Key Insights

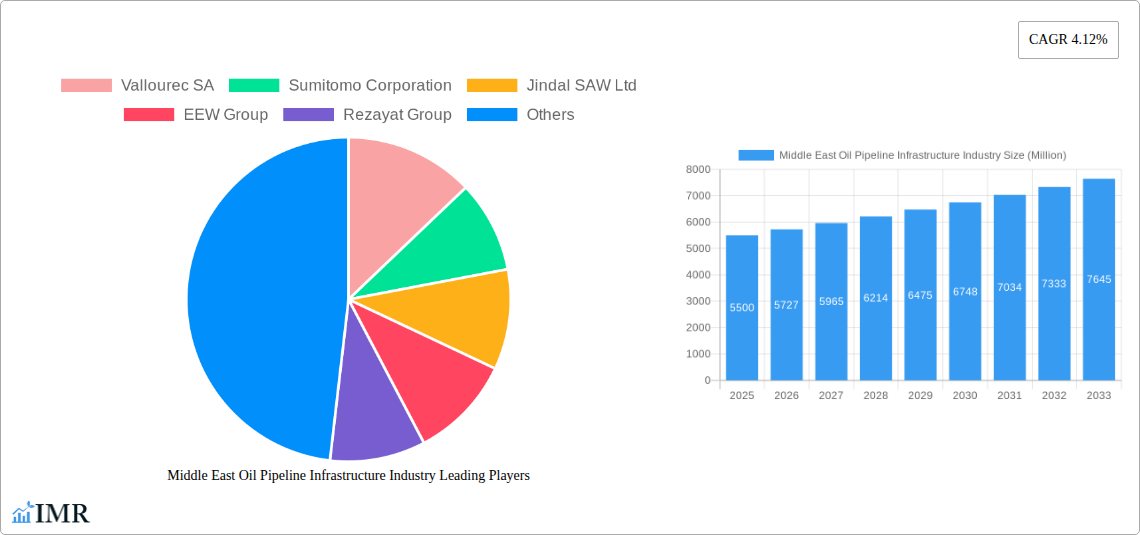

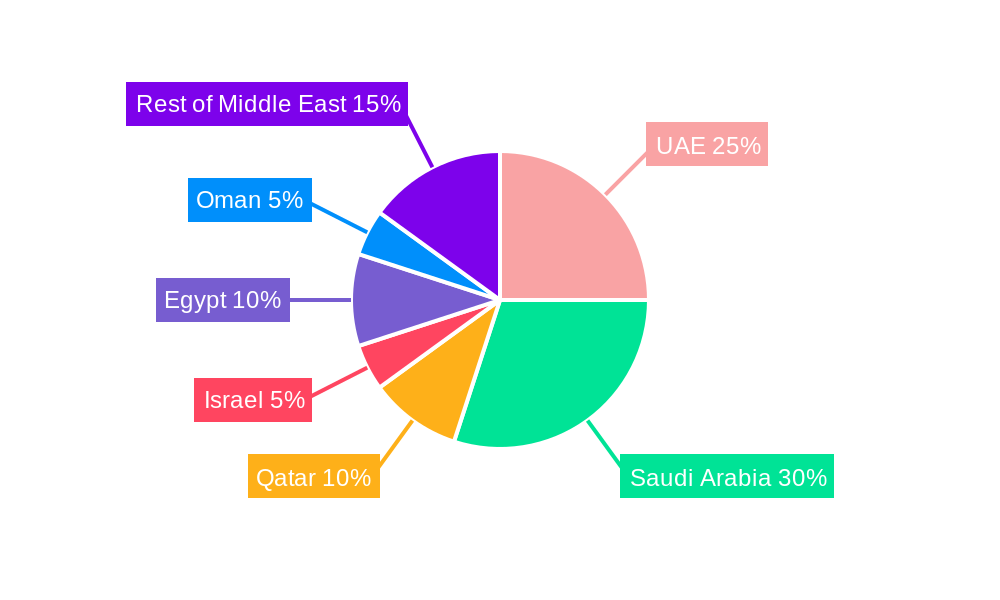

The Middle East Oil Pipeline Infrastructure market, valued at $5.5 billion in 2025, is projected to experience robust growth, driven by increasing oil production and rising energy demand within the region and globally. A Compound Annual Growth Rate (CAGR) of 4.12% from 2025 to 2033 indicates a significant expansion of the market. Key drivers include substantial investments in new pipeline projects to enhance oil transportation efficiency and reliability, coupled with ongoing efforts to modernize existing infrastructure. The growing focus on energy security and diversification within the region further fuels market expansion. The market is segmented by pipe type, primarily encompassing seamless and welded pipes, each catering to specific pipeline requirements. Major players such as Vallourec SA, Sumitomo Corporation, Jindal SAW Ltd, EEW Group, Rezayat Group, Arabian Pipes Company, and ArcelorMittal SA are shaping the competitive landscape through technological advancements, strategic partnerships, and regional expansion initiatives. The UAE, Saudi Arabia, and Qatar represent significant markets within the Middle East, owing to their substantial oil reserves and production capacity.

However, challenges persist. Geopolitical instability in certain parts of the region can disrupt project timelines and investments. Furthermore, fluctuating oil prices pose a risk to long-term market predictability. Stringent environmental regulations and a growing emphasis on sustainability are also influencing the adoption of advanced pipeline technologies and materials, potentially impacting the overall market dynamics. Despite these constraints, the long-term outlook for the Middle East Oil Pipeline Infrastructure market remains positive, underpinned by sustained demand for oil and continued infrastructure development initiatives throughout the region. Growth is expected to be driven by increased cross-border pipeline projects and the expansion of existing networks to support increasing production and export capacities.

Middle East Oil Pipeline Infrastructure Industry: Market Report 2019-2033

This comprehensive report provides a detailed analysis of the Middle East oil pipeline infrastructure industry, encompassing market dynamics, growth trends, key players, and future outlook. With a focus on the parent market (Oil & Gas Infrastructure) and child market (Pipeline Infrastructure), this report is essential for industry professionals, investors, and strategic decision-makers seeking actionable insights. The study period covers 2019-2033, with 2025 as the base and estimated year.

Middle East Oil Pipeline Infrastructure Industry Market Dynamics & Structure

The Middle East oil pipeline infrastructure market is characterized by a moderate level of concentration, with a few major players dominating alongside numerous regional operators. Technological innovation, primarily driven by the need for enhanced efficiency, safety, and environmental sustainability, is a key driver. Stringent regulatory frameworks governing pipeline construction, operation, and maintenance significantly influence market dynamics. Competitive substitutes, such as alternative energy transportation methods, pose a growing challenge. End-user demographics are primarily dictated by the oil and gas producing and consuming nations within the region. Mergers and acquisitions (M&A) activity has been relatively modest in recent years, but is expected to increase with ongoing industry consolidation.

- Market Concentration: xx% controlled by top 5 players (2024).

- Technological Innovation: Focus on smart pipelines, advanced materials, and predictive maintenance.

- Regulatory Framework: Stringent safety and environmental standards influence investment decisions.

- Competitive Substitutes: Growing adoption of LNG and other energy sources poses a threat.

- M&A Activity: xx deals valued at USD xx million in 2019-2024.

- Innovation Barriers: High capital expenditure requirements and lengthy approval processes.

Middle East Oil Pipeline Infrastructure Industry Growth Trends & Insights

The Middle East oil pipeline infrastructure market has experienced steady growth over the historical period (2019-2024), driven by increased oil and gas production and the need to upgrade aging infrastructure. The market is projected to exhibit a CAGR of xx% during the forecast period (2025-2033), propelled by significant investments in new pipeline projects and ongoing capacity expansion. Technological advancements, such as the adoption of smart pipeline technologies, are further enhancing efficiency and reducing operational costs. Shifting consumer behavior towards increased energy consumption in the region will continue to drive demand for reliable pipeline networks.

- Market Size: USD xx million in 2024, projected to reach USD xx million by 2033.

- CAGR (2025-2033): xx%

- Market Penetration: xx% in 2024.

- Key Growth Drivers: Increased oil and gas production, infrastructure upgrades, and technological advancements.

Dominant Regions, Countries, or Segments in Middle East Oil Pipeline Infrastructure Industry

The Saudi Arabia and the UAE are currently the dominant regions in the Middle East oil pipeline infrastructure market due to their significant oil and gas reserves and extensive pipeline networks. The high concentration of oil and gas production facilities in these regions directly translates into greater demand for pipeline infrastructure. Within pipeline types, welded pipes currently hold the largest market share due to cost-effectiveness and suitability for large-diameter pipelines. However, seamless pipes are expected to witness significant growth, driven by their superior pressure resistance and longevity.

- Key Drivers in Saudi Arabia and UAE: Significant oil and gas reserves, major pipeline projects, and government investment.

- Welded Pipes: Cost-effective solution suitable for large-diameter pipelines.

- Seamless Pipes: Higher pressure resistance and longevity for critical applications.

- Market Share (2024): Welded pipes: xx%, Seamless pipes: xx%.

- Growth Potential: Seamless pipes are projected to exhibit faster growth than welded pipes.

Middle East Oil Pipeline Infrastructure Industry Product Landscape

The Middle East oil pipeline infrastructure market features a diverse range of products, including welded and seamless pipes made from various materials such as carbon steel, stainless steel, and high-strength alloys. Innovations focus on enhancing pipeline lifespan, corrosion resistance, and leak detection capabilities. The adoption of smart pipeline technologies, incorporating sensors and data analytics, is revolutionizing pipeline management, improving safety, and optimizing operational efficiency. Unique selling propositions focus on enhanced durability, reduced maintenance costs, and improved environmental performance.

Key Drivers, Barriers & Challenges in Middle East Oil Pipeline Infrastructure Industry

Key Drivers:

- Increased oil and gas production and export demand.

- Government initiatives to modernize infrastructure.

- Investments in new pipeline projects and capacity expansions.

Challenges & Restraints:

- High initial investment costs for pipeline construction and maintenance.

- Geopolitical risks and security concerns along pipeline routes.

- Environmental regulations and sustainability concerns.

- Supply chain disruptions, impacting material availability and project timelines.

Emerging Opportunities in Middle East Oil Pipeline Infrastructure Industry

- Expanding pipeline networks to new oil and gas fields.

- Adoption of smart pipeline technologies and digitalization initiatives.

- Increased focus on pipeline integrity management and leak detection.

- Development of sustainable and environmentally friendly pipeline solutions.

Growth Accelerators in the Middle East Oil Pipeline Infrastructure Industry

Technological innovation, specifically in smart pipeline technologies and advanced materials, presents significant growth opportunities. Strategic partnerships between pipeline operators and technology providers are enhancing efficiency and safety. Expansion into new oil and gas fields and the development of regional pipeline networks will create substantial growth opportunities in the coming decade.

Key Players Shaping the Middle East Oil Pipeline Infrastructure Industry Market

- Vallourec SA

- Sumitomo Corporation

- Jindal SAW Ltd

- EEW Group

- Rezayat Group

- Arabian Pipes Company

- ArcelorMittal SA

- *List Not Exhaustive

Notable Milestones in Middle East Oil Pipeline Infrastructure Industry Sector

- August 2022: Kazakhstan plans to utilize Azerbaijan's pipeline network for crude oil export, diversifying its routes.

- March 2023: Gas Arabian Services Company secures a USD 13.58 million EPC contract for a gas pipeline project in Saudi Arabia.

In-Depth Middle East Oil Pipeline Infrastructure Industry Market Outlook

The Middle East oil pipeline infrastructure market is poised for significant growth in the coming years, driven by continued investment in new projects, technological advancements, and increasing oil and gas production. Strategic partnerships, focusing on technological integration and infrastructure development, will be crucial for maximizing long-term market potential. The region’s commitment to infrastructure development, coupled with technological innovation, positions the market for sustained expansion.

Middle East Oil Pipeline Infrastructure Industry Segmentation

-

1. Type

- 1.1. Seamless

- 1.2. Welded

-

2. Geography

- 2.1. United Arab Emirates

- 2.2. Saudi Arabia

- 2.3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry Segmentation By Geography

- 1. United Arab Emirates

- 2. Saudi Arabia

- 3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.12% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Proven Shale Gas Reserves 4.; Technological Advancement in Horizontal Drilling and Hydraulic Fracturing

- 3.3. Market Restrains

- 3.3.1. 4.; High Exploration Cost

- 3.4. Market Trends

- 3.4.1. Seamless Type Segment to Witness a Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Seamless

- 5.1.2. Welded

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United Arab Emirates

- 5.2.2. Saudi Arabia

- 5.2.3. Rest of Middle East

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Rest of Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Seamless

- 6.1.2. Welded

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United Arab Emirates

- 6.2.2. Saudi Arabia

- 6.2.3. Rest of Middle East

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Seamless

- 7.1.2. Welded

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United Arab Emirates

- 7.2.2. Saudi Arabia

- 7.2.3. Rest of Middle East

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Seamless

- 8.1.2. Welded

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United Arab Emirates

- 8.2.2. Saudi Arabia

- 8.2.3. Rest of Middle East

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 10. Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 11. Qatar Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 12. Israel Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 13. Egypt Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 14. Oman Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 15. Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Vallourec SA

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Sumitomo Corporation

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Jindal SAW Ltd

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 EEW Group

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Rezayat Group

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Arabian Pipes Company

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 ArcelorMittal SA*List Not Exhaustive

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.1 Vallourec SA

List of Figures

- Figure 1: Middle East Oil Pipeline Infrastructure Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Middle East Oil Pipeline Infrastructure Industry Share (%) by Company 2024

List of Tables

- Table 1: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 4: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Qatar Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Israel Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Egypt Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Oman Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 15: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 17: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 20: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 21: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Oil Pipeline Infrastructure Industry?

The projected CAGR is approximately 4.12%.

2. Which companies are prominent players in the Middle East Oil Pipeline Infrastructure Industry?

Key companies in the market include Vallourec SA, Sumitomo Corporation, Jindal SAW Ltd, EEW Group, Rezayat Group, Arabian Pipes Company, ArcelorMittal SA*List Not Exhaustive.

3. What are the main segments of the Middle East Oil Pipeline Infrastructure Industry?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.50 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Proven Shale Gas Reserves 4.; Technological Advancement in Horizontal Drilling and Hydraulic Fracturing.

6. What are the notable trends driving market growth?

Seamless Type Segment to Witness a Significant Growth.

7. Are there any restraints impacting market growth?

4.; High Exploration Cost.

8. Can you provide examples of recent developments in the market?

August 2022: Kazakhstan is expected to sell its crude oil through Azerbaijan's main oil pipeline, as the country seeks alternatives to a route threatened by Russia. Another 3.5 million metric tons of Kazakh crude per year could begin flowing through another Azeri pipeline to Georgia's Black Sea port of Supsa in 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Oil Pipeline Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Oil Pipeline Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Oil Pipeline Infrastructure Industry?

To stay informed about further developments, trends, and reports in the Middle East Oil Pipeline Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence