Key Insights

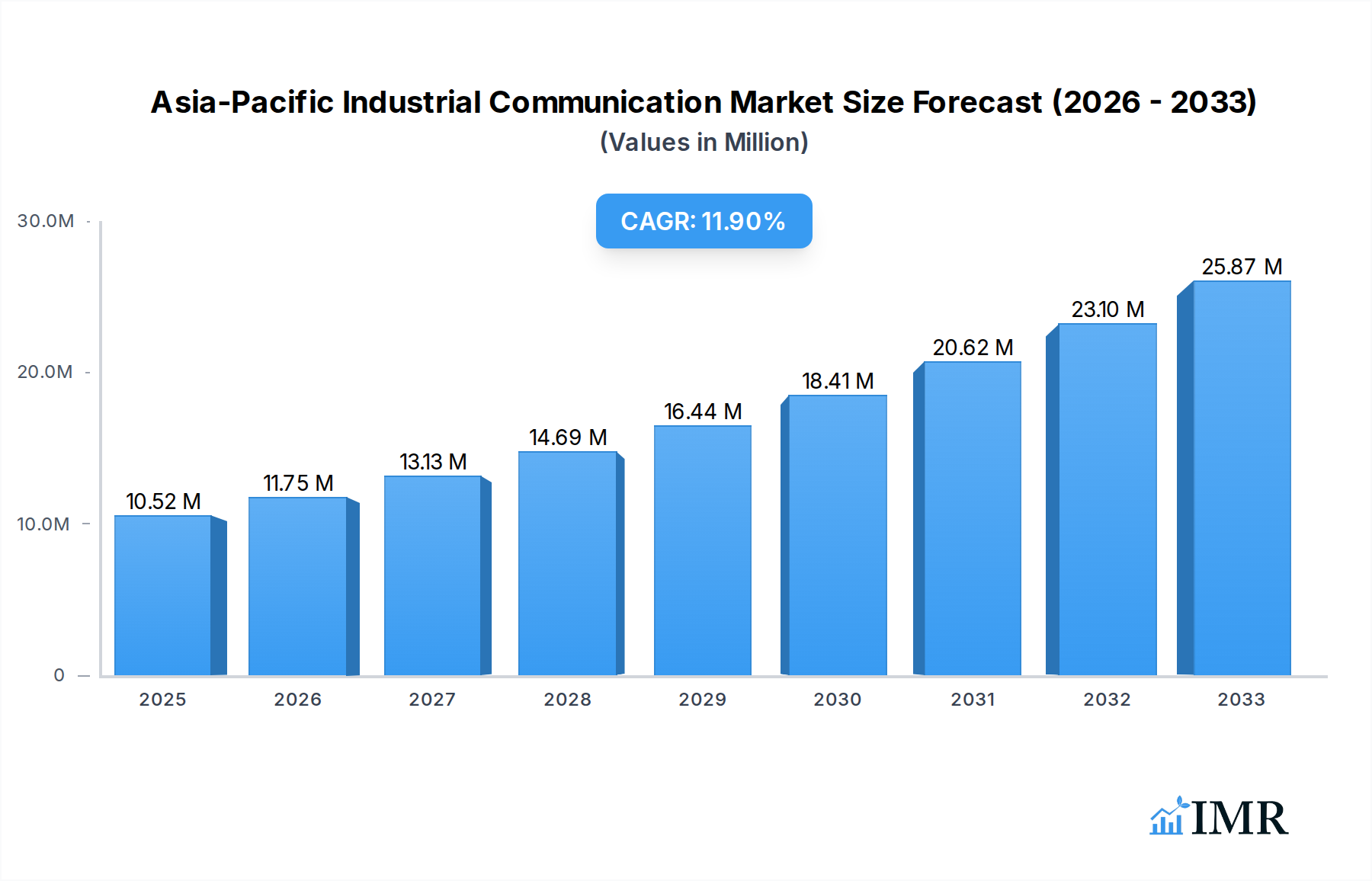

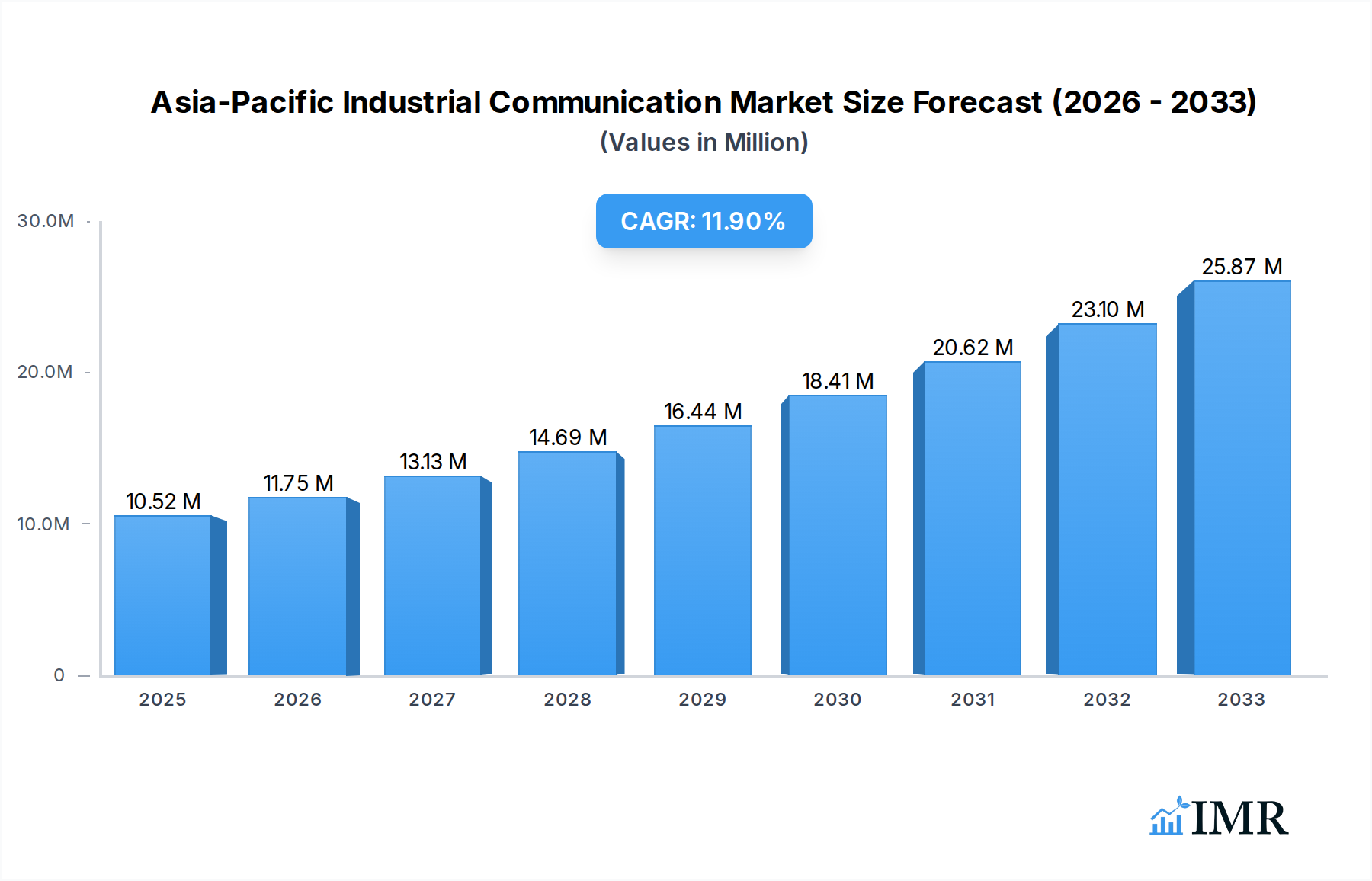

The Asia-Pacific industrial communication market is poised for significant expansion, with an estimated market size of 10.52 Million in 2025. This robust growth is driven by an anticipated Compound Annual Growth Rate (CAGR) of 11.63% over the forecast period of 2025-2033. The region's burgeoning industrial sector, characterized by rapid advancements in automation, smart manufacturing initiatives, and the increasing adoption of Industry 4.0 technologies, forms the bedrock of this surge. Key drivers include the escalating demand for real-time data acquisition and control systems, the imperative for enhanced operational efficiency, and the growing implementation of Industrial Internet of Things (IIoT) solutions across diverse industries. Furthermore, government support for digital transformation and manufacturing upgrades in countries like China, Japan, and South Korea is significantly fueling market penetration. The increasing complexity of industrial operations necessitates sophisticated communication networks capable of handling high bandwidth and low latency, making advanced industrial communication solutions indispensable.

Asia-Pacific Industrial Communication Market Market Size (In Million)

The market is segmented into Hardware, Software, and Services, with each segment contributing uniquely to the overall growth trajectory. Communication types, including Wired and Wireless technologies, are witnessing substantial adoption, with wireless solutions gaining traction due to their flexibility and ease of deployment in complex industrial environments. Major end-user industries such as Automotive, Oil and Gas, and the Utility Sector are at the forefront of adopting these technologies, seeking to optimize production processes, improve safety, and reduce downtime. Emerging trends like the convergence of IT and OT (Operational Technology), the rise of edge computing for localized data processing, and the increasing emphasis on cybersecurity for industrial networks are shaping the market landscape. While the market presents immense opportunities, potential restraints such as the high initial investment costs for advanced infrastructure and the need for skilled personnel to manage and maintain these complex systems could pose challenges. However, the overarching trend towards digitalization and automation is expected to outweigh these challenges, ensuring sustained market expansion across the Asia-Pacific region.

Asia-Pacific Industrial Communication Market Company Market Share

Asia-Pacific Industrial Communication Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a granular analysis of the Asia-Pacific Industrial Communication Market, a critical sector powering the region's digital transformation and Industry 4.0 initiatives. We delve into market dynamics, growth trends, regional dominance, product innovations, key drivers, challenges, and emerging opportunities, offering strategic insights for stakeholders. The study encompasses a comprehensive period from 2019 to 2033, with a Base Year of 2025 and a Forecast Period of 2025–2033. Historical data from 2019–2024 is also included. High-traffic keywords such as "industrial IoT communication," "smart factory networking," "industrial ethernet APAC," "wireless industrial networks," and "IIoT connectivity Asia" are strategically integrated to maximize search engine visibility.

Asia-Pacific Industrial Communication Market Market Dynamics & Structure

The Asia-Pacific industrial communication market is characterized by a dynamic interplay of factors shaping its structure and competitive landscape. Market concentration is observed to be moderately high, with established global players and increasingly capable regional manufacturers vying for market share. Technological innovation serves as a primary driver, fueled by the escalating adoption of Industry 4.0, the Industrial Internet of Things (IIoT), and automation across diverse manufacturing sectors. Regulatory frameworks, while evolving, are generally supportive of digital infrastructure development, though varying standards and data localization policies across countries can present complexities. Competitive product substitutes are abundant, ranging from traditional wired solutions to advanced wireless technologies, forcing vendors to differentiate on performance, reliability, and cost-effectiveness. End-user demographics are shifting towards a greater demand for scalable, secure, and low-latency communication solutions. Mergers and acquisitions (M&A) trends are active, with larger companies acquiring innovative startups or complementary technology providers to expand their portfolios and market reach.

- Market Concentration: Moderately high, with a mix of global leaders and emerging regional players.

- Technological Innovation Drivers: Industry 4.0, IIoT adoption, AI in manufacturing, smart grid expansion.

- Regulatory Frameworks: Generally supportive, with some regional variations impacting interoperability and data management.

- Competitive Product Substitutes: Extensive, from industrial Ethernet to 5G-based solutions.

- End-User Demographics: Growing demand for high-bandwidth, low-latency, and secure communication.

- M&A Trends: Active, focused on technology acquisition and market consolidation.

- Innovation Barriers: High R&D costs, interoperability challenges between legacy and new systems, and the need for robust cybersecurity measures.

- Quantitative Insights: Expected M&A deal volume in the industrial communication sector for APAC to be around 15-20 per year in the forecast period. Market share concentration among the top 5 players is estimated at 45-50%.

Asia-Pacific Industrial Communication Market Growth Trends & Insights

The Asia-Pacific industrial communication market is poised for robust expansion, driven by a confluence of technological advancements and increasing industrial digitalization. The market size is projected to witness substantial growth, escalating from an estimated USD XXXX million in 2025 to USD XXXX million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX.XX%. Adoption rates for advanced industrial communication technologies are accelerating across key end-user industries, propelled by the imperative to enhance operational efficiency, improve data analytics, and enable real-time decision-making. Technological disruptions, such as the proliferation of 5G, AI-driven network management, and edge computing, are fundamentally reshaping communication architectures, enabling unprecedented levels of connectivity and automation.

Consumer behavior shifts within the industrial sector are marked by a growing preference for integrated, end-to-end solutions that offer seamless data flow from the sensor to the cloud. Manufacturers are increasingly investing in scalable and flexible communication infrastructure to support the dynamic needs of smart factories, predictive maintenance, and remote monitoring. The rising prominence of the Industrial Internet of Things (IIoT) is a significant catalyst, demanding reliable and high-performance communication networks for the vast number of connected devices. Furthermore, government initiatives promoting digital transformation and smart manufacturing across countries like China, Japan, South Korea, and India are creating a fertile ground for market growth. The demand for specialized communication solutions, such as those supporting harsh environments or requiring ultra-low latency, is also on the rise, catering to industries like oil and gas, mining, and utilities. The shift towards wireless communication, driven by its flexibility and ease of deployment, is a notable trend, although wired solutions continue to hold significant relevance for critical infrastructure requiring utmost reliability. This evolving landscape presents substantial opportunities for vendors offering innovative and future-proof industrial communication solutions.

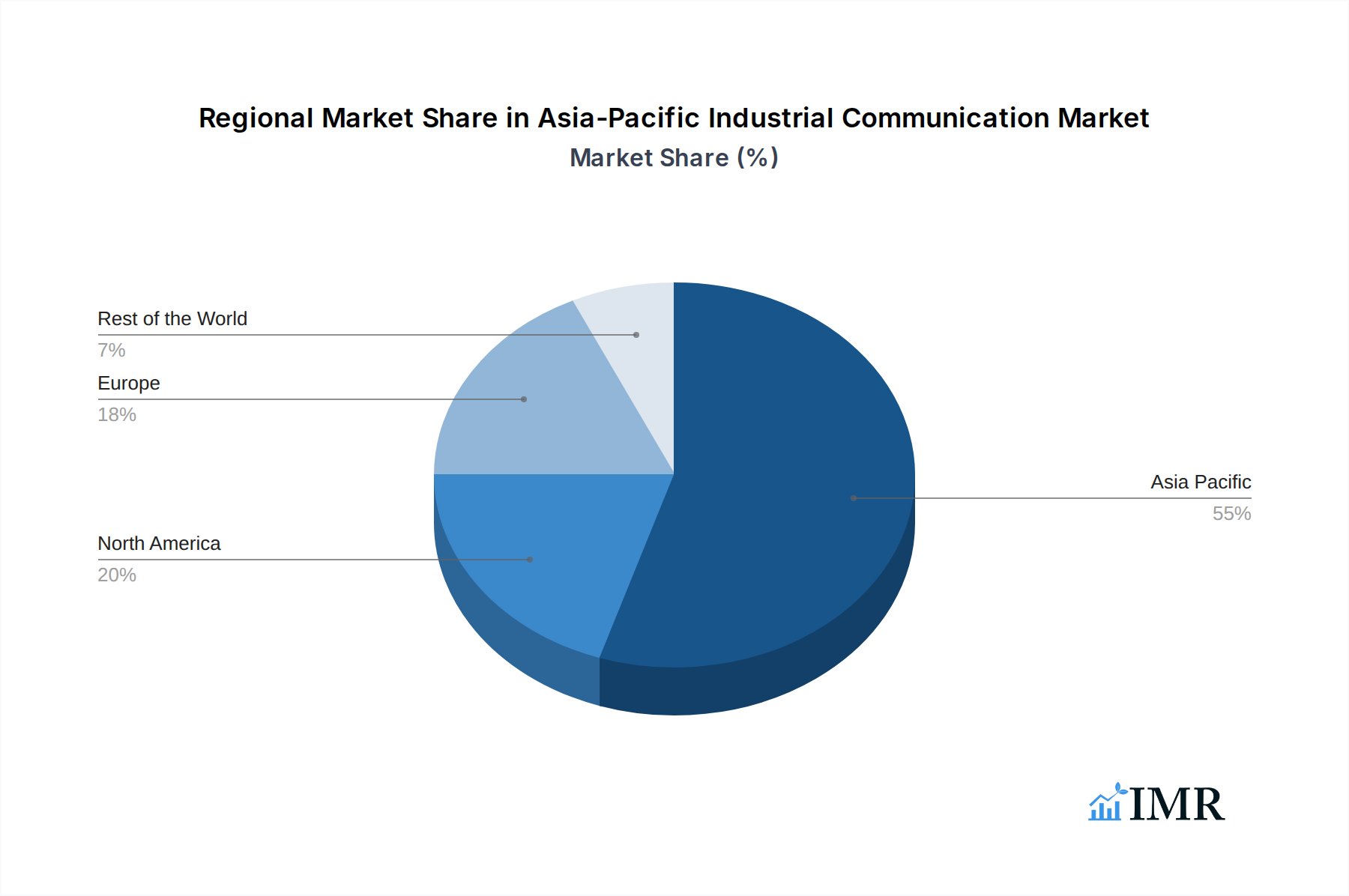

Dominant Regions, Countries, or Segments in Asia-Pacific Industrial Communication Market

The Asia-Pacific industrial communication market is a vast and diverse landscape, with several regions, countries, and segments playing pivotal roles in its growth. China emerges as the dominant country, driven by its immense manufacturing base, rapid adoption of Industry 4.0 technologies, and significant government investment in digital infrastructure. The country’s proactive approach to smart manufacturing and extensive deployment of industrial IoT networks position it as a key growth engine.

Among the Segments, Hardware represents the largest and most crucial component of the industrial communication market. This includes a wide array of devices such as industrial Ethernet switches, routers, gateways, wireless access points, and specialized communication modules. The increasing deployment of IIoT devices and the need for robust, high-performance networking infrastructure directly fuel the demand for industrial communication hardware.

In terms of Communication Type, Wired communication, particularly Industrial Ethernet, continues to be a dominant force due to its inherent reliability, deterministic performance, and high bandwidth, essential for critical automation and control systems. However, Wireless communication is experiencing rapid growth, fueled by the need for flexible deployments, mobility, and the proliferation of IIoT sensors. Technologies like Wi-Fi, cellular (4G/5G), and specialized industrial wireless protocols are gaining traction.

Focusing on End User Industry, the Automotive sector is a significant contributor, driven by the demand for sophisticated communication networks for automated assembly lines, robotics, and vehicle-to-everything (V2X) communication. The Utility Sector is another key driver, with increasing investments in smart grid technologies, remote monitoring of substations, and efficient energy management systems requiring advanced industrial communication. The Oil and Gas industry also plays a crucial role, with communication solutions needed for exploration, production, and transportation in challenging and remote environments, demanding ruggedized and reliable networking.

- Dominant Country: China, due to its massive manufacturing scale and government-led digital transformation initiatives.

- Dominant Segment: Hardware, encompassing switches, routers, gateways, and industrial PCs.

- Dominant Communication Type: Industrial Ethernet (Wired) for its reliability, with significant and growing adoption of Wireless solutions.

- Key End User Industries: Automotive, Utility Sector, and Oil and Gas are primary growth drivers.

- Market Share: China is estimated to hold over 40% of the Asia-Pacific industrial communication market share. The Hardware segment accounts for approximately 55-60% of the total market revenue.

- Growth Potential: The Wireless communication segment is projected to exhibit the highest CAGR due to the expanding IIoT ecosystem.

Asia-Pacific Industrial Communication Market Product Landscape

The product landscape of the Asia-Pacific industrial communication market is characterized by innovation and an increasing convergence of technologies. Manufacturers are developing solutions that offer enhanced cybersecurity features, greater bandwidth, lower latency, and improved ruggedness for deployment in harsh industrial environments. Key product advancements include the development of intelligent industrial switches with built-in analytics capabilities, compact and power-efficient wireless gateways supporting multiple protocols, and robust communication modules designed for extreme temperatures and vibration. The integration of AI and machine learning into network management software is enabling proactive fault detection and optimized network performance. Furthermore, the growing demand for edge computing is driving the development of edge-ready communication devices that can process data closer to the source, reducing reliance on centralized cloud infrastructure.

Key Drivers, Barriers & Challenges in Asia-Pacific Industrial Communication Market

The Asia-Pacific industrial communication market is propelled by several key drivers, including the escalating adoption of Industry 4.0 and IIoT across manufacturing sectors, the growing demand for automation and data-driven operational efficiency, and significant government initiatives supporting digital transformation and smart manufacturing. The increasing need for real-time monitoring, predictive maintenance, and remote access further fuels market expansion. Technological advancements, such as the rollout of 5G networks, are also creating new opportunities for high-performance industrial communication.

However, the market faces significant barriers and challenges. Supply chain disruptions, particularly those stemming from geopolitical factors and component shortages, can impede production and delivery timelines. Regulatory hurdles, including varying data privacy laws and standardization challenges across different countries, can create complexities for global vendors. Cybersecurity threats remain a paramount concern, requiring continuous investment in robust security measures to protect critical industrial infrastructure. Interoperability issues between legacy systems and newer technologies, along with the high initial cost of implementation for advanced communication solutions, can also act as restraints for smaller enterprises. Competitive pressures among a growing number of vendors also necessitate constant innovation and cost optimization.

Emerging Opportunities in Asia-Pacific Industrial Communication Market

Emerging opportunities in the Asia-Pacific industrial communication market are largely driven by the expanding reach of Industry 4.0 and the increasing demand for specialized connectivity solutions. The rapid growth of the IIoT ecosystem across nascent industries such as smart agriculture, aquaculture, and advanced logistics presents a significant untapped market. The development of 5G-enabled industrial applications, including autonomous mobile robots, enhanced remote control systems, and real-time quality inspection, offers considerable potential. Furthermore, the growing emphasis on sustainability and energy efficiency is creating demand for communication solutions that enable better energy management and resource optimization in industrial processes. The edge computing paradigm is also opening avenues for localized data processing and analytics, requiring robust and intelligent edge communication devices.

Growth Accelerators in the Asia-Pacific Industrial Communication Market Industry

Long-term growth in the Asia-Pacific industrial communication market will be significantly accelerated by continued technological breakthroughs, particularly in the realm of wireless communication standards like 5G and Wi-Fi 6E, offering unprecedented speed and low latency. Strategic partnerships between hardware manufacturers, software providers, and system integrators will be crucial for delivering comprehensive, end-to-end solutions tailored to specific industry needs. Market expansion strategies targeting developing economies within the APAC region, coupled with localized product development and support, will unlock new customer bases. The increasing focus on predictive maintenance and AI-driven automation will necessitate more sophisticated and resilient communication networks, acting as a powerful growth catalyst. Furthermore, government incentives and policies promoting digital transformation will continue to provide a favorable environment for market expansion.

Key Players Shaping the Asia-Pacific Industrial Communication Market Market

- Belden Inc

- Rockwell Automation

- Hilscher

- Antaira Technologies Co Ltd

- ORing Industrial Networking Corp

- Lantech Communications Global Inc

- Aaeon Technology Inc

- Mitsubishi Electric Corporation

- MOXA Inc

- SICK AG

- Cisco Systems Inc

- Siemens AG

- Schneider Electric SE

- Omron Corporation

- HMS Networks AB

- Huawei Technologies Co Ltd

- Advantech Co Ltd

- Nokia Corporation

- Hitachi Energy Ltd (Hitachi Group)

- ABB Limited

- General Electric Company

Notable Milestones in Asia-Pacific Industrial Communication Market Sector

- February 2024: Hitachi Energy launched the TRO670 hybrid wireless router, a new addition to its TRO600 series, designed for low-latency and high-throughput industrial wireless communications, supporting smart grid and IIoT applications.

- February 2024: Helukabel announced the commencement of operations at its new, 25,000 square meter production facility in Changzhou, China, representing its largest investment outside Germany and bolstering its industrial cable and accessory manufacturing capabilities in the region.

In-Depth Asia-Pacific Industrial Communication Market Market Outlook

The Asia-Pacific industrial communication market is set for sustained and dynamic growth, driven by the relentless pursuit of operational excellence and digital integration. Future market potential is significantly boosted by the ongoing global shift towards smart manufacturing and the increasing adoption of IIoT solutions across diverse industrial verticals. Strategic opportunities lie in catering to the evolving needs for highly secure, resilient, and low-latency communication networks, particularly with the continued rollout of 5G infrastructure. Vendors that can offer integrated hardware, software, and service packages, alongside robust cybersecurity and reliable post-sales support, will be best positioned for success. The market's trajectory indicates a strong preference for scalable and adaptable solutions that can evolve with the rapid pace of technological advancement, promising a vibrant and expanding future for industrial communication in the region.

Asia-Pacific Industrial Communication Market Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

- 1.3. Services

-

2. Communication Type

- 2.1. Wired

- 2.2. Wireless

- 2.3. Analysis

-

3. End User Industry

- 3.1. Automotive

- 3.2. Oil and Gas

- 3.3. Utility Sector

- 3.4. Food and Beverage

- 3.5. Aerospace and Defense

- 3.6. Metal and Mining

- 3.7. Other End-user Industries

Asia-Pacific Industrial Communication Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Industrial Communication Market Regional Market Share

Geographic Coverage of Asia-Pacific Industrial Communication Market

Asia-Pacific Industrial Communication Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Services

- 5.2. Market Analysis, Insights and Forecast - by Communication Type

- 5.2.1. Wired

- 5.2.2. Wireless

- 5.2.3. Analysis

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. Automotive

- 5.3.2. Oil and Gas

- 5.3.3. Utility Sector

- 5.3.4. Food and Beverage

- 5.3.5. Aerospace and Defense

- 5.3.6. Metal and Mining

- 5.3.7. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Asia-Pacific Industrial Communication Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Services

- 6.2. Market Analysis, Insights and Forecast - by Communication Type

- 6.2.1. Wired

- 6.2.2. Wireless

- 6.2.3. Analysis

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. Automotive

- 6.3.2. Oil and Gas

- 6.3.3. Utility Sector

- 6.3.4. Food and Beverage

- 6.3.5. Aerospace and Defense

- 6.3.6. Metal and Mining

- 6.3.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Belden Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Rockwell Automation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hilscher

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Antaira Technologies Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ORing Industrial Networking Corp

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Lantech Communications Global Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Aaeon Technology Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mitsubishi Electric Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 MOXA Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 SICK AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Cisco Systems Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Siemens AG

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Schneider Electric SE

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Omron Corporation

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 HMS Networks A

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Huawei Technologies Co Ltd

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Advantech Co Ltd

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Nokia Corporation

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Hitachi Energy Ltd (Hitachi Group)

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.20 ABB Limited

- 7.1.20.1. Company Overview

- 7.1.20.2. Products

- 7.1.20.3. Company Financials

- 7.1.20.4. SWOT Analysis

- 7.1.21 General Electric Company

- 7.1.21.1. Company Overview

- 7.1.21.2. Products

- 7.1.21.3. Company Financials

- 7.1.21.4. SWOT Analysis

- 7.1.1 Belden Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Industrial Communication Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Industrial Communication Market Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by Communication Type 2020 & 2033

- Table 4: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by Communication Type 2020 & 2033

- Table 5: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by End User Industry 2020 & 2033

- Table 6: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by End User Industry 2020 & 2033

- Table 7: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by Component 2020 & 2033

- Table 10: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 11: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by Communication Type 2020 & 2033

- Table 12: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by Communication Type 2020 & 2033

- Table 13: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by End User Industry 2020 & 2033

- Table 14: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by End User Industry 2020 & 2033

- Table 15: Asia-Pacific Industrial Communication Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Industrial Communication Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: China Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Japan Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Japan Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: South Korea Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: India Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Australia Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: New Zealand Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: New Zealand Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Indonesia Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Indonesia Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Malaysia Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Malaysia Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Singapore Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Singapore Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Thailand Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Thailand Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Vietnam Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Vietnam Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Philippines Asia-Pacific Industrial Communication Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Philippines Asia-Pacific Industrial Communication Market Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Industrial Communication Market?

The projected CAGR is approximately 11.63%.

2. Which companies are prominent players in the Asia-Pacific Industrial Communication Market?

Key companies in the market include Belden Inc, Rockwell Automation, Hilscher, Antaira Technologies Co Ltd, ORing Industrial Networking Corp, Lantech Communications Global Inc, Aaeon Technology Inc, Mitsubishi Electric Corporation, MOXA Inc, SICK AG, Cisco Systems Inc, Siemens AG, Schneider Electric SE, Omron Corporation, HMS Networks A, Huawei Technologies Co Ltd, Advantech Co Ltd, Nokia Corporation, Hitachi Energy Ltd (Hitachi Group), ABB Limited, General Electric Company.

3. What are the main segments of the Asia-Pacific Industrial Communication Market?

The market segments include Component, Communication Type, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.52 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of Industrial Automation; Expansion of Supporting Infrastructure Such as 5G Network. Iiot. Etc.

6. What are the notable trends driving market growth?

Automotive Industry to be the Largest End User.

7. Are there any restraints impacting market growth?

6.1 High Cost Involved & Lack of Standardization.

8. Can you provide examples of recent developments in the market?

February 2024 - Hitachi Energy launched the TRO670 hybrid wireless router. According to the company, the newly launched router is the latest addition to its TRO600 series of low-latency and high-throughput industrial wireless communications devices. It has been developed to support a variety of smart grid and Industrial Internet of Things (IIoT) applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Industrial Communication Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Industrial Communication Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Industrial Communication Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Industrial Communication Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence