Key Insights

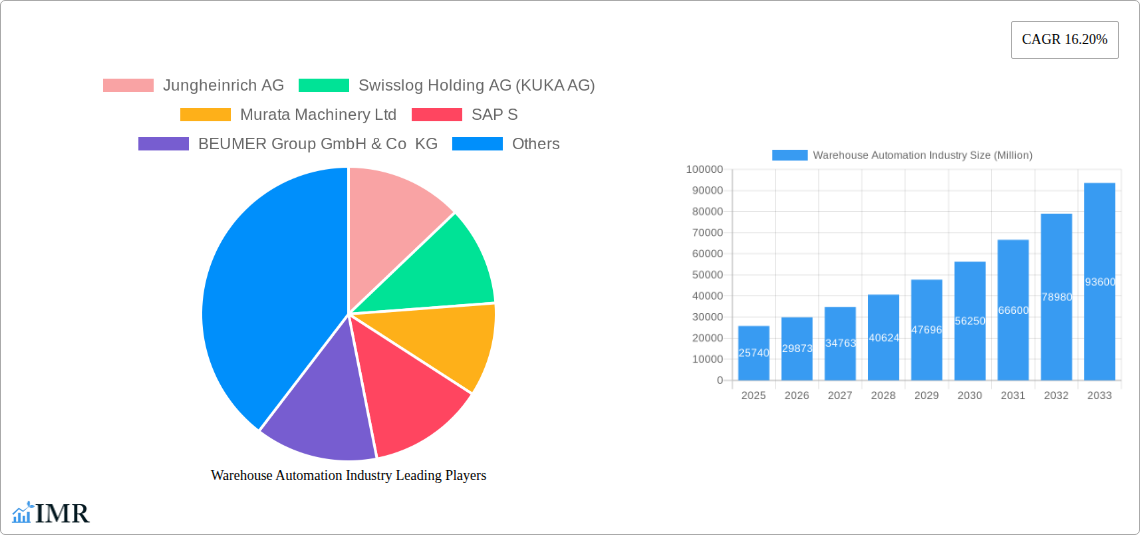

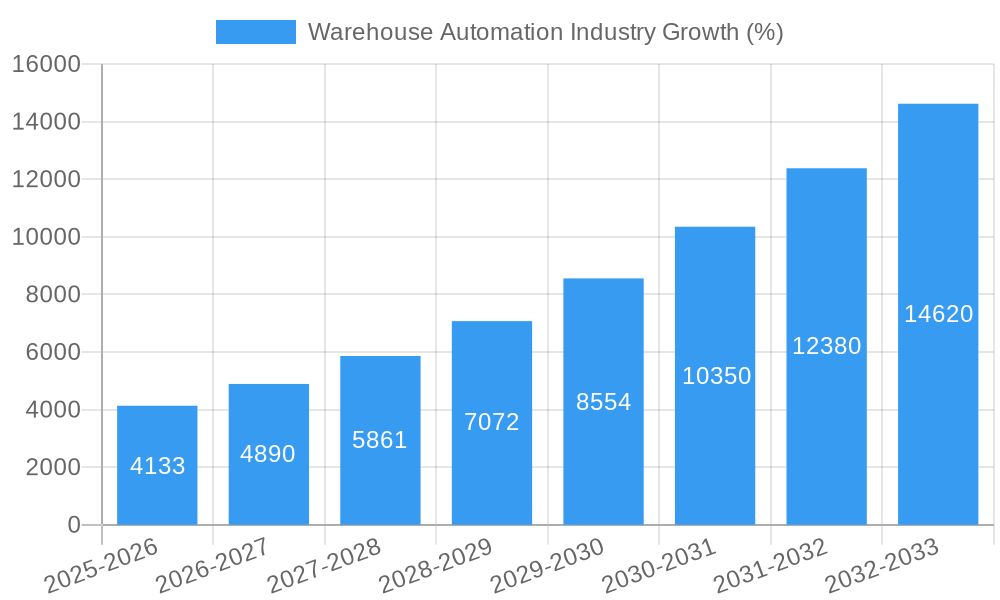

The warehouse automation market is experiencing robust growth, projected to reach \$25.74 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 16.20% from 2025 to 2033. This expansion is driven by several key factors. E-commerce's continuous surge demands faster and more efficient order fulfillment, pushing businesses to adopt automated solutions for improved productivity and reduced operational costs. Simultaneously, labor shortages and rising labor costs are incentivizing automation as a cost-effective and reliable alternative. Technological advancements, such as the development of sophisticated robotics, advanced warehouse management systems (WMS), and artificial intelligence (AI)-powered solutions, further fuel market growth. The increasing adoption of cloud-based WMS solutions enhances scalability and accessibility, contributing to wider market penetration. Segment-wise, hardware, particularly piece-picking robots, are expected to dominate, followed by software solutions including WMS and WES. The food and beverage, post and parcel, and retail sectors are leading end-users, reflecting their high-volume and fast-paced operational needs. Geographically, North America and Europe are currently major markets, but the Asia-Pacific region is poised for significant growth due to its expanding e-commerce sector and rising manufacturing activity.

Competition within the warehouse automation sector is intense, with established players like Jungheinrich AG, Swisslog Holding AG, and Dematic Group vying for market share alongside emerging technology providers. Successful companies are focusing on developing integrated solutions combining hardware, software, and services to offer comprehensive automation packages tailored to specific customer needs. The future of the market hinges on the continued innovation in robotics, AI, and data analytics, as well as the seamless integration of these technologies into existing warehouse infrastructure. Addressing challenges like high initial investment costs, system integration complexities, and cybersecurity concerns will be crucial for sustained market growth. The market's trajectory suggests a continued shift towards advanced automation, driven by the need for operational efficiency, resilience, and adaptability in an ever-evolving supply chain landscape.

Warehouse Automation Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Warehouse Automation Industry, encompassing market size, growth trends, key players, and future outlook. With a focus on parent and child markets, this report is an invaluable resource for industry professionals, investors, and anyone seeking to understand this dynamic sector. The study period covers 2019-2033, with 2025 as the base and estimated year.

Warehouse Automation Industry Market Dynamics & Structure

The warehouse automation market, valued at xx million units in 2024, exhibits a moderately consolidated structure with several key players holding significant market share. Technological innovation, driven by advancements in robotics, AI, and cloud computing, is a primary growth driver. Stringent regulatory frameworks concerning safety and data privacy influence market dynamics, while rising labor costs and the need for improved efficiency are key adoption drivers. Competition from traditional manual warehousing methods continues, although this is diminishing. Mergers and acquisitions (M&A) activity is significant, reflecting the industry's consolidation and expansion.

- Market Concentration: High, with top 10 players accounting for approximately 60% of the market share in 2024.

- Technological Innovation Drivers: Artificial intelligence (AI), machine learning (ML), robotics, Internet of Things (IoT), cloud computing, and big data analytics.

- Regulatory Frameworks: OSHA regulations (safety), GDPR (data privacy), and industry-specific compliance standards.

- Competitive Product Substitutes: Manual labor, traditional warehouse management systems.

- End-User Demographics: Growth is predominantly driven by e-commerce expansion and the rise of omnichannel retail.

- M&A Trends: A high volume of deals in recent years, driven by companies seeking to expand their market reach and technological capabilities (e.g., Blue Yonder's acquisition of One Network). Approximately xx M&A deals were completed between 2019 and 2024.

Warehouse Automation Industry Growth Trends & Insights

The warehouse automation market is experiencing robust growth, driven by increasing e-commerce sales, the need for supply chain optimization, and advancements in automation technologies. The market size is projected to reach xx million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Adoption rates are significantly increasing across various end-user industries, particularly in the food and beverage, retail, and manufacturing sectors. Technological disruptions, such as the introduction of autonomous mobile robots and advanced warehouse management systems (WMS), are accelerating this growth. Consumer behavior shifts, such as increased online shopping and demand for faster delivery times, are further fueling market expansion. Market penetration is expected to reach xx% by 2033.

Dominant Regions, Countries, or Segments in Warehouse Automation Industry

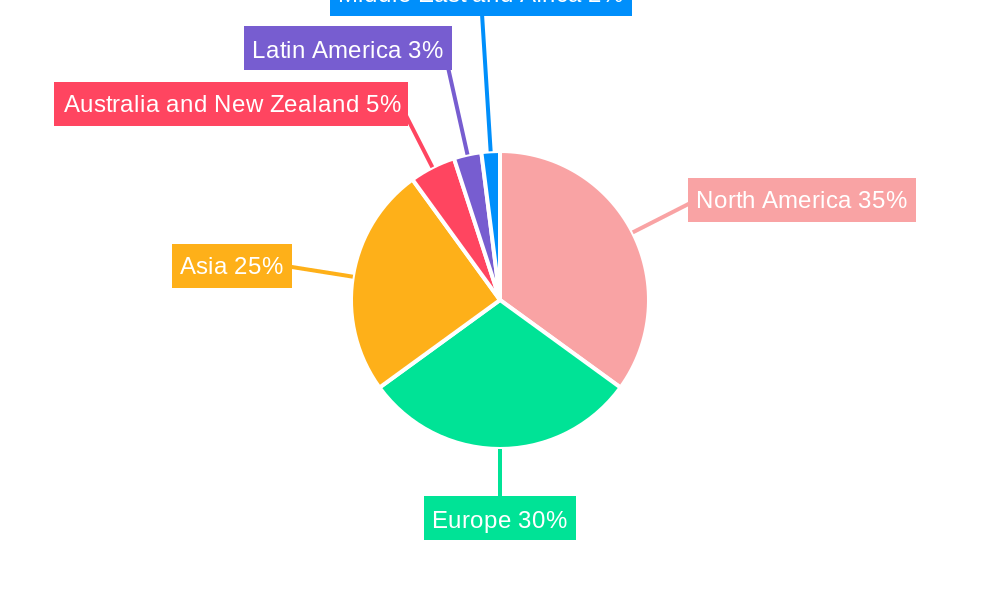

North America and Europe currently dominate the warehouse automation market, driven by high adoption rates in advanced economies and robust e-commerce sectors. However, Asia-Pacific is anticipated to experience the fastest growth during the forecast period due to rapid industrialization and increasing investments in automation technologies.

By Component:

- Hardware: The hardware segment currently holds the largest market share, driven by high demand for automated guided vehicles (AGVs), robotics, and conveyor systems. This segment is projected to continue its dominance throughout the forecast period.

- Software: WMS and WES are witnessing significant growth due to increased focus on efficient warehouse operations. The cloud-based WMS is expected to see substantial growth.

- Piece-Picking Robots: This segment exhibits high growth potential due to increased demand for enhanced order fulfillment capabilities.

- Services: Maintenance and value-added services are integral components, contributing significantly to market value.

By End-User:

- Food and Beverage: The food and beverage industry is a major adopter of warehouse automation due to stringent quality control, traceability requirements and need for efficient cold chain management.

- E-Commerce & Retail: The growth in online shopping is a primary driver of the market’s expansion in this sector.

- Manufacturing: The manufacturing segment drives significant growth, with increased adoption of automation to boost productivity and optimize supply chain operations.

- Post and Parcel: This segment contributes considerable demand for high-throughput automated sorting systems and delivery optimization solutions.

Warehouse Automation Industry Product Landscape

The warehouse automation market offers a diverse range of products, from advanced robotics and automated guided vehicles (AGVs) to sophisticated warehouse management systems (WMS) and warehouse execution systems (WES). These solutions enhance operational efficiency, optimize inventory management, and improve order fulfillment accuracy. Key innovations include autonomous mobile robots (AMRs) capable of self-navigation and adaptive decision-making, AI-powered vision systems for precise object recognition and picking, and cloud-based WMS for improved scalability and real-time visibility. These solutions boast high return on investment (ROI) due to increased productivity, reduced labor costs, and minimized errors.

Key Drivers, Barriers & Challenges in Warehouse Automation Industry

Key Drivers:

- E-commerce boom: Driving demand for faster, more efficient order fulfillment.

- Labor shortages: Automation addresses workforce challenges and rising labor costs.

- Technological advancements: AI, robotics, and IoT are constantly improving efficiency and capabilities.

- Supply chain optimization: Automation streamlines operations and reduces delays.

Key Challenges:

- High initial investment costs: A significant barrier to entry for smaller businesses.

- Integration complexity: Seamless integration with existing systems can be challenging and costly.

- Cybersecurity concerns: Protecting sensitive data in connected warehouse environments is critical.

- Lack of skilled workforce: Operation and maintenance require specialized expertise. The shortage of skilled professionals is estimated to impact xx% of implementations.

Emerging Opportunities in Warehouse Automation Industry

- Growth in developing economies: Significant potential in emerging markets with rapid industrialization.

- Expansion into new verticals: Opportunities exist in healthcare, pharmaceuticals, and other industries.

- Development of collaborative robots (cobots): Cobots can work alongside human workers, addressing safety concerns and improving efficiency.

- Focus on sustainability: Energy-efficient solutions and environmentally friendly practices are gaining traction.

Growth Accelerators in the Warehouse Automation Industry Industry

Several factors are poised to accelerate growth in the warehouse automation market in the coming years. Advancements in AI and machine learning are leading to the development of more intelligent and adaptable automation systems. Strategic partnerships between technology providers and warehouse operators are fostering innovation and wider adoption. The expansion of e-commerce and the increasing demand for faster delivery times are continuing to fuel growth. Furthermore, government incentives and supportive policies are encouraging investment in automation technologies.

Key Players Shaping the Warehouse Automation Industry Market

- Jungheinrich AG

- Swisslog Holding AG (KUKA AG)

- Murata Machinery Ltd

- SAP S

- BEUMER Group GmbH & Co KG

- Daifuku Co Limited

- Honeywell Intelligrated (Honeywell International Inc)

- SSI Schaefer AG

- WITRON Logistik + Informatik GmbH

- TGW Logistics Group GmbH

- Kardex Group

- Oracle Corporation

- One Network Enterprises Inc

- Vanderlande Industries BV

- Knapp AG

- Mecalux SA

- Dematic Group (Kion Group AG)

Notable Milestones in Warehouse Automation Industry Sector

- July 2023: Jungheinrich premiered its latest mobile robot solution at LogiMAT 2023, showcasing advancements in adaptable warehouse automation.

- March 2024: Blue Yonder's acquisition of One Network Enterprises for approximately USD 839 million signifies a major consolidation in the intelligent control tower market.

In-Depth Warehouse Automation Industry Market Outlook

The warehouse automation market is poised for sustained growth, driven by continuous technological advancements, rising e-commerce penetration, and the ongoing need for efficient supply chain management. The integration of AI and machine learning will lead to the development of more sophisticated automation systems, improving accuracy, adaptability, and overall efficiency. Strategic partnerships and investments in research and development will further propel market expansion. The long-term market outlook is highly positive, presenting significant strategic opportunities for both established players and new entrants.

Warehouse Automation Industry Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. Mobile Robots (AGV, AMR)

- 1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 1.1.3. Automated Conveyor & Sorting Systems

- 1.1.4. De-palletizing/Palletizing Systems

- 1.1.5. Automati

- 1.1.6. Piece Picking Robots

- 1.2. Software

- 1.3. Services (Value Added Services, Maintenance, etc.)

-

1.1. Hardware

-

2. End-User

- 2.1. Food and

- 2.2. Post and Parcel

- 2.3. Retail

- 2.4. Apparel

- 2.5. Manufacturing (Durable and Non-Durable)

- 2.6. Other End-user Industries

Warehouse Automation Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Warehouse Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 16.20% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Exponential Growth of the E-commerce Industry and Customer Expectation; Increasing Manufacturing Complexity and Technology Availability

- 3.3. Market Restrains

- 3.3.1. Optimizing Battery Life of Hearable Device

- 3.4. Market Trends

- 3.4.1. Retail to Have a Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. Mobile Robots (AGV, AMR)

- 5.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 5.1.1.3. Automated Conveyor & Sorting Systems

- 5.1.1.4. De-palletizing/Palletizing Systems

- 5.1.1.5. Automati

- 5.1.1.6. Piece Picking Robots

- 5.1.2. Software

- 5.1.3. Services (Value Added Services, Maintenance, etc.)

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Food and

- 5.2.2. Post and Parcel

- 5.2.3. Retail

- 5.2.4. Apparel

- 5.2.5. Manufacturing (Durable and Non-Durable)

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. North America Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. Mobile Robots (AGV, AMR)

- 6.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3. Automated Conveyor & Sorting Systems

- 6.1.1.4. De-palletizing/Palletizing Systems

- 6.1.1.5. Automati

- 6.1.1.6. Piece Picking Robots

- 6.1.2. Software

- 6.1.3. Services (Value Added Services, Maintenance, etc.)

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Food and

- 6.2.2. Post and Parcel

- 6.2.3. Retail

- 6.2.4. Apparel

- 6.2.5. Manufacturing (Durable and Non-Durable)

- 6.2.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Europe Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.1.1. Mobile Robots (AGV, AMR)

- 7.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 7.1.1.3. Automated Conveyor & Sorting Systems

- 7.1.1.4. De-palletizing/Palletizing Systems

- 7.1.1.5. Automati

- 7.1.1.6. Piece Picking Robots

- 7.1.2. Software

- 7.1.3. Services (Value Added Services, Maintenance, etc.)

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Food and

- 7.2.2. Post and Parcel

- 7.2.3. Retail

- 7.2.4. Apparel

- 7.2.5. Manufacturing (Durable and Non-Durable)

- 7.2.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Asia Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.1.1. Mobile Robots (AGV, AMR)

- 8.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 8.1.1.3. Automated Conveyor & Sorting Systems

- 8.1.1.4. De-palletizing/Palletizing Systems

- 8.1.1.5. Automati

- 8.1.1.6. Piece Picking Robots

- 8.1.2. Software

- 8.1.3. Services (Value Added Services, Maintenance, etc.)

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Food and

- 8.2.2. Post and Parcel

- 8.2.3. Retail

- 8.2.4. Apparel

- 8.2.5. Manufacturing (Durable and Non-Durable)

- 8.2.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Australia and New Zealand Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.1.1. Mobile Robots (AGV, AMR)

- 9.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 9.1.1.3. Automated Conveyor & Sorting Systems

- 9.1.1.4. De-palletizing/Palletizing Systems

- 9.1.1.5. Automati

- 9.1.1.6. Piece Picking Robots

- 9.1.2. Software

- 9.1.3. Services (Value Added Services, Maintenance, etc.)

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Food and

- 9.2.2. Post and Parcel

- 9.2.3. Retail

- 9.2.4. Apparel

- 9.2.5. Manufacturing (Durable and Non-Durable)

- 9.2.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Latin America Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.1.1. Mobile Robots (AGV, AMR)

- 10.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 10.1.1.3. Automated Conveyor & Sorting Systems

- 10.1.1.4. De-palletizing/Palletizing Systems

- 10.1.1.5. Automati

- 10.1.1.6. Piece Picking Robots

- 10.1.2. Software

- 10.1.3. Services (Value Added Services, Maintenance, etc.)

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Food and

- 10.2.2. Post and Parcel

- 10.2.3. Retail

- 10.2.4. Apparel

- 10.2.5. Manufacturing (Durable and Non-Durable)

- 10.2.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Middle East and Africa Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Hardware

- 11.1.1.1. Mobile Robots (AGV, AMR)

- 11.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 11.1.1.3. Automated Conveyor & Sorting Systems

- 11.1.1.4. De-palletizing/Palletizing Systems

- 11.1.1.5. Automati

- 11.1.1.6. Piece Picking Robots

- 11.1.2. Software

- 11.1.3. Services (Value Added Services, Maintenance, etc.)

- 11.1.1. Hardware

- 11.2. Market Analysis, Insights and Forecast - by End-User

- 11.2.1. Food and

- 11.2.2. Post and Parcel

- 11.2.3. Retail

- 11.2.4. Apparel

- 11.2.5. Manufacturing (Durable and Non-Durable)

- 11.2.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. North America Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Europe Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Asia Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Australia and New Zealand Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Latin America Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1.

- 17. Middle East and Africa Warehouse Automation Industry Analysis, Insights and Forecast, 2019-2031

- 17.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 17.1.1.

- 18. Competitive Analysis

- 18.1. Global Market Share Analysis 2024

- 18.2. Company Profiles

- 18.2.1 Jungheinrich AG

- 18.2.1.1. Overview

- 18.2.1.2. Products

- 18.2.1.3. SWOT Analysis

- 18.2.1.4. Recent Developments

- 18.2.1.5. Financials (Based on Availability)

- 18.2.2 Swisslog Holding AG (KUKA AG)

- 18.2.2.1. Overview

- 18.2.2.2. Products

- 18.2.2.3. SWOT Analysis

- 18.2.2.4. Recent Developments

- 18.2.2.5. Financials (Based on Availability)

- 18.2.3 Murata Machinery Ltd

- 18.2.3.1. Overview

- 18.2.3.2. Products

- 18.2.3.3. SWOT Analysis

- 18.2.3.4. Recent Developments

- 18.2.3.5. Financials (Based on Availability)

- 18.2.4 SAP S

- 18.2.4.1. Overview

- 18.2.4.2. Products

- 18.2.4.3. SWOT Analysis

- 18.2.4.4. Recent Developments

- 18.2.4.5. Financials (Based on Availability)

- 18.2.5 BEUMER Group GmbH & Co KG

- 18.2.5.1. Overview

- 18.2.5.2. Products

- 18.2.5.3. SWOT Analysis

- 18.2.5.4. Recent Developments

- 18.2.5.5. Financials (Based on Availability)

- 18.2.6 Daifuku Co Limited

- 18.2.6.1. Overview

- 18.2.6.2. Products

- 18.2.6.3. SWOT Analysis

- 18.2.6.4. Recent Developments

- 18.2.6.5. Financials (Based on Availability)

- 18.2.7 Honeywell Intelligrated (Honeywell International Inc )

- 18.2.7.1. Overview

- 18.2.7.2. Products

- 18.2.7.3. SWOT Analysis

- 18.2.7.4. Recent Developments

- 18.2.7.5. Financials (Based on Availability)

- 18.2.8 SSI Schaefer AG

- 18.2.8.1. Overview

- 18.2.8.2. Products

- 18.2.8.3. SWOT Analysis

- 18.2.8.4. Recent Developments

- 18.2.8.5. Financials (Based on Availability)

- 18.2.9 WITRON Logistik + Informatik GmbH

- 18.2.9.1. Overview

- 18.2.9.2. Products

- 18.2.9.3. SWOT Analysis

- 18.2.9.4. Recent Developments

- 18.2.9.5. Financials (Based on Availability)

- 18.2.10 TGW Logistics Group GmbH

- 18.2.10.1. Overview

- 18.2.10.2. Products

- 18.2.10.3. SWOT Analysis

- 18.2.10.4. Recent Developments

- 18.2.10.5. Financials (Based on Availability)

- 18.2.11 Kardex Group

- 18.2.11.1. Overview

- 18.2.11.2. Products

- 18.2.11.3. SWOT Analysis

- 18.2.11.4. Recent Developments

- 18.2.11.5. Financials (Based on Availability)

- 18.2.12 Oracle Corporation

- 18.2.12.1. Overview

- 18.2.12.2. Products

- 18.2.12.3. SWOT Analysis

- 18.2.12.4. Recent Developments

- 18.2.12.5. Financials (Based on Availability)

- 18.2.13 One Network Enterprises Inc

- 18.2.13.1. Overview

- 18.2.13.2. Products

- 18.2.13.3. SWOT Analysis

- 18.2.13.4. Recent Developments

- 18.2.13.5. Financials (Based on Availability)

- 18.2.14 Vanderlande Industries BV

- 18.2.14.1. Overview

- 18.2.14.2. Products

- 18.2.14.3. SWOT Analysis

- 18.2.14.4. Recent Developments

- 18.2.14.5. Financials (Based on Availability)

- 18.2.15 Knapp AG

- 18.2.15.1. Overview

- 18.2.15.2. Products

- 18.2.15.3. SWOT Analysis

- 18.2.15.4. Recent Developments

- 18.2.15.5. Financials (Based on Availability)

- 18.2.16 Mecalux SA

- 18.2.16.1. Overview

- 18.2.16.2. Products

- 18.2.16.3. SWOT Analysis

- 18.2.16.4. Recent Developments

- 18.2.16.5. Financials (Based on Availability)

- 18.2.17 Dematic Group (Kion Group AG)

- 18.2.17.1. Overview

- 18.2.17.2. Products

- 18.2.17.3. SWOT Analysis

- 18.2.17.4. Recent Developments

- 18.2.17.5. Financials (Based on Availability)

- 18.2.1 Jungheinrich AG

List of Figures

- Figure 1: Global Warehouse Automation Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Australia and New Zealand Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Australia and New Zealand Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Latin America Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Latin America Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: Middle East and Africa Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 13: Middle East and Africa Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Warehouse Automation Industry Revenue (Million), by Component 2024 & 2032

- Figure 15: North America Warehouse Automation Industry Revenue Share (%), by Component 2024 & 2032

- Figure 16: North America Warehouse Automation Industry Revenue (Million), by End-User 2024 & 2032

- Figure 17: North America Warehouse Automation Industry Revenue Share (%), by End-User 2024 & 2032

- Figure 18: North America Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: North America Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Europe Warehouse Automation Industry Revenue (Million), by Component 2024 & 2032

- Figure 21: Europe Warehouse Automation Industry Revenue Share (%), by Component 2024 & 2032

- Figure 22: Europe Warehouse Automation Industry Revenue (Million), by End-User 2024 & 2032

- Figure 23: Europe Warehouse Automation Industry Revenue Share (%), by End-User 2024 & 2032

- Figure 24: Europe Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 25: Europe Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Warehouse Automation Industry Revenue (Million), by Component 2024 & 2032

- Figure 27: Asia Warehouse Automation Industry Revenue Share (%), by Component 2024 & 2032

- Figure 28: Asia Warehouse Automation Industry Revenue (Million), by End-User 2024 & 2032

- Figure 29: Asia Warehouse Automation Industry Revenue Share (%), by End-User 2024 & 2032

- Figure 30: Asia Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 31: Asia Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 32: Australia and New Zealand Warehouse Automation Industry Revenue (Million), by Component 2024 & 2032

- Figure 33: Australia and New Zealand Warehouse Automation Industry Revenue Share (%), by Component 2024 & 2032

- Figure 34: Australia and New Zealand Warehouse Automation Industry Revenue (Million), by End-User 2024 & 2032

- Figure 35: Australia and New Zealand Warehouse Automation Industry Revenue Share (%), by End-User 2024 & 2032

- Figure 36: Australia and New Zealand Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 37: Australia and New Zealand Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 38: Latin America Warehouse Automation Industry Revenue (Million), by Component 2024 & 2032

- Figure 39: Latin America Warehouse Automation Industry Revenue Share (%), by Component 2024 & 2032

- Figure 40: Latin America Warehouse Automation Industry Revenue (Million), by End-User 2024 & 2032

- Figure 41: Latin America Warehouse Automation Industry Revenue Share (%), by End-User 2024 & 2032

- Figure 42: Latin America Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 43: Latin America Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 44: Middle East and Africa Warehouse Automation Industry Revenue (Million), by Component 2024 & 2032

- Figure 45: Middle East and Africa Warehouse Automation Industry Revenue Share (%), by Component 2024 & 2032

- Figure 46: Middle East and Africa Warehouse Automation Industry Revenue (Million), by End-User 2024 & 2032

- Figure 47: Middle East and Africa Warehouse Automation Industry Revenue Share (%), by End-User 2024 & 2032

- Figure 48: Middle East and Africa Warehouse Automation Industry Revenue (Million), by Country 2024 & 2032

- Figure 49: Middle East and Africa Warehouse Automation Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Warehouse Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 3: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 4: Global Warehouse Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Warehouse Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Warehouse Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Warehouse Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Warehouse Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Warehouse Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Warehouse Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 18: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 19: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 21: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 22: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 23: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 24: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 25: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 27: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 28: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 29: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 30: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 31: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 33: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 34: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Warehouse Automation Industry?

The projected CAGR is approximately 16.20%.

2. Which companies are prominent players in the Warehouse Automation Industry?

Key companies in the market include Jungheinrich AG, Swisslog Holding AG (KUKA AG), Murata Machinery Ltd, SAP S, BEUMER Group GmbH & Co KG, Daifuku Co Limited, Honeywell Intelligrated (Honeywell International Inc ), SSI Schaefer AG, WITRON Logistik + Informatik GmbH, TGW Logistics Group GmbH, Kardex Group, Oracle Corporation, One Network Enterprises Inc, Vanderlande Industries BV, Knapp AG, Mecalux SA, Dematic Group (Kion Group AG).

3. What are the main segments of the Warehouse Automation Industry?

The market segments include Component, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.74 Million as of 2022.

5. What are some drivers contributing to market growth?

Exponential Growth of the E-commerce Industry and Customer Expectation; Increasing Manufacturing Complexity and Technology Availability.

6. What are the notable trends driving market growth?

Retail to Have a Significant Growth.

7. Are there any restraints impacting market growth?

Optimizing Battery Life of Hearable Device.

8. Can you provide examples of recent developments in the market?

July 2023 - Jungheinrich, premiered its latest mobile robot solution at Stuttgart's LogiMAT 2023, the international trade fair for intralogistics solutions. It's a robot that can be easily integrated into any warehouse, which finds its own solutions, and which adapts to changing warehouse needs, increasing performance and efficiency. Its newly developed control system and toolchain enable smooth, simple integration with any existing warehouse environment and guarantee impressive flexibility from planning stage to day-to-day operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Warehouse Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Warehouse Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Warehouse Automation Industry?

To stay informed about further developments, trends, and reports in the Warehouse Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence