Key Insights

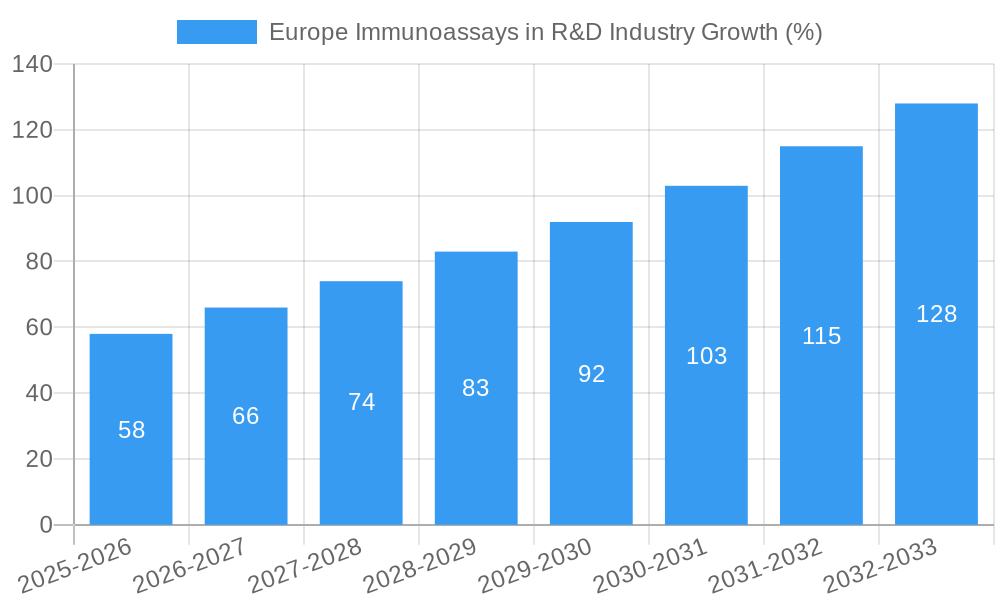

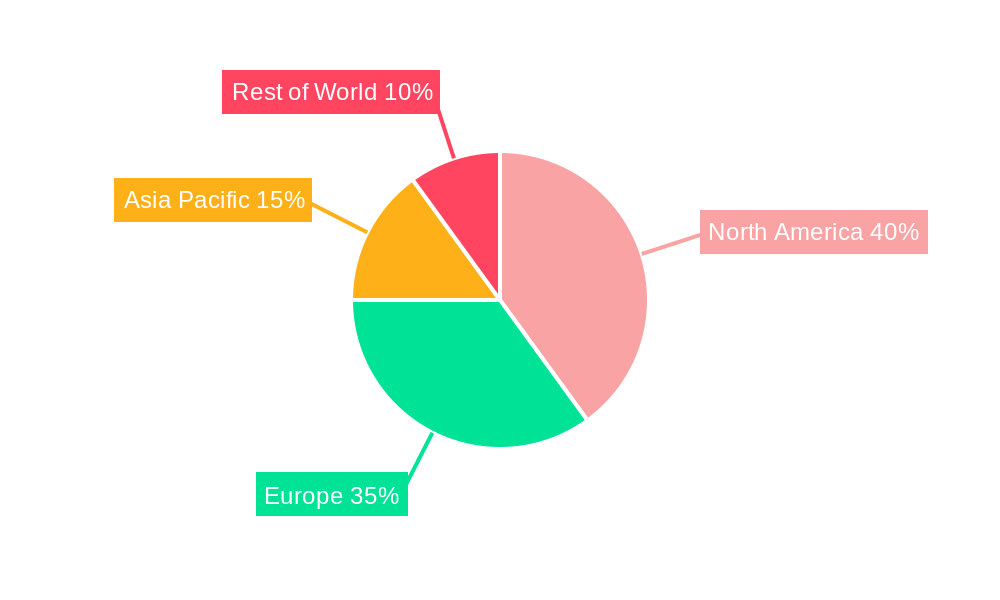

The European immunoassays market within the R&D sector is experiencing robust growth, driven by the increasing prevalence of cancer and other chronic diseases, coupled with advancements in biomarker discovery and technological innovations. The market, estimated at €[Insert Estimated 2025 Market Size in Millions based on provided CAGR and Market Size] million in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 11.60% throughout the forecast period (2025-2033). This expansion is fueled by several key factors. Firstly, the rising incidence of cancers such as prostate, breast, lung, and colorectal cancers is significantly increasing the demand for accurate and efficient diagnostic tools. Secondly, the ongoing development and adoption of advanced immunoassay technologies, such as OMICS technologies and highly sensitive immunoassays, enable earlier and more precise disease detection, personalized medicine approaches, and improved drug development processes. Furthermore, substantial investments in research and development by pharmaceutical and biotechnology companies are bolstering innovation within the immunoassay sector. Germany, France, the UK, and Italy are expected to be major contributors to the market's growth, reflecting their well-established healthcare infrastructure and robust R&D ecosystems.

However, certain challenges remain. High costs associated with advanced immunoassay technologies and the complexities involved in data analysis could hinder market penetration to some degree. Regulatory hurdles and stringent approval processes for new diagnostic tests also pose constraints. Despite these challenges, the overall outlook for the European immunoassays market in R&D remains positive, with considerable growth potential driven by a confluence of scientific advancements, increasing healthcare spending, and a growing emphasis on early disease diagnosis and personalized medicine. The market segmentation by disease, biomarker type, and profiling technology offers significant opportunities for specialized players to gain market share by focusing on specific niche areas.

Europe Immunoassays in R&D Industry: A Comprehensive Market Report (2019-2033)

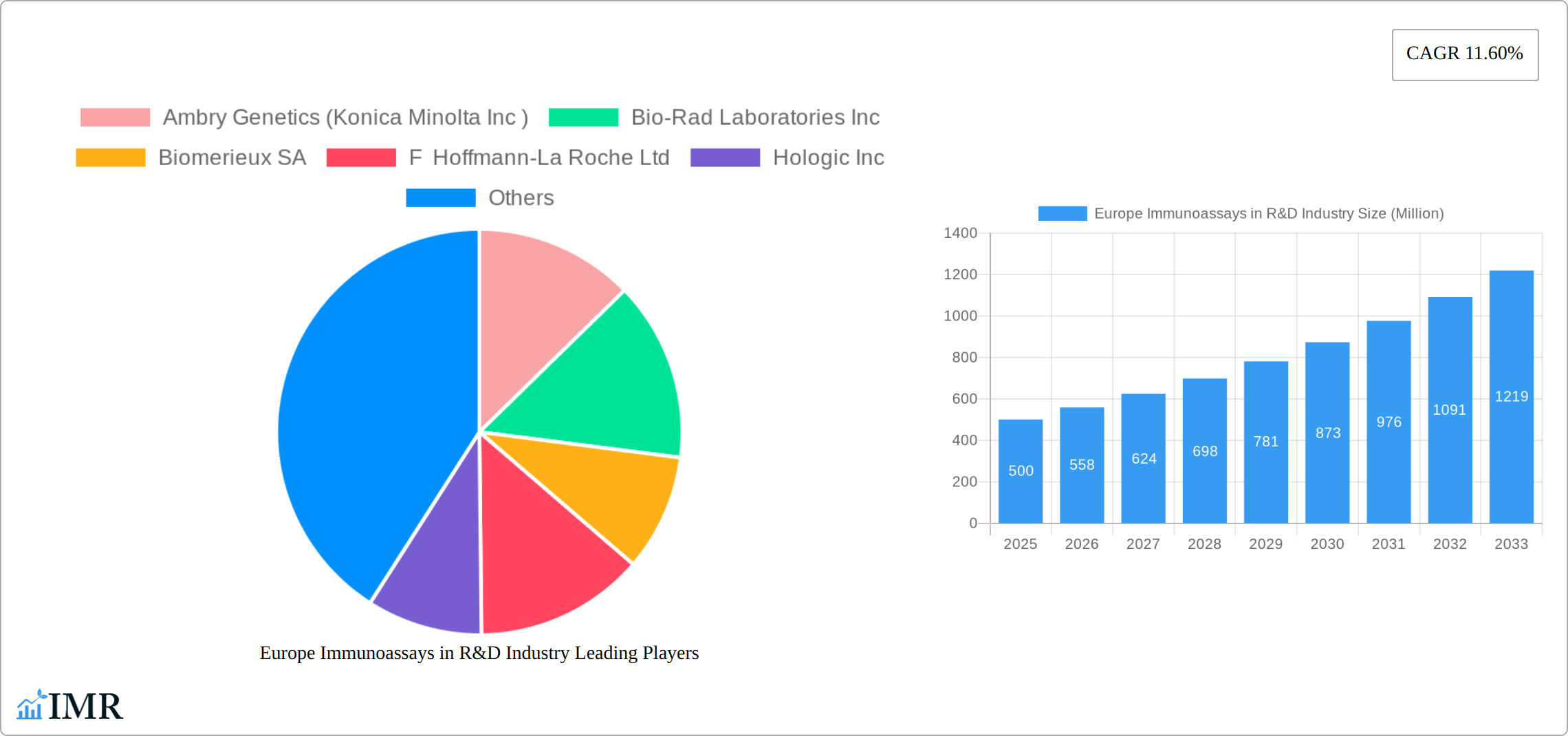

This comprehensive report provides a detailed analysis of the European immunoassays market within the R&D industry, offering invaluable insights for stakeholders, investors, and industry professionals. The report covers the period 2019-2033, with a focus on the 2025-2033 forecast period. It segments the market by disease (Prostate Cancer, Breast Cancer, Lung Cancer, Colorectal Cancer, Cervical Cancer, Other Diseases), biomarker type (Protein Biomarkers, Genetic Biomarkers, Other Types), and profiling technology (OMICS Technology, Imaging Technology, Immunoassays, Cytogenetics). Key players like Ambry Genetics (Konica Minolta Inc), Bio-Rad Laboratories Inc, Biomerieux SA, F Hoffmann-La Roche Ltd, Hologic Inc, Thermo Fisher Scientific Inc, Epigenomics AG, Quest Diagnostics, Qiagen AG, Creative Diagnostics, 23andMe, Johnson & Johnson Services Inc, Illumina Inc, Abbott Laboratories Inc, PerkinElmer Inc, Agilent Technologies, and many others are analyzed in detail.

Europe Immunoassays in R&D Industry Market Dynamics & Structure

The European immunoassays market in the R&D sector is characterized by a moderately concentrated landscape, with a few major players holding significant market share. The market is driven by technological advancements in biomarker discovery and profiling technologies, particularly OMICS technologies and advanced immunoassays. Stringent regulatory frameworks, such as those enforced by the EMA (European Medicines Agency), influence product development and market entry. Competitive pressures from substitute technologies, like next-generation sequencing (NGS), exist, but the unique advantages of immunoassays, such as high sensitivity and specificity, ensure continued market demand. The market size in 2025 is estimated at xx Million units.

- Market Concentration: The top 5 players account for approximately xx% of the market share in 2025.

- Technological Innovation: Ongoing R&D in high-throughput screening and multiplexing technologies is driving market growth.

- Regulatory Landscape: Stringent regulatory approvals are a key barrier to entry, particularly for novel immunoassay platforms.

- Competitive Substitutes: Next-generation sequencing and other molecular diagnostics pose a competitive threat.

- M&A Activity: The number of M&A deals in this sector has averaged xx per year over the past 5 years, indicating significant consolidation.

- End-User Demographics: Academic research institutions, pharmaceutical companies, and biotechnology firms are the primary end-users.

Europe Immunoassays in R&D Industry Growth Trends & Insights

The European immunoassays market in R&D is experiencing robust growth, fueled by the increasing prevalence of chronic diseases and the rising demand for personalized medicine. The market size witnessed a CAGR of xx% during the historical period (2019-2024) and is projected to grow at a CAGR of xx% during the forecast period (2025-2033), reaching an estimated xx Million units by 2033. This growth is driven by factors such as increasing investments in R&D, technological advancements, and growing adoption of immunoassays in early disease detection and diagnosis. The market penetration of advanced immunoassay technologies is increasing steadily, particularly in the areas of cancer research and immunology. Consumer behavior shifts toward proactive healthcare management and personalized therapies contribute to market expansion. Furthermore, increased government funding for research into infectious diseases has spurred the development and adoption of new immunoassay-based diagnostic tools. Specific market segments showing particularly high growth include protein biomarkers in oncology and OMICS technology-based platforms for high-throughput screening.

Dominant Regions, Countries, or Segments in Europe Immunoassays in R&D Industry

Germany, France, and the UK are currently the leading countries in the European immunoassays R&D market, driven by a strong presence of pharmaceutical and biotechnology companies, well-established research infrastructure, and significant government funding for healthcare research. The oncology segment, specifically focusing on prostate, breast, and lung cancer, demonstrates the highest growth potential, due to rising disease prevalence and ongoing clinical research. Within biomarker types, protein biomarkers dominate the market, while OMICS technologies are experiencing rapid adoption due to their ability to process large datasets and identify multiple biomarkers simultaneously.

- Key Drivers (Germany): Strong pharmaceutical industry, robust R&D infrastructure, government support for healthcare innovation.

- Key Drivers (France): Significant investment in biotechnology and life sciences, increasing prevalence of chronic diseases.

- Key Drivers (UK): Well-established academic research institutions, attractive regulatory environment.

- Leading Segment (Oncology): High disease prevalence, strong focus on early detection and targeted therapies.

- Leading Biomarker Type (Protein Biomarkers): Established technology, ease of use, high sensitivity and specificity.

- Leading Profiling Technology (OMICS): Potential for high-throughput analysis and biomarker discovery.

Europe Immunoassays in R&D Industry Product Landscape

The immunoassays market features a wide range of products, from traditional ELISA kits to advanced multiplex assays and microfluidic-based platforms. Recent innovations focus on improving assay sensitivity, specificity, and throughput. Key advancements include the development of novel antibody reagents, improved detection technologies, and integrated automated platforms for high-throughput screening. Unique selling propositions include faster turnaround times, minimized sample volumes, and improved data analysis capabilities. The market is witnessing the emergence of point-of-care diagnostics, which could significantly impact the accessibility and affordability of immunoassays.

Key Drivers, Barriers & Challenges in Europe Immunoassays in R&D Industry

Key Drivers: The increasing prevalence of chronic diseases, the rising demand for personalized medicine, technological advancements in immunoassay technology, and substantial investments in R&D are major drivers for market growth. Government initiatives promoting healthcare innovation and supportive regulatory frameworks are also contributing factors.

Key Challenges: High costs associated with developing and validating novel immunoassays, stringent regulatory hurdles for obtaining market approvals, and competitive pressures from substitute diagnostic technologies are major challenges. Supply chain disruptions, particularly during pandemics, can also impact the availability of reagents and consumables. The complexities in biomarker discovery and validation can also slow market penetration. These challenges result in an estimated xx% reduction in overall market growth in 2025.

Emerging Opportunities in Europe Immunoassays in R&D Industry

Untapped market potential exists in developing immunoassays for early diagnosis of infectious diseases, personalized cancer therapies, and autoimmune disorders. The integration of artificial intelligence and machine learning for data analysis is another exciting opportunity. Evolving consumer preferences towards proactive healthcare management and home-based diagnostics create opportunities for point-of-care testing devices and direct-to-consumer immunoassays.

Growth Accelerators in the Europe Immunoassays in R&D Industry Industry

Technological breakthroughs in multiplexing technologies and automation, coupled with strategic partnerships between academic institutions, pharmaceutical companies, and diagnostic manufacturers, are accelerating market growth. Expansion into underserved markets and the development of novel immunoassay-based diagnostic tools for emerging infectious diseases and rare genetic disorders contribute to long-term growth potential.

Key Players Shaping the Europe Immunoassays in R&D Industry Market

- Ambry Genetics (Konica Minolta Inc)

- Bio-Rad Laboratories Inc

- Biomerieux SA

- F Hoffmann-La Roche Ltd

- Hologic Inc

- Thermo Fisher Scientific Inc

- Epigenomics AG

- Quest Diagnostics

- Qiagen AG

- Creative Diagnostics

- 23andMe

- Johnson & Johnson Services Inc

- Illumina Inc

- Abbott Laboratories Inc

- PerkinElmer Inc

- Agilent Technologies

- List Not Exhaustive

Notable Milestones in Europe Immunoassays in R&D Industry Sector

- November 2020: Agilent Technologies launched the Biomarker Pathologist Training Program.

- March 2020: Proteomedix launched Proclarix, a blood-based test for prostate cancer diagnosis.

In-Depth Europe Immunoassays in R&D Industry Market Outlook

The European immunoassays market in R&D exhibits strong long-term growth potential, driven by continuous technological innovation, increasing healthcare investments, and a rising prevalence of chronic diseases. Strategic partnerships and collaborations between key players are likely to accelerate market expansion. The focus on developing point-of-care diagnostics and personalized medicine solutions will shape future market dynamics. The market is projected to continue its trajectory of steady growth, offering significant opportunities for companies involved in the development, manufacturing, and distribution of immunoassays.

Europe Immunoassays in R&D Industry Segmentation

-

1. Disease

- 1.1. Prostate Cancer

- 1.2. Breast Cancer

- 1.3. Lung Cancer

- 1.4. Colorectal Cancer

- 1.5. Cervical Cancer

- 1.6. Other Diseases

-

2. Type

- 2.1. Protein Biomarkers

- 2.2. Genetic Biomarkers

- 2.3. Other Types

-

3. Profiling Technology

- 3.1. OMICS Technology

- 3.2. Imaging Technology

- 3.3. Immunoassays

- 3.4. Cytogenetics

Europe Immunoassays in R&D Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Europe Immunoassays in R&D Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Burden of Cancer and Higher Acceptance for Treatment; Increasing Focus on Innovative Drug Development

- 3.3. Market Restrains

- 3.3.1. High Cost of Diagnosis

- 3.4. Market Trends

- 3.4.1. The Lung Cancer Segment is Expected to Hold a Major Market Share in the European Cancer Biomarkers Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Disease

- 5.1.1. Prostate Cancer

- 5.1.2. Breast Cancer

- 5.1.3. Lung Cancer

- 5.1.4. Colorectal Cancer

- 5.1.5. Cervical Cancer

- 5.1.6. Other Diseases

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Protein Biomarkers

- 5.2.2. Genetic Biomarkers

- 5.2.3. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 5.3.1. OMICS Technology

- 5.3.2. Imaging Technology

- 5.3.3. Immunoassays

- 5.3.4. Cytogenetics

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Disease

- 6. Europe Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Disease

- 6.1.1. Prostate Cancer

- 6.1.2. Breast Cancer

- 6.1.3. Lung Cancer

- 6.1.4. Colorectal Cancer

- 6.1.5. Cervical Cancer

- 6.1.6. Other Diseases

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Protein Biomarkers

- 6.2.2. Genetic Biomarkers

- 6.2.3. Other Types

- 6.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 6.3.1. OMICS Technology

- 6.3.2. Imaging Technology

- 6.3.3. Immunoassays

- 6.3.4. Cytogenetics

- 6.1. Market Analysis, Insights and Forecast - by Disease

- 7. United Kingdom Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Disease

- 7.1.1. Prostate Cancer

- 7.1.2. Breast Cancer

- 7.1.3. Lung Cancer

- 7.1.4. Colorectal Cancer

- 7.1.5. Cervical Cancer

- 7.1.6. Other Diseases

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Protein Biomarkers

- 7.2.2. Genetic Biomarkers

- 7.2.3. Other Types

- 7.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 7.3.1. OMICS Technology

- 7.3.2. Imaging Technology

- 7.3.3. Immunoassays

- 7.3.4. Cytogenetics

- 7.1. Market Analysis, Insights and Forecast - by Disease

- 8. France Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Disease

- 8.1.1. Prostate Cancer

- 8.1.2. Breast Cancer

- 8.1.3. Lung Cancer

- 8.1.4. Colorectal Cancer

- 8.1.5. Cervical Cancer

- 8.1.6. Other Diseases

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Protein Biomarkers

- 8.2.2. Genetic Biomarkers

- 8.2.3. Other Types

- 8.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 8.3.1. OMICS Technology

- 8.3.2. Imaging Technology

- 8.3.3. Immunoassays

- 8.3.4. Cytogenetics

- 8.1. Market Analysis, Insights and Forecast - by Disease

- 9. Italy Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Disease

- 9.1.1. Prostate Cancer

- 9.1.2. Breast Cancer

- 9.1.3. Lung Cancer

- 9.1.4. Colorectal Cancer

- 9.1.5. Cervical Cancer

- 9.1.6. Other Diseases

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Protein Biomarkers

- 9.2.2. Genetic Biomarkers

- 9.2.3. Other Types

- 9.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 9.3.1. OMICS Technology

- 9.3.2. Imaging Technology

- 9.3.3. Immunoassays

- 9.3.4. Cytogenetics

- 9.1. Market Analysis, Insights and Forecast - by Disease

- 10. Spain Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Disease

- 10.1.1. Prostate Cancer

- 10.1.2. Breast Cancer

- 10.1.3. Lung Cancer

- 10.1.4. Colorectal Cancer

- 10.1.5. Cervical Cancer

- 10.1.6. Other Diseases

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Protein Biomarkers

- 10.2.2. Genetic Biomarkers

- 10.2.3. Other Types

- 10.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 10.3.1. OMICS Technology

- 10.3.2. Imaging Technology

- 10.3.3. Immunoassays

- 10.3.4. Cytogenetics

- 10.1. Market Analysis, Insights and Forecast - by Disease

- 11. Rest of Europe Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Disease

- 11.1.1. Prostate Cancer

- 11.1.2. Breast Cancer

- 11.1.3. Lung Cancer

- 11.1.4. Colorectal Cancer

- 11.1.5. Cervical Cancer

- 11.1.6. Other Diseases

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Protein Biomarkers

- 11.2.2. Genetic Biomarkers

- 11.2.3. Other Types

- 11.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 11.3.1. OMICS Technology

- 11.3.2. Imaging Technology

- 11.3.3. Immunoassays

- 11.3.4. Cytogenetics

- 11.1. Market Analysis, Insights and Forecast - by Disease

- 12. Germany Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 13. France Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 14. Italy Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 15. United Kingdom Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 16. Netherlands Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 17. Sweden Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 18. Rest of Europe Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 19. Competitive Analysis

- 19.1. Market Share Analysis 2024

- 19.2. Company Profiles

- 19.2.1 Ambry Genetics (Konica Minolta Inc )

- 19.2.1.1. Overview

- 19.2.1.2. Products

- 19.2.1.3. SWOT Analysis

- 19.2.1.4. Recent Developments

- 19.2.1.5. Financials (Based on Availability)

- 19.2.2 Bio-Rad Laboratories Inc

- 19.2.2.1. Overview

- 19.2.2.2. Products

- 19.2.2.3. SWOT Analysis

- 19.2.2.4. Recent Developments

- 19.2.2.5. Financials (Based on Availability)

- 19.2.3 Biomerieux SA

- 19.2.3.1. Overview

- 19.2.3.2. Products

- 19.2.3.3. SWOT Analysis

- 19.2.3.4. Recent Developments

- 19.2.3.5. Financials (Based on Availability)

- 19.2.4 F Hoffmann-La Roche Ltd

- 19.2.4.1. Overview

- 19.2.4.2. Products

- 19.2.4.3. SWOT Analysis

- 19.2.4.4. Recent Developments

- 19.2.4.5. Financials (Based on Availability)

- 19.2.5 Hologic Inc

- 19.2.5.1. Overview

- 19.2.5.2. Products

- 19.2.5.3. SWOT Analysis

- 19.2.5.4. Recent Developments

- 19.2.5.5. Financials (Based on Availability)

- 19.2.6 Thermo Fisher Scientific Inc

- 19.2.6.1. Overview

- 19.2.6.2. Products

- 19.2.6.3. SWOT Analysis

- 19.2.6.4. Recent Developments

- 19.2.6.5. Financials (Based on Availability)

- 19.2.7 Epigenomics AG

- 19.2.7.1. Overview

- 19.2.7.2. Products

- 19.2.7.3. SWOT Analysis

- 19.2.7.4. Recent Developments

- 19.2.7.5. Financials (Based on Availability)

- 19.2.8 Quest Diagnostics

- 19.2.8.1. Overview

- 19.2.8.2. Products

- 19.2.8.3. SWOT Analysis

- 19.2.8.4. Recent Developments

- 19.2.8.5. Financials (Based on Availability)

- 19.2.9 Qiagen AG

- 19.2.9.1. Overview

- 19.2.9.2. Products

- 19.2.9.3. SWOT Analysis

- 19.2.9.4. Recent Developments

- 19.2.9.5. Financials (Based on Availability)

- 19.2.10 Creative Diagnostics

- 19.2.10.1. Overview

- 19.2.10.2. Products

- 19.2.10.3. SWOT Analysis

- 19.2.10.4. Recent Developments

- 19.2.10.5. Financials (Based on Availability)

- 19.2.11 23andMe

- 19.2.11.1. Overview

- 19.2.11.2. Products

- 19.2.11.3. SWOT Analysis

- 19.2.11.4. Recent Developments

- 19.2.11.5. Financials (Based on Availability)

- 19.2.12 Johnson & Johnson Services Inc

- 19.2.12.1. Overview

- 19.2.12.2. Products

- 19.2.12.3. SWOT Analysis

- 19.2.12.4. Recent Developments

- 19.2.12.5. Financials (Based on Availability)

- 19.2.13 Illumina Inc

- 19.2.13.1. Overview

- 19.2.13.2. Products

- 19.2.13.3. SWOT Analysis

- 19.2.13.4. Recent Developments

- 19.2.13.5. Financials (Based on Availability)

- 19.2.14 Abbott Laboratories Inc

- 19.2.14.1. Overview

- 19.2.14.2. Products

- 19.2.14.3. SWOT Analysis

- 19.2.14.4. Recent Developments

- 19.2.14.5. Financials (Based on Availability)

- 19.2.15 PerkinElmer Inc *List Not Exhaustive

- 19.2.15.1. Overview

- 19.2.15.2. Products

- 19.2.15.3. SWOT Analysis

- 19.2.15.4. Recent Developments

- 19.2.15.5. Financials (Based on Availability)

- 19.2.16 Agilent Technologies

- 19.2.16.1. Overview

- 19.2.16.2. Products

- 19.2.16.3. SWOT Analysis

- 19.2.16.4. Recent Developments

- 19.2.16.5. Financials (Based on Availability)

- 19.2.1 Ambry Genetics (Konica Minolta Inc )

List of Figures

- Figure 1: Europe Immunoassays in R&D Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Immunoassays in R&D Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 3: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 5: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 15: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 16: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 17: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Germany Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 20: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 21: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 22: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 23: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 24: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 25: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 26: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 28: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 29: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 30: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 31: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 32: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 33: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 34: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 35: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 36: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 37: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 38: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Immunoassays in R&D Industry?

The projected CAGR is approximately 11.60%.

2. Which companies are prominent players in the Europe Immunoassays in R&D Industry?

Key companies in the market include Ambry Genetics (Konica Minolta Inc ), Bio-Rad Laboratories Inc, Biomerieux SA, F Hoffmann-La Roche Ltd, Hologic Inc, Thermo Fisher Scientific Inc, Epigenomics AG, Quest Diagnostics, Qiagen AG, Creative Diagnostics, 23andMe, Johnson & Johnson Services Inc, Illumina Inc, Abbott Laboratories Inc, PerkinElmer Inc *List Not Exhaustive, Agilent Technologies.

3. What are the main segments of the Europe Immunoassays in R&D Industry?

The market segments include Disease, Type, Profiling Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Burden of Cancer and Higher Acceptance for Treatment; Increasing Focus on Innovative Drug Development.

6. What are the notable trends driving market growth?

The Lung Cancer Segment is Expected to Hold a Major Market Share in the European Cancer Biomarkers Market.

7. Are there any restraints impacting market growth?

High Cost of Diagnosis.

8. Can you provide examples of recent developments in the market?

In November 2020, Agilent Technologies announced the launch of the Biomarker Pathologist Training Program, a global initiative created to empower pathologists to score biomarkers accurately and confidently.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Immunoassays in R&D Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Immunoassays in R&D Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Immunoassays in R&D Industry?

To stay informed about further developments, trends, and reports in the Europe Immunoassays in R&D Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence