Key Insights

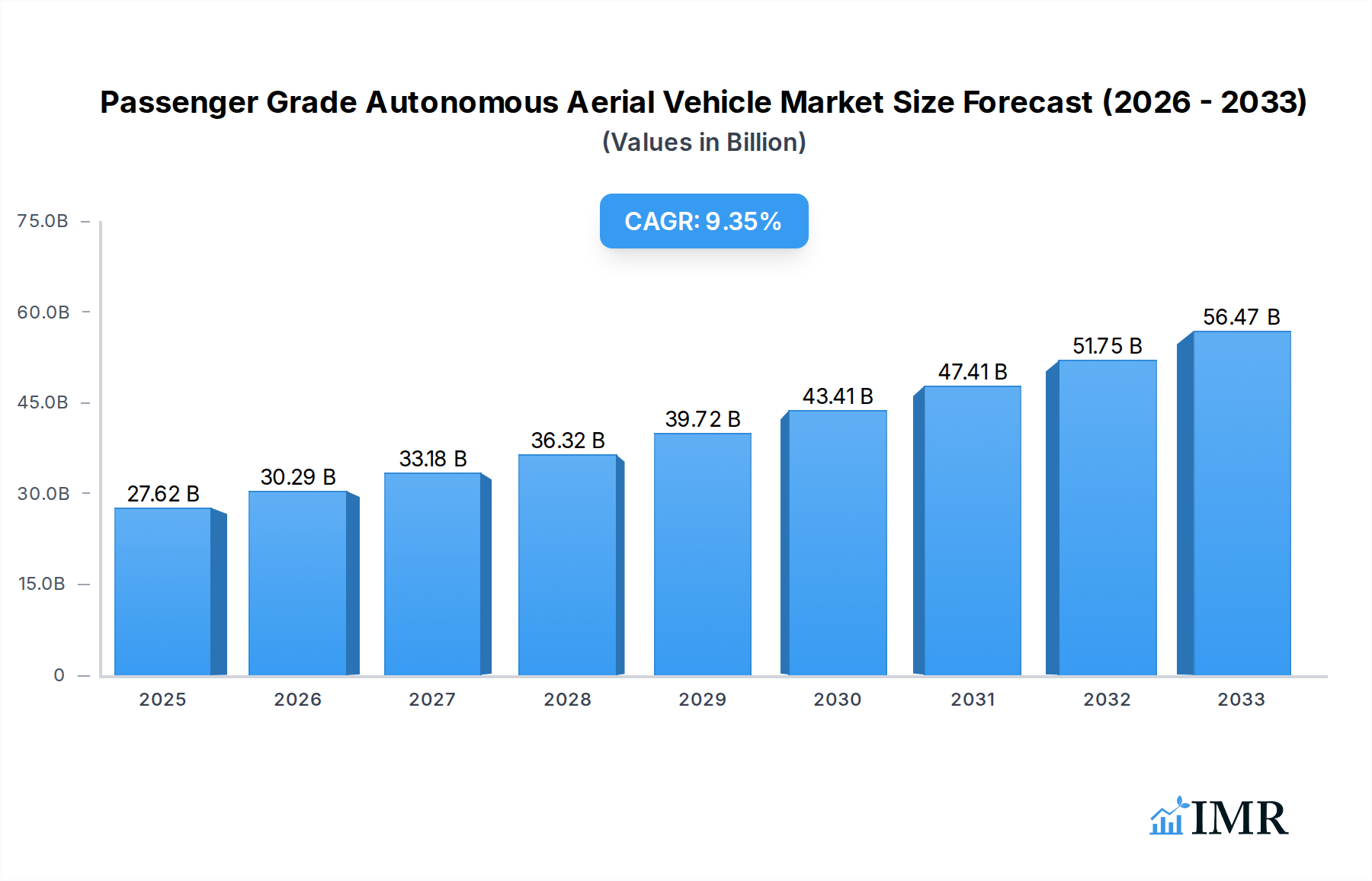

The Passenger Grade Autonomous Aerial Vehicle market is poised for substantial expansion, projected to reach $27.62 billion in 2025, driven by an impressive 9.7% CAGR. This burgeoning sector is rapidly transforming urban and intercity mobility, offering a glimpse into the future of transportation. Key drivers fueling this growth include the escalating need for efficient and sustainable urban air mobility solutions, aimed at alleviating traffic congestion and reducing commute times in densely populated areas. Advancements in autonomous flight technology, coupled with increasing regulatory support and a growing appetite for novel transportation experiences, are further accelerating market adoption. The market segmentation highlights a strong focus on diverse applications, ranging from efficient intercity travel to seamless intracity commuting, catering to both single and multi-passenger needs. Innovations in electric Vertical Take-Off and Landing (eVTOL) aircraft are central to this evolution, promising quieter, cleaner, and more accessible aerial transit.

Passenger Grade Autonomous Aerial Vehicle Market Size (In Billion)

The competitive landscape is dynamic, featuring a blend of established aerospace giants like Airbus and Boeing, alongside innovative startups such as Ehang, Volocopter, and Joby Aviation. These companies are heavily investing in research and development, pushing the boundaries of what's possible in autonomous flight. Emerging trends include the development of advanced battery technologies for longer flight ranges, sophisticated AI for enhanced navigation and safety, and the integration of these aerial vehicles into existing transportation networks. While the market exhibits immense potential, certain restraints, such as the significant capital investment required for infrastructure development (vertiports, charging stations) and the ongoing need for robust regulatory frameworks and public acceptance, will need to be addressed. Nevertheless, the overarching trajectory indicates a significant shift towards autonomous aerial vehicles as a mainstream mode of passenger transport, promising a more connected and efficient future.

Passenger Grade Autonomous Aerial Vehicle Company Market Share

Here is a compelling, SEO-optimized report description for Passenger Grade Autonomous Aerial Vehicle, designed for maximum search engine visibility and industry professional engagement.

Report Title: Passenger Grade Autonomous Aerial Vehicle Market: Size, Share, Trends, Growth, and Forecast (2024-2033) - Intercity, Intracity, Single, Double, Multi-Seat AAVs, and Key Player Analysis

Report Description:

This comprehensive report provides an in-depth analysis of the global Passenger Grade Autonomous Aerial Vehicle (AAV) market, a rapidly evolving sector poised to revolutionize urban and intercity transportation. Explore market dynamics, growth trends, dominant regions, and the competitive landscape from 2019 to 2033, with a base year of 2025 and an estimated forecast period of 2025–2033. Discover the significant impact of technological innovation, stringent regulatory frameworks, and strategic partnerships on the AAV industry.

This report meticulously examines the Passenger Grade Autonomous Aerial Vehicle market across diverse applications including Intercity AAVs and Intracity AAVs. It delves into various vehicle types, categorizing them into Single Seat AAVs, Double Seats AAVs, and Multi-seats AAVs. We provide granular insights into the market size evolution, adoption rates, and consumer behavior shifts, projecting a robust CAGR. Understand the drivers and challenges shaping the future of flying cars, eVTOL (electric Vertical Take-Off and Landing) aircraft, and air taxis.

The report offers a detailed exploration of the parent market and child market dynamics within the Autonomous Aerial Vehicle sector. Uncover insights into market concentration, M&A trends, and the strategic moves of industry leaders such as Airbus, Ehang, Vertical Aerospace, Boeing, Volocopter, Lilium, Joby Aviation, AeroMobil, Kitty Hawk, Urban Aeronautics, Bell Textron, Aston Martin, Samson Sky, and AeroMobil. Witness the latest industry developments and notable milestones that are accelerating the adoption of passenger drones and electric aircraft. This analysis is crucial for stakeholders seeking to capitalize on the multi-billion dollar potential of the eVTOL market and the broader urban air mobility (UAM) ecosystem.

Passenger Grade Autonomous Aerial Vehicle Market Dynamics & Structure

The Passenger Grade Autonomous Aerial Vehicle market is characterized by a dynamic interplay of rapid technological innovation, evolving regulatory landscapes, and increasing investor interest. Market concentration is currently moderate, with a few key players like Joby Aviation, Volocopter, and Ehang leading in development and testing, while a broader ecosystem of startups and established aerospace giants are actively engaged. Technological innovation is primarily driven by advancements in battery technology for extended range, sophisticated AI for autonomous navigation, lightweight composite materials for improved efficiency, and advanced sensor suites for enhanced safety. Regulatory frameworks are still under development globally, with bodies like the FAA and EASA working to establish certification standards, flight corridors, and operational protocols, which currently act as a significant innovation barrier but are crucial for widespread adoption. Competitive product substitutes are minimal in the direct AAV passenger transport segment, but indirectly, high-speed rail, traditional aviation, and improved ground-based public transport pose challenges. End-user demographics are gradually shifting from early adopters and tech enthusiasts to a broader consumer base as AAVs become more accessible and perceived as a viable transportation solution. Mergers and acquisitions (M&A) trends are on the rise as larger aerospace companies invest in or acquire promising AAV startups to secure market positions and technological expertise. For instance, significant investments have been observed in companies like Lilium and Vertical Aerospace.

- Market Concentration: Moderate, with key players like Joby Aviation and Volocopter in advanced stages of development.

- Technological Innovation Drivers: Battery density, AI autonomy, advanced materials, and sensor fusion.

- Regulatory Frameworks: Developing, with critical impact on certification and air traffic management.

- Competitive Product Substitutes: Indirectly from high-speed rail and enhanced ground transport.

- End-User Demographics: Transitioning from early adopters to a wider consumer base.

- M&A Trends: Increasing, with strategic investments and acquisitions by major aerospace firms.

Passenger Grade Autonomous Aerial Vehicle Growth Trends & Insights

The global Passenger Grade Autonomous Aerial Vehicle market is poised for exponential growth, driven by increasing demand for efficient, sustainable, and decongested transportation solutions. The market size evolution is projected to be significant, moving from a nascent stage in the historical period (2019–2024) to a multi-billion dollar valuation by the end of the forecast period (2033). Adoption rates are expected to accelerate as regulatory approvals become widespread and public trust in autonomous flight systems grows. Technological disruptions, including breakthroughs in electric propulsion, battery energy density, and advanced AI algorithms for sophisticated flight management and collision avoidance, are key to unlocking this potential. Consumer behavior shifts are anticipated, with a growing willingness to embrace air taxi services for their speed and convenience, especially in dense urban environments. The CAGR for this market is projected to be robust, reflecting the transformative nature of AAVs. Market penetration will initially be concentrated in early adopter cities and for specific applications like airport transfers and premium commuter services, gradually expanding to more widespread intercity and intracity routes. The integration of AAVs into existing transportation networks, often referred to as Urban Air Mobility (UAM), will be a critical factor in their success, creating new mobility paradigms and enhancing connectivity. The ongoing development of digital infrastructure, including vertiports and advanced air traffic management systems, is crucial for scaling operations and ensuring seamless integration. Furthermore, the increasing focus on sustainability and reduced carbon emissions makes electric AAVs a highly attractive alternative to traditional modes of transport, aligning with global environmental goals. The financial commitment from venture capital and established aerospace firms underscores the strong belief in the long-term viability and profitability of this market. The transition from research and development to commercial operations is a key phase, marked by increasing prototype testing, certification processes, and the establishment of operational frameworks.

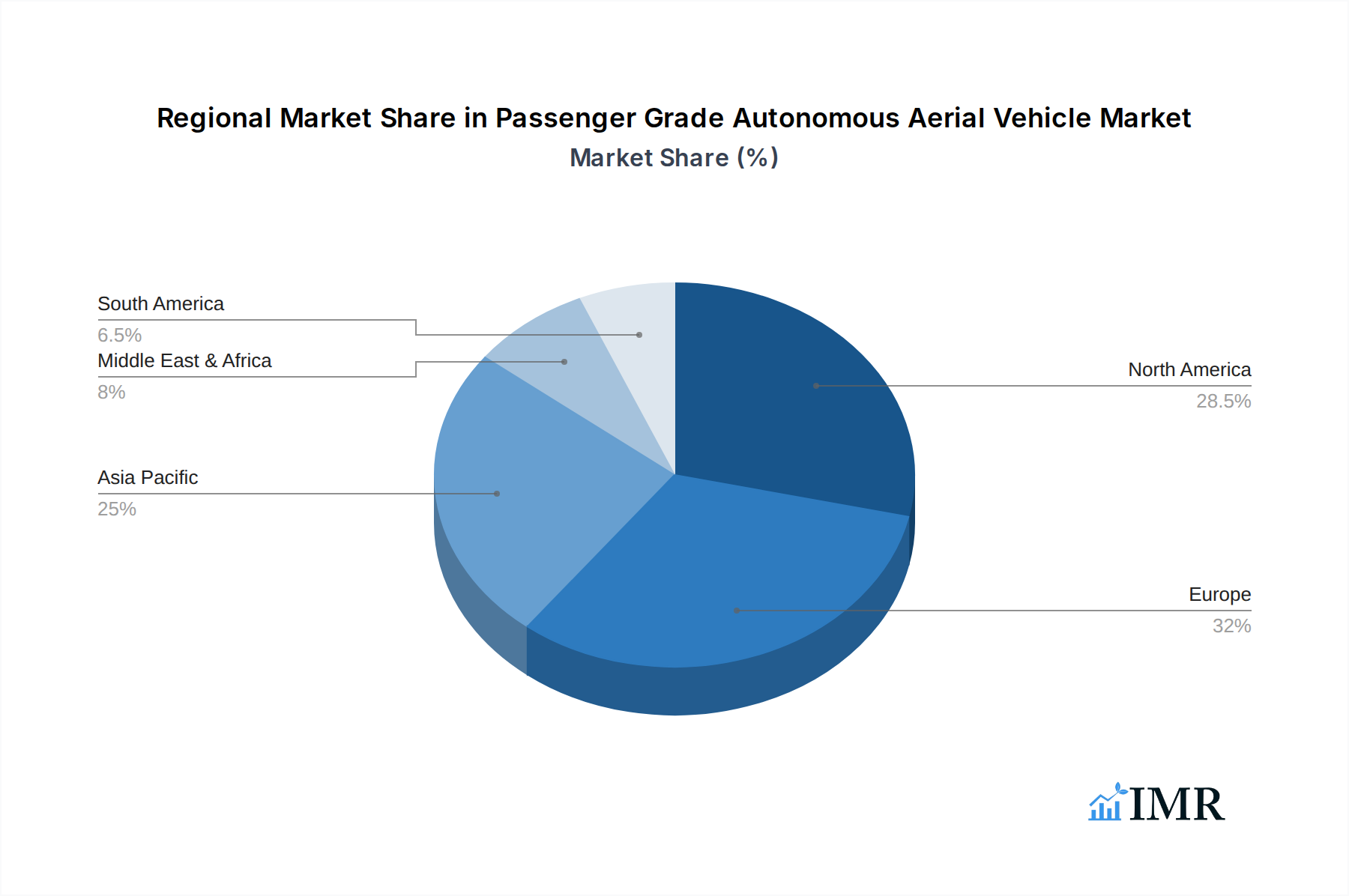

Dominant Regions, Countries, or Segments in Passenger Grade Autonomous Aerial Vehicle

The Intracity AAV segment is emerging as the dominant force in the Passenger Grade Autonomous Aerial Vehicle market, primarily driven by the pressing need to alleviate urban congestion and provide rapid transit solutions. This dominance is especially pronounced in densely populated metropolitan areas across North America and Europe. Key drivers for this segment's growth include significant economic policies supporting innovative transportation, coupled with substantial investments in the development of vertiport infrastructure – designated landing and takeoff sites for AAVs. For instance, cities like Los Angeles, New York, London, and Paris are actively exploring and piloting intracity AAV services. The Double Seats AAVs and Multi-seats AAVs types are expected to witness higher market share and growth potential within the intracity application, catering to commuter demand and ride-sharing models. Their ability to carry multiple passengers offers greater economic viability and scalability for operators.

North America, particularly the United States, is a leading region due to its advanced technological ecosystem, proactive regulatory engagement from the FAA, and substantial private sector funding. Countries like Germany and the UK are also showing strong leadership in Europe, with government initiatives and a robust aerospace industry pushing the boundaries of AAV development and deployment. The market share within these dominant regions is steadily increasing, with projections indicating a substantial portion of the global AAV market will be accounted for by these areas in the coming years. Economic policies favoring the adoption of electric and autonomous technologies, alongside significant public and private investment in research and development, are critical factors contributing to this dominance. The accessibility of funding for startups and established players alike allows for accelerated development cycles and the rapid testing of new AAV models. Furthermore, the increasing public awareness and acceptance of AAVs as a safe and efficient mode of transport are critical enablers. The development of comprehensive air traffic management systems tailored for AAVs is also a key focus in these regions, ensuring safe and efficient operation within complex urban airspace. The growth potential within these leading segments and regions is immense, fueled by ongoing technological advancements and a clear market demand for faster, more sustainable urban mobility solutions.

Passenger Grade Autonomous Aerial Vehicle Product Landscape

The product landscape of Passenger Grade Autonomous Aerial Vehicles is characterized by rapid innovation and a focus on safety, efficiency, and passenger comfort. Companies like Joby Aviation are developing sleek, battery-electric aircraft designed for multiple passengers, boasting quiet operation and low emissions. Ehang has pioneered fully autonomous passenger drones, emphasizing simplified operation and accessibility. Vertical Aerospace is producing modular eVTOLs, aiming for cost-effectiveness and scalability. Lilium's innovative ducted fan technology promises high speeds for intercity travel. These vehicles often feature advanced avionics, intuitive interfaces for potential pilot oversight or full autonomy, and ergonomic cabin designs to enhance the passenger experience. Key performance metrics include flight range, payload capacity, energy efficiency, noise reduction, and certification status. Unique selling propositions often revolve around reduced travel times, lower environmental impact compared to traditional transport, and the novelty of aerial travel.

Key Drivers, Barriers & Challenges in Passenger Grade Autonomous Aerial Vehicle

Key Drivers:

- Urban Congestion: Escalating traffic congestion in major cities globally is creating a strong demand for alternative, faster transportation methods.

- Technological Advancements: Breakthroughs in battery technology, AI, lightweight materials, and propulsion systems are making AAVs increasingly viable.

- Sustainability Mandates: The growing focus on reducing carbon emissions and noise pollution favors electric and more efficient aerial transport.

- Government Support & Investment: Increasing regulatory clarity and financial incentives from governments worldwide are accelerating development and adoption.

- Demand for Enhanced Connectivity: The need for rapid point-to-point travel for both passengers and cargo drives innovation in this sector.

Barriers & Challenges:

- Regulatory Hurdles: Developing comprehensive certification standards, air traffic management systems, and operational guidelines for autonomous flight is a complex and time-consuming process.

- Public Perception & Safety Concerns: Gaining public trust and addressing anxieties surrounding the safety and reliability of autonomous aerial vehicles remains a significant challenge.

- Infrastructure Development: The establishment of a robust network of vertiports, charging stations, and maintenance facilities requires substantial investment and urban planning.

- High Development & Production Costs: The initial investment in research, development, certification, and manufacturing of AAVs is substantial, impacting affordability.

- Battery Technology Limitations: Current battery technology, while improving, can still limit flight range and increase charging times, impacting operational efficiency.

- Supply Chain & Manufacturing Scalability: Building a sustainable and scalable supply chain for specialized components and scaling up production to meet anticipated demand presents logistical challenges.

- Cybersecurity Threats: Protecting autonomous systems from cyberattacks is paramount to ensuring passenger safety and data integrity.

Emerging Opportunities in Passenger Grade Autonomous Aerial Vehicle

Emerging opportunities in the Passenger Grade Autonomous Aerial Vehicle sector are vast and multifaceted. Untapped markets include emergency medical services (EMS) and critical cargo delivery, where the speed and accessibility of AAVs can be life-saving. Innovative applications such as aerial tourism and executive transport are poised for growth, offering premium, time-saving experiences. Evolving consumer preferences are leaning towards on-demand, personalized mobility solutions, which AAVs are ideally positioned to fulfill. The development of specialized AAVs for specific weather conditions and extended range missions presents further avenues for market expansion. Integration with existing transportation hubs and smart city initiatives offers significant potential for seamless mobility networks.

Growth Accelerators in the Passenger Grade Autonomous Aerial Vehicle Industry

Growth in the Passenger Grade Autonomous Aerial Vehicle industry is being significantly accelerated by several key catalysts. Continuous technological breakthroughs, particularly in energy storage, autonomous navigation systems, and advanced materials, are enhancing vehicle performance and safety, making them more commercially viable. Strategic partnerships between aircraft manufacturers, technology providers, and infrastructure developers are crucial for creating integrated ecosystems and streamlining the path to market. Furthermore, global market expansion strategies, including penetration into emerging economies and the establishment of new operational routes, are driving demand and fostering innovation. The increasing interest and investment from venture capital and established aerospace giants underscore the belief in the sector's transformative potential. The ongoing refinement of regulatory frameworks, coupled with successful pilot programs and early commercial deployments, is building confidence and paving the way for wider adoption.

Key Players Shaping the Passenger Grade Autonomous Aerial Vehicle Market

- Airbus

- Ehang

- Vertical Aerospace

- Boeing

- Volocopter

- Lilium

- Joby Aviation

- AeroMobil

- Kitty Hawk

- Urban Aeronautics

- Bell Textron

- Aston Martin

- Samson Sky

Notable Milestones in Passenger Grade Autonomous Aerial Vehicle Sector

- 2019: Kitty Hawk demonstrates its Flyer eVTOL prototype in flight.

- 2020: Ehang receives type certification for its EH216 AAV in China.

- 2021: Joby Aviation completes its first eVTOL flight as a publicly traded company.

- 2021: Volocopter conducts successful public demonstrations of its VoloCity air taxi in several cities.

- 2022: Lilium completes the first flight of its all-electric, vertical take-off and landing jet.

- 2022: Vertical Aerospace achieves its first flight milestone for its VX4 eVTOL prototype.

- 2023: Boeing's Wisk Aero achieves significant progress in autonomous flight testing.

- 2023: Airbus begins rigorous testing of its CityAirbus NextGen eVTOL.

- 2024: AeroMobil unveils its latest flying car model, showcasing advancements in dual-mode transportation.

- 2024: Bell Textron continues extensive testing and development of its autonomous aerial systems.

In-Depth Passenger Grade Autonomous Aerial Vehicle Market Outlook

The Passenger Grade Autonomous Aerial Vehicle market outlook is exceptionally positive, driven by a confluence of accelerating factors that are propelling the industry forward at an unprecedented pace. Continued technological breakthroughs in battery energy density, AI-driven autonomy, and lightweight materials are enhancing vehicle performance, safety, and economic viability, laying the groundwork for widespread commercialization. Strategic partnerships between leading aerospace manufacturers, innovative startups, and infrastructure developers are proving instrumental in creating comprehensive ecosystems and accelerating the deployment of AAVs. The global market expansion, spurred by increasing urban populations and the demand for efficient connectivity, coupled with supportive governmental policies and investments, further bolsters the growth trajectory. As regulatory frameworks mature and successful pilot programs demonstrate the safety and efficacy of AAVs, public acceptance is set to rise, unlocking significant future market potential and offering substantial strategic opportunities for early movers and established players alike.

Passenger Grade Autonomous Aerial Vehicle Segmentation

-

1. Application

- 1.1. Intercity

- 1.2. Intracity

-

2. Types

- 2.1. Single Seat

- 2.2. Double Seats

- 2.3. Multi-seats

Passenger Grade Autonomous Aerial Vehicle Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Passenger Grade Autonomous Aerial Vehicle Regional Market Share

Geographic Coverage of Passenger Grade Autonomous Aerial Vehicle

Passenger Grade Autonomous Aerial Vehicle REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Passenger Grade Autonomous Aerial Vehicle Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Intercity

- 5.1.2. Intracity

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Single Seat

- 5.2.2. Double Seats

- 5.2.3. Multi-seats

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Passenger Grade Autonomous Aerial Vehicle Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Intercity

- 6.1.2. Intracity

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Single Seat

- 6.2.2. Double Seats

- 6.2.3. Multi-seats

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Passenger Grade Autonomous Aerial Vehicle Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Intercity

- 7.1.2. Intracity

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Single Seat

- 7.2.2. Double Seats

- 7.2.3. Multi-seats

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Passenger Grade Autonomous Aerial Vehicle Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Intercity

- 8.1.2. Intracity

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Single Seat

- 8.2.2. Double Seats

- 8.2.3. Multi-seats

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Intercity

- 9.1.2. Intracity

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Single Seat

- 9.2.2. Double Seats

- 9.2.3. Multi-seats

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Passenger Grade Autonomous Aerial Vehicle Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Intercity

- 10.1.2. Intracity

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Single Seat

- 10.2.2. Double Seats

- 10.2.3. Multi-seats

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Airbus

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ehang

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Vertical Aerospace

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Boeing

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Volocopter

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Lilium

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Joby Aviation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AeroMobil

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Kitty Hawk

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 AeroMobil

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Urban Aeronautics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Bell Textron

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Aston Martin

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Samson Sky

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Airbus

List of Figures

- Figure 1: Global Passenger Grade Autonomous Aerial Vehicle Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Passenger Grade Autonomous Aerial Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Passenger Grade Autonomous Aerial Vehicle Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Passenger Grade Autonomous Aerial Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Passenger Grade Autonomous Aerial Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Passenger Grade Autonomous Aerial Vehicle?

The projected CAGR is approximately 9.7%.

2. Which companies are prominent players in the Passenger Grade Autonomous Aerial Vehicle?

Key companies in the market include Airbus, Ehang, Vertical Aerospace, Boeing, Volocopter, Lilium, Joby Aviation, AeroMobil, Kitty Hawk, AeroMobil, Urban Aeronautics, Bell Textron, Aston Martin, Samson Sky.

3. What are the main segments of the Passenger Grade Autonomous Aerial Vehicle?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Passenger Grade Autonomous Aerial Vehicle," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Passenger Grade Autonomous Aerial Vehicle report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Passenger Grade Autonomous Aerial Vehicle?

To stay informed about further developments, trends, and reports in the Passenger Grade Autonomous Aerial Vehicle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence