Key Insights

The semiconductor foundry market is experiencing robust growth, driven by the increasing demand for advanced semiconductor devices across various applications. The market, currently valued at approximately $XX million in 2025 (assuming a logical extrapolation based on the provided CAGR of 7.67% and a 2019-2024 historical period), is projected to expand significantly over the forecast period (2025-2033). This growth is fueled by several key factors, including the proliferation of consumer electronics (smartphones, wearables, IoT devices), the rapid expansion of the automotive sector (autonomous driving, advanced driver-assistance systems), and the escalating need for high-performance computing (HPC) capabilities in data centers and cloud infrastructure. Technological advancements, such as the transition to smaller technology nodes (e.g., 5nm, 3nm) and the development of new materials and packaging technologies, are further propelling market expansion. The market segmentation highlights a strong demand across various technology nodes, with 10/7/5nm and 16/14nm nodes dominating due to their performance advantages in advanced applications. The leading players, including TSMC, Samsung Foundry, Intel, Globalfoundries, and UMC, are heavily investing in research and development to maintain their competitive edge, fueling innovation and driving market growth.

However, the market faces certain challenges. Geopolitical uncertainties, supply chain disruptions, and the increasing complexity and cost of advanced node manufacturing pose significant restraints. Competition is fierce, with established players vying for market share while emerging foundries strive to gain traction. Despite these constraints, the long-term outlook for the semiconductor foundry market remains positive, driven by continuous technological innovation and increasing demand from diverse end-use sectors. The market's future will likely be shaped by strategic alliances, mergers and acquisitions, and the ongoing battle for technological supremacy among leading players. The continued growth in demand for higher performance, lower power consumption, and smaller form factors across numerous industries ensures a sustainable trajectory for this critical sector of the electronics industry.

Semiconductor Foundry Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Semiconductor Foundry Market, encompassing market dynamics, growth trends, regional dominance, product landscape, key players, and future outlook. The study period spans 2019-2033, with 2025 as the base and estimated year, and a forecast period of 2025-2033. The report is crucial for industry professionals, investors, and strategists seeking to understand this rapidly evolving market. The market is segmented by technology node (10/7/5 nm, 16/14 nm, 20 nm, 28 nm, 45/40 nm, 65 nm, Other Technology Nodes) and application (Consumer Electronics and Communication, Automotive, Industrial, HPC, Other Applications).

Semiconductor Foundry Market Market Dynamics & Structure

The Semiconductor Foundry market is characterized by a high level of consolidation, with a few major players commanding significant market share. The market's dynamics are shaped by intense technological innovation, stringent regulatory frameworks, and the emergence of competitive product substitutes. The industry is witnessing continuous mergers and acquisitions (M&A) activity, aiming to consolidate market power and expand technological capabilities. The parent market encompasses the broader semiconductor industry, while this child market focuses specifically on foundry services.

- Market Concentration: The top 5 players hold approximately xx% of the global market share in 2025 (estimated).

- Technological Innovation: Continuous advancements in process technology nodes (e.g., 5nm, 3nm) drive market growth, but high R&D costs present significant barriers to entry for smaller players.

- Regulatory Frameworks: Government policies and regulations regarding export controls and intellectual property rights significantly influence market dynamics, especially in relation to geopolitical tensions between major players.

- Competitive Product Substitutes: Advances in alternative technologies, such as photonics and quantum computing, pose potential long-term challenges.

- End-User Demographics: The growth is fueled by increasing demand from various sectors, particularly consumer electronics, automotive, and high-performance computing (HPC).

- M&A Trends: The past five years have seen xx major M&A deals, averaging xx million USD per deal, indicating a strong trend toward consolidation.

Semiconductor Foundry Market Growth Trends & Insights

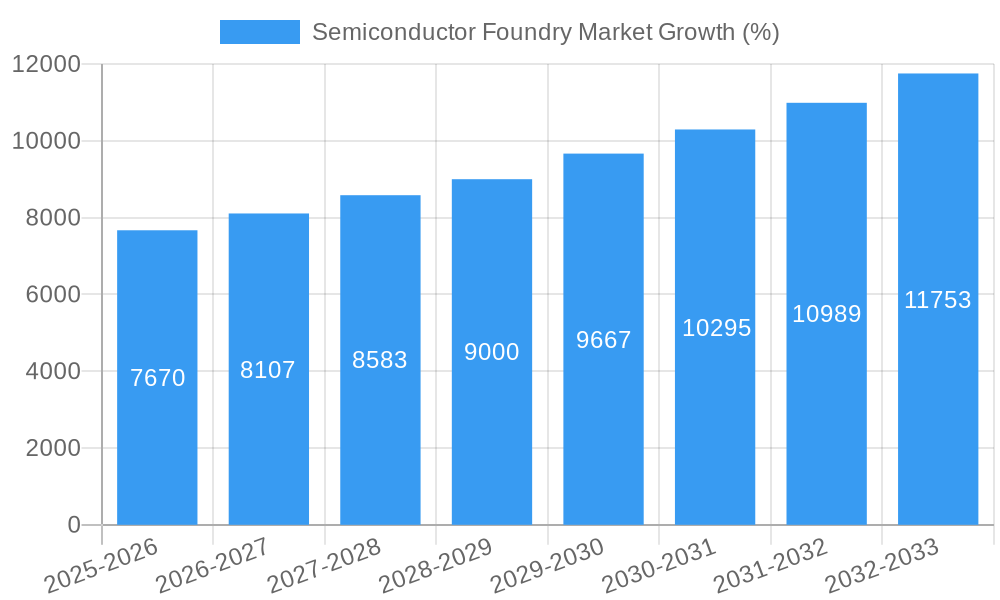

The Semiconductor Foundry market is experiencing robust growth, driven by the increasing demand for advanced semiconductor chips across diverse applications. The market size is projected to reach xx million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth reflects increasing adoption rates across various sectors. The historical period (2019-2024) showed a CAGR of yy%, laying the groundwork for sustained future expansion. Technological disruptions, such as the shift towards advanced packaging and heterogeneous integration, are further fueling market expansion. Consumer behavior is also shifting towards more sophisticated and energy-efficient devices, further increasing demand. Market penetration in emerging economies is also a significant growth driver.

Dominant Regions, Countries, or Segments in Semiconductor Foundry Market

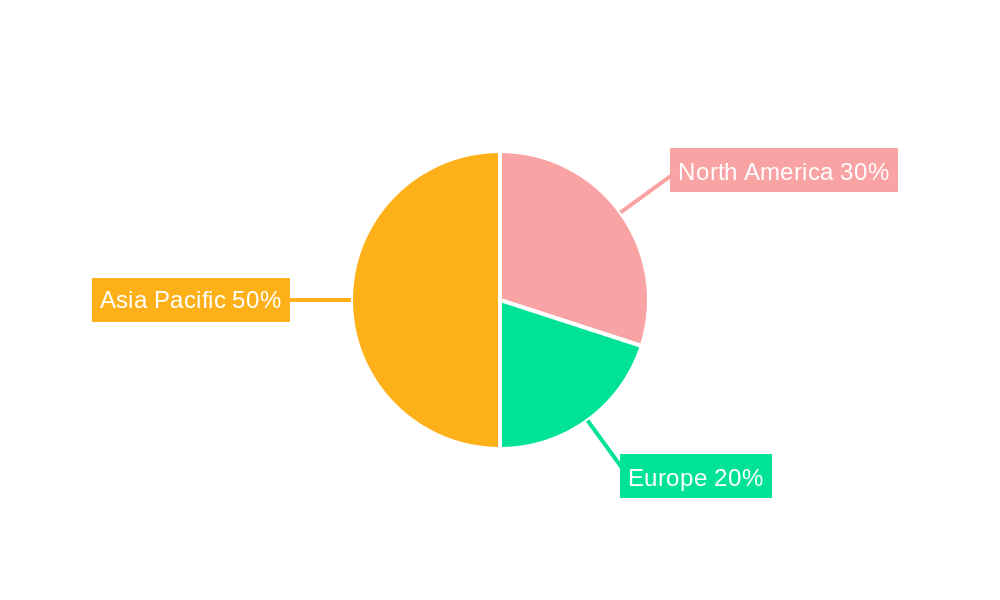

The Asia-Pacific region dominates the Semiconductor Foundry market, driven by strong manufacturing capabilities in countries like Taiwan, South Korea, and China. Within technology nodes, the 28nm and 16/14nm nodes currently hold the largest market share, though the 10/7/5nm segment is rapidly gaining traction due to higher performance needs of cutting-edge applications. The consumer electronics and communication sector is currently the largest application segment.

- Key Drivers in Asia-Pacific:

- Strong government support for the semiconductor industry.

- Abundant skilled labor and established supply chains.

- High concentration of major semiconductor foundries.

- High Growth Potential in Automotive and HPC:

- Increasing adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs) in the automotive industry.

- Growing demand for high-performance computing (HPC) in various applications such as AI and machine learning.

- Market Share: Taiwan holds approximately xx% of the global market share, followed by South Korea (xx%) and China (xx%).

Semiconductor Foundry Market Product Landscape

The semiconductor foundry market offers a wide range of products tailored to diverse customer needs, encompassing various technology nodes and specialized process capabilities. Continuous innovations focus on improving performance, reducing power consumption, and enhancing cost-effectiveness. Key innovations involve advanced packaging technologies like 3D stacking and chiplets, leading to higher integration density and improved system performance. Unique selling propositions center around superior process technology nodes, leading-edge manufacturing capabilities, and robust support for diverse applications.

Key Drivers, Barriers & Challenges in Semiconductor Foundry Market

Key Drivers: The market is primarily propelled by increasing demand for high-performance semiconductors in consumer electronics, automotive, industrial automation, and HPC sectors. Technological advancements like 5nm and beyond, along with government incentives for domestic semiconductor production in various regions, further accelerate growth.

Key Challenges: The industry faces significant challenges, including escalating capital expenditures for advanced technology nodes, geopolitical risks affecting supply chains, and intense competition. Supply chain disruptions, particularly in the availability of specialized materials and equipment, have a quantifiable impact, leading to production delays and increased costs. Regulatory hurdles related to export controls also impact market expansion.

Emerging Opportunities in Semiconductor Foundry Market

Emerging opportunities lie in the expansion of specialized foundry services catering to niche applications, such as quantum computing and advanced sensor technologies. The growth of IoT and edge computing is driving the need for specialized low-power semiconductors, offering significant potential. Furthermore, untapped markets in developing economies present immense growth possibilities.

Growth Accelerators in the Semiconductor Foundry Market Industry

Long-term growth is fueled by ongoing technological breakthroughs in process technology, materials science, and packaging. Strategic partnerships between foundries and design houses are accelerating innovation and enabling faster time-to-market. Aggressive expansion into new markets and applications, particularly in emerging economies and specialized sectors, is crucial for sustained growth.

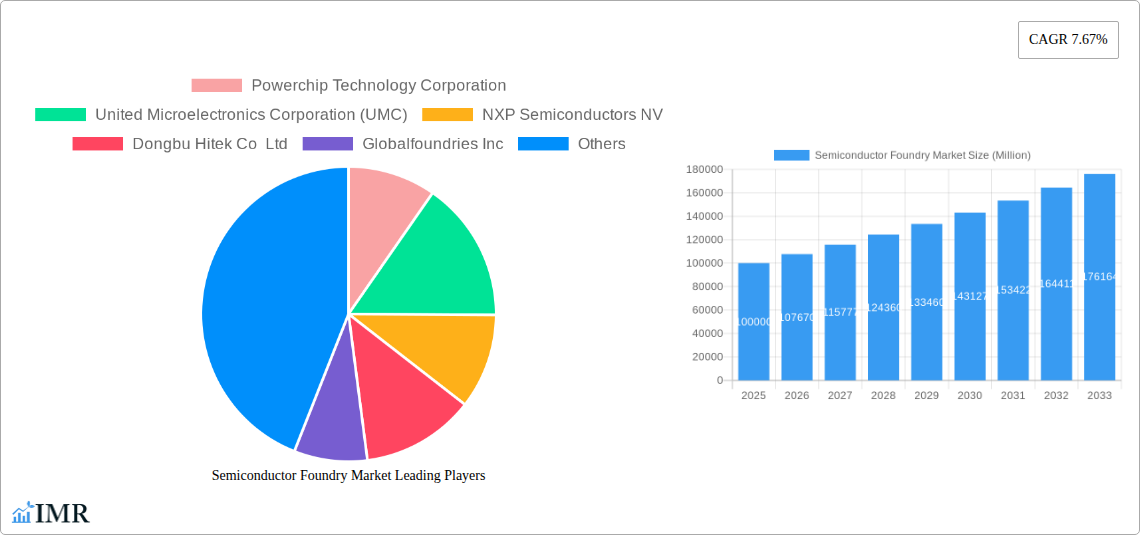

Key Players Shaping the Semiconductor Foundry Market Market

- Powerchip Technology Corporation

- United Microelectronics Corporation (UMC) [UMC Website]

- NXP Semiconductors NV [NXP Website]

- Dongbu Hitek Co Ltd

- Globalfoundries Inc [Globalfoundries Website]

- Texas Instruments Inc [TI Website]

- Vanguard International Semiconductor Corporation

- Tower Semiconductor Ltd [Tower Semiconductor Website]

- Hua Hong Semiconductor Limited

- Samsung Electronics Co Ltd (Samsung Foundry) [Samsung Semiconductor Website]

- TSMC Limited [TSMC Website]

- STMicroelectronics NV [STMicroelectronics Website]

- Renesas Electronics Corporation [Renesas Website]

- Semiconductor Manufacturing International Corporation (SMIC) [SMIC Website]

- X-FAB Silicon Foundries [X-FAB Website]

- Microchip Technologies Inc [Microchip Website]

- Intel Corporation [Intel Website]

Notable Milestones in Semiconductor Foundry Market Sector

- December 2022: EPC and Vanguard International Semiconductor Corporation (VIS) announced a multi-year production agreement for gallium nitride-based power semiconductors.

- November 2022: Hua Hong Semiconductor Ltd received regulatory approval for a USD 2.5 billion IPO.

In-Depth Semiconductor Foundry Market Market Outlook

The Semiconductor Foundry market is poised for continued strong growth, driven by technological advancements and increasing demand across diverse applications. Strategic investments in advanced manufacturing technologies, coupled with expansion into emerging markets, will be crucial for capturing significant market share. The focus on sustainability and energy efficiency within the semiconductor industry presents both challenges and opportunities for innovation and market leadership.

Semiconductor Foundry Market Segmentation

-

1. Technology Node

- 1.1. 10/7/5 nm

- 1.2. 16/14 nm

- 1.3. 20 nm

- 1.4. 28 nm

- 1.5. 45/40 nm

- 1.6. 65 nm

- 1.7. Other Technology Nodes

-

2. Application

- 2.1. Consumer Electronics and Communication

- 2.2. Automotive

- 2.3. Industrial

- 2.4. HPC

- 2.5. Other Applications

Semiconductor Foundry Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

Semiconductor Foundry Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.67% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Optimization of Semiconductor Processes through Analytics; Automotive

- 3.2.2 IoT

- 3.2.3 and AI Sectors are Driving the Market

- 3.3. Market Restrains

- 3.3.1. ; Lack of Technological Awareness

- 3.4. Market Trends

- 3.4.1. Consumer Electronics and Communication to be the Largest End-user Industry

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Semiconductor Foundry Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Technology Node

- 5.1.1. 10/7/5 nm

- 5.1.2. 16/14 nm

- 5.1.3. 20 nm

- 5.1.4. 28 nm

- 5.1.5. 45/40 nm

- 5.1.6. 65 nm

- 5.1.7. Other Technology Nodes

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Consumer Electronics and Communication

- 5.2.2. Automotive

- 5.2.3. Industrial

- 5.2.4. HPC

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Technology Node

- 6. North America Semiconductor Foundry Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Technology Node

- 6.1.1. 10/7/5 nm

- 6.1.2. 16/14 nm

- 6.1.3. 20 nm

- 6.1.4. 28 nm

- 6.1.5. 45/40 nm

- 6.1.6. 65 nm

- 6.1.7. Other Technology Nodes

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Consumer Electronics and Communication

- 6.2.2. Automotive

- 6.2.3. Industrial

- 6.2.4. HPC

- 6.2.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Technology Node

- 7. Europe Semiconductor Foundry Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Technology Node

- 7.1.1. 10/7/5 nm

- 7.1.2. 16/14 nm

- 7.1.3. 20 nm

- 7.1.4. 28 nm

- 7.1.5. 45/40 nm

- 7.1.6. 65 nm

- 7.1.7. Other Technology Nodes

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Consumer Electronics and Communication

- 7.2.2. Automotive

- 7.2.3. Industrial

- 7.2.4. HPC

- 7.2.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Technology Node

- 8. Asia Pacific Semiconductor Foundry Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Technology Node

- 8.1.1. 10/7/5 nm

- 8.1.2. 16/14 nm

- 8.1.3. 20 nm

- 8.1.4. 28 nm

- 8.1.5. 45/40 nm

- 8.1.6. 65 nm

- 8.1.7. Other Technology Nodes

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Consumer Electronics and Communication

- 8.2.2. Automotive

- 8.2.3. Industrial

- 8.2.4. HPC

- 8.2.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Technology Node

- 9. North America Semiconductor Foundry Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 9.1.1.

- 10. Europe Semiconductor Foundry Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1.

- 11. Asia Pacific Semiconductor Foundry Market Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Competitive Analysis

- 12.1. Global Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 Powerchip Technology Corporation

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 United Microelectronics Corporation (UMC)

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 NXP Semiconductors NV

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Dongbu Hitek Co Ltd

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Globalfoundries Inc

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Texas Instruments Inc

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Vanguard International Semiconductor Corporation

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Tower Semiconductor Ltd

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Hua Hong Semiconductor Limited

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Samsung Electronics Co Ltd (Samsung Foundry)

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.11 TSMC Limited

- 12.2.11.1. Overview

- 12.2.11.2. Products

- 12.2.11.3. SWOT Analysis

- 12.2.11.4. Recent Developments

- 12.2.11.5. Financials (Based on Availability)

- 12.2.12 STMicroelectronics NV

- 12.2.12.1. Overview

- 12.2.12.2. Products

- 12.2.12.3. SWOT Analysis

- 12.2.12.4. Recent Developments

- 12.2.12.5. Financials (Based on Availability)

- 12.2.13 Renesas Electronics Corporation

- 12.2.13.1. Overview

- 12.2.13.2. Products

- 12.2.13.3. SWOT Analysis

- 12.2.13.4. Recent Developments

- 12.2.13.5. Financials (Based on Availability)

- 12.2.14 Semiconductor Manufacturing International Corporation (SMIC)

- 12.2.14.1. Overview

- 12.2.14.2. Products

- 12.2.14.3. SWOT Analysis

- 12.2.14.4. Recent Developments

- 12.2.14.5. Financials (Based on Availability)

- 12.2.15 X-FAB Silicon Foundries

- 12.2.15.1. Overview

- 12.2.15.2. Products

- 12.2.15.3. SWOT Analysis

- 12.2.15.4. Recent Developments

- 12.2.15.5. Financials (Based on Availability)

- 12.2.16 Microchip Technologies Inc

- 12.2.16.1. Overview

- 12.2.16.2. Products

- 12.2.16.3. SWOT Analysis

- 12.2.16.4. Recent Developments

- 12.2.16.5. Financials (Based on Availability)

- 12.2.17 Intel Corporation

- 12.2.17.1. Overview

- 12.2.17.2. Products

- 12.2.17.3. SWOT Analysis

- 12.2.17.4. Recent Developments

- 12.2.17.5. Financials (Based on Availability)

- 12.2.1 Powerchip Technology Corporation

List of Figures

- Figure 1: Global Semiconductor Foundry Market Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Semiconductor Foundry Market Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Semiconductor Foundry Market Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Semiconductor Foundry Market Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Semiconductor Foundry Market Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Semiconductor Foundry Market Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Semiconductor Foundry Market Revenue Share (%), by Country 2024 & 2032

- Figure 8: North America Semiconductor Foundry Market Revenue (Million), by Technology Node 2024 & 2032

- Figure 9: North America Semiconductor Foundry Market Revenue Share (%), by Technology Node 2024 & 2032

- Figure 10: North America Semiconductor Foundry Market Revenue (Million), by Application 2024 & 2032

- Figure 11: North America Semiconductor Foundry Market Revenue Share (%), by Application 2024 & 2032

- Figure 12: North America Semiconductor Foundry Market Revenue (Million), by Country 2024 & 2032

- Figure 13: North America Semiconductor Foundry Market Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Semiconductor Foundry Market Revenue (Million), by Technology Node 2024 & 2032

- Figure 15: Europe Semiconductor Foundry Market Revenue Share (%), by Technology Node 2024 & 2032

- Figure 16: Europe Semiconductor Foundry Market Revenue (Million), by Application 2024 & 2032

- Figure 17: Europe Semiconductor Foundry Market Revenue Share (%), by Application 2024 & 2032

- Figure 18: Europe Semiconductor Foundry Market Revenue (Million), by Country 2024 & 2032

- Figure 19: Europe Semiconductor Foundry Market Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific Semiconductor Foundry Market Revenue (Million), by Technology Node 2024 & 2032

- Figure 21: Asia Pacific Semiconductor Foundry Market Revenue Share (%), by Technology Node 2024 & 2032

- Figure 22: Asia Pacific Semiconductor Foundry Market Revenue (Million), by Application 2024 & 2032

- Figure 23: Asia Pacific Semiconductor Foundry Market Revenue Share (%), by Application 2024 & 2032

- Figure 24: Asia Pacific Semiconductor Foundry Market Revenue (Million), by Country 2024 & 2032

- Figure 25: Asia Pacific Semiconductor Foundry Market Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Semiconductor Foundry Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Semiconductor Foundry Market Revenue Million Forecast, by Technology Node 2019 & 2032

- Table 3: Global Semiconductor Foundry Market Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Global Semiconductor Foundry Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Semiconductor Foundry Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Semiconductor Foundry Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Global Semiconductor Foundry Market Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Semiconductor Foundry Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Semiconductor Foundry Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Semiconductor Foundry Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Semiconductor Foundry Market Revenue Million Forecast, by Technology Node 2019 & 2032

- Table 12: Global Semiconductor Foundry Market Revenue Million Forecast, by Application 2019 & 2032

- Table 13: Global Semiconductor Foundry Market Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Global Semiconductor Foundry Market Revenue Million Forecast, by Technology Node 2019 & 2032

- Table 15: Global Semiconductor Foundry Market Revenue Million Forecast, by Application 2019 & 2032

- Table 16: Global Semiconductor Foundry Market Revenue Million Forecast, by Country 2019 & 2032

- Table 17: Global Semiconductor Foundry Market Revenue Million Forecast, by Technology Node 2019 & 2032

- Table 18: Global Semiconductor Foundry Market Revenue Million Forecast, by Application 2019 & 2032

- Table 19: Global Semiconductor Foundry Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Foundry Market?

The projected CAGR is approximately 7.67%.

2. Which companies are prominent players in the Semiconductor Foundry Market?

Key companies in the market include Powerchip Technology Corporation, United Microelectronics Corporation (UMC), NXP Semiconductors NV, Dongbu Hitek Co Ltd, Globalfoundries Inc, Texas Instruments Inc, Vanguard International Semiconductor Corporation, Tower Semiconductor Ltd, Hua Hong Semiconductor Limited, Samsung Electronics Co Ltd (Samsung Foundry), TSMC Limited, STMicroelectronics NV, Renesas Electronics Corporation, Semiconductor Manufacturing International Corporation (SMIC), X-FAB Silicon Foundries, Microchip Technologies Inc, Intel Corporation.

3. What are the main segments of the Semiconductor Foundry Market?

The market segments include Technology Node, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Optimization of Semiconductor Processes through Analytics; Automotive. IoT. and AI Sectors are Driving the Market.

6. What are the notable trends driving market growth?

Consumer Electronics and Communication to be the Largest End-user Industry.

7. Are there any restraints impacting market growth?

; Lack of Technological Awareness.

8. Can you provide examples of recent developments in the market?

December 2022 - EPC and Vanguard International Semiconductor Corporation (VIS) announced a multi-year production agreement for gallium nitride-based power semiconductors in December 2022. EPC will take advantage of VIS' 8-inch (200 mm) wafer fabrication capabilities, which is expected to significantly increase manufacturing capacity for EPC's high-performance GaN transistors and integrated circuits. Production will begin in early 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Foundry Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Foundry Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Foundry Market?

To stay informed about further developments, trends, and reports in the Semiconductor Foundry Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence