Key Insights

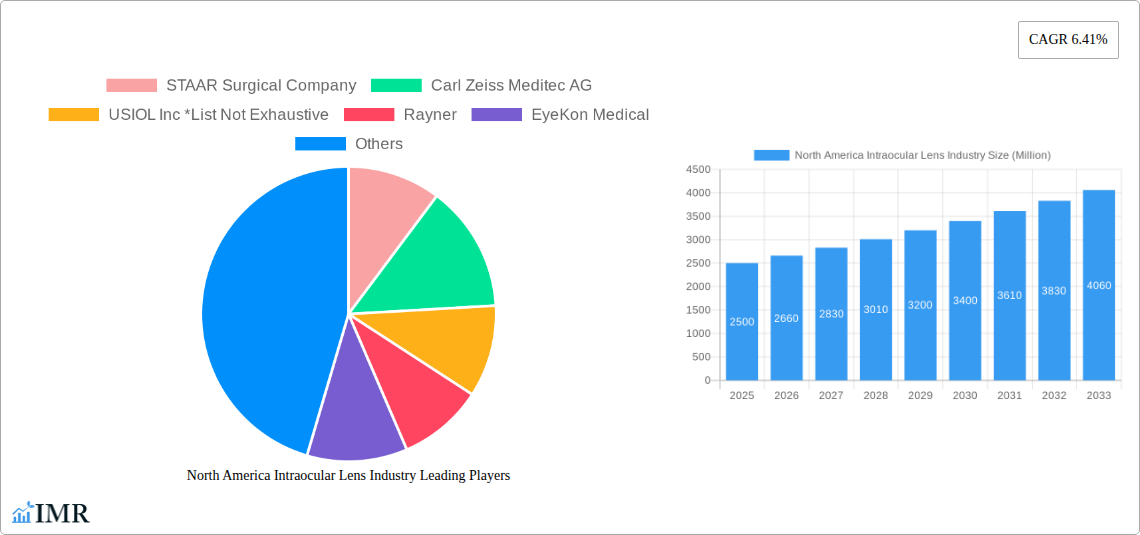

The North American intraocular lens (IOL) market, valued at approximately $2.5 billion in 2025, is projected to experience robust growth, driven by a rising geriatric population susceptible to cataracts and refractive errors, and increasing demand for premium IOLs offering improved visual acuity. The market's Compound Annual Growth Rate (CAGR) of 6.41% from 2025-2033 indicates a significant expansion, reaching an estimated $4.2 billion by 2033. This growth is fueled by several factors. Technological advancements are leading to the development of innovative IOL designs, such as multifocal and toric lenses, which correct presbyopia and astigmatism, respectively, resulting in enhanced patient outcomes and increased adoption. The rising prevalence of age-related eye diseases like cataracts is also a major contributor, necessitating a larger number of IOL implantations. Furthermore, the increasing number of ambulatory surgical centers and well-equipped hospitals contributes to market expansion by providing better access to IOL procedures.

However, the market faces some challenges. High procedure costs and the associated expenses of premium IOLs can limit access for some patients, potentially hindering market growth. The market is also moderately competitive, with several established players such as Johnson & Johnson, Alcon, and Bausch + Lomb competing alongside specialized IOL manufacturers. Strategic partnerships, technological innovation, and effective marketing strategies will be crucial for companies to maintain a competitive edge. The market segmentation, with hospitals holding the largest share of end-users, indicates that hospitals are key distribution channels, and the dominance of multifocal and toric IOLs within the product segment reflects the growing demand for technologically advanced vision correction solutions. The United States is expected to remain the largest market within North America, due to its substantial elderly population and advanced healthcare infrastructure.

North America Intraocular Lens (IOL) Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the North American intraocular lens (IOL) market, covering the period from 2019 to 2033. It offers in-depth insights into market dynamics, growth trends, competitive landscape, and future opportunities within this crucial segment of the ophthalmic devices market. The report segments the market by product type (monofocal, accommodative, multifocal, toric IOLs) and end-user (hospitals, ambulatory surgery centers, other centers), providing granular analysis of each segment’s performance and growth trajectory. Key players like STAAR Surgical Company, Carl Zeiss Meditec AG, Bausch Health Companies Inc (Bausch + Lomb), Johnson & Johnson, Alcon, and others are profiled, offering competitive intelligence and strategic insights. This report is an invaluable resource for industry professionals, investors, and stakeholders seeking a clear understanding of this dynamic market. The total market size in 2025 is estimated to be XX Million units.

North America Intraocular Lens Industry Market Dynamics & Structure

The North American intraocular lens (IOL) market is characterized by a moderately consolidated structure with several major players commanding significant market share. Technological innovation, particularly in areas like multifocal and toric IOLs, remains a key driver of growth. Stringent regulatory frameworks, primarily governed by the FDA, influence product development and market entry. Competitive pressures arise from both established players and emerging companies introducing innovative products. The ageing population and rising prevalence of cataracts fuel market expansion, while the increasing adoption of minimally invasive surgical procedures supports the growth of ambulatory surgical centers as key end-users. Furthermore, mergers and acquisitions (M&A) activity have shaped the competitive landscape.

- Market Concentration: The top 5 players hold approximately XX% of the market share in 2025.

- Technological Innovation: Focus on improved visual acuity, reduced complications, and faster recovery times drives innovation.

- Regulatory Framework: FDA approvals significantly impact product launch timelines and market access.

- Competitive Substitutes: Limited direct substitutes exist; however, refractive surgeries like LASIK offer alternative solutions.

- End-User Demographics: Aging population and increasing cataract prevalence fuel demand. A shift towards ambulatory surgery centers is observed.

- M&A Trends: XX major M&A deals were recorded between 2019 and 2024, resulting in market consolidation and expansion.

North America Intraocular Lens Industry Growth Trends & Insights

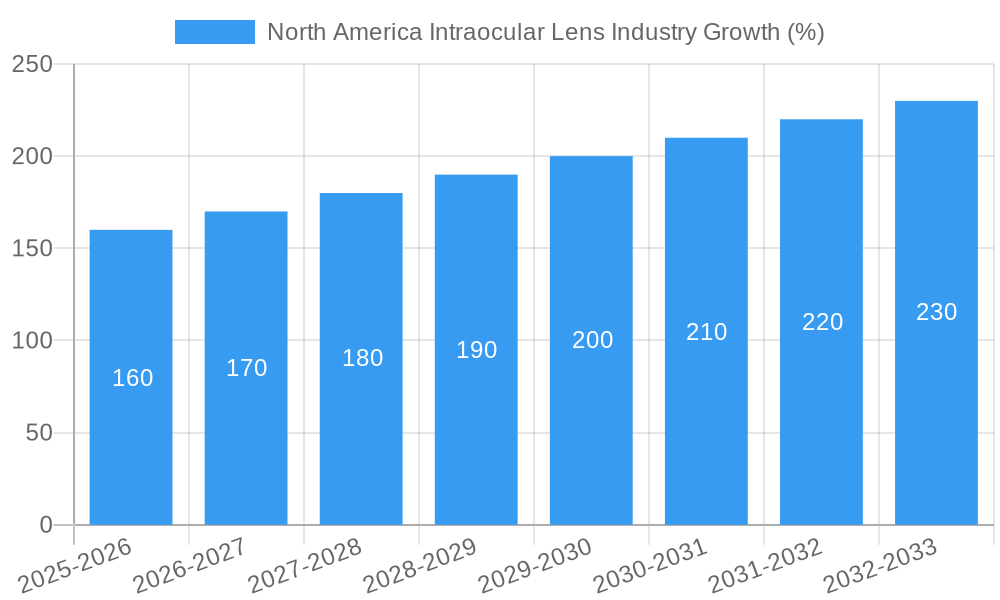

The North American IOL market has witnessed significant growth over the historical period (2019-2024), with a Compound Annual Growth Rate (CAGR) of XX% and is projected to maintain a CAGR of XX% during the forecast period (2025-2033). This growth is attributed to factors including an aging population, increasing cataract prevalence, technological advancements in IOL designs, and rising disposable incomes. The adoption rate of premium IOLs, such as multifocal and toric lenses, is increasing steadily, driven by patient preference for improved visual outcomes and reduced dependence on spectacles. Technological disruptions, such as the development of advanced materials and surgical techniques, further enhance market expansion. Consumer behavior shows a preference for less invasive procedures and faster recovery times, influencing the choice of IOLs and surgical centers. Market penetration of premium IOLs is projected to reach XX% by 2033.

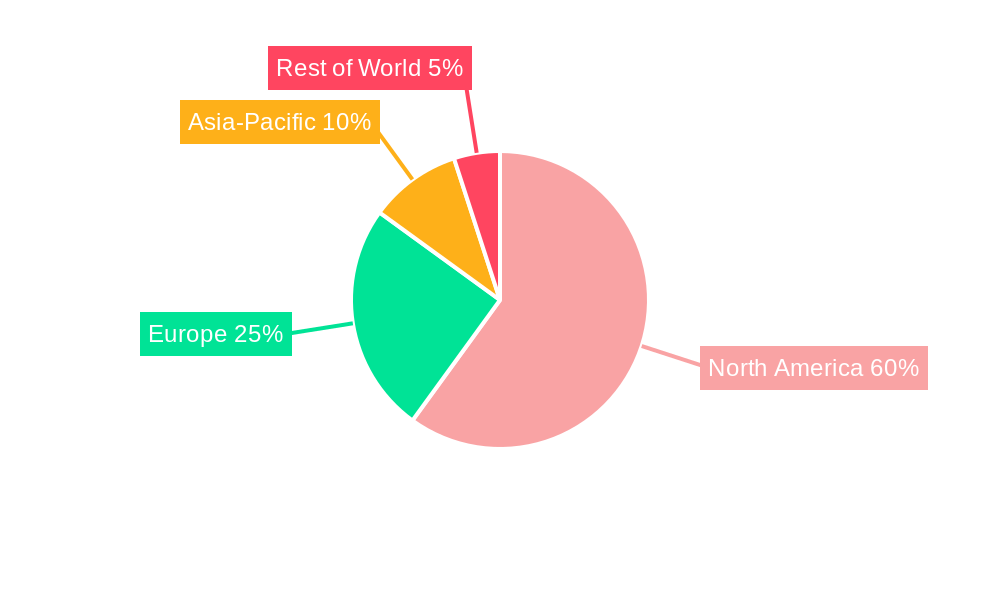

Dominant Regions, Countries, or Segments in North America Intraocular Lens Industry

The United States dominates the North American IOL market, accounting for the largest share of total units due to its large aging population and high prevalence of cataracts. Within the product segments, multifocal IOLs are experiencing the fastest growth, driven by increasing patient demand for improved vision quality after cataract surgery. Hospitals currently dominate the end-user segment, although ambulatory surgical centers are experiencing a faster growth rate due to their cost-effectiveness and convenience.

- Key Drivers (US): High prevalence of cataracts, aging population, advanced healthcare infrastructure, and high healthcare expenditure.

- Key Drivers (Ambulatory Centers): Cost-effectiveness, convenient access, shorter recovery times, and increasing patient preference.

- Market Share: The US accounts for approximately XX% of the total market in 2025. Multifocal IOLs hold a growing market share estimated at XX% in 2025.

North America Intraocular Lens Industry Product Landscape

The IOL market offers a diverse range of products catering to various patient needs and preferences. Monofocal IOLs remain the most widely used, providing clear distance vision. However, multifocal and toric IOLs are gaining traction, offering solutions for presbyopia (age-related vision loss) and astigmatism, respectively. Accommodative IOLs aim to mimic the eye’s natural focusing ability. Continuous innovation focuses on enhancing visual acuity, minimizing glare and halos, and improving biocompatibility. Manufacturers are introducing IOLs made from advanced materials with improved durability and longevity.

Key Drivers, Barriers & Challenges in North America Intraocular Lens Industry

Key Drivers: The aging population and rising prevalence of cataracts are the primary drivers. Technological advancements leading to improved IOL designs and surgical techniques contribute significantly. Increased awareness of premium IOL options among patients also fuels growth.

Key Challenges & Restraints: High cost of premium IOLs presents a barrier to widespread adoption, especially among price-sensitive patients. Regulatory hurdles and approval processes can delay product launches. Intense competition among established players and emerging companies exerts pressure on pricing and profit margins. Supply chain disruptions can impact the availability of IOLs and related products. XX% of the potential market remains untapped due to these barriers.

Emerging Opportunities in North America Intraocular Lens Industry

Emerging opportunities include the growing demand for premium IOLs with advanced features, such as extended depth of focus and reduced glare. Expansion into untapped markets, such as underserved populations, presents significant potential. Technological innovations, such as the development of artificial intelligence (AI)-powered diagnostic tools, may streamline the surgical process. The focus on personalized medicine and tailored IOL selection holds promise.

Growth Accelerators in the North America Intraocular Lens Industry

Technological advancements, such as the development of new materials and improved surgical techniques, will continue to propel market growth. Strategic partnerships and collaborations between IOL manufacturers and ophthalmic surgeons will optimize product development and market penetration. Expansion into new geographical areas and penetration into underserved populations will offer significant growth potential.

Key Players Shaping the North America Intraocular Lens Industry Market

- STAAR Surgical Company

- Carl Zeiss Meditec AG

- USIOL Inc

- Rayner

- EyeKon Medical

- Bausch Health Companies Inc (Bausch + Lomb)

- Lenstec Inc

- HumanOptics Holding AG

- Johnson & Johnson

- HOYA Corporation

- Alcon

Notable Milestones in North America Intraocular Lens Industry Sector

- April 2023: ZEISS Medical Technology received FDA approval for CT LUCIA 621P Monofocal IOL. This approval expanded the company’s product portfolio and broadened its market reach.

- May 2023: Atia Vision presented clinical data on the OmniVu IOL System at ASCRS. This milestone highlighted a potential technological advancement in IOL technology, potentially driving future market growth.

In-Depth North America Intraocular Lens Industry Market Outlook

The North American IOL market is poised for continued growth, driven by an aging population, increasing cataract prevalence, and ongoing technological advancements. The rising adoption of premium IOLs and expansion into untapped markets offer significant opportunities for market players. Strategic partnerships and investments in research and development will be crucial for sustained growth in this dynamic sector. The market is projected to reach XX Million units by 2033, representing a significant expansion of the current market size.

North America Intraocular Lens Industry Segmentation

-

1. Product

- 1.1. Monofocal Intraocular Lens

- 1.2. Accommodative Intraocular Lens

- 1.3. Multifocal Intraocular Lens

- 1.4. Toric Intraocular Lens

-

2. End-User

- 2.1. Hospitals

- 2.2. Ambulatory Centers

- 2.3. Other Centers

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Intraocular Lens Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Intraocular Lens Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.41% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Burden of Ophthalmic Issues; Increasing Cases of Cataract in the Diabetic Population

- 3.3. Market Restrains

- 3.3.1. High Cost of Intraocular Lens; Lack of Reimbursement Policies

- 3.4. Market Trends

- 3.4.1. Accommodative Intraocular Lens is Expected to Exhibit Fastest Growth Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Monofocal Intraocular Lens

- 5.1.2. Accommodative Intraocular Lens

- 5.1.3. Multifocal Intraocular Lens

- 5.1.4. Toric Intraocular Lens

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Hospitals

- 5.2.2. Ambulatory Centers

- 5.2.3. Other Centers

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. United States North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Monofocal Intraocular Lens

- 6.1.2. Accommodative Intraocular Lens

- 6.1.3. Multifocal Intraocular Lens

- 6.1.4. Toric Intraocular Lens

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Hospitals

- 6.2.2. Ambulatory Centers

- 6.2.3. Other Centers

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Canada North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Monofocal Intraocular Lens

- 7.1.2. Accommodative Intraocular Lens

- 7.1.3. Multifocal Intraocular Lens

- 7.1.4. Toric Intraocular Lens

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Hospitals

- 7.2.2. Ambulatory Centers

- 7.2.3. Other Centers

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Mexico North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Monofocal Intraocular Lens

- 8.1.2. Accommodative Intraocular Lens

- 8.1.3. Multifocal Intraocular Lens

- 8.1.4. Toric Intraocular Lens

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Hospitals

- 8.2.2. Ambulatory Centers

- 8.2.3. Other Centers

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. United States North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Intraocular Lens Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 STAAR Surgical Company

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Carl Zeiss Meditec AG

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 USIOL Inc *List Not Exhaustive

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Rayner

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 EyeKon Medical

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Bausch Health Companies Inc (Bausch + Lomb)

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Lenstec Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 HumanOptics Holding AG

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Johnson & Johnson

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 HOYA Corporation

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Alcon

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.1 STAAR Surgical Company

List of Figures

- Figure 1: North America Intraocular Lens Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Intraocular Lens Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Intraocular Lens Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Intraocular Lens Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: North America Intraocular Lens Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 4: North America Intraocular Lens Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: North America Intraocular Lens Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Intraocular Lens Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Intraocular Lens Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Intraocular Lens Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Intraocular Lens Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Intraocular Lens Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Intraocular Lens Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 12: North America Intraocular Lens Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 13: North America Intraocular Lens Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 14: North America Intraocular Lens Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: North America Intraocular Lens Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 16: North America Intraocular Lens Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 17: North America Intraocular Lens Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: North America Intraocular Lens Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: North America Intraocular Lens Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 20: North America Intraocular Lens Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 21: North America Intraocular Lens Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 22: North America Intraocular Lens Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Intraocular Lens Industry?

The projected CAGR is approximately 6.41%.

2. Which companies are prominent players in the North America Intraocular Lens Industry?

Key companies in the market include STAAR Surgical Company, Carl Zeiss Meditec AG, USIOL Inc *List Not Exhaustive, Rayner, EyeKon Medical, Bausch Health Companies Inc (Bausch + Lomb), Lenstec Inc, HumanOptics Holding AG, Johnson & Johnson, HOYA Corporation, Alcon.

3. What are the main segments of the North America Intraocular Lens Industry?

The market segments include Product, End-User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Burden of Ophthalmic Issues; Increasing Cases of Cataract in the Diabetic Population.

6. What are the notable trends driving market growth?

Accommodative Intraocular Lens is Expected to Exhibit Fastest Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Intraocular Lens; Lack of Reimbursement Policies.

8. Can you provide examples of recent developments in the market?

May 2023: Atia Vision presented the first clinical data on the patented OmniVu IOL System at the 2023 Annual Meeting of the American Society of Cataract Refractive Surgery (ASCRS) in San Diego, California.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Intraocular Lens Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Intraocular Lens Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Intraocular Lens Industry?

To stay informed about further developments, trends, and reports in the North America Intraocular Lens Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence