Key Insights

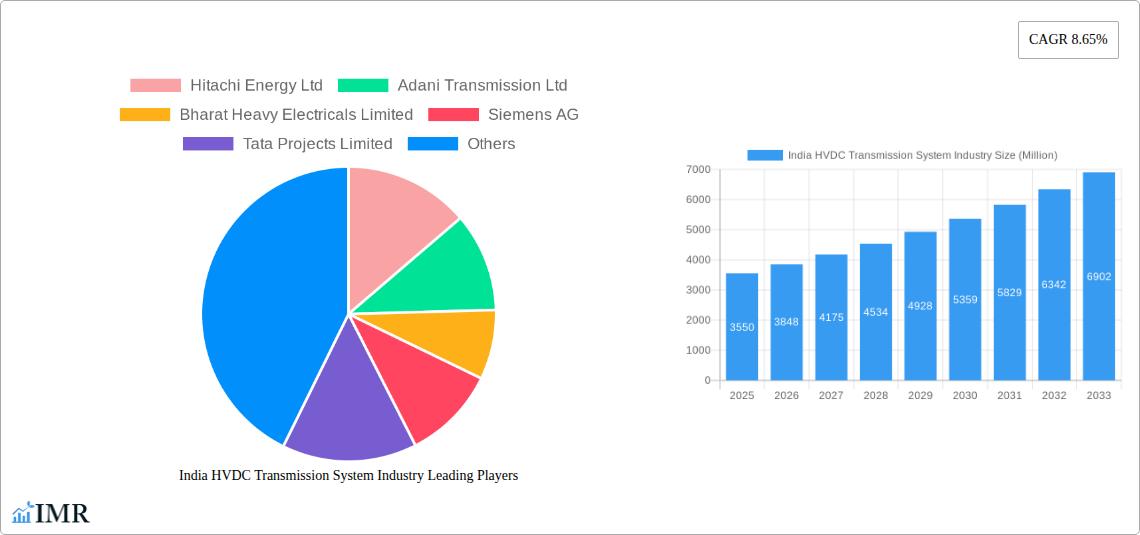

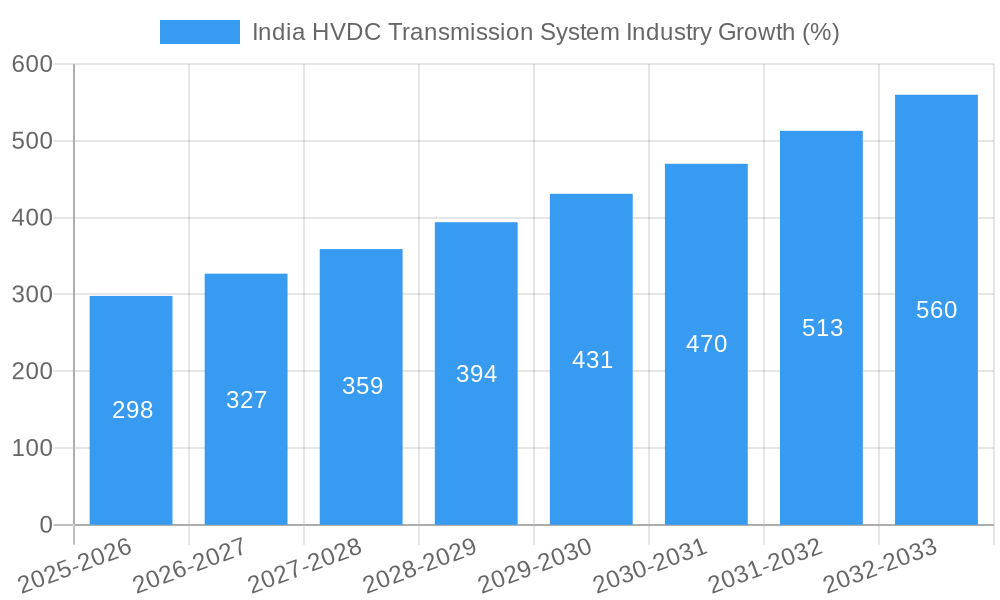

The India HVDC Transmission System market is experiencing robust growth, projected to reach \$3.55 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 8.65% from 2025 to 2033. This expansion is driven by several key factors. Increasing electricity demand, particularly in rapidly developing regions, necessitates efficient long-distance power transmission solutions. HVDC technology offers significant advantages over traditional AC systems, including reduced transmission losses, increased capacity on existing rights-of-way, and enhanced stability for integrating renewable energy sources like solar and wind power, which are often located far from load centers. Government initiatives promoting renewable energy integration and grid modernization further fuel market growth. The market segmentation reveals a strong demand for converter stations and cables, with both overhead and underground/submarine HVDC transmission systems contributing significantly. Leading players like Hitachi Energy, Adani Transmission, and Siemens are actively investing in expanding their capabilities and securing projects within this dynamic landscape. Regional variations exist, with the North and West regions potentially exhibiting faster growth due to existing infrastructure development and higher electricity consumption.

The continued growth trajectory is expected to be influenced by ongoing infrastructure investments, policy support for clean energy integration, and technological advancements in HVDC components. However, challenges remain, including the high initial capital cost of HVDC projects, the need for specialized expertise, and the complexities involved in land acquisition and permitting. Despite these restraints, the long-term outlook for the India HVDC Transmission System market remains positive, driven by the increasing urgency to address the nation's growing energy needs and the inherent advantages of HVDC technology in achieving this goal. The market's expansion is anticipated to attract further investment, competition, and innovation, leading to improved efficiency and cost-effectiveness in the coming years.

India HVDC Transmission System Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the India HVDC Transmission System industry, covering market dynamics, growth trends, key players, and future outlook. The report offers invaluable insights for industry professionals, investors, and policymakers seeking to understand and capitalize on the opportunities within this rapidly evolving sector. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year.

Parent Market: India Power Transmission Industry Child Market: India HVDC Transmission System Industry

India HVDC Transmission System Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory environment, and market trends within the Indian HVDC transmission system market. The analysis covers the period from 2019 to 2024, providing a historical perspective for future forecasting.

Market Concentration: The Indian HVDC transmission system market exhibits a moderately concentrated structure, with a few major players holding significant market share. Power Grid Corporation of India Limited (PGCIL) holds a dominant position, while other key players such as Adani Transmission Ltd, Tata Projects Limited, and international players like Hitachi Energy Ltd and Siemens AG compete for market share. The market share distribution for 2024 is estimated as follows: PGCIL (45%), Adani Transmission (15%), Tata Projects (10%), Hitachi Energy (8%), Siemens (7%), Others (15%).

Technological Innovation: The industry is witnessing significant technological advancements, driven by the adoption of Voltage Source Converter (VSC) technology, as seen in the recent Pugalur-Thrissur project. Further innovation is focused on improving efficiency, reliability, and cost-effectiveness of HVDC systems. However, challenges remain in integrating advanced technologies with existing infrastructure.

Regulatory Framework: The Indian government's focus on improving power transmission infrastructure and promoting renewable energy sources is creating a favorable regulatory environment. Clear policies and supportive regulations are crucial for attracting investments and accelerating market growth. However, bureaucratic procedures and land acquisition challenges can hinder project implementation.

Competitive Product Substitutes: While HVDC is becoming increasingly preferred for long-distance and high-capacity power transmission, alternative technologies such as HVAC (High Voltage AC) transmission remain competitive, particularly for shorter distances.

End-User Demographics: The primary end-users are power utilities, renewable energy developers, and industrial consumers requiring large-scale power transmission. The growth of renewable energy sources is a crucial driver for HVDC system adoption.

M&A Trends: The past five years have witnessed a moderate level of mergers and acquisitions (M&A) activity in the sector, driven primarily by the consolidation efforts of larger players aiming to enhance their market presence and technological capabilities. xx M&A deals were recorded between 2019 and 2024, with a total value of approximately xx million.

India HVDC Transmission System Industry Growth Trends & Insights

The Indian HVDC transmission system market is projected to experience robust growth over the forecast period (2025-2033). Driven by increasing electricity demand, the expansion of renewable energy integration, and government initiatives to enhance grid infrastructure, the market is expected to witness significant expansion. This analysis leverages secondary research data and expert industry forecasts to present this comprehensive overview.

The market size in 2024 is estimated at xx million, with a CAGR of xx% during the historical period (2019-2024). The market is projected to reach xx million by 2033, driven by factors including increased investment in renewable energy projects, expanding transmission networks, and government policies promoting grid modernization. Key trends driving growth include increased adoption of VSC technology, rising demand for long-distance power transmission, and the growing need for reliable and efficient energy transmission to meet India's burgeoning energy requirements. The adoption rate of HVDC technology is increasing steadily, driven by its suitability for large-scale renewable energy integration, and is expected to achieve xx% market penetration by 2033. Technological disruptions like the implementation of advanced grid management systems and smart grid technologies are further augmenting the market's overall potential. Consumer behavior shifts towards greater demand for reliable power supply and acceptance of renewable energy further solidify the long-term growth prospects for HVDC.

Dominant Regions, Countries, or Segments in India HVDC Transmission System Industry

This section identifies the leading regions, countries, or segments within the Indian HVDC transmission system market driving market growth.

Transmission Type: HVDC Overhead Transmission Systems currently dominate the market due to their lower initial cost compared to underground/submarine systems. However, HVDC Underground & Submarine Transmission Systems are experiencing faster growth, driven by the need for reliable transmission in densely populated areas and challenging terrains.

Component: Converter Stations represent a larger market share compared to Transmission Medium (Cables). This is due to the higher capital expenditure involved in setting up converter stations, which are essential for the conversion of AC to DC and vice-versa. However, the transmission medium (cables) segment is poised for significant growth, driven by the increasing adoption of underground and submarine transmission systems.

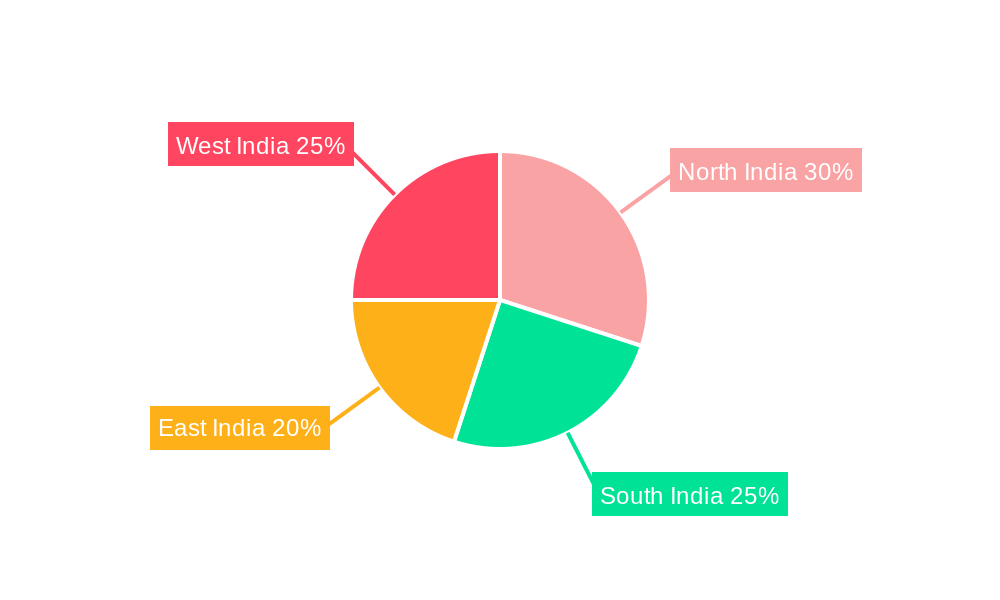

Regional Dominance: The Western and Southern regions of India are currently leading in HVDC transmission system adoption due to high electricity demand, the presence of large renewable energy projects, and favorable government initiatives in these regions. However, other regions are expected to witness significant growth in the coming years, as the government pushes for nationwide grid modernization.

Key Drivers:

- Government policies promoting renewable energy integration.

- Increasing demand for long-distance power transmission.

- Growing investments in grid modernization projects.

- Development of advanced HVDC technologies.

India HVDC Transmission System Industry Product Landscape

The Indian HVDC transmission system market offers a range of products, including converter stations, overhead lines, and underground/submarine cables. Recent innovations focus on improving efficiency, reliability, and capacity. Key technological advancements include the use of VSC technology, which enhances grid stability and allows for better integration of renewable energy sources. Manufacturers are focusing on developing compact and modular designs to reduce installation costs and improve ease of maintenance. Unique selling propositions include improved energy efficiency, enhanced grid stability, and optimized power transfer capabilities. Many manufacturers are offering customized solutions to meet specific client needs, further contributing to the market's dynamism.

Key Drivers, Barriers & Challenges in India HVDC Transmission System Industry

Key Drivers: The Indian HVDC transmission system market is primarily driven by the increasing demand for electricity, the government's push for renewable energy integration, and the need for improved grid infrastructure. The government's commitment to strengthening the nation's power transmission network creates a strong foundation for market expansion. Furthermore, technological advancements and the falling cost of HVDC technology are accelerating market growth.

Key Challenges and Restraints: Challenges include the high capital investment required for HVDC projects, land acquisition issues, and regulatory complexities. Supply chain disruptions and the dependence on imported components can impact project timelines and costs. The competitive landscape adds pressure, forcing companies to constantly innovate to remain profitable. The complexity of integrating HVDC technology into existing grids also poses a significant challenge.

Emerging Opportunities in India HVDC Transmission System Industry

Significant opportunities exist in expanding HVDC transmission infrastructure to connect remote renewable energy sources to the national grid. The increasing demand for efficient long-distance power transmission creates potential for further market expansion. The growing emphasis on grid modernization and smart grid technologies opens up opportunities for innovative solutions. Moreover, the potential for technological advancement and cost reduction in HVDC technology will further fuel opportunities in untapped markets and emerging applications.

Growth Accelerators in the India HVDC Transmission System Industry Industry

Long-term growth in the Indian HVDC transmission system market will be driven by ongoing investments in grid modernization, strategic partnerships between domestic and international players, and technological innovations that reduce costs and enhance efficiency. Expanding into untapped markets and focusing on customized solutions tailored to specific client needs will also drive market expansion. The government's continued support for renewable energy integration, alongside evolving grid management strategies, remains a significant catalyst.

Key Players Shaping the India HVDC Transmission System Industry Market

- Hitachi Energy Ltd

- Adani Transmission Ltd

- Bharat Heavy Electricals Limited

- Siemens AG

- Tata Projects Limited

- TAG Corporation

- General Electric Company

- Power Grid Corporation of India Limited

Notable Milestones in India HVDC Transmission System Industry Sector

- February 2021: Power Grid Corporation of India Limited (POWERGRID) inaugurated its 320 kV 2000 MW Pugalur (Tamil Nadu) - Thrissur (Kerala) HVDC project, marking the first use of VSC technology in the country. This project significantly impacted market dynamics by demonstrating the feasibility and benefits of VSC technology.

- December 2020: The Maharashtra Government announced plans to invest INR 8000 crore on an 80-kilometer underground HVDC line, highlighting the growing preference for underground transmission solutions in densely populated areas.

In-Depth India HVDC Transmission System Industry Market Outlook

The Indian HVDC transmission system market is poised for significant growth over the next decade. Continued government support for grid modernization, coupled with increasing renewable energy integration and technological advancements, will drive market expansion. Strategic partnerships and investments in R&D will play a crucial role in accelerating market growth. The focus on cost optimization and the development of customized solutions tailored to specific needs will be key factors in shaping the future of the Indian HVDC transmission system market. The potential for untapped markets and emerging applications presents exciting opportunities for industry players.

India HVDC Transmission System Industry Segmentation

-

1. Transmission Type

- 1.1. HVDC Overhead Transmission System

- 1.2. HVDC Underground & Submarine Transmission System

-

2. Component

- 2.1. Converter Stations

- 2.2. Transmission Medium (Cables)

India HVDC Transmission System Industry Segmentation By Geography

- 1. India

India HVDC Transmission System Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.65% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Demand For Power Quality In Industrial And Manufacturing Sectors4.; Increase In Smart Grid Infrastructure

- 3.3. Market Restrains

- 3.3.1. 4.; High Costs Of Power Quality Equipment

- 3.4. Market Trends

- 3.4.1. HVDC Overhead Transmission Systems Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India HVDC Transmission System Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Transmission Type

- 5.1.1. HVDC Overhead Transmission System

- 5.1.2. HVDC Underground & Submarine Transmission System

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. Converter Stations

- 5.2.2. Transmission Medium (Cables)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Transmission Type

- 6. North India India HVDC Transmission System Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India India HVDC Transmission System Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India India HVDC Transmission System Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India India HVDC Transmission System Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Hitachi Energy Ltd

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Adani Transmission Ltd

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Bharat Heavy Electricals Limited

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Siemens AG

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Tata Projects Limited

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 TAG Corporation

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 General Electric Company

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Power Grid Corporation of India Limited

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.1 Hitachi Energy Ltd

List of Figures

- Figure 1: India HVDC Transmission System Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India HVDC Transmission System Industry Share (%) by Company 2024

List of Tables

- Table 1: India HVDC Transmission System Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India HVDC Transmission System Industry Revenue Million Forecast, by Transmission Type 2019 & 2032

- Table 3: India HVDC Transmission System Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 4: India HVDC Transmission System Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: India HVDC Transmission System Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: North India India HVDC Transmission System Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: South India India HVDC Transmission System Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: East India India HVDC Transmission System Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: West India India HVDC Transmission System Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: India HVDC Transmission System Industry Revenue Million Forecast, by Transmission Type 2019 & 2032

- Table 11: India HVDC Transmission System Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 12: India HVDC Transmission System Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India HVDC Transmission System Industry?

The projected CAGR is approximately 8.65%.

2. Which companies are prominent players in the India HVDC Transmission System Industry?

Key companies in the market include Hitachi Energy Ltd, Adani Transmission Ltd, Bharat Heavy Electricals Limited, Siemens AG, Tata Projects Limited, TAG Corporation, General Electric Company, Power Grid Corporation of India Limited.

3. What are the main segments of the India HVDC Transmission System Industry?

The market segments include Transmission Type, Component.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.55 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Demand For Power Quality In Industrial And Manufacturing Sectors4.; Increase In Smart Grid Infrastructure.

6. What are the notable trends driving market growth?

HVDC Overhead Transmission Systems Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Costs Of Power Quality Equipment.

8. Can you provide examples of recent developments in the market?

In February 2021, Power Grid Corporation of India Limited (POWERGRID) inaugurated its 320 kV 2000 MW Pugalur (Tamil Nadu) - Thrissur (Kerala) HVDC project. The project was the first time a Voltage Source Converter (VSC) technology has been used introduced in the country for transmission. Out of the 165 kilometers (km) of the transmission, 27 Km were underground cables. The overall project cost was approximately INR 5070 crores.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India HVDC Transmission System Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India HVDC Transmission System Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India HVDC Transmission System Industry?

To stay informed about further developments, trends, and reports in the India HVDC Transmission System Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence