Key Insights

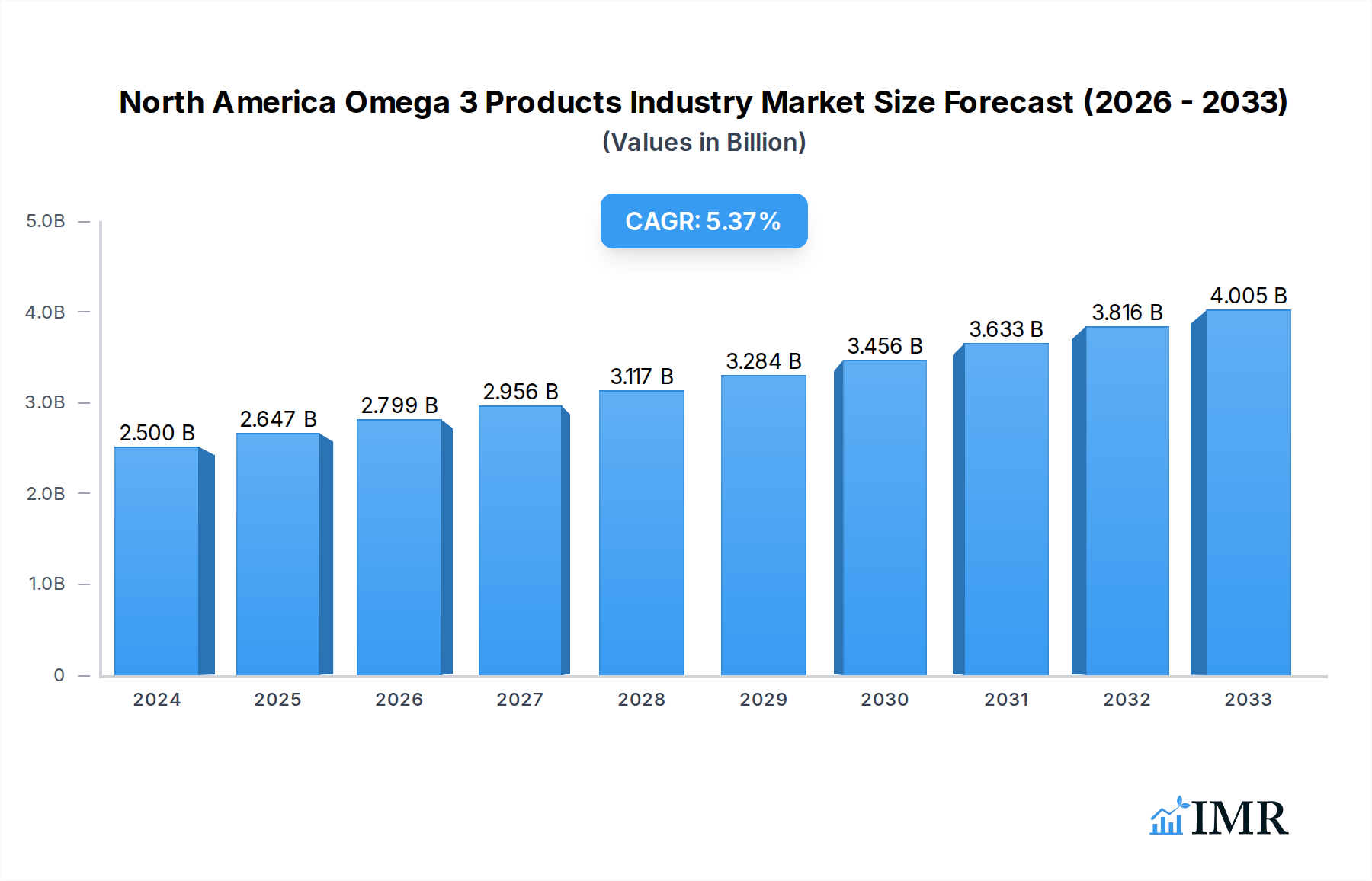

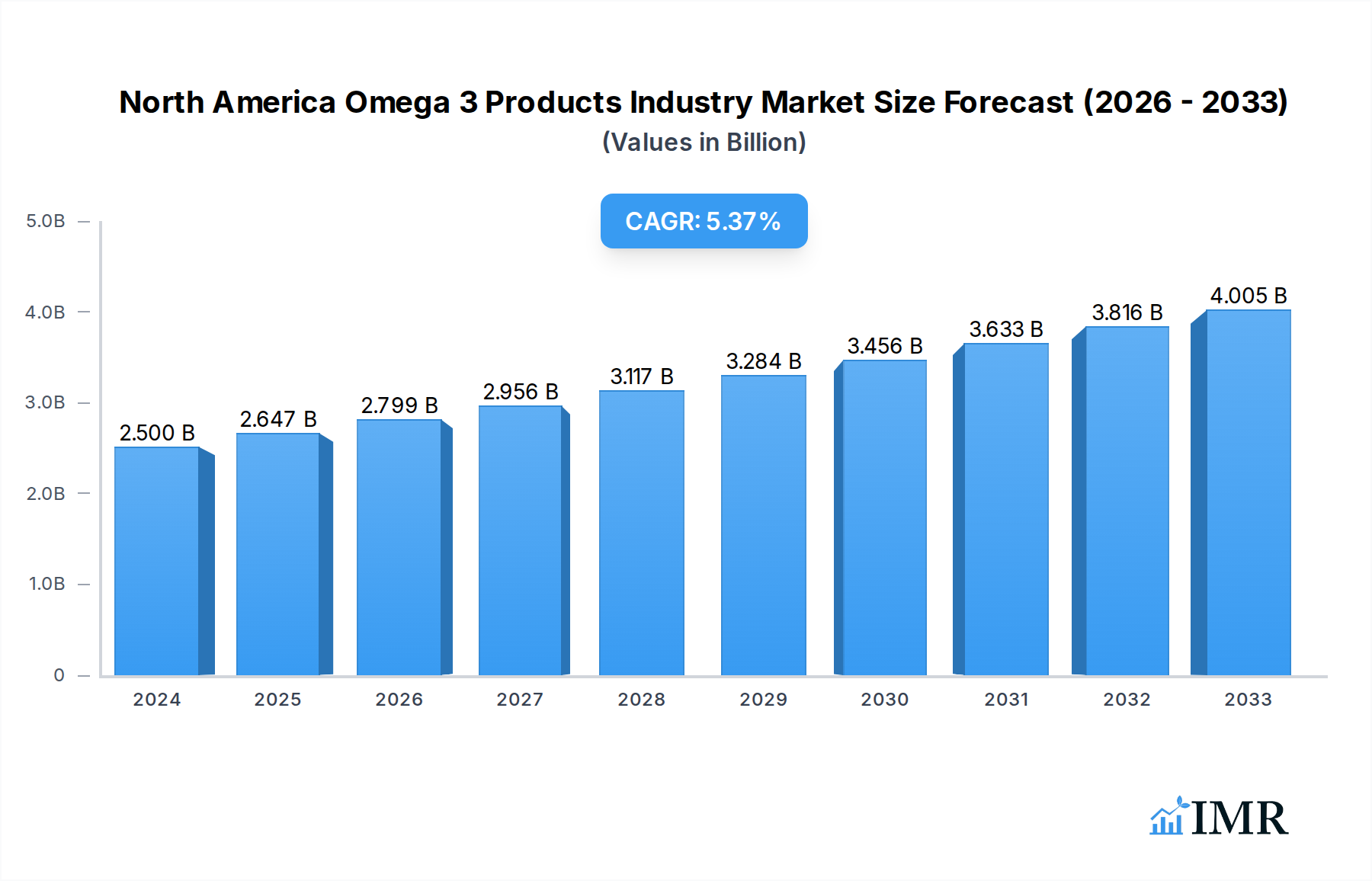

The North America Omega-3 Products Industry is poised for significant expansion, projected to reach an estimated $2.5 billion in 2024 and exhibiting a robust CAGR of 5.9% through 2033. This growth is propelled by a confluence of evolving consumer lifestyles, an increasing awareness of the health benefits associated with omega-3 fatty acids, and a proactive approach towards preventative healthcare. Key drivers include the rising prevalence of chronic diseases, where omega-3s are recognized for their anti-inflammatory properties and cardiovascular support, and the growing demand for dietary supplements as individuals seek to enhance their overall well-being. Furthermore, the burgeoning pet food and feed sector, incorporating omega-3s for animal health and coat condition, represents a substantial growth avenue. The expanding pharmaceutical applications of omega-3s in treating specific medical conditions also contribute significantly to market momentum.

North America Omega 3 Products Industry Market Size (In Billion)

The market landscape is characterized by several key trends that are shaping consumer purchasing decisions and product innovation. The increasing popularity of functional foods and beverages fortified with omega-3s, offering convenient health benefits, is a prominent trend. Alongside this, e-commerce and internet retailing channels are witnessing substantial growth, providing consumers with greater accessibility and a wider selection of omega-3 products. While the market is generally optimistic, certain restraints, such as fluctuating raw material prices for fish oil and potential regulatory hurdles, may present challenges. However, the industry is actively innovating, exploring alternative sources like algal oil to mitigate supply chain concerns and cater to vegetarian and vegan consumers. The North American region, led by the United States, Canada, and Mexico, is expected to remain a dominant force, driven by high disposable incomes and a strong emphasis on health and wellness.

North America Omega 3 Products Industry Company Market Share

North America Omega 3 Products Industry Report: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the North America Omega 3 Products Industry, a rapidly expanding sector driven by increasing health consciousness and diverse product applications. Delving into market dynamics, growth trajectories, regional dominance, product innovations, and strategic opportunities, this report is an indispensable resource for industry stakeholders, investors, and strategic planners. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this analysis leverages extensive data to offer actionable insights into this dynamic market.

North America Omega 3 Products Industry Market Dynamics & Structure

The North America Omega 3 Products Industry exhibits a moderately concentrated market structure, with key players like Reckitt Benckiser Group PLC, Nestle SA, Unilever, Amway Corp, Abbott Laboratories, Herbalife Nutrition, Nutrigold Inc., and GNC dominating significant market shares. Technological innovation is primarily driven by advancements in extraction and purification processes, leading to higher purity and efficacy of Omega 3 compounds, especially EPA and DHA. The regulatory landscape, governed by bodies such as the FDA in the United States and Health Canada, focuses on product safety, labeling accuracy, and health claims, influencing product development and market entry. Competitive product substitutes include other dietary supplements and functional foods offering perceived health benefits, though the scientifically validated advantages of Omega 3s provide a strong competitive edge. End-user demographics are broad, encompassing health-conscious individuals across age groups, pregnant women, athletes, and parents seeking nutritional benefits for their children. Mergers and acquisitions (M&A) trends indicate consolidation and strategic expansion by larger corporations seeking to broaden their product portfolios and market reach within the Omega 3 space. For instance, the market witnessed approximately 20 M&A deals within the historical period, with deal values ranging from $10 million to $250 million, indicating a healthy appetite for strategic acquisitions. Barriers to innovation include high R&D costs for novel delivery systems and stringent regulatory approvals for therapeutic claims, but ongoing research into new applications, such as cognitive health and cardiovascular disease prevention, continues to propel the market forward.

North America Omega 3 Products Industry Growth Trends & Insights

The North America Omega 3 Products Industry is poised for robust growth, projected to reach approximately $18.5 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 7.2% from the base year of 2025. This growth is underpinned by a substantial increase in consumer awareness regarding the myriad health benefits associated with Omega 3 fatty acids, particularly EPA and DHA. These benefits, ranging from cardiovascular health and cognitive function to anti-inflammatory properties, are increasingly supported by scientific research and public health campaigns, leading to higher adoption rates across various age demographics. The market penetration of Omega 3 products, especially in dietary supplements, has reached an estimated 45% of the health-conscious adult population in the United States and Canada. Technological disruptions are playing a crucial role, with innovations in microencapsulation and targeted delivery systems enhancing bioavailability and palatability, thereby improving consumer experience and product efficacy. Furthermore, the rise of plant-based Omega 3 alternatives derived from algae is catering to a growing vegan and vegetarian consumer base, expanding the addressable market significantly. Consumer behavior shifts are evident in the increasing demand for premium, sustainably sourced, and transparently manufactured Omega 3 products. Consumers are actively seeking products with third-party certifications for purity and potency. The functional food segment is experiencing accelerated growth as manufacturers integrate Omega 3s into everyday food items like yogurts, cereals, and beverages, making nutritional benefits more accessible. The infant nutrition segment is also a key growth driver, with a rising emphasis on early childhood development and brain health, fueling demand for DHA-enriched formulas. The pharmaceutical segment, while smaller, is expected to grow with the development of prescription Omega 3 medications for specific medical conditions. The online retail channel is emerging as a dominant distribution point, offering convenience and wider product selection to consumers, contributing an estimated 35% of total sales by 2028. The overall market evolution is characterized by a sustained upward trajectory, driven by a confluence of health imperatives, scientific validation, and innovative product development, projected to contribute significantly to the global health and wellness market.

Dominant Regions, Countries, or Segments in North America Omega 3 Products Industry

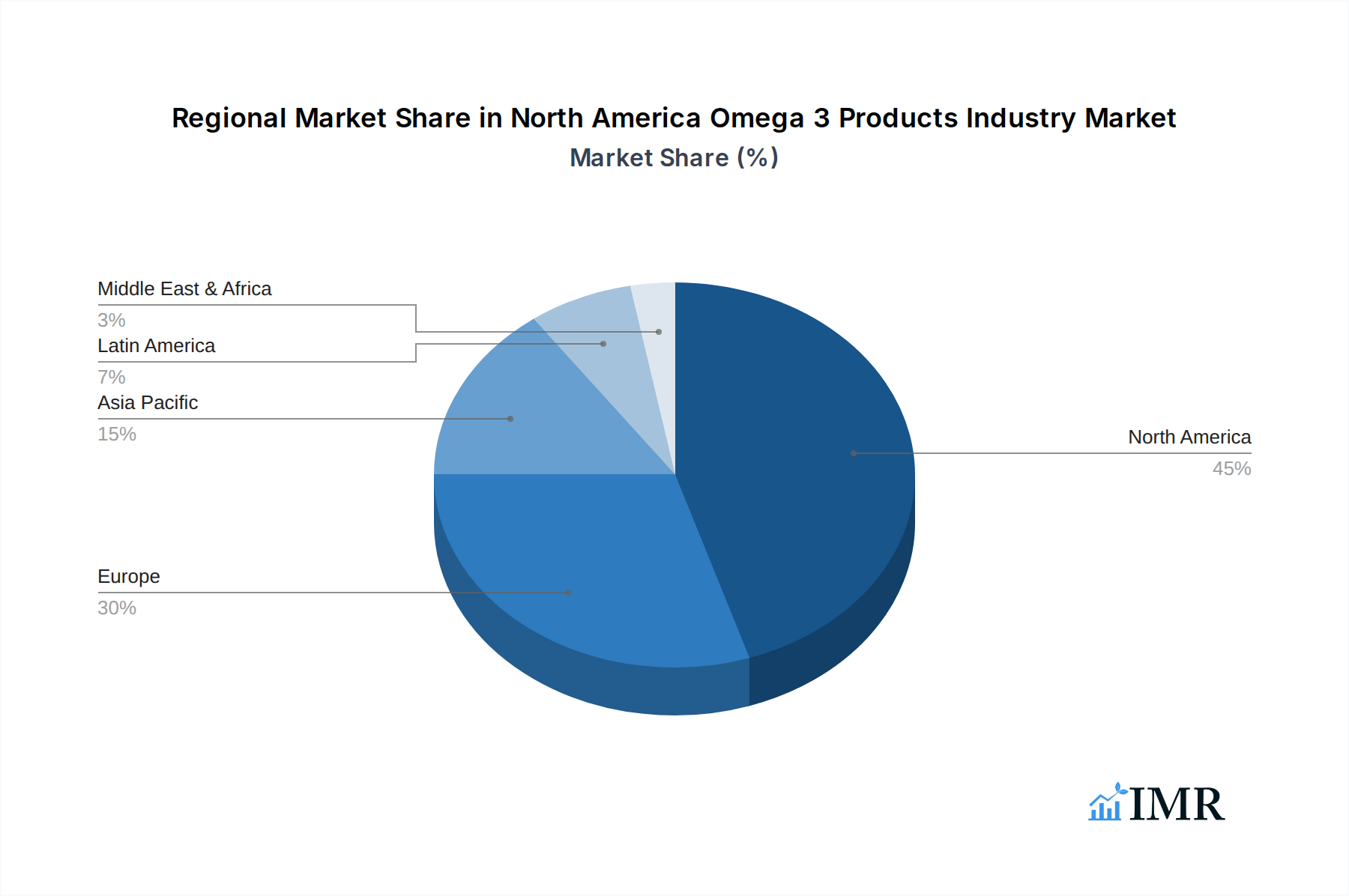

Within the North America Omega 3 Products Industry, the United States stands out as the dominant region, accounting for an estimated 75% of the total market revenue in 2025, projected to reach approximately $13.8 billion. This dominance is fueled by a combination of factors: a highly health-conscious consumer base, robust research and development infrastructure, a well-established pharmaceutical and dietary supplement industry, and significant disposable income allocated towards health and wellness products. The strong presence of key players like Abbott Laboratories, Amway Corp, and Nutrigold Inc. in the U.S. market further solidifies its leadership position. Economic policies favoring innovation and consumer protection, coupled with extensive public health awareness campaigns highlighting the benefits of Omega 3s, contribute significantly to market growth.

In terms of Product Type, Dietary Supplements is the leading segment, representing an estimated 55% of the North America market share, projected at $10.1 billion in 2025. This segment's strength lies in its direct appeal to consumers seeking targeted health benefits, with a wide array of formulations, dosages, and ingredient sources available. The perceived efficacy and convenience of capsule or softgel forms make them a preferred choice for daily supplementation.

Analyzing Distribution Channels, Internet Retailing is emerging as a powerful growth driver, projected to capture 35% of the market by 2028, with an estimated value of $6.4 billion in 2025. The convenience of online purchasing, the availability of a broader product selection, competitive pricing, and direct-to-consumer models are propelling its ascendancy.

Key drivers for the dominance of the United States include:

- High Consumer Spending on Health & Wellness: An estimated 60% of American households regularly purchase dietary supplements.

- Advanced Research & Development: Significant investment in scientific research validates and expands the applications of Omega 3s.

- Strong Regulatory Framework: While stringent, it fosters consumer trust and product quality.

The Dietary Supplements segment's dominance is attributed to:

- Targeted Health Benefits: Consumers actively seek Omega 3s for cardiovascular health, brain function, and joint support.

- Product Versatility: Wide range of formulations (EPA, DHA, ALA) and delivery forms (capsules, liquids).

- Effective Marketing and Endorsements: Influencer marketing and celebrity endorsements amplify product appeal.

The rise of Internet Retailing is driven by:

- E-commerce Penetration: High internet and smartphone adoption rates in North America.

- Consumer Convenience: 24/7 accessibility and home delivery options.

- Price Competitiveness: Online platforms often offer better pricing and promotional deals.

North America Omega 3 Products Industry Product Landscape

The North America Omega 3 Products Industry is characterized by continuous product innovation focused on enhancing bioavailability, palatability, and targeted delivery. Key innovations include the development of microencapsulated Omega 3s that mask unpleasant flavors and improve stability, as well as the growing availability of vegan Omega 3 supplements derived from algae, catering to a broader consumer base. Furthermore, advancements in purification techniques ensure higher purity levels of EPA and DHA, minimizing contaminants like heavy metals and PCBs. Applications are expanding beyond traditional supplements to include functional foods like fortified beverages, dairy products, and baked goods, as well as specialized infant formulas designed to support cognitive development. Performance metrics such as higher EPA/DHA concentrations, improved absorption rates, and targeted release mechanisms are becoming key differentiators in a competitive market.

Key Drivers, Barriers & Challenges in North America Omega 3 Products Industry

Key Drivers:

- Growing Health and Wellness Consciousness: Increasing consumer awareness of Omega 3s' benefits for heart health, brain function, and inflammation management is a primary growth driver.

- Scientifically Validated Benefits: Robust scientific research supporting the efficacy of EPA and DHA continues to fuel demand.

- Product Diversification: Expansion into functional foods, infant nutrition, and pet food broadens market reach.

- Technological Advancements: Innovations in extraction, purification, and delivery systems enhance product quality and consumer experience.

- Aging Population: Increased prevalence of age-related health concerns drives demand for preventive nutritional solutions.

Barriers & Challenges:

- Supply Chain Volatility: Reliance on fish oil sources can lead to price fluctuations and sustainability concerns. The industry is projected to face a potential 10-15% increase in raw material costs for fish oil within the next two years.

- Regulatory Scrutiny: Stringent regulations on health claims and product labeling can pose challenges for market entry and product innovation.

- Consumer Education Gaps: Misconceptions about different types of Omega 3s (ALA vs. EPA/DHA) and their sources persist, requiring ongoing education efforts.

- Competition from Substitutes: Other supplements and fortified foods offering perceived health benefits present indirect competition.

- Cost Sensitivity: While demand is high, price sensitivity can be a barrier for some consumer segments, particularly for premium products.

Emerging Opportunities in North America Omega 3 Products Industry

Emerging opportunities in the North America Omega 3 Products Industry lie in the development of novel delivery systems for enhanced bioavailability, such as liposomal formulations and chewable gummies with improved taste profiles. The burgeoning demand for sustainable and traceable Omega 3 sources, particularly from algae and krill, presents a significant untapped market. Expanding into specialized nutritional segments like cognitive health for athletes and seniors, and mental wellness support, offers substantial growth potential. Furthermore, the increasing adoption of Omega 3 fortified pet food and feed is a rapidly growing niche. Collaborations with healthcare professionals to promote Omega 3 supplementation for specific medical conditions also represent a promising avenue. The market for personalized nutrition plans incorporating Omega 3s is also poised for rapid expansion.

Growth Accelerators in the North America Omega 3 Products Industry Industry

Several key catalysts are accelerating the long-term growth of the North America Omega 3 Products Industry. Technological breakthroughs in sustainable sourcing and efficient extraction of Omega 3s from non-traditional sources like algae and genetically modified crops are reducing reliance on finite marine resources and mitigating price volatility. Strategic partnerships between supplement manufacturers, food and beverage companies, and pharmaceutical firms are fostering product innovation and wider market penetration. For instance, the recent integration of Omega 3s into plant-based dairy alternatives by major food manufacturers signifies a strategic move to capture a larger consumer segment. Furthermore, market expansion strategies targeting emerging demographics, such as active seniors and millennials seeking preventative health solutions, are driving sustained demand. The development of scientifically validated therapeutic applications for Omega 3s in managing chronic diseases is also a significant growth accelerator, paving the way for prescription-grade Omega 3 products.

Key Players Shaping the North America Omega 3 Products Industry Market

- Reckitt Benckiser Group PLC

- Nestle SA

- Unilever

- Amway Corp

- Abbott Laboratories

- Herbalife Nutrition

- Nutrigold Inc.

- GNC

Notable Milestones in North America Omega 3 Products Industry Sector

- 2019: Increased research publications highlighting Omega 3s' role in cardiovascular health and cognitive function, boosting consumer interest.

- 2020: Launch of several algae-based Omega 3 supplements catering to the growing vegan population.

- 2021: Significant increase in online sales of Omega 3 products due to pandemic-driven health awareness and e-commerce growth.

- 2022: FDA approval for enhanced labeling regulations, allowing for more specific health claims on Omega 3 products.

- 2023: Major food corporations announce plans to fortify a wider range of consumer products with Omega 3 fatty acids.

- 2024: Introduction of novel Omega 3 delivery systems, such as flavored gummies with improved palatability and efficacy.

In-Depth North America Omega 3 Products Industry Market Outlook

The future outlook for the North America Omega 3 Products Industry is exceptionally bright, propelled by sustained consumer demand for health and wellness solutions. Growth accelerators such as ongoing scientific validation of Omega 3 benefits, particularly in areas of brain health and preventative medicine, will continue to fuel market expansion. Innovations in sustainable sourcing and product formulation, including plant-based alternatives and advanced delivery mechanisms, will broaden market appeal and cater to diverse consumer preferences. Strategic collaborations and market expansion into niche applications like personalized nutrition and specialized pet care are expected to unlock new revenue streams. The increasing focus on proactive health management and the aging demographic will ensure a consistent demand for Omega 3 products, positioning the industry for substantial and sustained growth in the coming years. The market is anticipated to not only meet existing needs but also to pioneer new avenues in therapeutic nutrition.

North America Omega 3 Products Industry Segmentation

-

1. Product Type

- 1.1. Functional Food

- 1.2. Dietary Supplements

- 1.3. Infant Nutrition

- 1.4. Pet Food and Feed

- 1.5. Pharmaceuticals

-

2. Distribution Channel

- 2.1. Grocery Retailers

- 2.2. Pharmacies and Health Stores

- 2.3. Internet Retailing

- 2.4. Other Distribution Channels

-

3. Geography

-

3.1. North America

- 3.1.1. United States

- 3.1.2. Canada

- 3.1.3. Mexico

- 3.1.4. Rest of North America

-

3.1. North America

North America Omega 3 Products Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

North America Omega 3 Products Industry Regional Market Share

Geographic Coverage of North America Omega 3 Products Industry

North America Omega 3 Products Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Functional Food

- 5.1.2. Dietary Supplements

- 5.1.3. Infant Nutrition

- 5.1.4. Pet Food and Feed

- 5.1.5. Pharmaceuticals

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Grocery Retailers

- 5.2.2. Pharmacies and Health Stores

- 5.2.3. Internet Retailing

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. North America

- 5.3.1.1. United States

- 5.3.1.2. Canada

- 5.3.1.3. Mexico

- 5.3.1.4. Rest of North America

- 5.3.1. North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. North America Omega 3 Products Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Functional Food

- 6.1.2. Dietary Supplements

- 6.1.3. Infant Nutrition

- 6.1.4. Pet Food and Feed

- 6.1.5. Pharmaceuticals

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Grocery Retailers

- 6.2.2. Pharmacies and Health Stores

- 6.2.3. Internet Retailing

- 6.2.4. Other Distribution Channels

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. North America

- 6.3.1.1. United States

- 6.3.1.2. Canada

- 6.3.1.3. Mexico

- 6.3.1.4. Rest of North America

- 6.3.1. North America

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Reckitt Benckiser Group PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Nestle SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Unilever

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Amway Corp

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Abbott Laboratories

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Herbalife Nutrition

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nutrigold Inc.

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 GNC

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Reckitt Benckiser Group PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Omega 3 Products Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Omega 3 Products Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Omega 3 Products Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: North America Omega 3 Products Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: North America Omega 3 Products Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: North America Omega 3 Products Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Omega 3 Products Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: North America Omega 3 Products Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 7: North America Omega 3 Products Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: North America Omega 3 Products Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States North America Omega 3 Products Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Omega 3 Products Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Omega 3 Products Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of North America North America Omega 3 Products Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Omega 3 Products Industry?

The projected CAGR is approximately 5.9%.

2. Which companies are prominent players in the North America Omega 3 Products Industry?

Key companies in the market include Reckitt Benckiser Group PLC, Nestle SA, Unilever, Amway Corp, Abbott Laboratories, Herbalife Nutrition, Nutrigold Inc., GNC.

3. What are the main segments of the North America Omega 3 Products Industry?

The market segments include Product Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing awareness of the health benefits of Omega-3 fatty acids; Rising Prevalence of Chronic Diseases.

6. What are the notable trends driving market growth?

Growing interest in plant-based diets and veganism is driving demand for plant-derived Omega-3 sources.

7. Are there any restraints impacting market growth?

Omega-3 supplements can be expensive compared to other nutritional products.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Omega 3 Products Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Omega 3 Products Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Omega 3 Products Industry?

To stay informed about further developments, trends, and reports in the North America Omega 3 Products Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence