and segments. Government support for digital transformation and a growing young population accustomed to digital solutions are additional accelerators.

Key Players Shaping the Japan Mobile Payments Industry Market

- PayPay: A dominant force in the Japanese market, known for its aggressive promotions and widespread merchant network.

- Visa Inc: A global leader in digital payments, actively expanding its presence and offerings in Japan's mobile payment sector.

- MasterCard Inc: Similar to Visa, MasterCard is a key player, focusing on innovative solutions and partnerships to capture market share.

- Rakuten Group Inc: Leveraging its vast e-commerce and digital services ecosystem, Rakuten offers integrated mobile payment solutions through Rakuten Pay.

- Credit Saison: A major credit card company in Japan, actively involved in developing and promoting mobile payment services.

- Mitsubishi UFJ Financial Group: One of Japan's largest financial institutions, investing heavily in fintech and digital payment infrastructure.

- JCB: A prominent Japanese credit card company with a significant stake in the domestic mobile payment market.

- PayPal: While a global player, PayPal continues to adapt its services for the Japanese market, focusing on cross-border and e-commerce transactions.

- Aeon Credit Service: A significant player in the retail and credit sector, offering mobile payment solutions tied to its extensive retail network.

- Resona Holdings: Another major financial group in Japan, actively participating in the development of digital payment solutions.

Notable Milestones in Japan Mobile Payments Industry Sector

- April 2023: In a significant stride towards enhanced security and convenience, PayPay, in collaboration with Yahoo Japan and Z Holdings Group, introduced face biometrics payments at select convenience stores. This partnership also involved ASKUL and Demae-can, expanding the reach of this advanced payment method.

- February 2023: Mitsubishi UFJ Financial Group (MUFG) demonstrated its commitment to global fintech innovation by launching a USD 100 million fund specifically targeting startups in Indonesia, signaling a broader strategic investment in emerging digital payment markets.

In-Depth Japan Mobile Payments Industry Market Outlook

The Japanese mobile payments market exhibits significant growth potential driven by technological advancements, increasing smartphone penetration, and government support for digital transformation. Strategic partnerships and expansion into new market segments will further propel growth. The focus on enhancing security and user experience will be crucial for sustained market expansion and wider consumer adoption.

Japan Mobile Payments Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Other Points of Sale

-

1.2. Online Sale

- 1.2.1. Card Pay

- 1.2.2. Other On

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Japan Mobile Payments Industry Segmentation By Geography

- 1. Japan

Japan Mobile Payments Industry Regional Market Share

Geographic Coverage of Japan Mobile Payments Industry

Japan Mobile Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 31.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Other Points of Sale

- 5.1.2. Online Sale

- 5.1.2.1. Card Pay

- 5.1.2.2. Other On

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Japan Mobile Payments Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6.1.1. Point of Sale

- 6.1.1.1. Card Pay

- 6.1.1.2. Digital Wallet (includes Mobile Wallets)

- 6.1.1.3. Cash

- 6.1.1.4. Other Points of Sale

- 6.1.2. Online Sale

- 6.1.2.1. Card Pay

- 6.1.2.2. Other On

- 6.1.1. Point of Sale

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. Entertainment

- 6.2.3. Healthcare

- 6.2.4. Hospitality

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 PayPay

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Visa Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 MasterCard Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Rakuten Group Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Credit Saison

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mitsubishi UFJ Financial Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 JCB

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 PayPal*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Aeon Credit Service

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Resona Holdings

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 PayPay

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Mobile Payments Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Japan Mobile Payments Industry Share (%) by Company 2025

List of Tables

- Table 1: Japan Mobile Payments Industry Revenue Million Forecast, by Mode of Payment 2020 & 2033

- Table 2: Japan Mobile Payments Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Japan Mobile Payments Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Japan Mobile Payments Industry Revenue Million Forecast, by Mode of Payment 2020 & 2033

- Table 5: Japan Mobile Payments Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Japan Mobile Payments Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Mobile Payments Industry?

The projected CAGR is approximately 31.04%.

2. Which companies are prominent players in the Japan Mobile Payments Industry?

Key companies in the market include PayPay, Visa Inc, MasterCard Inc, Rakuten Group Inc, Credit Saison, Mitsubishi UFJ Financial Group, JCB, PayPal*List Not Exhaustive, Aeon Credit Service, Resona Holdings.

3. What are the main segments of the Japan Mobile Payments Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 211.13 Million as of 2022.

5. What are some drivers contributing to market growth?

High Proliferation of E-commerce. including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power andand Increasing Internet Penetration in Japan Driving the Market.

6. What are the notable trends driving market growth?

Development of M-Commerce Platforms and Increasing Internet Penetration in Japan Driving the Market.

7. Are there any restraints impacting market growth?

Lack of a standard legislative policy remains especially in the case of cross-border transactions.

8. Can you provide examples of recent developments in the market?

April 2023 - PayPay and Yahoo Japan have launched face biometrics payments at convenience stores. The self-service POS cash register pilot, similar to the one unveiled by Glory in Niigata City last year, also saw the collaboration of e-commerce company Z Holdings Group ASKUL and its subsidiary Demae-can, a food delivery service platform.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Mobile Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Mobile Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Mobile Payments Industry?

To stay informed about further developments, trends, and reports in the Japan Mobile Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence