Key Insights

The mobile phone semiconductor industry, valued at approximately $XX million in 2025, is experiencing robust growth, projected to maintain a 7.49% Compound Annual Growth Rate (CAGR) from 2025 to 2033. This expansion is fueled by several key drivers. The increasing demand for advanced features in smartphones, such as high-resolution cameras, enhanced processing power for AI and augmented reality applications, and faster 5G connectivity, necessitates more sophisticated and powerful semiconductors. Furthermore, the burgeoning adoption of foldable and flexible displays is creating new opportunities within the market, requiring specialized components and driving innovation. While supply chain disruptions and fluctuating raw material prices pose challenges, the long-term outlook remains positive, driven by continuous technological advancements and the ever-increasing penetration of smartphones globally. The market is segmented by component type, encompassing mobile processors, memory chips (DRAM and NAND), logic chips, and analog components. Key players such as Qualcomm, Samsung, MediaTek, and others are fiercely competing to provide cutting-edge technology to meet the evolving needs of Original Equipment Manufacturers (OEMs). Regional growth is anticipated to be strongest in the Asia-Pacific region, driven by high smartphone adoption rates and manufacturing hubs in countries like China, South Korea, and India, followed by North America and Europe.

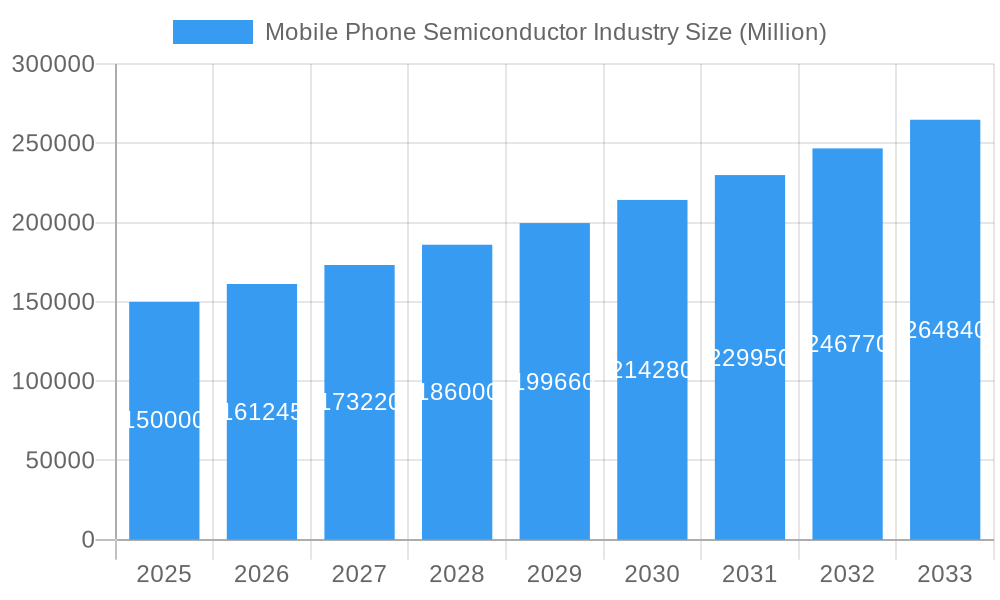

Mobile Phone Semiconductor Industry Market Size (In Billion)

The industry faces several restraints. Geopolitical instability and trade tensions can disrupt supply chains and increase component costs. The increasing complexity of semiconductor design and manufacturing necessitates substantial investments in research and development, potentially limiting market entry for smaller players. However, continuous innovation in areas like energy efficiency, miniaturization, and advanced processing capabilities will likely outweigh these restraints, contributing to sustained growth in the long term. The shift towards more advanced semiconductor nodes, such as 5nm and 3nm, further fuels industry growth by enabling enhanced performance and energy efficiency in mobile devices. The integration of AI capabilities directly into mobile processors is also a key trend, driving demand for specialized chips with high computational power.

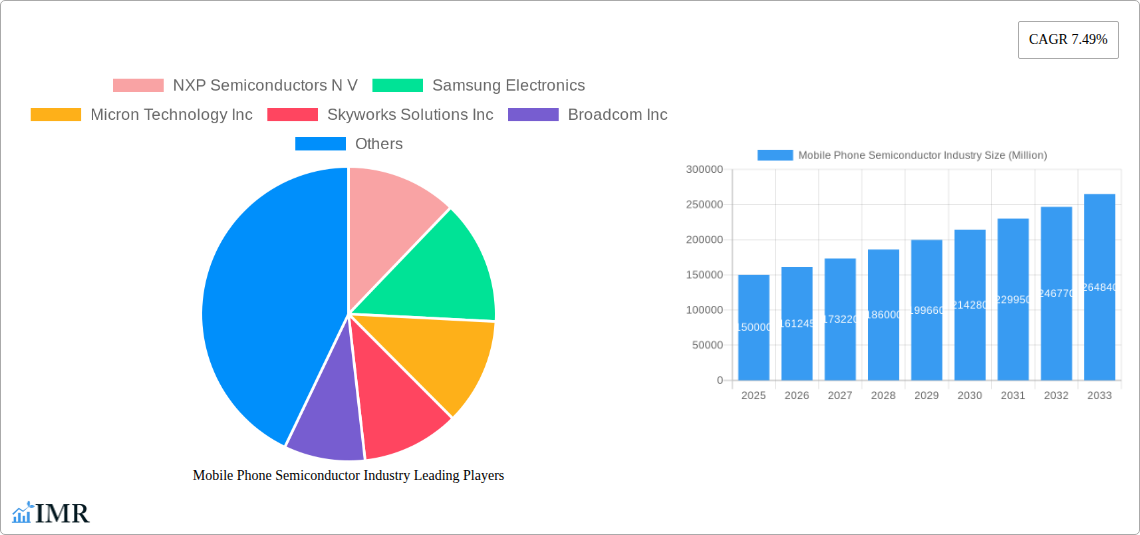

Mobile Phone Semiconductor Industry Company Market Share

Mobile Phone Semiconductor Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the mobile phone semiconductor industry, encompassing market dynamics, growth trends, key players, and future prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for industry professionals, investors, and strategic decision-makers. The report analyzes the parent market of semiconductors and the child market of mobile phone semiconductors, providing a granular view of market segments including Mobile Processors, Memory, Logic Chips, and Analog components. Market size is presented in million units.

Mobile Phone Semiconductor Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory influences, and market trends within the mobile phone semiconductor industry. The market is characterized by a high degree of concentration with a few dominant players holding significant market share. Technological innovation, particularly in areas like 5G, AI, and advanced memory technologies, is a key driver of market growth. Stringent regulatory frameworks, varying by region, impact production and distribution. The emergence of substitutes, like alternative computing architectures, poses a potential challenge, though the impact remains limited in the short term.

- Market Concentration: High, with top 10 players holding xx% market share in 2024 (Estimated).

- Technological Innovation: Driven by 5G, AI, and advanced memory technologies. Significant R&D investments are observed.

- Regulatory Frameworks: Vary significantly across regions, impacting production and trade.

- Competitive Substitutes: Limited impact currently, but alternative computing technologies are emerging.

- M&A Activity: xx major deals concluded between 2019-2024 (Estimated), indicating consolidation within the industry.

- End-User Demographics: Driven primarily by the growing adoption of smartphones globally, with significant regional variations.

Mobile Phone Semiconductor Industry Growth Trends & Insights

The mobile phone semiconductor market exhibits robust growth, driven by increasing smartphone penetration globally, particularly in emerging markets. The market size (in million units) is estimated to be xx in 2025, exhibiting a CAGR of xx% during the forecast period (2025-2033). This growth is fueled by technological disruptions, such as the adoption of 5G and the increasing demand for higher performance and energy-efficient mobile devices. Consumer behavior shifts towards premium smartphones and multi-device usage further contribute to this positive trend. Adoption rates for advanced semiconductor technologies are increasing steadily, mirroring overall market expansion.

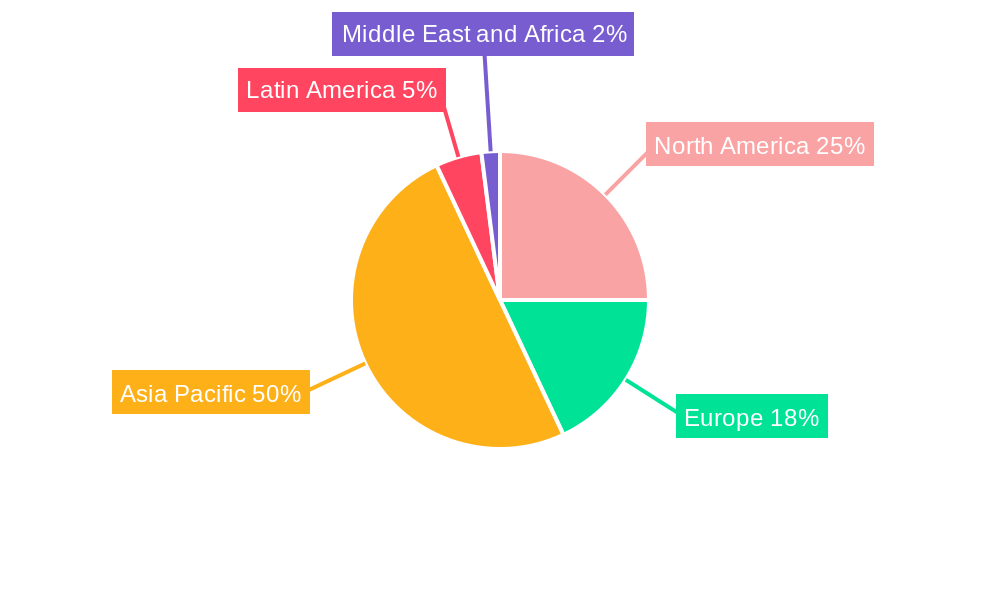

Dominant Regions, Countries, or Segments in Mobile Phone Semiconductor Industry

Asia, particularly East Asia, dominates the mobile phone semiconductor market, driven by high smartphone production and consumption. Within component types, Mobile Processors and Memory segments exhibit the strongest growth, reflecting the increasing demand for high-performance and large-capacity mobile devices.

- Key Drivers in Asia: Strong domestic demand, established manufacturing infrastructure, and favorable government policies.

- Mobile Processors Segment: Driven by demand for high-performance computing and advanced features in smartphones. Holding a market share of xx% in 2024 (Estimated).

- Memory Segment: Driven by the increasing storage needs of high-resolution cameras, video recording, and mobile applications. Holding a market share of xx% in 2024 (Estimated).

- Logic Chips Segment: Growth is moderate compared to mobile processors and memory, holding a market share of xx% in 2024 (Estimated).

- Analog Segment: Essential for various functions in mobile devices but with relatively slower growth than other segments, holding a market share of xx% in 2024 (Estimated).

Mobile Phone Semiconductor Industry Product Landscape

The mobile phone semiconductor landscape is characterized by continuous product innovation, focusing on enhanced performance, reduced power consumption, and miniaturization. New generations of mobile processors incorporate advanced AI capabilities, improved graphics processing, and increased energy efficiency. Memory chips are evolving towards higher density and lower power consumption. The development of innovative packaging technologies and 3D integration further enhances performance and reduces footprint. Unique selling propositions focus on enhanced speed, power efficiency, and integration capabilities.

Key Drivers, Barriers & Challenges in Mobile Phone Semiconductor Industry

Key Drivers: The increasing demand for smartphones, technological advancements in 5G and AI, and government support for the semiconductor industry are primary growth drivers.

Key Challenges: Supply chain disruptions, geopolitical uncertainties, and intense competition among major players pose significant challenges. These factors can lead to production delays, increased costs, and potential market share fluctuations.

Emerging Opportunities in Mobile Phone Semiconductor Industry

The growing adoption of IoT devices, the expanding automotive semiconductor market, and the rise of foldable smartphones present significant emerging opportunities. Further advancements in AI and 5G technology will drive demand for sophisticated semiconductor components.

Growth Accelerators in the Mobile Phone Semiconductor Industry

Technological breakthroughs in materials science, advanced packaging, and innovative architectures are key growth catalysts. Strategic partnerships between semiconductor manufacturers and mobile device makers enhance supply chain efficiency and product development. Expansion into emerging markets with high growth potential further accelerates industry growth.

Key Players Shaping the Mobile Phone Semiconductor Industry Market

- NXP Semiconductors N V

- Samsung Electronics

- Micron Technology Inc

- Skyworks Solutions Inc

- Broadcom Inc

- Qorvo Inc

- Qualcomm Technologies Inc

- Huawei Technologies Co Ltd

- MediaTek Inc

- Intel Corporation

Notable Milestones in Mobile Phone Semiconductor Industry Sector

- November 2022: Micron Technology launched its 1-beta DRAM, aiming for a 15% power efficiency and 35% bit density improvement.

- October 2022: Polymatech initiated production of Opto-semiconductors and memory modules, backed by USD 1 billion investment.

In-Depth Mobile Phone Semiconductor Industry Market Outlook

The mobile phone semiconductor industry is poised for sustained growth, driven by technological advancements, expanding applications, and increasing smartphone adoption globally. Strategic partnerships, investments in R&D, and expansion into new markets will shape the future landscape. The focus on energy efficiency, enhanced performance, and miniaturization will remain crucial for maintaining competitiveness.

Mobile Phone Semiconductor Industry Segmentation

-

1. Component Type

- 1.1. Mobile Processors

- 1.2. Memory

- 1.3. Logic Chips

- 1.4. Analog

Mobile Phone Semiconductor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Mobile Phone Semiconductor Industry Regional Market Share

Geographic Coverage of Mobile Phone Semiconductor Industry

Mobile Phone Semiconductor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Rapid Introduction of Next-generation Mobile-communications Standard

- 3.2.2 LTE or 4G; Emergence of 'Multicom' Solutions

- 3.3. Market Restrains

- 3.3.1. Complexity Regarding Manufacturing; Consumer Demand Exceeding Factory Capacity

- 3.4. Market Trends

- 3.4.1. Memory to Significantly Drive the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 5.1.1. Mobile Processors

- 5.1.2. Memory

- 5.1.3. Logic Chips

- 5.1.4. Analog

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 6. North America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 6.1.1. Mobile Processors

- 6.1.2. Memory

- 6.1.3. Logic Chips

- 6.1.4. Analog

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 7. Europe Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 7.1.1. Mobile Processors

- 7.1.2. Memory

- 7.1.3. Logic Chips

- 7.1.4. Analog

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 8. Asia Pacific Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 8.1.1. Mobile Processors

- 8.1.2. Memory

- 8.1.3. Logic Chips

- 8.1.4. Analog

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 9. Latin America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 9.1.1. Mobile Processors

- 9.1.2. Memory

- 9.1.3. Logic Chips

- 9.1.4. Analog

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 10. Middle East and Africa Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 10.1.1. Mobile Processors

- 10.1.2. Memory

- 10.1.3. Logic Chips

- 10.1.4. Analog

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 NXP Semiconductors N V

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Samsung Electronics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Micron Technology Inc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Skyworks Solutions Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Broadcom Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Qorvo Inc *List Not Exhaustive

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Qualcomm Technologies Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Huawei Technologies Co Ltd

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 MediaTek Inc

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Intel Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 NXP Semiconductors N V

List of Figures

- Figure 1: Global Mobile Phone Semiconductor Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 3: North America Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 4: North America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 7: Europe Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 8: Europe Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 11: Asia Pacific Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 12: Asia Pacific Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 15: Latin America Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 16: Latin America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Latin America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 19: Middle East and Africa Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 20: Middle East and Africa Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Middle East and Africa Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 2: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 4: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 6: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 8: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 10: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 12: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Phone Semiconductor Industry?

The projected CAGR is approximately 7.49%.

2. Which companies are prominent players in the Mobile Phone Semiconductor Industry?

Key companies in the market include NXP Semiconductors N V, Samsung Electronics, Micron Technology Inc, Skyworks Solutions Inc, Broadcom Inc, Qorvo Inc *List Not Exhaustive, Qualcomm Technologies Inc, Huawei Technologies Co Ltd, MediaTek Inc, Intel Corporation.

3. What are the main segments of the Mobile Phone Semiconductor Industry?

The market segments include Component Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Introduction of Next-generation Mobile-communications Standard. LTE or 4G; Emergence of 'Multicom' Solutions.

6. What are the notable trends driving market growth?

Memory to Significantly Drive the Market.

7. Are there any restraints impacting market growth?

Complexity Regarding Manufacturing; Consumer Demand Exceeding Factory Capacity.

8. Can you provide examples of recent developments in the market?

November 2022 - Micron Technology launched its 1-beta DRAM with an aim to improve power efficiency by 15% and bit density by 35% for memory chips. The new DRAM chips would underpin a new generation of memory chips for Micron.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mobile Phone Semiconductor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mobile Phone Semiconductor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mobile Phone Semiconductor Industry?

To stay informed about further developments, trends, and reports in the Mobile Phone Semiconductor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence