Key Insights

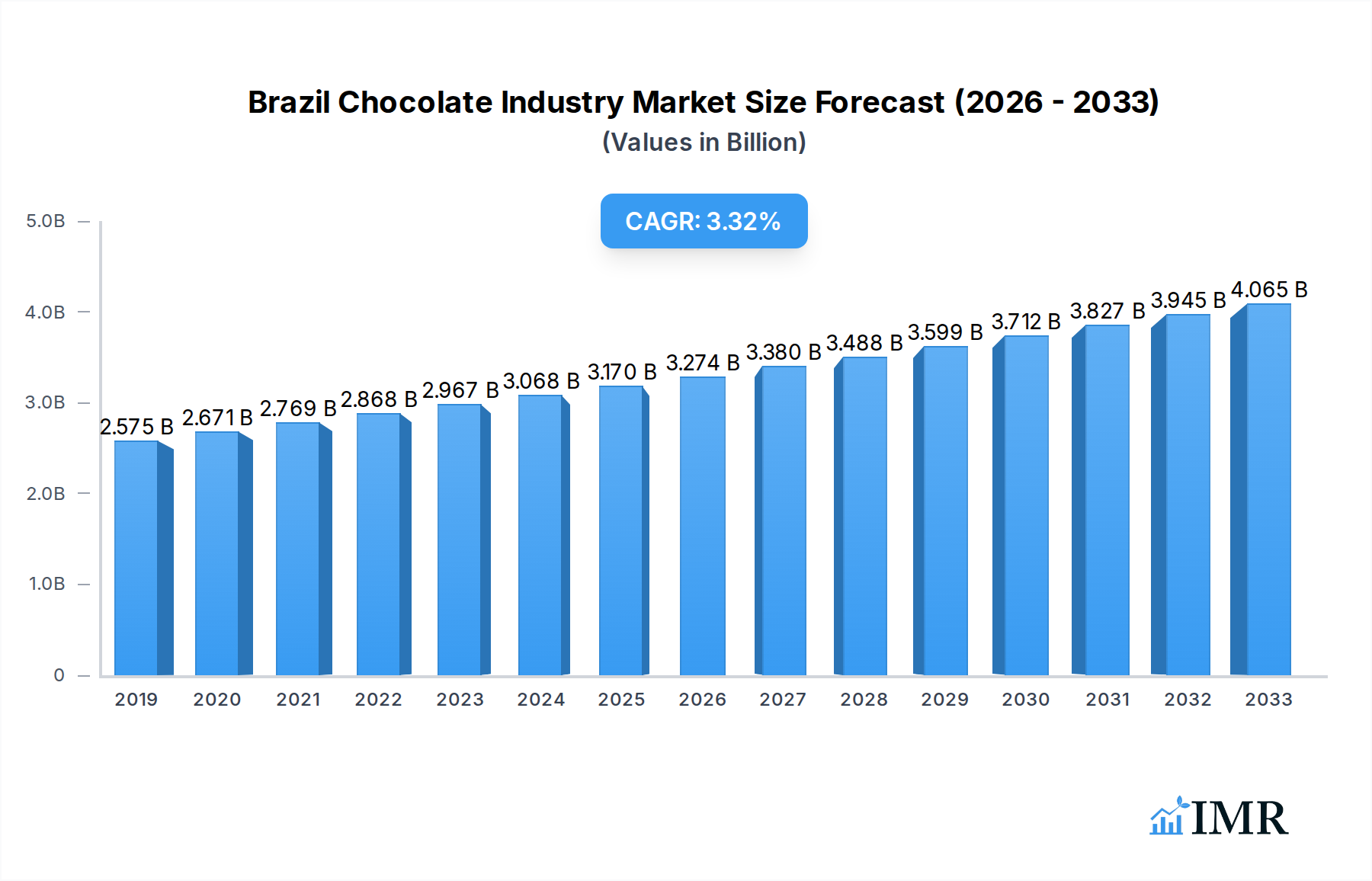

The Brazil Chocolate Industry is poised for significant growth, with a projected market size of $3 billion in 2025, expanding at a robust Compound Annual Growth Rate (CAGR) of 3.84% through 2033. This expansion is primarily driven by a confluence of factors, including a growing middle class with increased disposable income, a rising consumer preference for premium and artisanal chocolate products, and the expanding influence of online retail channels. The demand for dark chocolate, in particular, is surging, fueled by increasing consumer awareness of its perceived health benefits. Furthermore, the convenience store and online retail segments are witnessing a substantial uptick, catering to the evolving purchasing habits of Brazilian consumers who seek both accessibility and variety. Companies are strategically leveraging these trends by introducing innovative product formulations and expanding their distribution networks to capture a larger market share.

Brazil Chocolate Industry Market Size (In Billion)

While the market demonstrates strong upward momentum, certain restraints are present. These include fluctuations in raw material prices, particularly cocoa, which can impact production costs and profit margins for manufacturers. Intense competition among both domestic and international players also presents a challenge, necessitating continuous product innovation and aggressive marketing strategies. Despite these hurdles, the overall outlook for the Brazil Chocolate Industry remains exceptionally positive. The continuous innovation in product offerings, coupled with a strong emphasis on premiumization and the increasing adoption of digital sales platforms, are expected to propel the industry forward, creating significant opportunities for stakeholders. The market is characterized by a diverse range of segments, from traditional milk and white chocolates to the increasingly popular dark variants, all distributed through a blend of established channels like supermarkets and evolving platforms like e-commerce.

Brazil Chocolate Industry Company Market Share

Brazil Chocolate Industry Market Analysis Report: Growth, Trends, and Opportunities (2019-2033)

This comprehensive report provides an in-depth analysis of the Brazil Chocolate Industry, offering critical insights into market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, opportunities, and the strategic moves of major players. With a study period from 2019 to 2033, this report leverages the base year of 2025 and a forecast period extending to 2033 to deliver actionable intelligence for stakeholders. Covering both parent and child markets, this analysis is designed to maximize search engine visibility and engage industry professionals.

Brazil Chocolate Industry Market Dynamics & Structure

The Brazil Chocolate Industry exhibits a dynamic market structure influenced by a blend of global giants and strong local players. Market concentration is moderate, with key companies like Nestlé SA, Mondelēz International Inc, and Mars Incorporated holding significant shares, particularly in the mass-market confectionery segment. However, the rise of premium and artisanal chocolate brands such as Nugali Chocolates and Dengo Chocolates SA indicates a growing niche market and increased competition. Technological innovation is driven by the demand for healthier options, sustainable sourcing, and unique flavor profiles. Regulatory frameworks, primarily concerning food safety, labeling, and import/export, play a crucial role in shaping market entry and operational strategies. Competitive product substitutes include other confectionery items and snack options, requiring chocolate manufacturers to continually innovate and differentiate. End-user demographics are shifting, with an increasing preference for premium, ethically sourced, and indulgent chocolate experiences among urban populations, while affordability remains a key factor for a broader consumer base. Mergers and acquisitions (M&A) trends are evident, exemplified by Ferrero's expansion into the Brazilian market through acquisitions, indicating strategic consolidation and market penetration efforts.

- Market Concentration: Moderate, with a mix of multinational corporations and specialized artisanal producers.

- Technological Innovation: Focus on health-conscious products (e.g., sugar-free, dark chocolate with high cocoa content), sustainable sourcing, and novel flavor infusions.

- Regulatory Framework: Strict adherence to ANVISA regulations for food safety, quality, and labeling.

- Competitive Substitutes: Other snack categories, biscuits, and sugar-based confectionery.

- End-User Demographics: Growing demand for premium and ethically sourced chocolate among affluent urban consumers, alongside a large price-sensitive market.

- M&A Trends: Strategic acquisitions to expand product portfolios and market reach, especially in the confectionery segment.

Brazil Chocolate Industry Growth Trends & Insights

The Brazil Chocolate Industry is poised for significant growth, projected to reach xx billion by 2033. Driven by a burgeoning middle class, increasing disposable incomes, and a strong cultural appreciation for confectionery, the market has witnessed robust expansion throughout the historical period of 2019-2024. The estimated market size in the base year of 2025 stands at xx billion, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025-2033. Adoption rates for both mass-market and premium chocolate segments are on an upward trajectory. Technological disruptions, such as advancements in cocoa processing, ingredient innovation (e.g., plant-based alternatives), and sophisticated packaging solutions, are enhancing product appeal and shelf-life. Consumer behavior shifts are profoundly influencing the market. There's a discernible move towards premiumization, with consumers willing to spend more on higher-quality chocolate that offers unique flavor experiences and ethical sourcing credentials. The demand for dark chocolate, driven by perceived health benefits and sophisticated taste profiles, is rising. Simultaneously, the convenience of ready-to-eat and on-the-go chocolate formats continues to resonate with busy urban lifestyles. Online retail channels are gaining prominence, offering greater accessibility and a wider selection of products, complementing traditional distribution networks. Sustainability and traceability are becoming increasingly important purchasing considerations, pushing manufacturers to adopt more responsible sourcing practices. The influence of social media and digital marketing is also playing a vital role in shaping consumer preferences and driving brand awareness, particularly for newer, artisanal brands.

Dominant Regions, Countries, or Segments in Brazil Chocolate Industry

The Confectionery segment, particularly within the Milk and White Chocolate variant, is a dominant force driving growth in the Brazil Chocolate Industry. This dominance stems from its broad appeal across diverse consumer demographics and its prevalent presence in everyday consumption patterns. Supermarkets and hypermarkets remain the primary distribution channels, accounting for a substantial market share due to their extensive reach and the convenience they offer to a large consumer base. The economic policies supporting domestic agriculture and food processing, coupled with robust infrastructure development in key urban centers, further bolster the accessibility and sales of these widely consumed chocolate types.

- Confectionery Variant (Dominant): Milk and White Chocolate: These variants cater to a wider palate and are integral to celebratory occasions and daily snacking. Their production efficiency and market penetration capabilities ensure widespread availability and strong sales volumes.

- Distribution Channel (Dominant): Supermarket/Hypermarket: These retail giants offer a one-stop shopping experience, making them the preferred channel for everyday grocery purchases, including chocolate. Their strategic locations and promotional activities significantly influence consumer buying decisions.

- Market Share & Growth Potential: Milk and white chocolates, sold primarily through supermarkets, collectively hold an estimated xx% market share in 2025, with an anticipated CAGR of xx% through 2033. Their growth is propelled by consistent demand and the ability of major manufacturers to produce them at scale.

- Key Drivers:

- Affordability and Accessibility: Mass production ensures competitive pricing, making them accessible to a broad economic spectrum.

- Established Consumer Habits: Traditional consumption patterns heavily favor milk and white chocolate for gifting and personal consumption.

- Product Innovation within Variants: Continuous introduction of new flavors and formats within milk and white chocolate keeps them relevant and appealing.

- Extensive Retail Network: The ubiquitous presence of supermarkets and hypermarkets ensures these products are readily available across the country.

While dark chocolate is experiencing a notable growth spurt due to health consciousness and premiumization trends, and online retail is expanding rapidly, the sheer volume and established market presence of milk and white chocolates through traditional retail channels solidify their position as the current drivers of the Brazil Chocolate Industry.

Brazil Chocolate Industry Product Landscape

The Brazil Chocolate Industry is characterized by a diverse and evolving product landscape, increasingly focusing on premiumization and niche offerings. Innovations range from enhanced cocoa content and exotic flavor infusions to sustainable sourcing and artisanal crafting techniques. Performance metrics are influenced by consumer perception of quality, ethical sourcing, and unique taste experiences. Companies are differentiating through distinctive formulations, such as single-origin chocolates and bean-to-bar creations. Technological advancements in processing are enabling finer textures and more intense flavor profiles. The application of chocolate extends beyond traditional confectionery to gourmet desserts, functional foods, and beverages, creating new avenues for product development and market penetration.

Key Drivers, Barriers & Challenges in Brazil Chocolate Industry

The Brazil Chocolate Industry is propelled by several key drivers, including a growing middle class with increasing disposable income, a strong cultural affinity for chocolate, and a rising demand for premium and artisanal products. Technological advancements in cocoa cultivation and processing, coupled with the industry's focus on sustainability and ethical sourcing, are also significant growth accelerators. The expansion of online retail channels further enhances accessibility and market reach.

Key challenges and restraints include the volatility of cocoa prices due to weather patterns and global supply dynamics, impacting raw material costs significantly, estimated to affect profit margins by xx% in volatile periods. Supply chain inefficiencies, particularly in remote cocoa-producing regions, can lead to logistical hurdles and increased operational costs. Intense competition from both domestic and international players, coupled with the threat of substitute products, requires continuous innovation and competitive pricing strategies. Regulatory complexities and trade policies can also pose barriers to entry and expansion.

Emerging Opportunities in Brazil Chocolate Industry

Emerging opportunities in the Brazil Chocolate Industry lie in the growing demand for plant-based and vegan chocolate options, catering to an increasingly health-conscious and ethically aware consumer base. The expansion of the premium and artisanal chocolate market presents significant potential for niche producers focusing on single-origin beans and unique flavor profiles. Furthermore, exploring functional chocolate applications, such as those fortified with vitamins or probiotics, taps into the wellness trend. The untapped potential in smaller cities and rural areas, alongside the continued growth of e-commerce, offers avenues for market penetration and increased sales.

Growth Accelerators in the Brazil Chocolate Industry Industry

Growth accelerators in the Brazil Chocolate Industry are multifaceted, driven by strategic initiatives and evolving consumer preferences. The increasing emphasis on sustainable and ethically sourced cocoa is not only meeting consumer demand but also fostering stronger relationships with farmers, ensuring a more stable supply chain. Technological breakthroughs in processing and product development are leading to the creation of innovative chocolate varieties, including sugar-free and low-calorie options, catering to health-conscious consumers. Strategic partnerships between ingredient suppliers, manufacturers, and retailers are enhancing distribution networks and market penetration. Furthermore, government support for the agricultural sector and the promotion of Brazilian cocoa on a global scale are crucial in driving sustained growth.

Key Players Shaping the Brazil Chocolate Industry Market

- Nestlé SA

- Nugali Chocolates

- Chocoladefabriken Lindt & Sprüngli AG

- Cacau Show

- Ferrero International SA

- Florestal Alimentos SA

- Mars Incorporated

- Arcor S A I C

- Dori Alimentos SA

- Dengo Chocolates SA

- Fuji Oil Holdings Inc

- Mondelēz International Inc

- The Peccin S

- The Hershey Company

Notable Milestones in Brazil Chocolate Industry Sector

- July 2023: Ferrero's sister company, Ferrara Candy Co., announced the acquisition of Brazilian snacks company Dori Alimentos, significantly expanding its footprint in the Brazilian confectionery market.

- July 2023: Ferrara Candy Company, a Ferrero-related entity, finalized an agreement to acquire Dori Alimentos, a strategic move to bolster its presence in Brazil's fast-growing confectionery sector.

- December 2022: Mars Incorporated launched its limited edition Snickers Caramelo & Bacon chocolate bars in Brazil, showcasing product innovation and targeted market offerings.

In-Depth Brazil Chocolate Industry Market Outlook

The Brazil Chocolate Industry is set for robust future growth, fueled by a confluence of factors including evolving consumer preferences towards premium and healthy options, alongside the consistent demand for traditional confectionery. Strategic investments in sustainable sourcing and technological innovation will be pivotal in differentiating brands and capturing market share. The continued expansion of e-commerce and the increasing popularity of artisanal chocolate producers present significant untapped market potential. Furthermore, a focus on export markets and the promotion of Brazil's unique cocoa varieties can further accelerate industry growth. The interplay of these elements paints a promising outlook for a dynamic and expanding Brazil Chocolate Industry.

Brazil Chocolate Industry Segmentation

-

1. Confectionery Variant

- 1.1. Dark Chocolate

- 1.2. Milk and White Chocolate

-

2. Distribution Channel

- 2.1. Convenience Store

- 2.2. Online Retail Store

- 2.3. Supermarket/Hypermarket

- 2.4. Others

Brazil Chocolate Industry Segmentation By Geography

- 1. Brazil

Brazil Chocolate Industry Regional Market Share

Geographic Coverage of Brazil Chocolate Industry

Brazil Chocolate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.84% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 5.1.1. Dark Chocolate

- 5.1.2. Milk and White Chocolate

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Store

- 5.2.2. Online Retail Store

- 5.2.3. Supermarket/Hypermarket

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Brazil

- 5.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 6. Brazil Chocolate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 6.1.1. Dark Chocolate

- 6.1.2. Milk and White Chocolate

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Convenience Store

- 6.2.2. Online Retail Store

- 6.2.3. Supermarket/Hypermarket

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Nestlé SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Nugali Chocolates

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Chocoladefabriken Lindt & Sprüngli AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Cacau Show

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ferrero International SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Florestal Alimentos SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mars Incorporated

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Arcor S A I C

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Dori Alimentos SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Dengo Chocolates SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Fuji Oil Holdings Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Mondelēz International Inc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 The Peccin S

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 The Hershey Company

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 Nestlé SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Brazil Chocolate Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Brazil Chocolate Industry Share (%) by Company 2025

List of Tables

- Table 1: Brazil Chocolate Industry Revenue billion Forecast, by Confectionery Variant 2020 & 2033

- Table 2: Brazil Chocolate Industry Volume K Tons Forecast, by Confectionery Variant 2020 & 2033

- Table 3: Brazil Chocolate Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Brazil Chocolate Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 5: Brazil Chocolate Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Brazil Chocolate Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Brazil Chocolate Industry Revenue billion Forecast, by Confectionery Variant 2020 & 2033

- Table 8: Brazil Chocolate Industry Volume K Tons Forecast, by Confectionery Variant 2020 & 2033

- Table 9: Brazil Chocolate Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Brazil Chocolate Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 11: Brazil Chocolate Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Brazil Chocolate Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Brazil Chocolate Industry?

The projected CAGR is approximately 3.84%.

2. Which companies are prominent players in the Brazil Chocolate Industry?

Key companies in the market include Nestlé SA, Nugali Chocolates, Chocoladefabriken Lindt & Sprüngli AG, Cacau Show, Ferrero International SA, Florestal Alimentos SA, Mars Incorporated, Arcor S A I C, Dori Alimentos SA, Dengo Chocolates SA, Fuji Oil Holdings Inc, Mondelēz International Inc, The Peccin S, The Hershey Company.

3. What are the main segments of the Brazil Chocolate Industry?

The market segments include Confectionery Variant, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 3 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing demand for meat alternatives.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Presence of numerous alternatives in the plant proteins.

8. Can you provide examples of recent developments in the market?

July 2023: Ferrero's sister company, Ferrara Candy Co., announced the acquisition of Brazilian snacks company Dori Alimentos, which sells a variety of chocolate and sugar confectionery brands, including Dori, Pettiz, and Jubes.July 2023: Ferrara Candy Company, a Ferrero-related company, signed an agreement to acquire Dori Alimentos to expand its network in the fast-growing Brazilian confectionery market.December 2022: Mars Incorporated launched Snickers Caramelo & Bacon limited edition chocolate bars in Brazil.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Brazil Chocolate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Brazil Chocolate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Brazil Chocolate Industry?

To stay informed about further developments, trends, and reports in the Brazil Chocolate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence