Key Insights

The Malaysian oil and gas pipeline industry is experiencing steady growth, fueled by increasing domestic energy demand and ongoing investments in infrastructure development. The market, estimated at approximately $XX million in 2025 (assuming a logical value based on typical market sizes for similar economies and the provided CAGR), exhibits a Compound Annual Growth Rate (CAGR) exceeding 2.50% from 2025-2033. This growth is driven primarily by the expansion of existing pipelines to accommodate rising production and transportation needs, coupled with government initiatives promoting energy security and infrastructure modernization. The onshore segment currently dominates the market, but the offshore sector is poised for significant expansion as exploration activities in deeper waters increase. Crude oil pipelines currently hold a larger market share than gas pipelines, reflecting Malaysia's historical reliance on oil exports, though the gas pipeline segment is anticipated to experience faster growth due to increasing natural gas utilization for power generation and industrial processes. However, regulatory hurdles and environmental concerns related to pipeline construction and operation represent key restraints on market expansion. Key players, including PETRONAS, Sapura Energy Berhad, and international contractors, are actively involved in project development and maintenance, shaping the competitive landscape.

The forecast period (2025-2033) anticipates continued growth, driven by several factors. These include ongoing investments in upstream oil and gas exploration and production, the need for enhanced pipeline infrastructure to facilitate efficient transportation, and the growing demand for energy within Malaysia. While challenges such as fluctuating global energy prices and environmental regulations exist, the overall outlook for the Malaysian oil and gas pipeline industry remains positive, with potential for significant expansion, particularly in the offshore and gas pipeline segments. Strategic partnerships between international and domestic companies are expected to further drive innovation and technological advancements within the sector, leading to improvements in efficiency and safety.

Malaysia Oil & Gas Pipeline Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of the Malaysia Oil & Gas Pipeline Industry, covering market dynamics, growth trends, key players, and future outlook. With a focus on both onshore and offshore deployments, as well as crude oil and gas pipelines, this report is an essential resource for industry professionals, investors, and strategic decision-makers. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year.

Malaysia Oil & Gas Pipeline Industry Market Dynamics & Structure

The Malaysian oil and gas pipeline sector presents a dynamic landscape shaped by competitive pressures, technological advancements, regulatory oversight, and evolving market trends. The market exhibits moderate concentration, with a mix of established industry giants and specialized smaller companies vying for market share.

Market Concentration and Competitive Landscape: While precise market share figures are commercially sensitive, the landscape is characterized by PETRONAS holding a significant share, followed by other major players like Sapura Energy Berhad and a number of smaller, specialized firms. This structure fosters competition while also allowing for potential organic growth and strategic mergers and acquisitions (M&A) activity. The competitive landscape is further influenced by the availability of alternative transportation methods.

Technological Innovation and Digitalization: The industry is undergoing a significant transformation driven by technological advancements. This includes the widespread adoption of subsea pipeline construction and repair technologies (e.g., remotely operated vehicles (ROVs) and automated welding systems), the utilization of high-strength corrosion-resistant alloys, and sophisticated pipeline monitoring and management systems incorporating data analytics and AI-driven predictive maintenance. While these innovations enhance pipeline efficiency, safety, and environmental performance, substantial upfront investments and the requirement for a skilled workforce present challenges to widespread and rapid adoption.

Regulatory Framework and Policy Landscape: The Malaysian government's regulatory framework, largely overseen by PETRONAS, plays a pivotal role in shaping industry practices and investment decisions. Regulations focused on safety, environmental protection, and operational efficiency significantly impact project viability and operational procedures. Compliance with these regulations is paramount for all stakeholders.

Competitive Transportation Alternatives: Although pipelines remain the primary mode for oil and gas transportation in Malaysia, alternative transportation methods pose a degree of competition, particularly for shorter distances. Road and rail transport of refined products offer viable alternatives for shorter distances, while LNG shipping plays a role in long-distance transportation. This competition necessitates continuous innovation and cost optimization within the pipeline sector.

End-User Dynamics and Market Demand: The key end-users within the Malaysian oil and gas pipeline industry include power generation companies, industrial consumers, and the petrochemical sector. Their demand is heavily influenced by energy prices, economic growth, and evolving energy policies. The demand profile further influences investment decisions and pipeline expansion strategies.

Mergers and Acquisitions (M&A) Activity: The M&A landscape in the Malaysian oil and gas pipeline sector has seen considerable activity in recent years, though the pace may moderate based on market consolidation and prevailing macroeconomic conditions. Analyzing past M&A trends provides valuable insights into strategic shifts and future consolidation potential within the industry.

Malaysia Oil & Gas Pipeline Industry Growth Trends & Insights

The Malaysian oil and gas pipeline industry has demonstrated consistent growth in recent years (2019-2024), driven primarily by rising domestic energy demand, continuous exploration and production activities, and strategic investments in pipeline infrastructure. While precise figures are commercially sensitive, the market is poised for continued expansion, fueled by the growing demand for natural gas, particularly within the power generation sector. This aligns with Malaysia's broader strategy to diversify its energy mix and lessen reliance on traditional fossil fuels. However, several factors, such as fluctuating global energy prices, stringent environmental standards, and a growing emphasis on renewable energy sources, present both opportunities and challenges for the industry's future growth trajectory.

Technological advancements, including the implementation of smart pipeline technologies, enhanced pipeline integrity management systems, and the use of advanced materials, are pivotal in enhancing efficiency, bolstering operational safety, and optimizing overall performance. These improvements are critical for ensuring the long-term viability and sustainability of the sector.

Dominant Regions, Countries, or Segments in Malaysia Oil & Gas Pipeline Industry

The offshore segment currently dominates the Malaysian oil and gas pipeline market, accounting for approximately xx% of the total market value in 2024, driven primarily by significant offshore oil and gas reserves and ongoing exploration and production activities. Gas pipelines represent a larger share of the market than crude oil pipelines owing to increased gas production and consumption.

Key Drivers of Offshore Segment Dominance:

- Significant offshore oil and gas reserves.

- Government incentives and support for offshore exploration and production.

- Technological advancements in subsea pipeline construction and maintenance.

Onshore Segment: While smaller, the onshore segment is experiencing steady growth, driven by increasing demand for natural gas in industrial and power generation sectors. Growth is constrained by limited available land and the associated environmental regulatory challenges.

Malaysia Oil & Gas Pipeline Industry Product Landscape

The product landscape within the Malaysian oil and gas pipeline industry encompasses a wide range of pipeline components and technologies, including diverse pipe materials (steel, high-density polyethylene (HDPE), and specialized coatings designed for superior corrosion protection. Advanced pipeline monitoring and control systems are integral to modern operations. The integration of smart pipeline technologies with embedded sensors enables real-time monitoring of critical parameters (pressure, temperature, and flow rates), allowing for predictive maintenance and prompt mitigation of potential issues. This technological shift towards enhanced monitoring and control systems contributes to improved operational efficiency, safety, and reduced maintenance costs.

Key Drivers, Barriers & Challenges in Malaysia Oil & Gas Pipeline Industry

Key Drivers:

- Sustained growth in domestic energy demand, particularly for natural gas.

- Government support and policy initiatives that encourage the development of the energy sector.

- Technological advancements enabling enhanced pipeline safety, efficiency, and environmental performance.

- Strategic infrastructure development to support economic growth and energy security.

Key Challenges:

- Significant capital expenditures required for new pipeline projects and infrastructure upgrades.

- Stringent environmental regulations and permitting processes, requiring careful environmental impact assessments.

- Volatility in global oil and gas prices impacting project profitability and investment decisions.

- Potential supply chain disruptions and their impact on project timelines and costs. Mitigation strategies are crucial.

- Competition from alternative energy sources and transportation modes.

Emerging Opportunities in Malaysia Oil & Gas Pipeline Industry

- Expansion of natural gas pipeline networks to meet growing demand and support energy diversification strategies.

- Widespread adoption of smart pipeline technologies to enhance operational efficiency, safety, and environmental stewardship.

- Growth in complex offshore pipeline projects in deeper waters requiring advanced engineering and technological solutions.

- Potential for cross-border pipeline projects to facilitate regional energy cooperation and trade.

- Development of innovative solutions for pipeline integrity management and leak detection.

- Investment in skilled workforce development to support technological advancements and operational excellence.

Growth Accelerators in the Malaysia Oil & Gas Pipeline Industry

Technological advancements in materials science and pipeline management systems, coupled with strategic government initiatives and growing energy demand, are crucial growth catalysts. Strong partnerships between international and local companies are fostering technological transfer and enhancing local expertise. Furthermore, diversification of energy sources and the increasing focus on sustainable practices are likely to generate opportunities in areas such as carbon capture and storage pipeline projects.

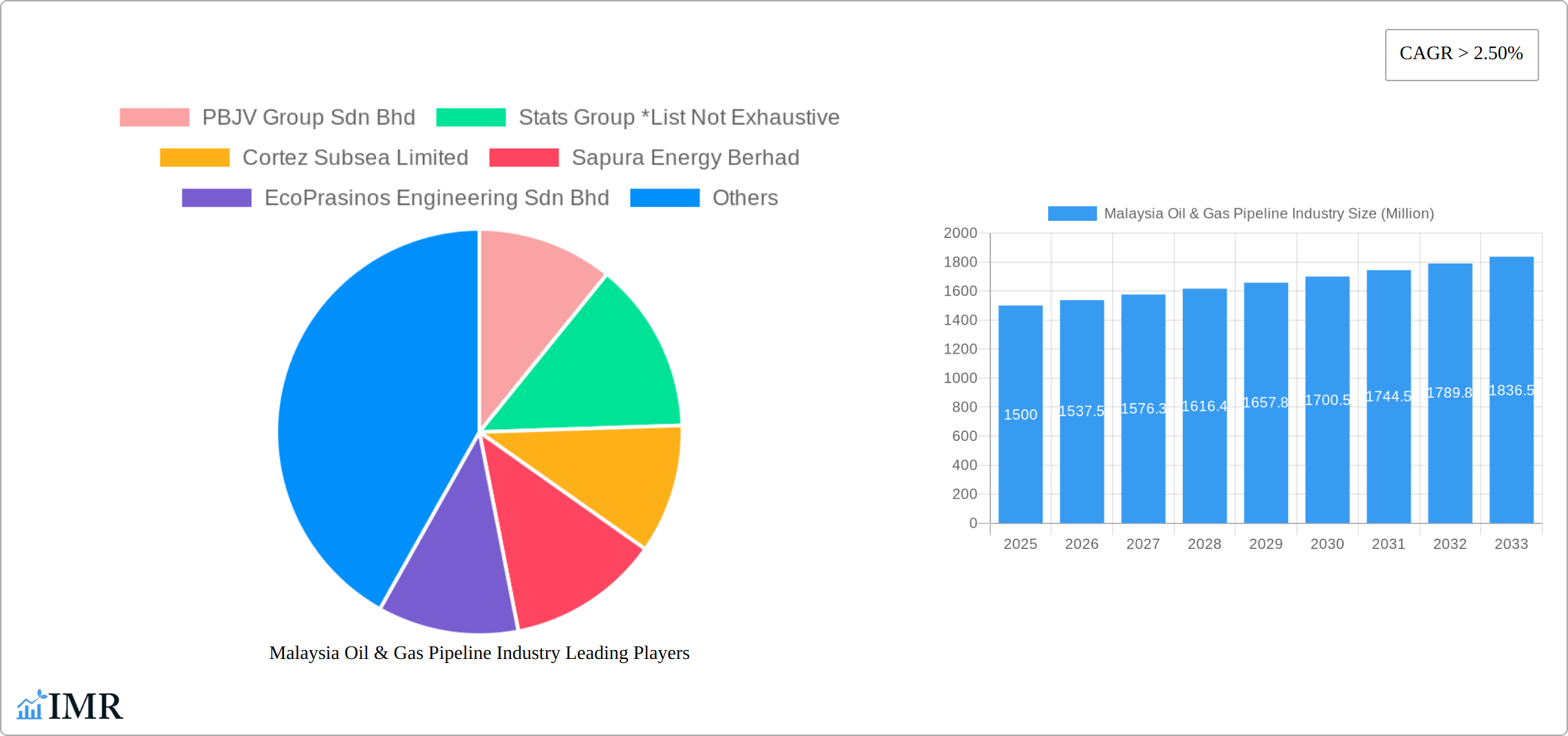

Key Players Shaping the Malaysia Oil & Gas Pipeline Industry Market

- PBJV Group Sdn Bhd

- Stats Group

- Cortez Subsea Limited

- Sapura Energy Berhad

- EcoPrasinos Engineering Sdn Bhd

- Petroliam Nasional Berhad (PETRONAS)

- Yokogawa Kontrol (Malaysia) Sdn Bhd

- Punj Lloyd Limited

- JFE Engineering Corporation

Notable Milestones in Malaysia Oil & Gas Pipeline Industry Sector

- March 2022: Mubadala Petroleum commences natural gas production from the Pegaga offshore field, utilizing a new 4-kilometer subsea pipeline. This signifies significant investment in offshore infrastructure.

- July 2020: Vestigo Petroleum completes a 68-km subsea pipelay for the Tembikai natural gas development, showcasing expertise in complex offshore pipeline projects.

- June 2020: Sapura Energy secures a USD 180 Million contract for pipeline replacement, highlighting ongoing maintenance and upgrade activities within the industry.

In-Depth Malaysia Oil & Gas Pipeline Industry Market Outlook

The Malaysian oil and gas pipeline industry is poised for continued growth over the next decade, driven by several factors. The increasing domestic energy demand, the development of new oil and gas fields, and the expansion of existing infrastructure are key growth drivers. Strategic partnerships between international and local companies, coupled with ongoing technological advancements and favourable government policies, are further strengthening the outlook. However, the long-term outlook is subject to fluctuations in global energy prices and the pace of adoption of renewable energy sources. The market holds significant potential for companies that can effectively navigate these challenges and capitalize on emerging opportunities, particularly within offshore development and the adoption of smart pipeline technologies.

Malaysia Oil & Gas Pipeline Industry Segmentation

-

1. Location of Deployment

- 1.1. Onshore

- 1.2. Offshore

-

2. Type

- 2.1. Crude Oil Pipeline

- 2.2. Gas Pipeline

Malaysia Oil & Gas Pipeline Industry Segmentation By Geography

- 1. Malaysia

Malaysia Oil & Gas Pipeline Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 2.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities

- 3.3. Market Restrains

- 3.3.1. 4.; Increasing Adoption of Clean Power Sources

- 3.4. Market Trends

- 3.4.1. Natural Gas Pipeline Segment is Expected to Witness Significant Development

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Malaysia Oil & Gas Pipeline Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Crude Oil Pipeline

- 5.2.2. Gas Pipeline

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Malaysia

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 PBJV Group Sdn Bhd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Stats Group *List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Cortez Subsea Limited

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Sapura Energy Berhad

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 EcoPrasinos Engineering Sdn Bhd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Petroliam Nasional Berhad (PETRONAS)

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Yokogawa Kontrol (Malaysia) Sdn Bhd

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Punj Lloyd Limited

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 JFE Engineering Corporation

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.1 PBJV Group Sdn Bhd

List of Figures

- Figure 1: Malaysia Oil & Gas Pipeline Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Malaysia Oil & Gas Pipeline Industry Share (%) by Company 2024

List of Tables

- Table 1: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 3: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 7: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 8: Malaysia Oil & Gas Pipeline Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Malaysia Oil & Gas Pipeline Industry?

The projected CAGR is approximately > 2.50%.

2. Which companies are prominent players in the Malaysia Oil & Gas Pipeline Industry?

Key companies in the market include PBJV Group Sdn Bhd, Stats Group *List Not Exhaustive, Cortez Subsea Limited, Sapura Energy Berhad, EcoPrasinos Engineering Sdn Bhd, Petroliam Nasional Berhad (PETRONAS), Yokogawa Kontrol (Malaysia) Sdn Bhd, Punj Lloyd Limited, JFE Engineering Corporation.

3. What are the main segments of the Malaysia Oil & Gas Pipeline Industry?

The market segments include Location of Deployment, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities.

6. What are the notable trends driving market growth?

Natural Gas Pipeline Segment is Expected to Witness Significant Development.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Clean Power Sources.

8. Can you provide examples of recent developments in the market?

In March 2022, the Abu Dhabi-based Mubadala Petroleum began producing natural gas from the Pegaga offshore field in Malaysia. It has the capacity to produce about 550 million standard cubic feet of gas per day in addition to the condensate. Gas produced will be directed through a new 4-kilometer, 38-inch subsea pipeline tying into an existing offshore gas network and subsequently to the onshore Petronas LNG Complex in Bintulu.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Malaysia Oil & Gas Pipeline Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Malaysia Oil & Gas Pipeline Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Malaysia Oil & Gas Pipeline Industry?

To stay informed about further developments, trends, and reports in the Malaysia Oil & Gas Pipeline Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence