Key Insights

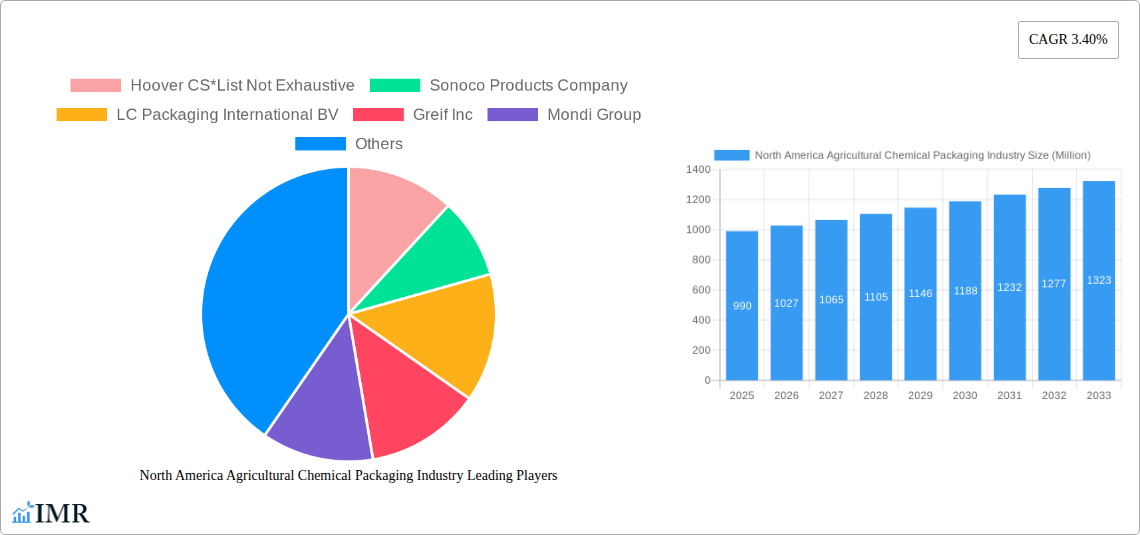

The North American agricultural chemical packaging market, valued at $0.99 billion in 2025, is projected to experience steady growth, driven by the increasing demand for efficient and safe packaging solutions within the agricultural sector. This growth is fueled by several factors. Firstly, the rising global population necessitates enhanced agricultural yields, leading to increased pesticide and fertilizer usage, consequently boosting demand for specialized packaging. Secondly, stringent government regulations regarding chemical handling and environmental protection are driving the adoption of sustainable and robust packaging materials like recyclable plastics and paper-based alternatives. This shift away from less environmentally friendly options presents significant opportunities for manufacturers focused on innovation and eco-conscious solutions. Finally, advancements in packaging technology, including improved barrier properties and tamper-evident seals, contribute to enhanced product safety and shelf life, further propelling market growth. Competition among key players like Sonoco Products Company, Greif Inc., and Mondi Group is intense, pushing innovation and efficiency gains.

However, the market faces certain challenges. Fluctuations in raw material prices, particularly for plastics and metals, can impact profitability. Additionally, the increasing adoption of sustainable packaging materials requires significant investments in research and development, posing a barrier to entry for some companies. Despite these restraints, the long-term outlook remains positive, particularly given the projected growth in agricultural production and the ongoing need for safe and effective chemical packaging solutions. Market segmentation reveals significant potential in plastic-based packaging due to its versatility and cost-effectiveness, while the growing preference for eco-friendly solutions will drive the adoption of paper and paperboard alternatives. The continued focus on efficient supply chains and improved logistics will also play a crucial role in shaping the future landscape of this dynamic market.

North America Agricultural Chemical Packaging Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the North America agricultural chemical packaging industry, encompassing market size, growth trends, competitive landscape, and future outlook. From the parent market of packaging to the child market of agricultural chemical packaging, this report delivers critical insights for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with 2025 as the base year and forecast period spanning 2025-2033. The historical period analyzed is 2019-2024. Market values are presented in million units.

North America Agricultural Chemical Packaging Industry Market Dynamics & Structure

This section analyzes the market's competitive intensity, technological advancements, regulatory landscape, substitute products, end-user demographics, and mergers & acquisitions (M&A) activity. The North American agricultural chemical packaging market exhibits a moderately concentrated structure with key players holding significant market share. Technological innovation, driven by sustainability concerns and efficiency demands, is a key driver. Stringent environmental regulations, particularly concerning plastic waste, significantly impact packaging choices. Alternative packaging materials are emerging as viable substitutes, challenging the dominance of traditional options. The agricultural sector's demographic shifts, including farm consolidation and technological adoption, influence packaging demand. M&A activity remains moderate, with strategic acquisitions focused on enhancing product portfolios and expanding geographical reach.

- Market Concentration: xx% market share held by top 5 players (2024).

- Technological Innovation: Focus on sustainable materials (bioplastics, recycled content), improved barrier properties, and lightweight packaging.

- Regulatory Framework: Increasingly stringent regulations on plastic waste and hazardous material handling.

- Competitive Substitutes: Growth of biodegradable and compostable packaging alternatives.

- End-User Demographics: Shift towards larger, more technologically advanced farms.

- M&A Trends: xx M&A deals observed in the last 5 years (2019-2024), driven by expansion and diversification strategies.

North America Agricultural Chemical Packaging Industry Growth Trends & Insights

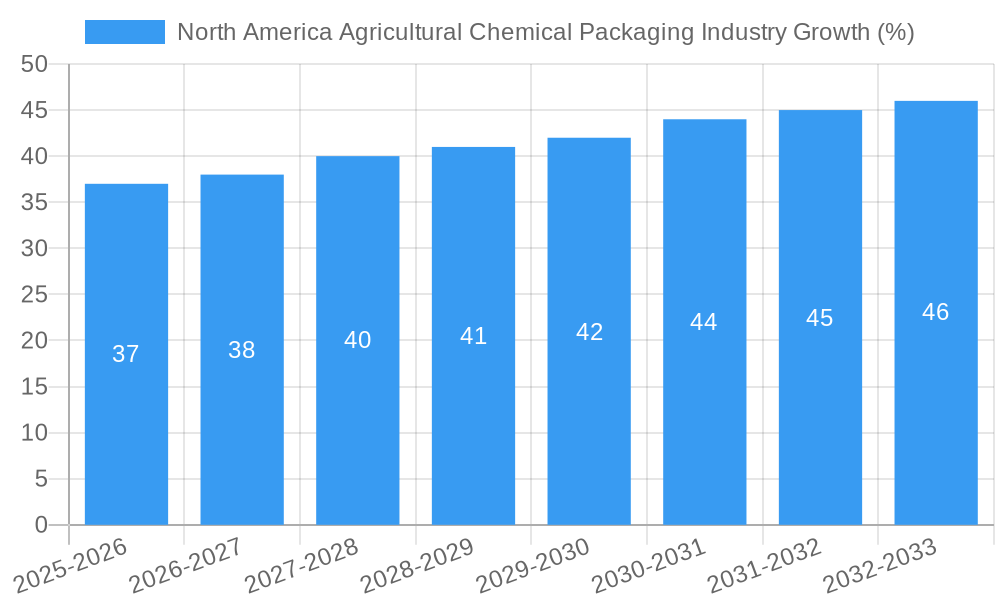

The North America agricultural chemical packaging market has witnessed consistent growth over the past years, driven by the increasing demand for agricultural chemicals and the focus on efficient and safe packaging solutions. The market size is expected to exhibit a CAGR of xx% during the forecast period (2025-2033), reaching xx million units by 2033. This growth is attributed to several factors, including rising agricultural production, technological advancements in packaging materials and designs, and increasing government support for the agricultural sector. Consumer behavior shifts towards sustainable and eco-friendly packaging are also influencing market trends. The adoption rate of innovative packaging solutions, such as smart packaging and recyclable materials, is gradually increasing. However, factors like economic fluctuations and potential regulatory changes could influence the market's trajectory.

Dominant Regions, Countries, or Segments in North America Agricultural Chemical Packaging Industry

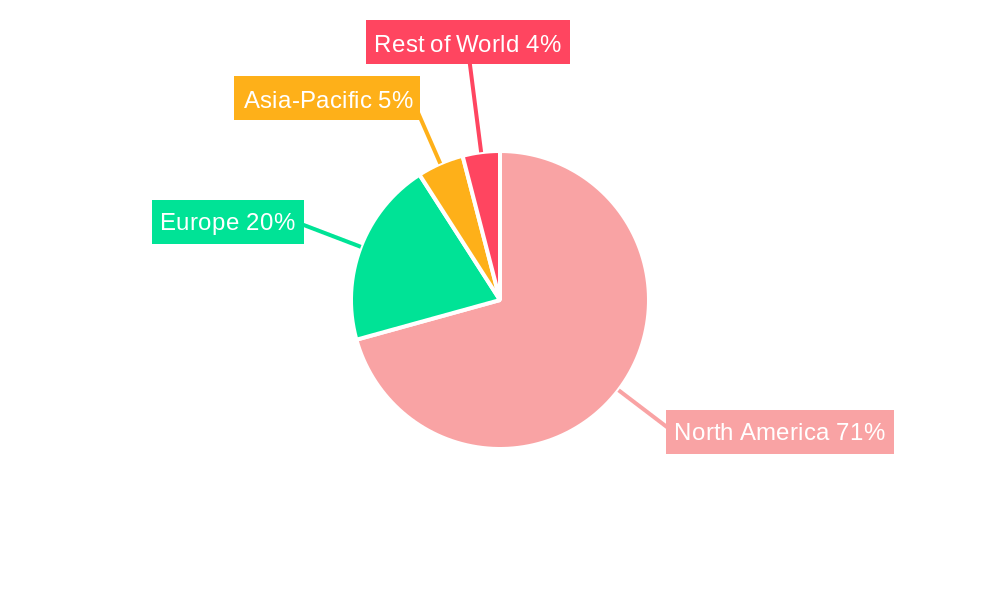

The North American agricultural chemical packaging market is geographically diverse, with significant variations in growth rates and market share across different regions and segments. The Midwest and Western regions of the United States, known for extensive agricultural activities, show the highest market share and growth potential. Canada's agricultural heartland also contributes significantly.

By Product Type: Containers and cans currently dominate the market, followed by bags and pouches. IBCs are gaining traction due to their efficiency in handling large volumes.

- Bags and Pouches: xx million units (2024). Growth driven by ease of use and cost-effectiveness for smaller packaging needs.

- Containers and Cans: xx million units (2024). Dominant due to suitability for various chemical types and robust protection.

- Intermediate Bulk Containers (IBCs): xx million units (2024). Growth driven by logistical efficiency for bulk handling.

- Other Product Types: xx million units (2024). Includes specialized containers and customized solutions.

By Material Type: Plastic remains the dominant material due to its versatility and cost-effectiveness, although concerns over sustainability are driving the increased adoption of paper and paperboard.

- Plastic: xx million units (2024). High volume due to its cost-effectiveness and versatility.

- Paper and Paperboard: xx million units (2024). Growing due to environmental concerns and increasing demand for sustainable alternatives.

- Metal: xx million units (2024). Used for specialized applications requiring high barrier properties and durability.

- Other Materials: xx million units (2024). Includes composites and biodegradable materials.

By Application Type: Fertilizers currently hold the largest market share, followed by pesticides and herbicides.

- Fertilizers: xx million units (2024). High demand driven by increasing agricultural production.

- Pesticides: xx million units (2024). Significant demand due to crop protection requirements.

- Herbicides: xx million units (2024). Growing demand driven by weed control needs.

- Other Application Types: xx million units (2024). Includes fungicides, insecticides, and other agricultural chemicals.

North America Agricultural Chemical Packaging Industry Product Landscape

The agricultural chemical packaging market is characterized by continuous innovation in materials, design, and functionality. Recent advancements include the development of lightweight, high-barrier films that reduce material usage and improve product protection. The integration of smart packaging technologies, providing real-time tracking and condition monitoring, is gaining traction. Recyclable and compostable packaging options are increasingly being adopted to address sustainability concerns. Unique selling propositions focus on enhanced product safety, extended shelf life, and reduced environmental impact.

Key Drivers, Barriers & Challenges in North America Agricultural Chemical Packaging Industry

Key Drivers:

- Increasing demand for agricultural chemicals driven by global population growth and food security concerns.

- Growing adoption of sustainable and eco-friendly packaging solutions.

- Technological advancements in packaging materials and design.

- Favorable government policies and incentives promoting sustainable agriculture.

Challenges & Restraints:

- Fluctuations in raw material prices, impacting packaging costs.

- Stringent environmental regulations and compliance requirements.

- Intense competition among packaging manufacturers.

- Supply chain disruptions impacting the timely delivery of packaging materials. xx% increase in lead times observed in 2023 (estimated).

Emerging Opportunities in North America Agricultural Chemical Packaging Industry

- Growth of the organic and sustainable agriculture sector, driving demand for eco-friendly packaging.

- Increasing adoption of smart packaging technologies for improved traceability and product safety.

- Development of innovative packaging solutions for specialized agricultural chemicals.

- Expansion into untapped markets in developing regions of North America.

Growth Accelerators in the North America Agricultural Chemical Packaging Industry

Long-term growth in this sector will be propelled by strategic partnerships between packaging manufacturers and agricultural chemical producers, fostering collaborative innovation. Advancements in materials science, enabling the development of more sustainable and efficient packaging options, will also be pivotal. Expansion into new geographical markets and diversification into adjacent segments will further fuel market growth.

Key Players Shaping the North America Agricultural Chemical Packaging Industry Market

- Hoover CS *List Not Exhaustive

- Sonoco Products Company

- LC Packaging International BV

- Greif Inc

- Mondi Group

- Tri Rinse

- ProAmpac LLC

- Mauser Packaging Solutions

- Silgan Holdings

Notable Milestones in North America Agricultural Chemical Packaging Industry Sector

- April 2022: Greif Inc. announced the divestiture of its Flexible Packaging joint venture (FPS) for USD 123 million, aiming to reduce debt.

- April 2022: LC Packaging collaborated with M.B. Nieuwenhuijse B.V. and Plastic Bank to prevent 50,000 kgs of plastic from entering the ocean, promoting sustainable sourcing and recyclable products.

In-Depth North America Agricultural Chemical Packaging Industry Market Outlook

The North America agricultural chemical packaging market is poised for continued expansion, driven by technological innovation, increasing sustainability concerns, and growth in the agricultural sector. Strategic investments in research and development, focusing on eco-friendly materials and smart packaging solutions, will shape the industry's future. Companies that embrace sustainability and actively participate in collaborative innovation will be best positioned to capitalize on the market's long-term potential. Opportunities abound for companies that can offer customized, high-performance packaging solutions tailored to the specific needs of various agricultural chemical applications.

North America Agricultural Chemical Packaging Industry Segmentation

-

1. Product Type

- 1.1. Bags and Pouches

- 1.2. Containers and Cans

- 1.3. Intermediate Bulk Containers (IBCs)

- 1.4. Other Product Types

-

2. Material Type

- 2.1. Plastic

- 2.2. Paper and Paperboard

- 2.3. Metal

- 2.4. Other Materials

-

3. Application Type

- 3.1. Fertilizers

- 3.2. Pesticides

- 3.3. Herbicides

- 3.4. Other Application Types

North America Agricultural Chemical Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Agricultural Chemical Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging

- 3.3. Market Restrains

- 3.3.1. ; High Inventory Costs and Premium Pricing

- 3.4. Market Trends

- 3.4.1. Fertilizers to Hold Major Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Bags and Pouches

- 5.1.2. Containers and Cans

- 5.1.3. Intermediate Bulk Containers (IBCs)

- 5.1.4. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Material Type

- 5.2.1. Plastic

- 5.2.2. Paper and Paperboard

- 5.2.3. Metal

- 5.2.4. Other Materials

- 5.3. Market Analysis, Insights and Forecast - by Application Type

- 5.3.1. Fertilizers

- 5.3.2. Pesticides

- 5.3.3. Herbicides

- 5.3.4. Other Application Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United States North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Hoover CS*List Not Exhaustive

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Sonoco Products Company

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 LC Packaging International BV

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Greif Inc

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Mondi Group

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Tri Rinse

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 ProAmpac LLC

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Mauser Packaging Solutions

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Silgan Holdings

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.1 Hoover CS*List Not Exhaustive

List of Figures

- Figure 1: North America Agricultural Chemical Packaging Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Agricultural Chemical Packaging Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 4: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 5: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 12: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 13: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 14: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Agricultural Chemical Packaging Industry?

The projected CAGR is approximately 3.40%.

2. Which companies are prominent players in the North America Agricultural Chemical Packaging Industry?

Key companies in the market include Hoover CS*List Not Exhaustive, Sonoco Products Company, LC Packaging International BV, Greif Inc, Mondi Group, Tri Rinse, ProAmpac LLC, Mauser Packaging Solutions, Silgan Holdings.

3. What are the main segments of the North America Agricultural Chemical Packaging Industry?

The market segments include Product Type, Material Type, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.99 Million as of 2022.

5. What are some drivers contributing to market growth?

Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging.

6. What are the notable trends driving market growth?

Fertilizers to Hold Major Market Share.

7. Are there any restraints impacting market growth?

; High Inventory Costs and Premium Pricing.

8. Can you provide examples of recent developments in the market?

April 2022 - Greif Inc. announced the divestiture of the Flexible Packaging joint venture or 'FPS' for USD 123 million. The company will use the sale of FPS to clear the debt payments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Agricultural Chemical Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Agricultural Chemical Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Agricultural Chemical Packaging Industry?

To stay informed about further developments, trends, and reports in the North America Agricultural Chemical Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence