Key Insights

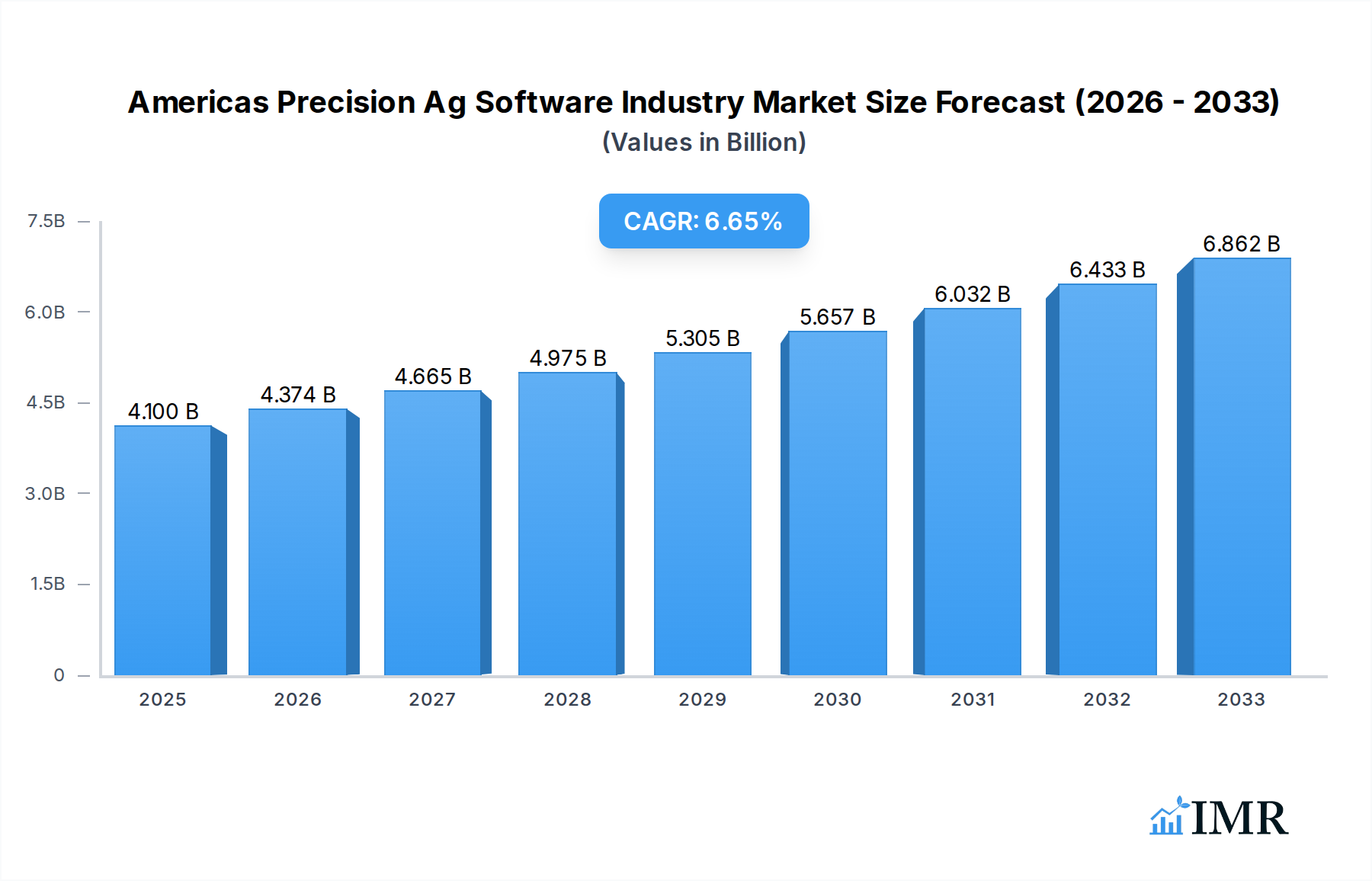

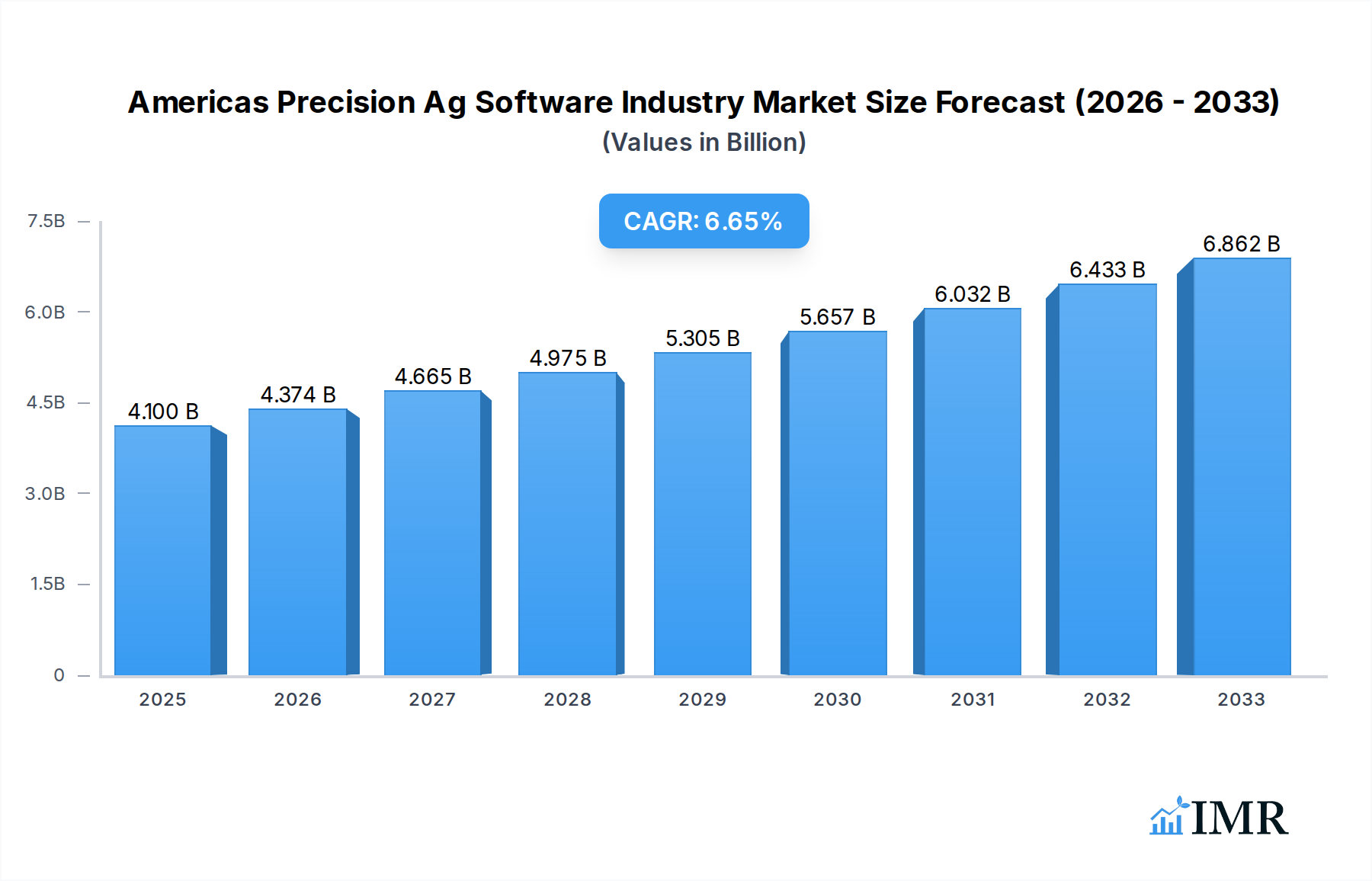

The Americas Precision Ag Software market is poised for robust expansion, reaching an estimated USD 4.1 billion in 2025. This growth is fueled by a significant compound annual growth rate (CAGR) of 6.7% projected over the forecast period. The increasing adoption of advanced agricultural technologies, driven by the need for enhanced crop yields, optimized resource utilization, and sustainable farming practices, is a primary catalyst. Farmers are increasingly recognizing the value of data-driven decision-making to mitigate risks associated with climate variability and fluctuating market demands. The market is segmented into Cloud-based and Local/Web-based solutions, with a discernible shift towards cloud offerings due to their scalability, accessibility, and advanced analytical capabilities. Key industry players like Deere & Company, IBM Corporation, and Trimble Inc. are heavily investing in research and development, introducing innovative software solutions that integrate with farm machinery and provide real-time insights into soil health, weather patterns, and pest management.

Americas Precision Ag Software Industry Market Size (In Billion)

The growth trajectory is further supported by favorable government initiatives promoting agricultural modernization and the rising disposable income among farmers, enabling them to invest in sophisticated precision agriculture tools. Key trends include the integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive analytics, the proliferation of IoT devices for seamless data collection, and the development of user-friendly interfaces to broaden accessibility. Despite the promising outlook, challenges such as high initial investment costs for some advanced solutions and the need for enhanced digital literacy among a segment of the farming community could pose some restraints. However, the overwhelming benefits of precision agriculture in terms of cost savings, improved efficiency, and environmental stewardship are expected to outweigh these challenges, ensuring sustained market expansion throughout the forecast period. The Americas, particularly the United States, Canada, and Brazil, are expected to remain dominant regions due to their large agricultural footprints and early adoption rates of precision farming technologies.

Americas Precision Ag Software Industry Company Market Share

This comprehensive report offers an in-depth analysis of the Americas Precision Ag Software market, providing critical insights for stakeholders navigating this dynamic sector. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, and a forecast period from 2025 to 2033, the report delves into historical trends, current market dynamics, and future growth trajectories. We examine the competitive landscape, technological advancements, and regional dominance, offering a holistic view of the market's evolution and potential.

Americas Precision Ag Software Industry Market Dynamics & Structure

The Americas Precision Ag Software market exhibits a moderately concentrated structure, with key players like Deere & Company, IBM Corporation, and AGCO Corporation holding significant market share. Technological innovation, driven by the need for increased efficiency, sustainability, and yield optimization, is a primary catalyst. Advancements in IoT, AI, machine learning, and big data analytics are transforming how farmers manage their operations. Regulatory frameworks, particularly concerning data privacy and agricultural subsidies, play a crucial role in shaping market entry and growth. Competitive product substitutes are emerging from adjacent software sectors and in-house solutions developed by agricultural equipment manufacturers. End-user demographics are shifting, with a growing adoption by younger, tech-savvy farmers and an increasing demand for user-friendly, integrated solutions. Mergers and acquisitions (M&A) activity is moderate, often aimed at acquiring specialized technologies or expanding market reach.

- Market Concentration: Moderate to high, with a few dominant players.

- Technological Innovation Drivers: IoT, AI, machine learning, big data analytics, remote sensing.

- Regulatory Frameworks: Data privacy laws, environmental regulations, agricultural policy.

- Competitive Product Substitutes: Farm management software from non-specialized providers, custom-built solutions.

- End-User Demographics: Growing adoption by millennials and Gen Z farmers, increasing demand for cloud-based solutions.

- M&A Trends: Strategic acquisitions for technology integration and market expansion.

Americas Precision Ag Software Industry Growth Trends & Insights

The Americas Precision Ag Software market is poised for robust growth, projected to reach $XX billion by 2025, with an estimated Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This expansion is fueled by the escalating need for sustainable agricultural practices, enhanced crop yields, and reduced operational costs. Adoption rates are accelerating across various farm sizes, from large commercial operations to smaller family farms, as the benefits of precision agriculture become more evident. Technological disruptions are continuously reshaping the market, with the integration of advanced analytics, predictive modeling, and automation solutions becoming standard. Consumer behavior shifts towards demanding more sustainably produced food are indirectly driving the adoption of precision agriculture technologies that enable resource efficiency and traceability. The market penetration of precision ag software is expected to increase significantly as more farmers recognize its value proposition in optimizing resource allocation, minimizing waste, and improving overall farm profitability. The market size evolution will be characterized by a steady upward trend, supported by ongoing research and development and increasing investment in agricultural technology.

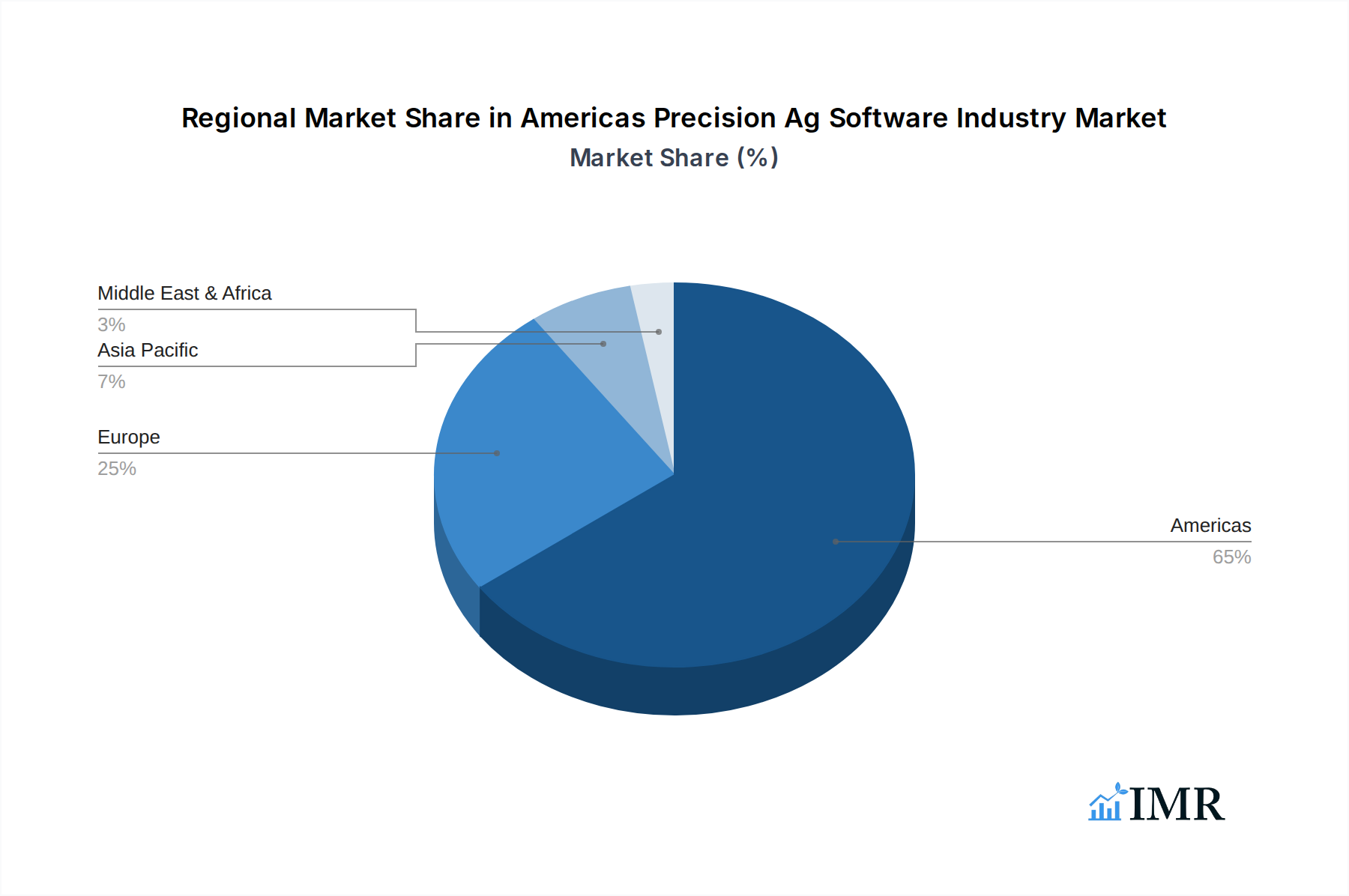

Dominant Regions, Countries, or Segments in Americas Precision Ag Software Industry

The United States stands out as the dominant country within the Americas Precision Ag Software market, driven by its vast agricultural landscape, significant investment in agricultural R&D, and a proactive approach to technological adoption. This dominance is further amplified by favorable government policies and robust infrastructure supporting the integration of advanced farming technologies. Within the "Type" segment, Cloud-based precision ag software is experiencing unprecedented growth and is projected to be the primary driver of market expansion. Its scalability, accessibility from any device, and ability to handle large datasets seamlessly make it an attractive option for farmers seeking efficient data management and analysis.

- Dominant Country: United States

- Key Drivers: Extensive arable land, high adoption of technology, government incentives, strong agricultural research ecosystem, increasing focus on data-driven farming.

- Market Share (Estimated 2025): XX% of the Americas market.

- Growth Potential: Continued innovation in AI and IoT integration, expansion into niche crop segments.

- Dominant Segment (Type): Cloud-based Precision Ag Software

- Key Drivers: Scalability, remote access, real-time data analytics, cost-effectiveness for data storage and processing, ease of integration with other cloud services.

- Market Share (Estimated 2025): XX% of the total Americas Precision Ag Software market.

- Growth Potential: Development of specialized cloud platforms for specific crop types and farming practices, enhanced cybersecurity measures for data protection.

- Other Contributing Factors: Canada also shows significant growth, particularly in regions with large-scale grain and oilseed production. Brazil, while still developing, presents a substantial long-term growth opportunity due to its massive agricultural output and increasing interest in modern farming techniques. The growing demand for automation and data-driven decision-making across all agricultural sectors in the Americas is further solidifying the market's upward trajectory.

Americas Precision Ag Software Industry Product Landscape

The product landscape of the Americas Precision Ag Software industry is characterized by continuous innovation, focusing on delivering actionable insights and automating complex farming tasks. Key product categories include farm management software, yield monitoring systems, soil sensing technologies, weather forecasting tools, and drone-based analytics platforms. Performance metrics emphasize increased yield by XX%, reduced input usage (fertilizers, water, pesticides) by XX%, and improved operational efficiency by XX%. Unique selling propositions often lie in the software's ability to integrate diverse data sources, provide predictive analytics for disease and pest outbreaks, and offer real-time guidance for planting, irrigation, and harvesting. Technological advancements are centered around the application of artificial intelligence and machine learning for hyper-personalized farm management, enabling farmers to make precise, data-backed decisions for each zone within their fields.

Key Drivers, Barriers & Challenges in Americas Precision Ag Software Industry

Key Drivers:

- Increasing demand for food security: Growing global population necessitates higher agricultural productivity.

- Technological advancements: Proliferation of IoT, AI, and big data analytics in agriculture.

- Focus on sustainability and resource efficiency: Drive to reduce water, fertilizer, and pesticide usage.

- Government initiatives and subsidies: Support for precision agriculture adoption.

- Declining costs of sensor technology: Making precision ag tools more accessible.

Barriers & Challenges:

- High initial investment costs: For some advanced precision ag hardware and software.

- Lack of digital literacy and technical expertise: Particularly among older farmers.

- Data connectivity and infrastructure limitations: In remote rural areas.

- Data security and privacy concerns: Regarding sensitive farm data.

- Interoperability issues: Between different hardware and software platforms.

- Resistance to change: From traditional farming practices.

- Supply chain disruptions: For hardware components.

- Regulatory hurdles: Evolving data privacy and ownership laws.

Emerging Opportunities in Americas Precision Ag Software Industry

Emerging opportunities in the Americas Precision Ag Software market lie in the development of highly specialized AI-driven decision support systems for niche crops, such as specialty fruits and vegetables, where precise management is critical for quality and yield. The integration of blockchain technology for enhanced traceability and supply chain transparency is another significant avenue, catering to consumer demand for verifiable origins of food products. Furthermore, the development of affordable, user-friendly mobile applications that provide real-time, localized agronomic advice will democratize access to precision agriculture for smaller farms. The expansion of predictive analytics for climate change adaptation, offering farmers tools to mitigate the impact of extreme weather events, also presents a substantial growth area.

Growth Accelerators in the Americas Precision Ag Software Industry Industry

Key catalysts accelerating long-term growth include breakthroughs in sensor technology, enabling more accurate and real-time data collection from fields. Strategic partnerships between software providers, hardware manufacturers, and agricultural cooperatives are crucial for bundling solutions and expanding market reach. The increasing availability of open-source data platforms and APIs is fostering innovation and integration, allowing for more comprehensive farm management solutions. Market expansion into underserved regions within Latin America, driven by increasing agricultural investment and a growing recognition of precision agriculture's benefits, will also significantly contribute to sustained growth.

Key Players Shaping the Americas Precision Ag Software Industry Market

- Deere & Company

- IBM Corporation

- AGCO Corporation

- AG Leader Technology Inc

- Taranis Inc

- AGJunction Inc

- Harris Geospatial Solutions Inc

- Trimble Inc

- AgDNA Technologies Inc

- Granular Inc

- Bayer CropScience AG

Notable Milestones in Americas Precision Ag Software Industry Sector

- 2019: Launch of advanced AI-powered scouting tools for early disease detection.

- 2020: Significant increase in cloud-based farm management platform adoption due to remote work trends.

- 2021: Major acquisitions of smaller precision ag technology startups by established players.

- 2022: Introduction of enhanced IoT sensor networks for real-time soil and environmental monitoring.

- 2023: Development of predictive analytics models for optimizing irrigation schedules based on weather forecasts and soil moisture data.

- 2024: Increased focus on data security and privacy solutions within precision ag software offerings.

In-Depth Americas Precision Ag Software Industry Market Outlook

The future of the Americas Precision Ag Software market is exceptionally promising, driven by ongoing technological advancements and a global imperative for sustainable food production. Growth accelerators will continue to stem from innovations in AI-driven analytics, the expansion of IoT connectivity across farms, and the development of more integrated and user-friendly platforms. Strategic partnerships and consolidation within the industry will foster more comprehensive solutions. The market's potential is further amplified by increasing government support for agricultural modernization and a growing awareness among farmers of the economic and environmental benefits of precision agriculture, ensuring a robust and expanding market.

Americas Precision Ag Software Industry Segmentation

-

1. Type

- 1.1. Cloud

- 1.2. Local/Web-based

Americas Precision Ag Software Industry Segmentation By Geography

-

1. Americas

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Brazil

- 1.5. Argentina

- 1.6. Chile

- 1.7. Colombia

- 1.8. Peru

Americas Precision Ag Software Industry Regional Market Share

Geographic Coverage of Americas Precision Ag Software Industry

Americas Precision Ag Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Cloud

- 5.1.2. Local/Web-based

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Americas

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Americas Precision Ag Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Cloud

- 6.1.2. Local/Web-based

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Deere & Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 IBM Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AGCO Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 AG Leader Technology Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Taranis Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 AGJunction Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Harris Geospatial Solutions Inc *List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Trimble Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AgDNA Technologies Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Granular Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Bayer CropScience AG

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Deere & Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Americas Precision Ag Software Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Americas Precision Ag Software Industry Share (%) by Company 2025

List of Tables

- Table 1: Americas Precision Ag Software Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Americas Precision Ag Software Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Americas Precision Ag Software Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Americas Precision Ag Software Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Brazil Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Argentina Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Chile Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Colombia Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Peru Americas Precision Ag Software Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Americas Precision Ag Software Industry?

The projected CAGR is approximately 10.5%.

2. Which companies are prominent players in the Americas Precision Ag Software Industry?

Key companies in the market include Deere & Company, IBM Corporation, AGCO Corporation, AG Leader Technology Inc, Taranis Inc, AGJunction Inc, Harris Geospatial Solutions Inc *List Not Exhaustive, Trimble Inc, AgDNA Technologies Inc, Granular Inc, Bayer CropScience AG.

3. What are the main segments of the Americas Precision Ag Software Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.5 billion as of 2022.

5. What are some drivers contributing to market growth?

; Adoption of Precision Technology in the Sustainable and Efficient Agriculture Sector in Americas; Shortage of Farm labor. Along with Increasing Farm Size Across North America.

6. What are the notable trends driving market growth?

Cloud-based Precision Farming Software is Expected to Grow Significantly.

7. Are there any restraints impacting market growth?

; High Capital Cost and Complexity Regarding System Upgrades.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Americas Precision Ag Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Americas Precision Ag Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Americas Precision Ag Software Industry?

To stay informed about further developments, trends, and reports in the Americas Precision Ag Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence