Key Insights

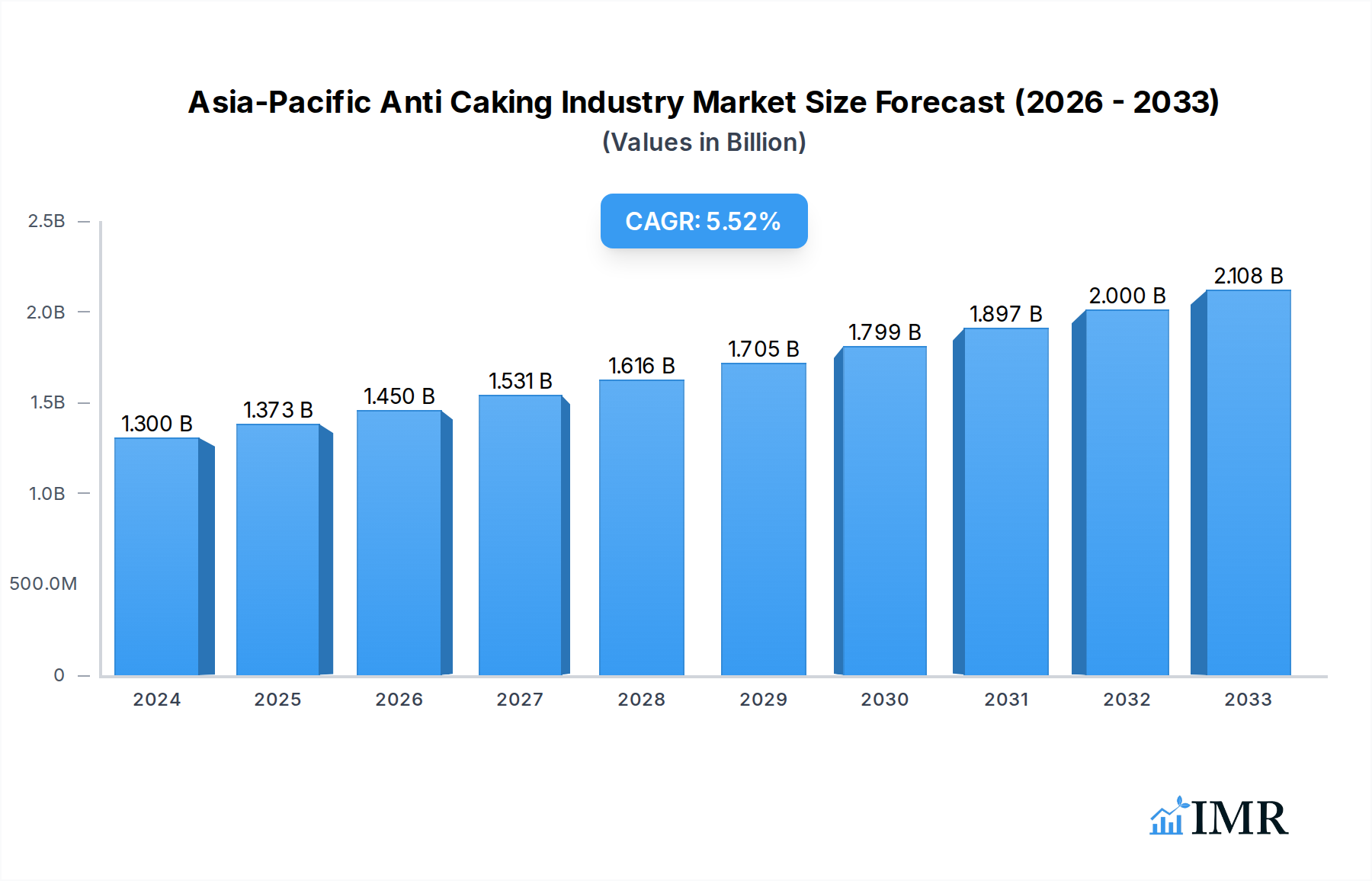

The Asia-Pacific Anti-Caking Agents market is poised for significant expansion, driven by robust demand across a spectrum of industries. With a market size of approximately USD 1.3 billion in 2024, the sector is projected to grow at a healthy Compound Annual Growth Rate (CAGR) of 5.6% through 2033. This growth is underpinned by the increasing reliance on anti-caking agents in food and beverage processing, particularly in bakery products, dairy, soups, sauces, and beverages, where they ensure product quality, shelf-life, and ease of handling. The cosmetic and personal care sector also presents a notable avenue for growth, as these agents improve the texture and flowability of powdered products. Furthermore, the animal feed industry's adoption of anti-caking solutions to maintain feed quality and prevent clumping contributes to market momentum.

Asia-Pacific Anti Caking Industry Market Size (In Billion)

The competitive landscape is characterized by the presence of major global players and a growing regional focus. Key drivers for this market include escalating food processing activities, increasing consumer demand for convenience foods, and stricter quality control standards in manufacturing. Emerging economies within the region, such as India and China, are expected to be significant contributors to market growth due to their expanding industrial bases and rising disposable incomes. While the market demonstrates strong upward potential, certain restraints, such as fluctuating raw material prices and increasing regulatory scrutiny on food additives in specific applications, warrant careful consideration by industry stakeholders. Nonetheless, the ongoing innovation in product development and strategic expansions by key companies are expected to propel the Asia-Pacific Anti-Caking Agents market forward.

Asia-Pacific Anti Caking Industry Company Market Share

Asia-Pacific Anti-Caking Agents Market Report: Unlock Growth Opportunities & Navigate Industry Dynamics (2019-2033)

This comprehensive report delves into the dynamic Asia-Pacific Anti-Caking Agents Market, offering unparalleled insights for stakeholders seeking to capitalize on burgeoning demand and evolving industry landscapes. Covering a study period from 2019 to 2033, with a base year of 2025, this report provides an in-depth analysis of market size, growth trends, key drivers, challenges, and emerging opportunities. Leveraging cutting-edge XXX, we deliver actionable intelligence on market concentration, technological innovation, regulatory frameworks, and competitive strategies.

Discover:

- Market Size & Forecast: Gain precise estimations of the market value in billions for the base year (2025) and forecast period (2025-2033).

- Segmentation Analysis: Understand the market penetration and growth potential across key segments including:

- Type: Calcium Compounds, Sodium Compounds, Magnesium Compounds, Others.

- Application: Food and Beverage (Bakery Products, Dairy Products, Soups & Sauces, Beverages, Others), Cosmetic and Personal Care, Feed.

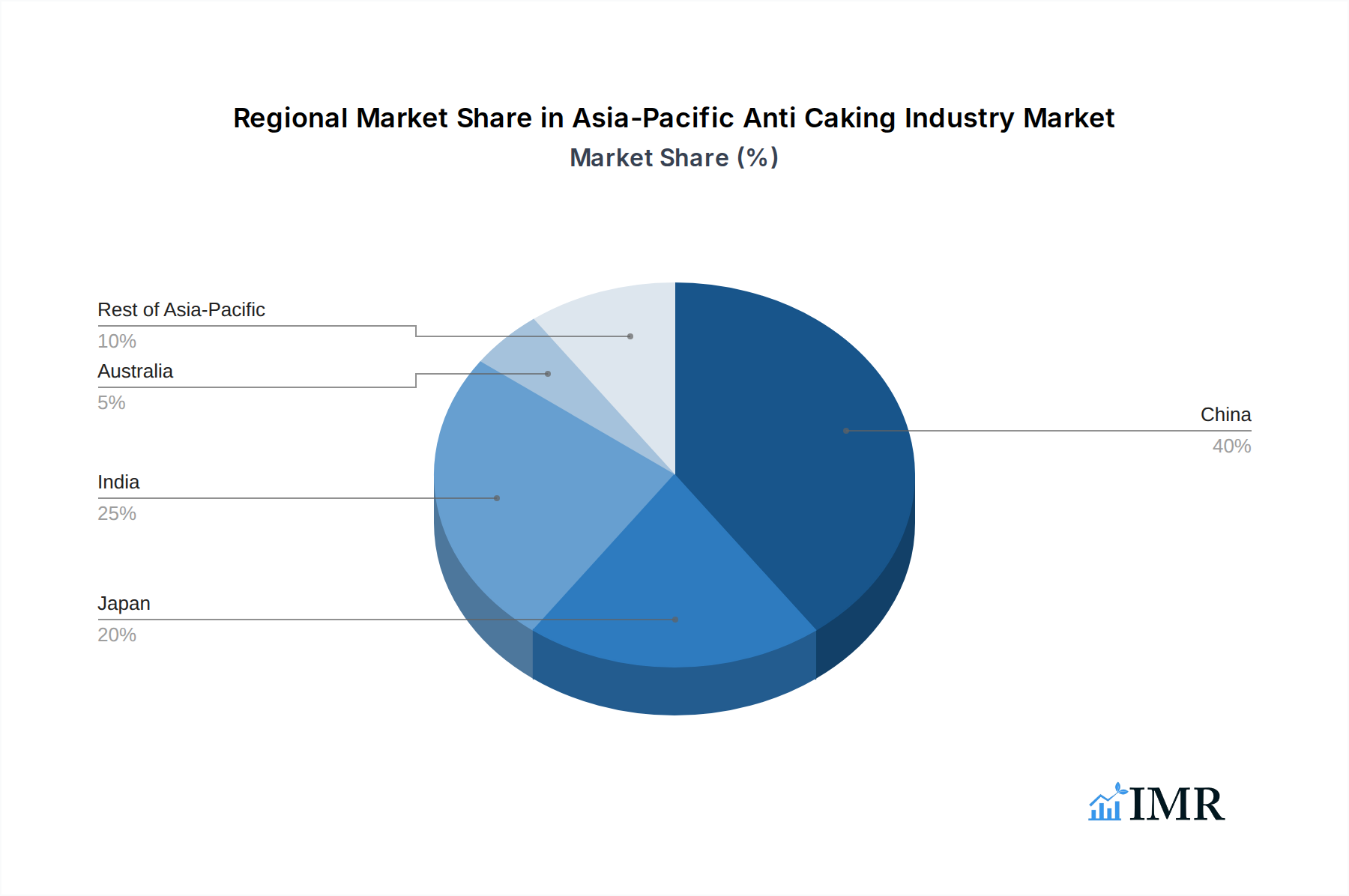

- Geographical Dominance: Identify leading markets and sub-regions, including China, Japan, India, Australia, and the Rest of Asia-Pacific.

- Competitive Landscape: Analyze the strategies and product offerings of key players, including AGC Chemicals, Merck KGaA, Kao Corporation, Roquette Freres, Evonik Industries AG, BASF SE, and others.

- Industry Developments: Track pivotal milestones and recent advancements shaping the market.

This report is essential for manufacturers, suppliers, R&D professionals, investors, and market strategists aiming to navigate the complexities and seize the immense growth potential of the Asia-Pacific Anti-Caking Agents industry.

Asia-Pacific Anti Caking Industry Market Dynamics & Structure

The Asia-Pacific anti-caking agents market is characterized by a moderately concentrated structure, with a few dominant players holding significant market share. Technological innovation remains a primary driver, with companies continuously investing in research and development to create more effective, versatile, and food-grade compliant anti-caking solutions. Emerging demand for natural and clean-label ingredients is pushing innovation towards plant-derived or naturally sourced anti-caking agents. The regulatory landscape varies across countries, with stringent food safety standards influencing product formulations and approvals, particularly for applications in the food and beverage sector. Competitive product substitutes, while present in some niche applications, are generally outpaced by the specialized functionalities of dedicated anti-caking agents. End-user demographics are evolving, with a growing middle class and increasing disposable income in countries like India and China driving demand for processed foods and personal care products, which in turn boosts the consumption of anti-caking agents. Merger and acquisition trends are observed as larger companies seek to expand their product portfolios, geographic reach, and technological capabilities within this growing market.

- Market Concentration: Dominated by a blend of global chemical giants and specialized ingredient providers.

- Technological Innovation Drivers: Focus on enhanced efficacy, broader application compatibility, and natural ingredient trends.

- Regulatory Frameworks: Driven by food safety standards (e.g., FDA, EFSA equivalents in APAC) and chemical regulations, impacting R&D and market entry.

- Competitive Product Substitutes: Limited direct substitutes for core applications, but natural alternatives are gaining traction.

- End-User Demographics: Shifting consumer preferences towards convenience foods and personal care products in emerging economies.

- M&A Trends: Strategic acquisitions to broaden product lines and expand market presence.

Asia-Pacific Anti Caking Industry Growth Trends & Insights

The Asia-Pacific anti-caking agents market is poised for robust growth, driven by the escalating demand for processed and convenience foods across the region. Market size is projected to expand significantly from an estimated \$XX billion in 2025 to a projected \$XX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX%. This expansion is fueled by increasing urbanization, changing lifestyles, and a growing middle-class population with higher disposable incomes, particularly in countries like China, India, and Southeast Asian nations. Adoption rates of anti-caking agents are steadily rising as manufacturers seek to improve product shelf-life, maintain product quality, and enhance handling and processing efficiency in a wide array of applications.

Technological disruptions, while not fundamentally altering the core chemistry of anti-caking agents, are focused on enhancing their performance and sustainability. Innovations include the development of highly efficient silica-based agents, improved natural alternatives like starches and cellulose derivatives, and optimized formulations for specific food matrices. The trend towards "clean label" products is influencing consumer behavior, prompting manufacturers to explore and adopt anti-caking agents that are perceived as natural and minimally processed. This consumer shift is a key factor driving research into plant-based and mineral-derived solutions.

The expanding food and beverage sector, particularly in bakery products, dairy products, and convenience meals, represents a primary growth engine. As these industries mature and cater to evolving consumer tastes, the need for effective anti-caking solutions to prevent clumping and ensure uniform product consistency becomes paramount. Furthermore, the burgeoning cosmetic and personal care industry, alongside the agricultural sector's increasing reliance on efficient animal feed formulations, also contributes to the overall market expansion. The inherent need to maintain the free-flowing nature of powders and granules across these diverse applications underscores the sustained demand for anti-caking agents.

Dominant Regions, Countries, or Segments in Asia-Pacific Anti Caking Industry

China stands as the undisputed dominant force within the Asia-Pacific anti-caking agents market, driven by its sheer population size, rapid industrialization, and the burgeoning demand across its vast food and beverage, cosmetic, and animal feed industries. The country's significant manufacturing capabilities and its role as a global production hub for various consumer goods directly translate into substantial consumption of anti-caking agents. China's rapidly expanding middle class, coupled with increasing urbanization, fuels a consistent demand for processed foods, baked goods, and personal care items, all of which rely on anti-caking agents for product integrity and shelf-life. For instance, the bakery products segment within China alone accounts for a substantial portion of the anti-caking agent demand due to the widespread consumption of bread, cakes, and pastries.

India emerges as another powerhouse, exhibiting a remarkable growth trajectory. Its large and young population, coupled with a growing economy and increasing disposable incomes, is driving significant expansion in its food processing and personal care sectors. The Indian government's "Make in India" initiative further bolsters domestic manufacturing, thereby increasing the local demand for various industrial ingredients, including anti-caking agents. The food and beverage segment, especially dairy products and processed snacks, is a key driver here.

The "Rest of Asia-Pacific" category, encompassing nations like Indonesia, Vietnam, and the Philippines, presents a significant and rapidly growing market. These economies are experiencing rapid industrialization, urbanization, and a demographic dividend, leading to a substantial increase in the consumption of processed foods and personal care products. Government policies aimed at promoting manufacturing and attracting foreign investment are further accelerating growth in these sub-regions.

Among the segments, Food and Beverage is the most dominant application area for anti-caking agents across the Asia-Pacific region. This dominance is attributed to the widespread use of anti-caking agents in enhancing the texture, flowability, and shelf-life of a vast array of products, including bakery items, dairy powders, soups, sauces, and beverages. The increasing consumer preference for convenience foods and the expansion of the foodservice industry further solidify the position of the food and beverage sector as the primary growth engine for anti-caking agents in the region.

Asia-Pacific Anti Caking Industry Product Landscape

The Asia-Pacific anti-caking agents market is characterized by a diverse product landscape catering to a wide spectrum of industrial needs. Leading manufacturers offer a range of compounds, including silica-based agents like amorphous silica and precipitated silica, which are highly effective due to their porous structure and high surface area. Calcium compounds such as calcium silicate and tricalcium phosphate are also widely utilized, particularly in food applications, owing to their regulatory approval and cost-effectiveness. Sodium compounds, including sodium ferrocyanide and sodium aluminosilicate, find extensive use in salt and seasoning applications. Beyond these, a growing emphasis is placed on natural and organic anti-caking agents, such as cellulose derivatives, starches, and plant-based extracts, appealing to the rising demand for clean-label products. Innovations focus on enhanced efficacy at lower dosage rates, improved particle dispersion, and tailored functionalities for specific applications, such as preventing caking in powdered dairy products or ensuring free flow of spices.

Key Drivers, Barriers & Challenges in Asia-Pacific Anti Caking Industry

The Asia-Pacific anti-caking industry is propelled by several key drivers. The burgeoning food and beverage sector, fueled by rising disposable incomes and evolving consumer lifestyles, necessitates effective solutions for product quality and shelf-life. Growing demand for convenience foods and the expansion of the cosmetic and personal care industries further boost consumption. Technological advancements in developing more efficient and specialized anti-caking agents also act as a significant growth accelerator. Favorable government initiatives promoting manufacturing and food processing in emerging economies like India and Southeast Asian nations provide a conducive environment.

However, the industry faces notable barriers and challenges. Stringent and varying regulatory frameworks across different Asia-Pacific countries can pose hurdles to market entry and product approval. Fluctuations in the prices of raw materials, such as silica and calcium compounds, can impact profitability margins. The increasing consumer preference for "clean label" and natural ingredients presents a challenge for synthetic anti-caking agents, necessitating innovation in plant-based alternatives. Supply chain disruptions, particularly in recent times, can affect the availability and cost of essential raw materials. Intense competition among established players and emerging regional manufacturers also exerts pressure on pricing and market share.

Emerging Opportunities in Asia-Pacific Anti Caking Industry

Emerging opportunities in the Asia-Pacific anti-caking industry lie in the growing demand for natural and organic anti-caking agents, driven by the "clean label" trend and increasing consumer awareness regarding health and wellness. The expansion of the functional food and beverage sector, incorporating specialized ingredients for health benefits, presents a niche market for anti-caking agents that complement these formulations. Furthermore, untapped markets in developing countries within Southeast Asia and the Indian subcontinent offer significant growth potential as their economies and consumer bases expand. Innovations in biodegradable and sustainable anti-caking solutions are also anticipated to gain traction, aligning with global environmental consciousness. The development of tailored anti-caking agents for specific emerging applications, such as specialized pharmaceutical powders or high-performance agricultural inputs, also represents a promising avenue.

Growth Accelerators in the Asia-Pacific Anti Caking Industry Industry

Several catalysts are accelerating long-term growth in the Asia-Pacific anti-caking industry. The continuous innovation pipeline, driven by R&D investments, is crucial, focusing on enhancing the efficacy and versatility of existing products while exploring novel, nature-derived alternatives. Strategic partnerships and collaborations between ingredient manufacturers and food processing companies are vital for developing customized solutions that meet evolving industry needs. Market expansion strategies, including targeting underserved geographical regions within Asia-Pacific and penetrating emerging application sectors, are key growth drivers. Furthermore, the increasing adoption of advanced manufacturing technologies and automation within the anti-caking agent production process contributes to improved efficiency and cost-effectiveness, thereby supporting market expansion. The growing emphasis on food safety and quality standards across the region also indirectly fuels the demand for reliable anti-caking solutions.

Key Players Shaping the Asia-Pacific Anti Caking Industry Market

- AGC Chemicals

- Merck KGaA

- Kao Corporation

- Roquette Freres

- Evonik Industries AG

- BASF SE

Notable Milestones in Asia-Pacific Anti Caking Industry Sector

- 2023: Increased R&D focus on plant-based anti-caking agents in response to clean-label trends.

- 2022: Introduction of enhanced silica-based anti-caking agents with improved moisture absorption capabilities.

- 2021: Several strategic acquisitions and mergers aimed at expanding product portfolios and market reach within the region.

- 2020: Heightened demand for anti-caking agents in food fortification applications due to increased health awareness.

- 2019: Growing adoption of magnesium compounds for their anti-caking properties in specialized food products.

In-Depth Asia-Pacific Anti Caking Industry Market Outlook

The Asia-Pacific anti-caking industry market outlook is exceptionally positive, driven by the confluence of increasing consumer demand for processed goods, rapid industrial growth, and a persistent need for product quality and stability. Growth accelerators will continue to be fueled by technological breakthroughs in developing highly effective and sustainable anti-caking solutions, including natural and organic alternatives that cater to the rising "clean label" trend. Strategic partnerships between ingredient suppliers and end-users will foster innovation and market penetration. As economies in emerging Asia-Pacific nations mature, the demand for advanced anti-caking agents in food and beverages, cosmetics, and animal feed will further intensify. The market is projected to witness sustained growth, presenting significant strategic opportunities for players who can adapt to evolving consumer preferences and regulatory landscapes while capitalizing on the expanding industrial base of the region.

Asia-Pacific Anti Caking Industry Segmentation

-

1. Type

- 1.1. Calcium Compounds

- 1.2. Sodium Compounds

- 1.3. Magnesium Compounds

- 1.4. Others

-

2. Application

-

2.1. Food and Beverage

- 2.1.1. Bakery Products

- 2.1.2. Dairy Products

- 2.1.3. Soups & Sauces

- 2.1.4. Beverages

- 2.1.5. Others

- 2.2. Cosmetic and Personal Care

- 2.3. Feed

-

2.1. Food and Beverage

-

3. Geography

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia-Pacific

Asia-Pacific Anti Caking Industry Segmentation By Geography

- 1. China

- 2. Japan

- 3. India

- 4. Australia

- 5. Rest of Asia Pacific

Asia-Pacific Anti Caking Industry Regional Market Share

Geographic Coverage of Asia-Pacific Anti Caking Industry

Asia-Pacific Anti Caking Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Calcium Compounds

- 5.1.2. Sodium Compounds

- 5.1.3. Magnesium Compounds

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Food and Beverage

- 5.2.1.1. Bakery Products

- 5.2.1.2. Dairy Products

- 5.2.1.3. Soups & Sauces

- 5.2.1.4. Beverages

- 5.2.1.5. Others

- 5.2.2. Cosmetic and Personal Care

- 5.2.3. Feed

- 5.2.1. Food and Beverage

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. China

- 5.3.2. Japan

- 5.3.3. India

- 5.3.4. Australia

- 5.3.5. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.4.2. Japan

- 5.4.3. India

- 5.4.4. Australia

- 5.4.5. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Calcium Compounds

- 6.1.2. Sodium Compounds

- 6.1.3. Magnesium Compounds

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Food and Beverage

- 6.2.1.1. Bakery Products

- 6.2.1.2. Dairy Products

- 6.2.1.3. Soups & Sauces

- 6.2.1.4. Beverages

- 6.2.1.5. Others

- 6.2.2. Cosmetic and Personal Care

- 6.2.3. Feed

- 6.2.1. Food and Beverage

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. China

- 6.3.2. Japan

- 6.3.3. India

- 6.3.4. Australia

- 6.3.5. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. China Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Calcium Compounds

- 7.1.2. Sodium Compounds

- 7.1.3. Magnesium Compounds

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Food and Beverage

- 7.2.1.1. Bakery Products

- 7.2.1.2. Dairy Products

- 7.2.1.3. Soups & Sauces

- 7.2.1.4. Beverages

- 7.2.1.5. Others

- 7.2.2. Cosmetic and Personal Care

- 7.2.3. Feed

- 7.2.1. Food and Beverage

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. China

- 7.3.2. Japan

- 7.3.3. India

- 7.3.4. Australia

- 7.3.5. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Japan Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Calcium Compounds

- 8.1.2. Sodium Compounds

- 8.1.3. Magnesium Compounds

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Food and Beverage

- 8.2.1.1. Bakery Products

- 8.2.1.2. Dairy Products

- 8.2.1.3. Soups & Sauces

- 8.2.1.4. Beverages

- 8.2.1.5. Others

- 8.2.2. Cosmetic and Personal Care

- 8.2.3. Feed

- 8.2.1. Food and Beverage

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. China

- 8.3.2. Japan

- 8.3.3. India

- 8.3.4. Australia

- 8.3.5. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. India Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Calcium Compounds

- 9.1.2. Sodium Compounds

- 9.1.3. Magnesium Compounds

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Food and Beverage

- 9.2.1.1. Bakery Products

- 9.2.1.2. Dairy Products

- 9.2.1.3. Soups & Sauces

- 9.2.1.4. Beverages

- 9.2.1.5. Others

- 9.2.2. Cosmetic and Personal Care

- 9.2.3. Feed

- 9.2.1. Food and Beverage

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. China

- 9.3.2. Japan

- 9.3.3. India

- 9.3.4. Australia

- 9.3.5. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Australia Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Calcium Compounds

- 10.1.2. Sodium Compounds

- 10.1.3. Magnesium Compounds

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Food and Beverage

- 10.2.1.1. Bakery Products

- 10.2.1.2. Dairy Products

- 10.2.1.3. Soups & Sauces

- 10.2.1.4. Beverages

- 10.2.1.5. Others

- 10.2.2. Cosmetic and Personal Care

- 10.2.3. Feed

- 10.2.1. Food and Beverage

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. China

- 10.3.2. Japan

- 10.3.3. India

- 10.3.4. Australia

- 10.3.5. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of Asia Pacific Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Calcium Compounds

- 11.1.2. Sodium Compounds

- 11.1.3. Magnesium Compounds

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Food and Beverage

- 11.2.1.1. Bakery Products

- 11.2.1.2. Dairy Products

- 11.2.1.3. Soups & Sauces

- 11.2.1.4. Beverages

- 11.2.1.5. Others

- 11.2.2. Cosmetic and Personal Care

- 11.2.3. Feed

- 11.2.1. Food and Beverage

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. China

- 11.3.2. Japan

- 11.3.3. India

- 11.3.4. Australia

- 11.3.5. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 AGC Chemicals

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck KGaA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kao Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Roquette Freres

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Evonik Industries AG*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BASF SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 AGC Chemicals

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Anti Caking Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Anti Caking Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 24: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Anti Caking Industry?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Asia-Pacific Anti Caking Industry?

Key companies in the market include AGC Chemicals, Merck KGaA, Kao Corporation, Roquette Freres, Evonik Industries AG*List Not Exhaustive, BASF SE.

3. What are the main segments of the Asia-Pacific Anti Caking Industry?

The market segments include Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.3 billion as of 2022.

5. What are some drivers contributing to market growth?

Innovation in Vanillin Synthesis; Diverse Functionality of Vanillin In End-use Industries.

6. What are the notable trends driving market growth?

Growing Demand in Bakery Industry.

7. Are there any restraints impacting market growth?

Supply Chain Variability Impacting Vanilla Bean Availability For Flavor Production.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Anti Caking Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Anti Caking Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Anti Caking Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Anti Caking Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence