Key Insights

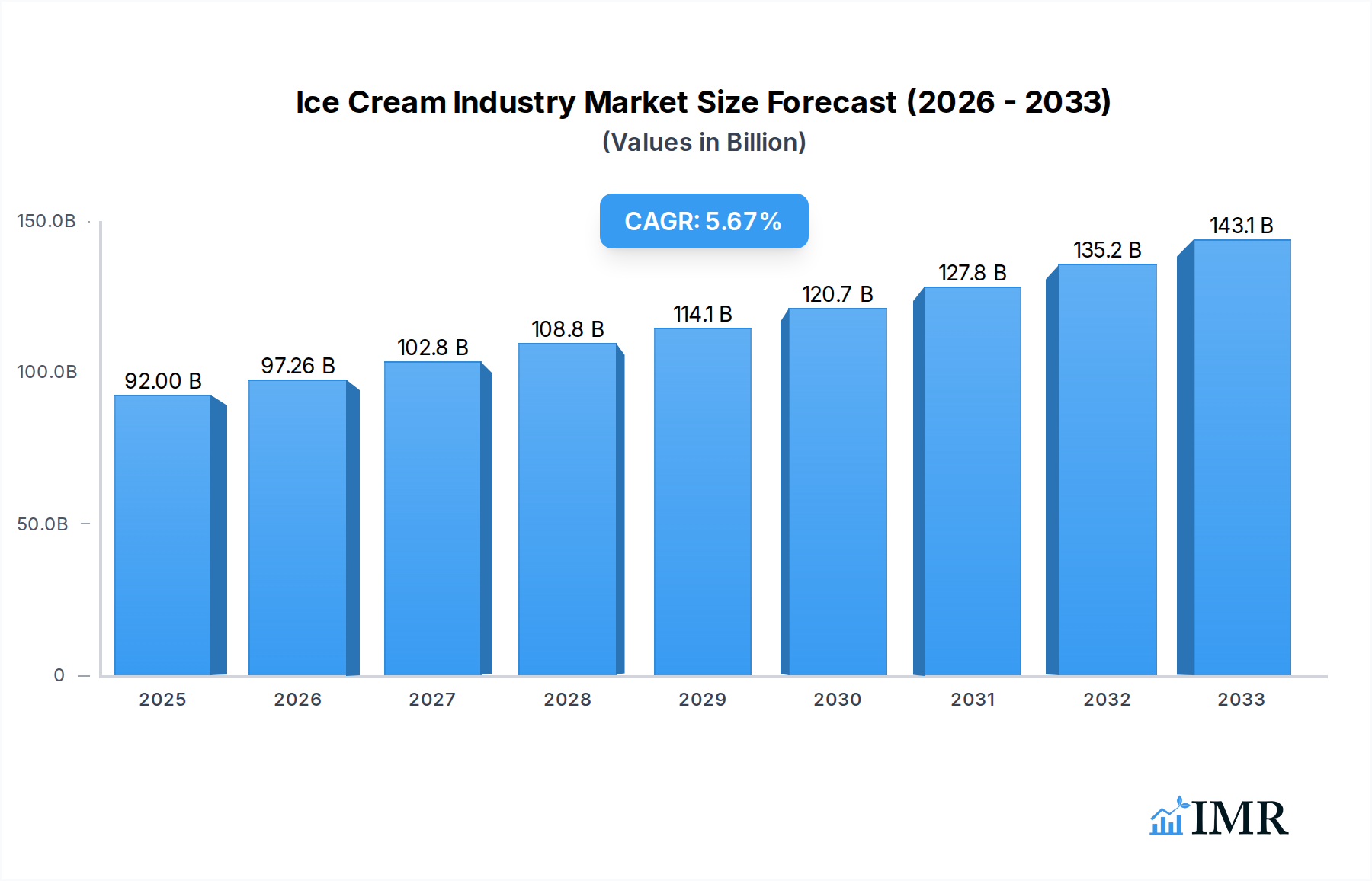

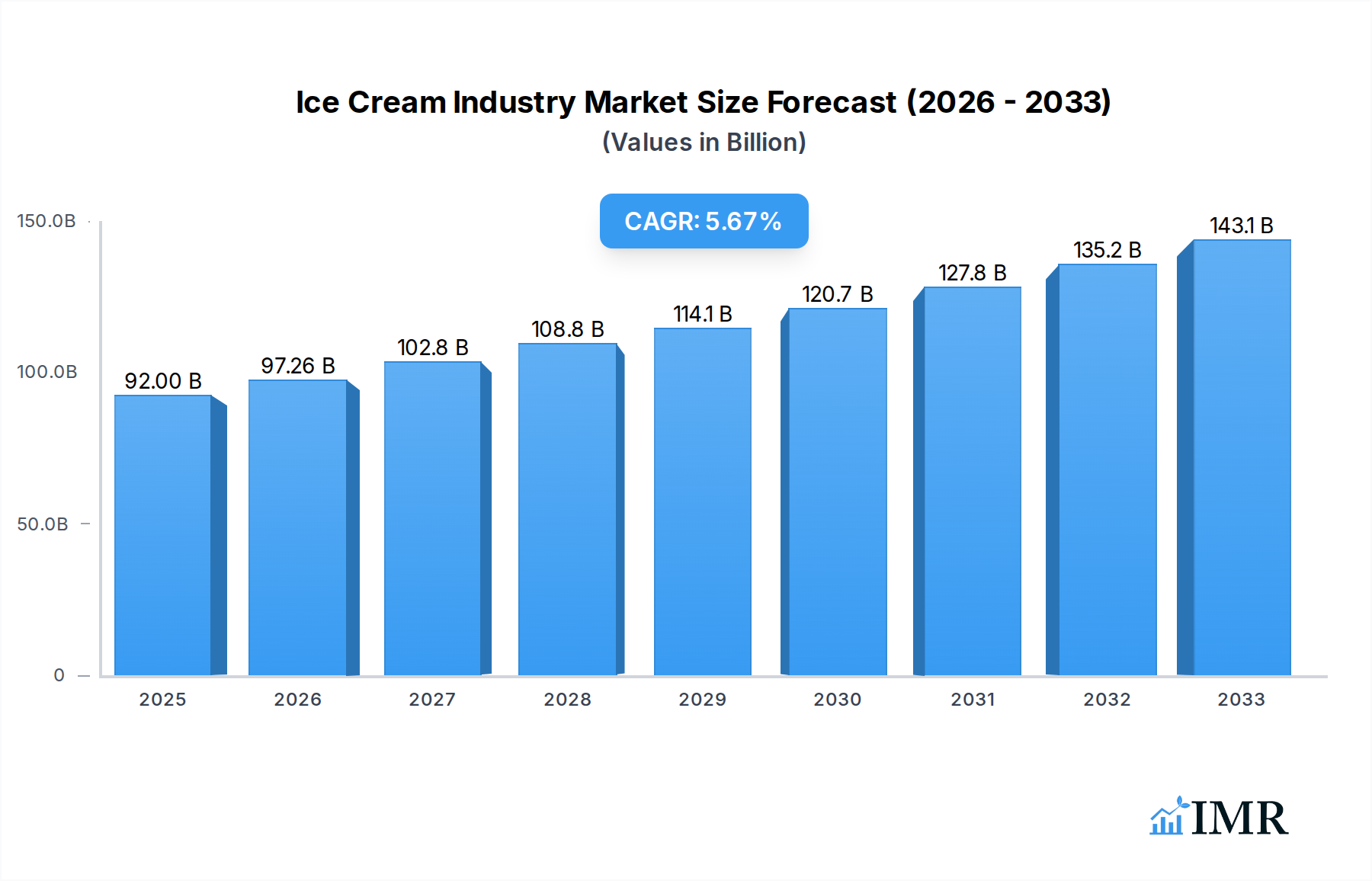

The global Ice Cream Industry is poised for robust growth, projected to reach a substantial USD 92 billion in 2025. Driven by an estimated Compound Annual Growth Rate (CAGR) of 5.7%, the market is expected to expand significantly throughout the forecast period of 2025-2033. This upward trajectory is underpinned by several key drivers, including the increasing demand for premium and artisanal ice cream products, fueled by evolving consumer preferences for unique flavors, high-quality ingredients, and healthier options. The rising disposable incomes in emerging economies, coupled with a growing global population, further contribute to the expanding consumer base for ice cream. Furthermore, innovative product development, such as plant-based and low-sugar ice cream alternatives, is attracting a broader demographic and tapping into new market segments. The convenience of ready-to-eat desserts and the emotional appeal associated with ice cream consumption also play crucial roles in sustaining market momentum.

Ice Cream Industry Market Size (In Billion)

However, the industry faces certain restraints that could temper its growth. Fluctuations in the prices of key raw materials like dairy and sugar can impact profit margins and influence final product pricing, potentially affecting consumer affordability. Intense competition among established global players and the emergence of numerous local brands necessitate continuous innovation and strategic marketing to maintain market share. Moreover, evolving regulatory landscapes concerning food safety and labeling standards across different regions can add to operational complexities and costs. Despite these challenges, the industry's ability to adapt through product diversification, sustainable sourcing practices, and aggressive market penetration strategies, particularly through off-trade channels like online retail and supermarkets, will be critical in realizing its full potential. The expanding reach of e-commerce and the increasing preference for convenient home delivery further bolster the off-trade segment's dominance.

Ice Cream Industry Company Market Share

Ice Cream Industry Report: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This comprehensive report offers an in-depth analysis of the global ice cream market, delving into its dynamic structure, growth trajectories, regional dominance, and evolving product landscape. Spanning the study period of 2019–2033, with a base year of 2025 and a forecast period from 2025–2033, this report provides critical insights for industry professionals, investors, and stakeholders. Leveraging extensive data from the historical period of 2019–2024, we present actionable intelligence on market segmentation, key drivers, challenges, and emerging opportunities.

Ice Cream Industry Market Dynamics & Structure

The global ice cream market exhibits a moderately concentrated structure, characterized by the presence of large multinational corporations alongside regional players. Technological innovation remains a key driver, with ongoing advancements in production efficiency, product formulation, and cold chain logistics significantly impacting market dynamics. Regulatory frameworks, primarily focused on food safety and labeling, present both compliance challenges and opportunities for differentiation. Competitive product substitutes, ranging from frozen yogurt and sorbets to other frozen desserts, necessitate continuous product development and marketing strategies. End-user demographics are increasingly diverse, with a growing demand for healthier options, premium indulgence, and plant-based alternatives. Mergers and Acquisitions (M&A) trends are prevalent, as major companies strategically expand their product portfolios and market reach.

- Market Concentration: Dominated by key players like Nestlé SA, Unilever PLC, and Inner Mongolia Yili Industrial Group Co Ltd, with significant contributions from Wells Enterprises Inc and Dairy Farmers of America Inc.

- Technological Innovation Drivers: Automation in manufacturing, novel ingredient technologies (e.g., plant-based dairy alternatives), and advanced cold chain solutions.

- Regulatory Frameworks: Stringent food safety standards (HACCP, FDA), allergen labeling mandates, and evolving nutritional guidelines.

- Competitive Product Substitutes: Frozen yogurt, gelato, sorbet, dairy-free frozen desserts, and novel frozen confectionery items.

- End-User Demographics: Shifting preferences towards lower sugar, vegan, gluten-free, and artisanal ice cream.

- M&A Trends: Strategic acquisitions to gain market share, access new technologies, and expand into emerging markets.

Ice Cream Industry Growth Trends & Insights

The ice cream industry is poised for robust growth, projected to witness a significant market size evolution driven by evolving consumer preferences and a growing global appetite for indulgence. The ice cream market size is expected to expand considerably, fueled by increasing disposable incomes in emerging economies and a sustained demand for premium and innovative products in developed regions. Adoption rates for both traditional and novel ice cream formats are on an upward trajectory, with online retail channels playing an increasingly crucial role in market penetration. Technological disruptions, particularly in ingredient innovation and sustainable packaging, are reshaping the competitive landscape. Consumer behavior shifts are evident, with a greater emphasis on health and wellness driving demand for reduced-sugar, lower-fat, and plant-based ice cream options, while the desire for premium and unique flavor experiences continues to fuel the indulgence segment. The global ice cream market CAGR is expected to be strong, reflecting these multifaceted growth drivers.

Dominant Regions, Countries, or Segments in Ice Cream Industry

The ice cream industry's growth is significantly propelled by the Off-Trade distribution channel, with Supermarkets and Hypermarkets emerging as the dominant segment. This segment's widespread presence, coupled with a diverse product offering and promotional activities, makes it a primary destination for ice cream purchases. Online Retail is rapidly gaining traction, presenting a significant growth potential due to convenience and the ability to offer specialized and premium products. Convenience Stores also play a vital role in immediate consumption occasions, especially in urban and high-traffic areas.

- Dominant Segment: Off-Trade, specifically Supermarkets and Hypermarkets, holding a substantial market share due to their extensive reach and product variety.

- Key Drivers of Dominance in Supermarkets/Hypermarkets:

- Market Share: Consistently the largest contributor to off-trade sales.

- Consumer Convenience: One-stop shopping experience for groceries and impulse buys like ice cream.

- Promotional Activities: Frequent discounts, loyalty programs, and in-store displays that attract consumers.

- Product Diversity: Ability to stock a wide range of brands, flavors, and sizes, catering to diverse consumer needs.

- Growth Potential in Online Retail:

- Expanding Reach: Overcoming geographical limitations and catering to a wider customer base.

- Niche Offerings: Facilitating the sale of premium, artisanal, and specialized ice cream products.

- Subscription Models: Emerging trend offering recurring purchases and customer loyalty.

- Technological Integration: Enhanced user experience, personalized recommendations, and efficient delivery logistics.

- Role of Convenience Stores: Crucial for impulse purchases and on-the-go consumption, particularly for single-serve options and popular brands.

- Emerging Trends: Integration of direct-to-consumer (DTC) models via online platforms by manufacturers.

Ice Cream Industry Product Landscape

The ice cream industry is characterized by relentless product innovation, driven by evolving consumer palates and a desire for novel sensory experiences. Beyond traditional dairy-based offerings, the market is witnessing a surge in plant-based alternatives, catering to vegan and lactose-intolerant consumers. Premiumization remains a key trend, with gourmet flavors, artisanal ingredients, and unique textures commanding higher price points. Performance metrics are increasingly focused on nutritional profiles, with reduced sugar, lower fat, and added functional ingredients (e.g., probiotics, protein) becoming significant selling propositions. Technological advancements are enabling the creation of smoother textures, richer flavors, and longer shelf-life products, enhancing overall consumer satisfaction and expanding application possibilities, from single-serve novelties to family-sized tubs and intricate dessert components.

Key Drivers, Barriers & Challenges in Ice Cream Industry

The ice cream industry is propelled by several key drivers, including rising disposable incomes globally, the persistent demand for indulgent treats, and continuous product innovation. Technological advancements in production and ingredient sourcing also play a pivotal role. Furthermore, evolving consumer preferences towards healthier options and plant-based alternatives are opening new market segments.

Key challenges facing the ice cream market include volatile raw material costs, particularly for dairy and sugar, and the complex cold chain logistics required for product distribution. Stringent food safety regulations and increasing consumer awareness regarding environmental sustainability also present hurdles. Intense competition from both established players and emerging brands, along with the threat of substitute products, further shapes the market landscape.

Emerging Opportunities in Ice Cream Industry

Emerging opportunities within the ice cream industry lie in the burgeoning demand for plant-based ice cream, offering significant potential for market expansion and innovation. The online retail segment continues to grow, presenting avenues for direct-to-consumer (DTC) models and the sale of niche, premium, and artisanal products. Furthermore, the trend towards functional ice creams, incorporating ingredients like protein or probiotics, appeals to health-conscious consumers. Untapped markets in developing economies, coupled with innovative flavor combinations and unique dessert experiences, represent substantial growth avenues for forward-thinking companies.

Growth Accelerators in the Ice Cream Industry Industry

Long-term growth in the ice cream industry is being significantly accelerated by technological breakthroughs in ingredient formulation, particularly in creating appealing plant-based alternatives that mimic the taste and texture of traditional dairy. Strategic partnerships, such as those focusing on enhanced delivery networks, are crucial for expanding market reach and improving customer accessibility. Market expansion strategies targeting emerging economies, where disposable incomes are rising, are also key growth catalysts. The development of sustainable packaging solutions is becoming increasingly important, aligning with consumer environmental concerns and potentially driving brand loyalty.

Key Players Shaping the Ice Cream Industry Market

- Inner Mongolia Yili Industrial Group Co Ltd

- Nestlé SA

- Wells Enterprises Inc

- Smith Foods Inc

- Unilever PLC

- Lotte Corporation

- Dairy Farmers of America Inc

- Blue Bell Creameries LP

Notable Milestones in Ice Cream Industry Sector

- October 2022: Unilever partnered with ASAP for the delivery of its ice cream products, expanding its virtual storefront reach.

- October 2022: Dairy Farmers of America completed the USD 433 million acquisition of Dean Foods properties, with Kemps replacing Dean Foods throughout Iowa and taking over the Le Mars milk factory for processing.

- October 2022: Blue Ribbon launched three new two-liter tubs for its Street range, featuring two flavors each, including chocolate affair, caramel hokey pokey, and velvety caramel.

In-Depth Ice Cream Industry Market Outlook

The ice cream industry market outlook is exceptionally promising, driven by a confluence of factors poised to shape future growth. Strategic opportunities abound in the continued expansion of plant-based and healthier ice cream alternatives, catering to a growing health-conscious consumer base. The digital landscape offers fertile ground for direct-to-consumer models and e-commerce expansion, enhancing customer accessibility and enabling the promotion of premium and artisanal offerings. Furthermore, penetrating emerging markets with tailored product portfolios and exploring innovative flavor profiles will be critical for sustained market leadership. The industry's ability to adapt to evolving consumer preferences and leverage technological advancements will be paramount in unlocking its full future potential.

Ice Cream Industry Segmentation

-

1. Distribution Channel

-

1.1. Off-Trade

- 1.1.1. Convenience Stores

- 1.1.2. Online Retail

- 1.1.3. Specialist Retailers

- 1.1.4. Supermarkets and Hypermarkets

- 1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 1.2. On-Trade

-

1.1. Off-Trade

Ice Cream Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

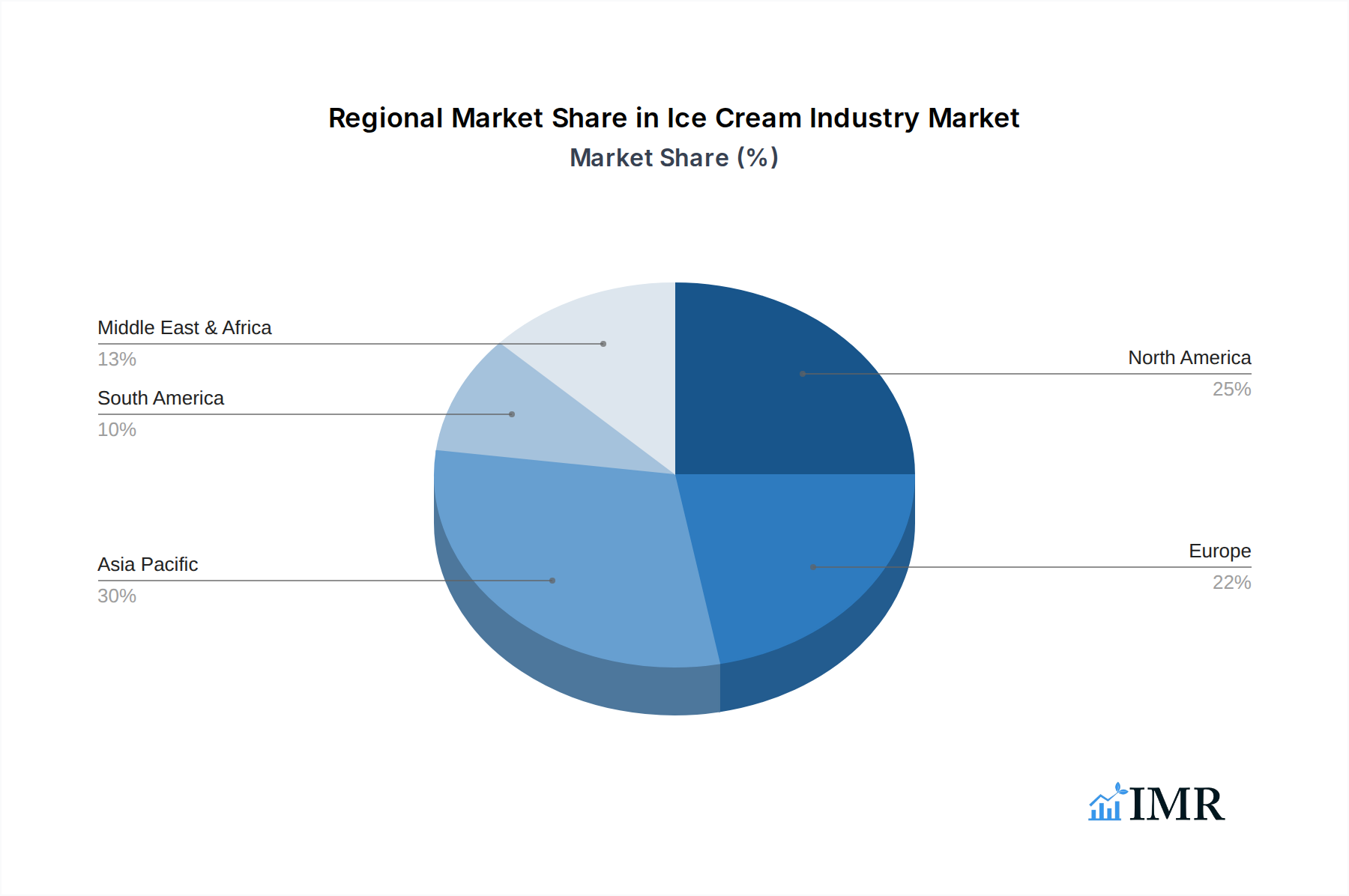

Ice Cream Industry Regional Market Share

Geographic Coverage of Ice Cream Industry

Ice Cream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.1.1. Off-Trade

- 5.1.1.1. Convenience Stores

- 5.1.1.2. Online Retail

- 5.1.1.3. Specialist Retailers

- 5.1.1.4. Supermarkets and Hypermarkets

- 5.1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 5.1.2. On-Trade

- 5.1.1. Off-Trade

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 6. Global Ice Cream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.1.1. Off-Trade

- 6.1.1.1. Convenience Stores

- 6.1.1.2. Online Retail

- 6.1.1.3. Specialist Retailers

- 6.1.1.4. Supermarkets and Hypermarkets

- 6.1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 6.1.2. On-Trade

- 6.1.1. Off-Trade

- 6.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 7. North America Ice Cream Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.1.1. Off-Trade

- 7.1.1.1. Convenience Stores

- 7.1.1.2. Online Retail

- 7.1.1.3. Specialist Retailers

- 7.1.1.4. Supermarkets and Hypermarkets

- 7.1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 7.1.2. On-Trade

- 7.1.1. Off-Trade

- 7.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 8. South America Ice Cream Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.1.1. Off-Trade

- 8.1.1.1. Convenience Stores

- 8.1.1.2. Online Retail

- 8.1.1.3. Specialist Retailers

- 8.1.1.4. Supermarkets and Hypermarkets

- 8.1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 8.1.2. On-Trade

- 8.1.1. Off-Trade

- 8.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 9. Europe Ice Cream Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.1.1. Off-Trade

- 9.1.1.1. Convenience Stores

- 9.1.1.2. Online Retail

- 9.1.1.3. Specialist Retailers

- 9.1.1.4. Supermarkets and Hypermarkets

- 9.1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 9.1.2. On-Trade

- 9.1.1. Off-Trade

- 9.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 10. Middle East & Africa Ice Cream Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.1.1. Off-Trade

- 10.1.1.1. Convenience Stores

- 10.1.1.2. Online Retail

- 10.1.1.3. Specialist Retailers

- 10.1.1.4. Supermarkets and Hypermarkets

- 10.1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 10.1.2. On-Trade

- 10.1.1. Off-Trade

- 10.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 11. Asia Pacific Ice Cream Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.1.1. Off-Trade

- 11.1.1.1. Convenience Stores

- 11.1.1.2. Online Retail

- 11.1.1.3. Specialist Retailers

- 11.1.1.4. Supermarkets and Hypermarkets

- 11.1.1.5. Others (Warehouse clubs, gas stations, etc.)

- 11.1.2. On-Trade

- 11.1.1. Off-Trade

- 11.1. Market Analysis, Insights and Forecast - by Distribution Channel

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Inner Mongolia Yili Industrial Group Co Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Nestlé SA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Wells Enterprises Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Smith Foods Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Unilever PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Lotte Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Dairy Farmers of America Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Blue Bell Creameries LP

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Inner Mongolia Yili Industrial Group Co Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ice Cream Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Ice Cream Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 3: North America Ice Cream Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 4: North America Ice Cream Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Ice Cream Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America Ice Cream Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 7: South America Ice Cream Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 8: South America Ice Cream Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: South America Ice Cream Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Ice Cream Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 11: Europe Ice Cream Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: Europe Ice Cream Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Ice Cream Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa Ice Cream Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 15: Middle East & Africa Ice Cream Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 16: Middle East & Africa Ice Cream Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa Ice Cream Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Ice Cream Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 19: Asia Pacific Ice Cream Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 20: Asia Pacific Ice Cream Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific Ice Cream Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ice Cream Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 2: Global Ice Cream Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Ice Cream Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global Ice Cream Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global Ice Cream Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Global Ice Cream Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global Ice Cream Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 14: Global Ice Cream Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global Ice Cream Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 25: Global Ice Cream Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Ice Cream Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 33: Global Ice Cream Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific Ice Cream Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ice Cream Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Ice Cream Industry?

Key companies in the market include Inner Mongolia Yili Industrial Group Co Ltd, Nestlé SA, Wells Enterprises Inc, Smith Foods Inc, Unilever PLC, Lotte Corporation, Dairy Farmers of America Inc, Blue Bell Creameries LP.

3. What are the main segments of the Ice Cream Industry?

The market segments include Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 92 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Inclination Towards Vegan/Plant-based Protein Sources; Increasing Demand for Functional Protein Beverages.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Competition from Substitute Products.

8. Can you provide examples of recent developments in the market?

October 2022: Unilever partnered with ASAP for the delivery of its ice cream products. As per the partnership, ASAP will also deliver ice cream and treats from Unilever's virtual storefront, The Ice Cream Shop.October 2022: Kemps replaced Dean Goods throughout Iowa as Dairy Farmers of America completed the USD 433 million acquisition of Dean Foods properties. The business took over the Le Mars milk factory, which can process numerous Kemps products, from cottage cheese to ice cream.October 2022: Blue Ribbon's Street range launched three new two-liter tubs, each featuring two flavors. The range includes chocolate affair, caramel hokey pokey, and velvety caramel.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ice Cream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ice Cream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ice Cream Industry?

To stay informed about further developments, trends, and reports in the Ice Cream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence