Key Insights

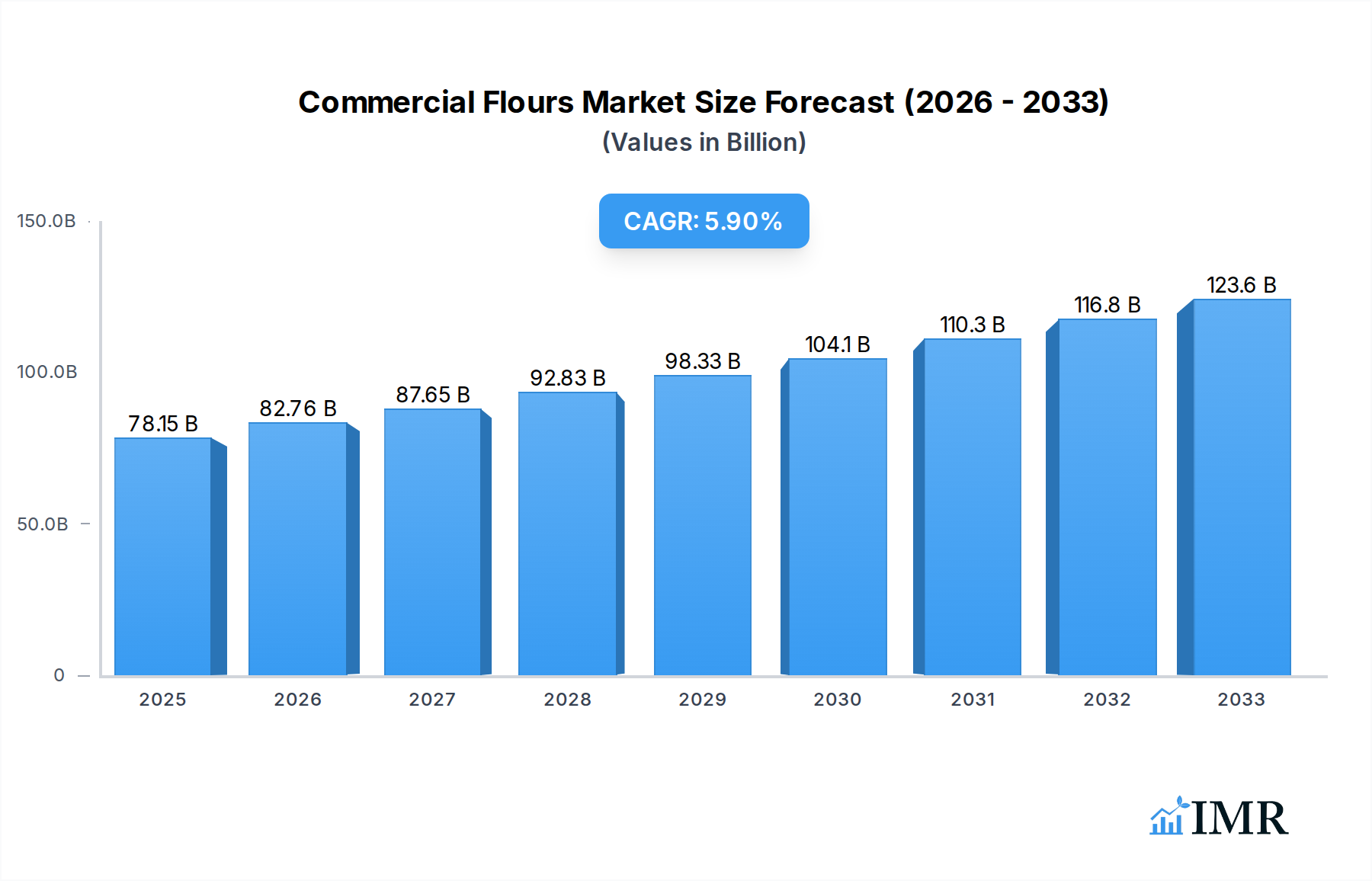

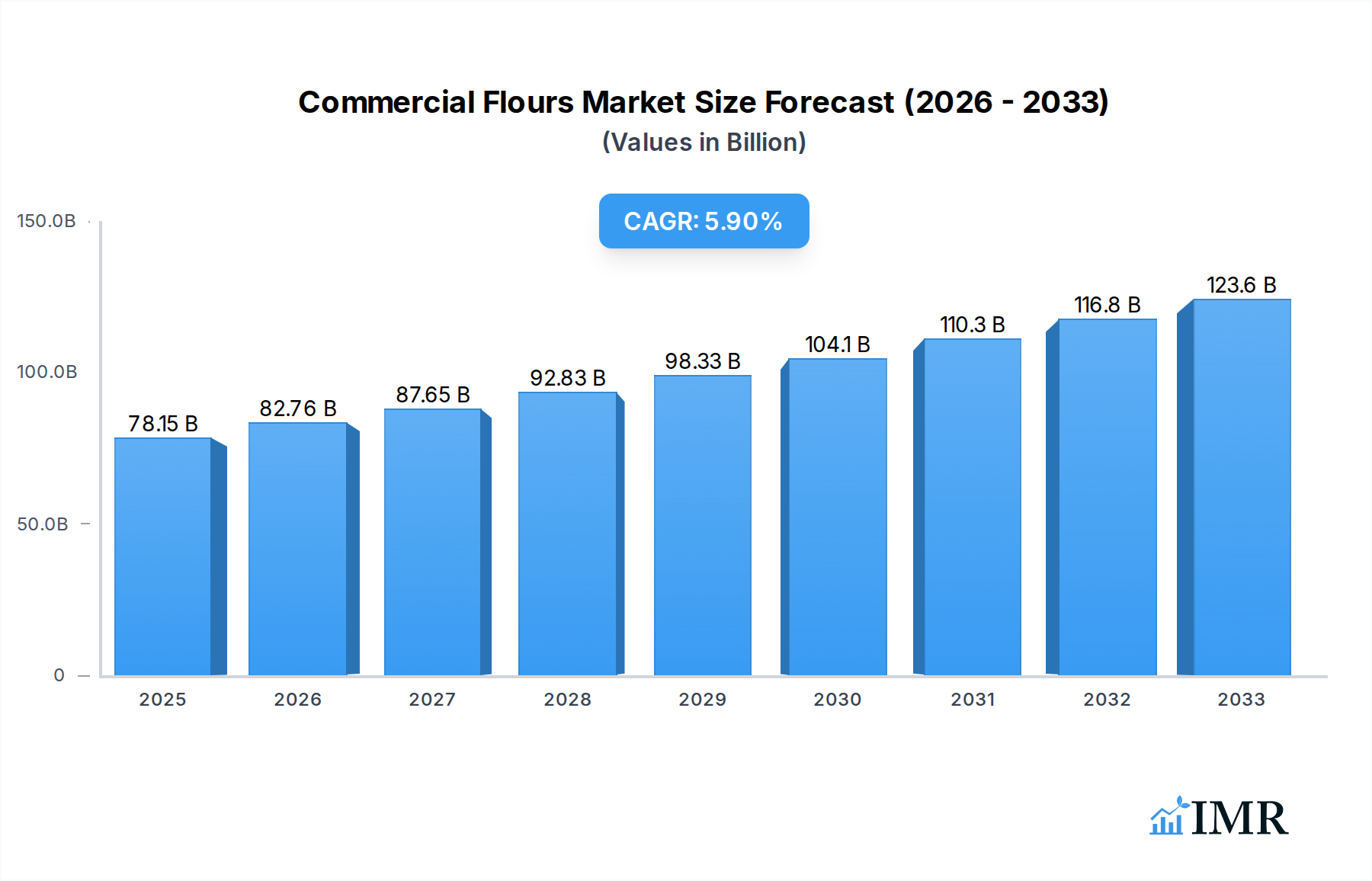

The global commercial flours market is poised for robust expansion, projected to reach an impressive $78.15 billion in 2025 and grow at a CAGR of 5.9% from 2025 to 2033. This substantial growth is primarily fueled by a burgeoning global population, the continuous expansion of the food processing and baking industries, and increasing consumer demand for convenience foods across various cultures. Innovations in product development, particularly the rise of specialty and functional flours, are significant market drivers. Trends indicate a notable shift towards healthier flour alternatives like whole wheat, ancient grains, and gluten-free options, alongside a growing emphasis on sustainable sourcing and organic certifications. The market is also benefiting from the diversification of culinary applications in both industrial and food service sectors, leading to enhanced product offerings and consumer choices.

Commercial Flours Market Size (In Billion)

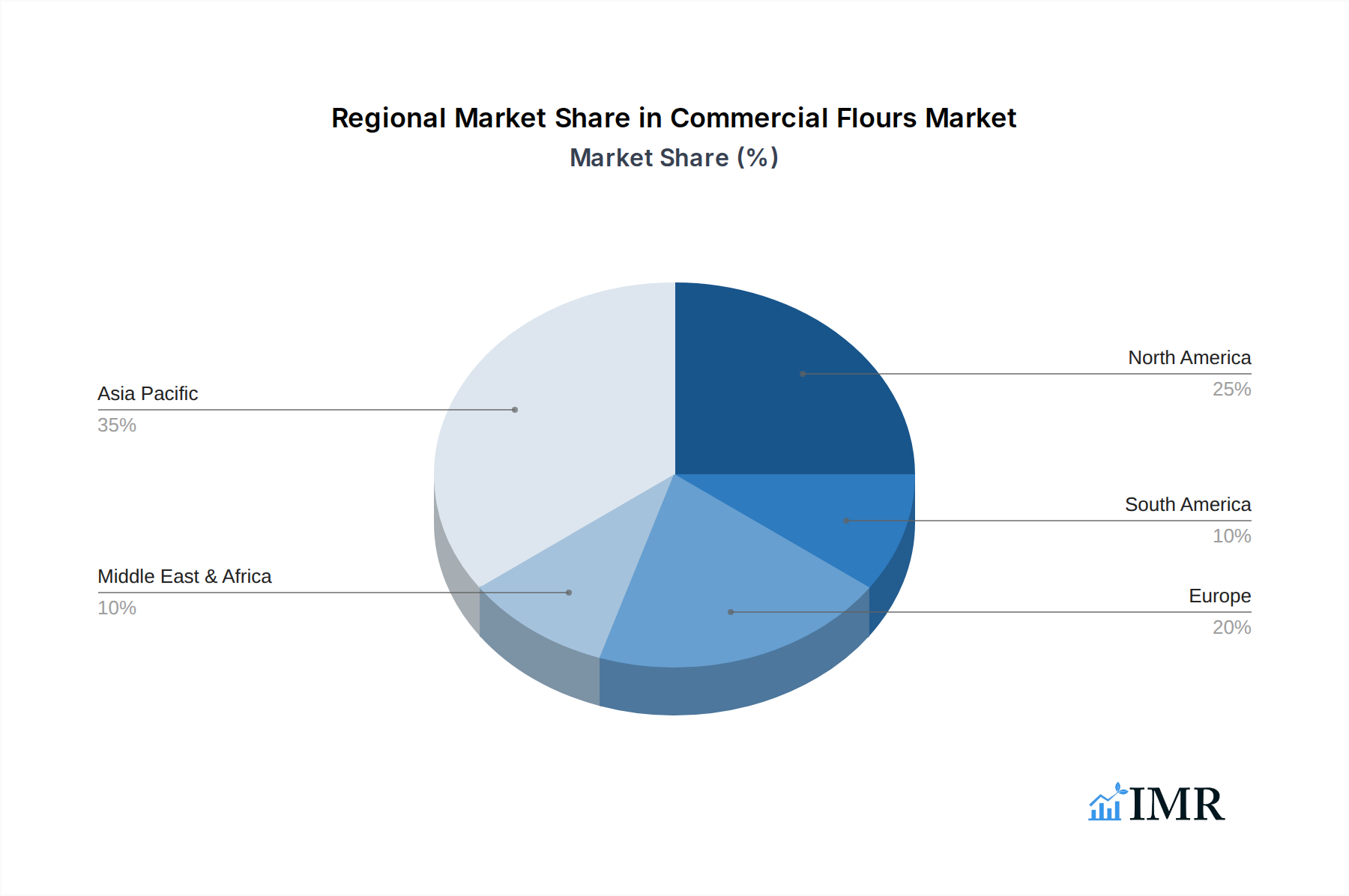

Segmented by application, industrial use accounts for the largest share, driven by its extensive integration in baking, confectionery, and processed food manufacturing, while the food services segment demonstrates strong growth potential as out-of-home consumption rises. From a type perspective, wheat flour remains the dominant category, yet rice flour, corn flour, and other grain-based flours are rapidly gaining traction due to evolving dietary preferences, allergen awareness, and a demand for diverse textures. Despite its promising trajectory, the market faces certain restraints, including the inherent volatility in agricultural commodity prices and increasing regulatory scrutiny regarding food safety and nutritional labeling. Key players like Cargill, Ardent Mills, and ADM are strategically investing in research and development to introduce fortified and value-added flour products that cater to evolving consumer needs. Geographically, Asia Pacific is anticipated to be a high-growth region, propelled by urbanization, increasing disposable incomes, and a large consumer base, while North America and Europe continue to be significant markets driven by innovation and established food industries.

Commercial Flours Company Market Share

This comprehensive report delves into the intricate dynamics of the Commercial Flours Market, a vital child market within the expansive Global Food & Beverage Ingredients and Agricultural Commodities parent markets. Designed for industry professionals, investors, and strategists, this analysis offers a deep dive into the forces shaping the flour industry, from innovative milling techniques to evolving consumer demand for specialty flour types. Covering the historical period of 2019–2024, with a base year and estimated year of 2025, and a robust forecast extending to 2033, this report provides unparalleled insights into market size, growth opportunities, competitive strategies, and future outlook for essential baking and food processing ingredients. Understand the pivotal roles played by major players like Cargill, ADM, and General Mills, and identify high-growth segments across industrial use, food services, and diverse flour types like wheat, rye, rice, and corn. Uncover critical market drivers, challenges, and emerging trends that will redefine the future of commercial flour production and consumption.

Commercial Flours Market Dynamics & Structure

The Commercial Flours market is characterized by a moderate to high level of concentration, with a few large multinational corporations dominating significant market shares, though a vibrant ecosystem of regional and specialty millers ensures competitive diversity. Market concentration is evidenced by the top five players collectively holding an estimated xx% of the global market share in 2025, driven by extensive supply chains, diverse product portfolios, and established distribution networks. Technological innovation acts as a crucial driver, particularly in areas like advanced milling techniques for improved yield and quality, nutrient fortification processes, and development of allergen-friendly or gluten-free flour alternatives. Regulatory frameworks, encompassing food safety standards, labeling requirements, and trade policies, significantly influence market entry and operational costs, creating barriers for smaller players but ensuring product integrity. The market faces competition from various product substitutes, including ready-mixes, alternative plant-based protein sources, and processed food ingredients that reduce the need for raw flour in certain applications. End-user demographics, such as the rising global population, increasing urbanization, and evolving dietary preferences (e.g., demand for whole grains, ancient grains, or low-carb options), directly impact flour consumption patterns. Mergers and acquisitions (M&A) remain a prevalent strategy for market expansion, consolidation, and diversification. Over the historical period of 2019-2024, the industry witnessed an average of xx M&A deals annually, with an estimated total deal volume of $xx billion, as companies seek to acquire new technologies, expand geographical reach, or secure raw material supply. For example, strategic acquisitions by large players have often focused on securing niche market segments or innovative production capabilities. While technological advancements are key, innovation barriers include high capital investment for upgrading machinery, the need for extensive R&D, and the complexities of scaling up new product formulations to commercial levels. Furthermore, geopolitical factors and climate change present ongoing challenges to consistent raw material supply and price stability, impacting overall market structure. The market's structure is also influenced by global trade dynamics, including tariffs and import/export restrictions, which can shift supply routes and impact regional flour prices and availability.

Commercial Flours Growth Trends & Insights

Leveraging Advanced Market Analytics, the Commercial Flours market is poised for robust expansion, with the global market size estimated at $xx billion in 2025, projected to reach $xx billion by 2033, exhibiting a compound annual growth rate (CAGR) of xx% during the forecast period of 2025–2033. This growth is predominantly fueled by a confluence of factors including sustained population growth, increased urbanization, and the evolving dietary habits across emerging economies. Market size evolution reflects a consistent upward trajectory, with demand primarily driven by the expanding food processing industry and the burgeoning food service sector globally. Adoption rates of specialty flours, such as rye flour for artisanal breads and rice flour for gluten-free applications, have seen significant acceleration, particularly in developed regions where health consciousness and diverse culinary experiences are highly valued.

Technological disruptions play a pivotal role in shaping this growth narrative. Advances in milling technology have led to improved yield, consistency, and the development of flours with enhanced functional properties, such as extended shelf-life or better baking performance. Furthermore, innovations in ingredient sourcing and processing, including sustainable agriculture practices and advanced quality control systems, are contributing to market sophistication. These technological advancements not only optimize production but also cater to consumer demands for transparency and quality.

Consumer behavior shifts are profoundly influencing the market landscape. There is a discernible trend towards healthier food choices, which translates into increased demand for whole grain flours, organic flours, and flours derived from ancient grains. The rising prevalence of dietary restrictions and preferences, such as gluten intolerance or veganism, has significantly boosted the market penetration of alternative flour types, including corn flour and various seed flours. Moreover, the convenience factor continues to drive demand in the food service sector, where pre-mixed or specialized flour blends are highly sought after to streamline operations. The market penetration of sustainable and ethically sourced flours is also steadily increasing, reflecting a global shift in consumer values towards environmental and social responsibility. These intricate shifts in consumer preferences and technological innovations collectively underpin the projected growth and transformation of the Commercial Flours market, making it a dynamic and opportunity-rich sector.

Dominant Regions, Countries, or Segments in Commercial Flours

The "Application: Industrial Use" segment stands out as the dominant force driving market growth in the Commercial Flours industry, exhibiting an estimated market share of xx% in 2025 and projected to maintain robust growth throughout the forecast period. This dominance is primarily attributable to the massive scale of the food processing industry, which utilizes commercial flours as a fundamental raw material for producing a vast array of consumer goods. Industrial use encompasses everything from large-scale bread and pastry production, snack foods, breakfast cereals, and processed meat binders to instant noodles and numerous other packaged food items. The sheer volume required by these manufacturing giants provides an unparalleled demand base, dwarfing the consumption from other segments. Key drivers for this segment’s dominance include economic policies supporting manufacturing growth in developing nations, established industrial infrastructure that facilitates large-scale production and distribution, and the continuous innovation in food product development that expands the applications of various flours.

Within the "Type" segment, Wheat Flour remains the undisputed leader, holding an estimated market share of xx% in 2025. Its supremacy stems from its unique viscoelastic properties, which are ideal for bread making and a wide range of baked goods, making it a staple ingredient globally. The extensive cultivation of wheat across major agricultural regions ensures a consistent and abundant supply, further cementing its dominant position. However, other flour types like Rice Flour and Corn Flour are experiencing accelerated growth, driven by dietary trends such as gluten-free diets and the expanding demand for specific ethnic cuisines.

Geographically, Asia-Pacific is identified as the leading region, spearheading market growth for Commercial Flours. Countries like China, India, and Southeast Asian nations are experiencing rapid urbanization, population expansion, and a burgeoning middle class with increasing disposable incomes. These demographic shifts fuel the demand for processed foods and baked goods, directly translating into higher flour consumption. Economic policies focused on food security and agricultural development also contribute to the region's dominance. Furthermore, the extensive agricultural land dedicated to wheat and rice cultivation in this region ensures a steady supply of raw materials. North America and Europe also hold significant market shares, driven by established food industries and high per capita consumption, but the growth momentum in Asia-Pacific is unparalleled due to its vast population base and ongoing economic development. The combination of industrial demand, wheat flour’s versatility, and Asia-Pacific’s demographic dividend makes these segments and regions the primary engines of growth for the Commercial Flours market.

Commercial Flours Product Landscape

The Commercial Flours product landscape is continuously evolving, marked by significant innovations and a focus on specialized applications. Wheat flour remains paramount, but advancements are seen in high-protein wheat flours for enhanced dough strength and whole-grain varieties that retain more nutritional value. Rye flour is gaining traction for its distinctive flavor and fiber content, particularly in artisanal baking. Rice flour is increasingly prominent in gluten-free applications, with fine-milled options offering improved texture for baked goods and coatings. Corn flour, beyond traditional uses, is being developed for specific functional properties in snacks and extrusion processes. Innovations include flour blends engineered for specific product outcomes, such as self-rising flours with precise leavening agents or enriched flours with added vitamins and minerals. Performance metrics like water absorption, dough stability, and starch damage are continually refined, offering millers and food manufacturers greater consistency and efficiency. Unique selling propositions revolve around functional benefits, nutritional profiles, and sourcing transparency, with a growing emphasis on organic, non-GMO, and sustainably milled products. Technological advancements in grain separation and particle size reduction are further enhancing the versatility and quality of commercial flour offerings.

Key Drivers, Barriers & Challenges in Commercial Flours

Key Drivers

The Commercial Flours market is primarily propelled by a rising global population and rapid urbanization, which inherently increases demand for staple food products. The expanding food processing industry acts as a significant catalyst, requiring large volumes of diverse flours for the production of bakery items, snacks, pasta, and convenience foods. Technological advancements in milling and processing techniques enhance efficiency, reduce waste, and improve flour quality, driving market competitiveness. Economic growth in emerging markets leads to higher disposable incomes, fostering increased consumption of processed and baked goods. Furthermore, policy-driven factors such as government subsidies for wheat and grain production, alongside initiatives promoting fortified foods, stimulate flour demand and consumption. For instance, the growing demand for fortified flour in regions with micronutrient deficiencies directly boosts industrial usage. The versatility of flour also drives its demand across various culinary applications, from traditional baking to modern food formulations.

Barriers & Challenges

The Commercial Flours market faces several significant challenges. Supply chain disruptions, exacerbated by climate change impacts on crop yields and geopolitical tensions, lead to price volatility and inconsistent raw material availability, affecting production schedules and profitability. Regulatory hurdles, including stringent food safety standards, allergen labeling requirements, and import/export restrictions, increase operational complexities and compliance costs for manufacturers. Competitive pressures from alternative ingredients and substitute products, such as plant-based proteins or gluten-free alternatives, continuously challenge traditional flour market share. Fluctuations in commodity prices, particularly for wheat, corn, and rice, directly impact production costs and retail prices, making market forecasting difficult. Furthermore, rising consumer health consciousness, while driving some specialty flour segments, also presents a challenge to conventional flour markets by fostering a negative perception of refined flours, potentially leading to declining demand in specific sub-segments. These challenges require strategic adaptation and resilience from market players to maintain growth.

Emerging Opportunities in Commercial Flours

Emerging opportunities in the Commercial Flours market are largely driven by evolving consumer preferences and technological advancements. Untapped markets in developing regions, especially in rural areas experiencing economic growth and increased access to processed foods, present significant potential for market penetration. The surging demand for innovative applications, such as specialized flour blends for 3D food printing or for enhanced textural properties in plant-based meat alternatives, opens new revenue streams. Evolving consumer preferences towards health-conscious and sustainable products are creating niches for organic, non-GMO, whole-grain, and ancient grain flours (like spelt, amaranth, and quinoa flour). Additionally, the rising awareness of specific dietary needs, such as gluten sensitivity or celiac disease, continues to fuel the expansion of the gluten-free flour segment, including rice, corn, and specialty legume flours. Opportunities also lie in personalized nutrition, where flour products could be tailored to individual dietary requirements. The development of functional flours with added nutritional benefits or specific performance characteristics also represents a fertile ground for innovation and market expansion.

Growth Accelerators in the Commercial Flours Industry

Several catalysts are driving long-term growth in the Commercial Flours industry. Technological breakthroughs in milling processes, such as improved automation, precision grinding, and optical sorting, enhance efficiency, reduce waste, and allow for the production of flours with superior and consistent quality. Strategic partnerships between flour millers and agricultural technology companies are ensuring sustainable sourcing of grains, improving crop yields, and developing climate-resilient varieties, thereby securing raw material supply. Furthermore, collaborations with food manufacturers enable the co-creation of innovative flour-based products tailored to emerging consumer trends. Market expansion strategies, particularly focusing on rapidly industrializing economies in Asia-Pacific and Africa, are unlocking new consumer bases with growing demand for processed and convenience foods. The increasing investment in research and development for functional flours, which offer enhanced nutritional profiles or specific baking characteristics, further accelerates market growth. The ongoing shift towards fortified foods globally, driven by public health initiatives, also acts as a significant accelerator, ensuring a baseline demand for nutrient-enhanced flours.

Key Players Shaping the Commercial Flours Market

Cargill ARDENT MILLS ADM General Mills Riviana Foods ConAgra Foods Bartlett and Company The Mennel Milling Company Bob's Red Mill Natural Foods Bay State Milling Company Hodgson Mill King Arthur Flour Company The Hain Celestial Group Grain Craft The White Lily Foods Company Wheat Montana North Dakota Mill Miller Milling Company Ingredion Incorporated Bunge Limited

Notable Milestones in Commercial Flours Sector

- 2020: Increased global demand for shelf-stable ingredients and home baking flours due to the COVID-19 pandemic, significantly boosting retail sales and shifting industrial demand patterns.

- 2021: Major investments in sustainable sourcing initiatives and traceability technologies across the grain supply chain by leading millers, driven by corporate social responsibility and consumer demand.

- 2022: Introduction of advanced specialty flour blends targeting specific dietary preferences, such as high-fiber, low-carb, or allergen-free options, expanding the functional flour segment.

- 2023: Significant mergers and acquisitions in the milling sector, consolidating regional markets and enhancing the global reach of major players, aiming for increased efficiency and reduced competition.

- 2024: Launch of innovative fortified flour programs in several developing nations, supported by government and NGOs, aiming to combat micronutrient deficiencies and drive industrial flour consumption.

- 2025 (Estimated): Continued surge in demand for organic and non-GMO certified flours, reflecting a sustained consumer shift towards clean label ingredients and natural food products.

In-Depth Commercial Flours Market Outlook

The future of the Commercial Flours market is characterized by dynamic growth, driven by sustained global population expansion and the relentless innovation within the food processing industry. Strategic partnerships focused on sustainable sourcing and technological advancements in milling will continue to enhance product quality and efficiency, acting as pivotal growth accelerators. Emerging opportunities in specialized and functional flour segments, catering to evolving consumer health trends and dietary preferences, will unlock new revenue streams, with the gluten-free and ancient grain categories showing particular promise. Geographic market expansion into rapidly developing economies, coupled with increased per capita consumption of processed and convenience foods, will significantly bolster market potential. The continuous investment in research and development for improved flour characteristics and novel applications ensures a robust future, making the commercial flours sector a fertile ground for strategic investment and innovation, projected to reach an impressive $xx billion by 2033.

Commercial Flours Segmentation

-

1. Application

- 1.1. Industrial Use

- 1.2. Food Services

- 1.3. Other

-

2. Type

- 2.1. Wheat Flour

- 2.2. Rye Flour

- 2.3. Rice Flour

- 2.4. Corn Flour

- 2.5. Others

Commercial Flours Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Commercial Flours Regional Market Share

Geographic Coverage of Commercial Flours

Commercial Flours REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Industrial Use

- 5.1.2. Food Services

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Wheat Flour

- 5.2.2. Rye Flour

- 5.2.3. Rice Flour

- 5.2.4. Corn Flour

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Commercial Flours Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Industrial Use

- 6.1.2. Food Services

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Wheat Flour

- 6.2.2. Rye Flour

- 6.2.3. Rice Flour

- 6.2.4. Corn Flour

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Commercial Flours Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Industrial Use

- 7.1.2. Food Services

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Wheat Flour

- 7.2.2. Rye Flour

- 7.2.3. Rice Flour

- 7.2.4. Corn Flour

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Commercial Flours Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Industrial Use

- 8.1.2. Food Services

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Wheat Flour

- 8.2.2. Rye Flour

- 8.2.3. Rice Flour

- 8.2.4. Corn Flour

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Commercial Flours Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Industrial Use

- 9.1.2. Food Services

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Wheat Flour

- 9.2.2. Rye Flour

- 9.2.3. Rice Flour

- 9.2.4. Corn Flour

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Commercial Flours Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Industrial Use

- 10.1.2. Food Services

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Wheat Flour

- 10.2.2. Rye Flour

- 10.2.3. Rice Flour

- 10.2.4. Corn Flour

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Commercial Flours Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Industrial Use

- 11.1.2. Food Services

- 11.1.3. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Wheat Flour

- 11.2.2. Rye Flour

- 11.2.3. Rice Flour

- 11.2.4. Corn Flour

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Cargill

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ARDENT MILLS

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ADM

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 General Mills

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Riviana Foods

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 ConAgra Foods

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bartlett and Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 The Mennel Milling Company

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bob's Red Mill Natural Foods

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Bay State Milling Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Hodgson Mill

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 King Arthur Flour Company

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 The Hain Celestial Group

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Grain Craft

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 The White Lily Foods Company

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Wheat Montana

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 North Dakota Mill

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Miller Milling Company

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Ingredion Incorporated

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Bunge Limited

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.1 Cargill

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Commercial Flours Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Commercial Flours Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Commercial Flours Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Commercial Flours Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Commercial Flours Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Commercial Flours Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Commercial Flours Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Commercial Flours Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Commercial Flours Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Commercial Flours Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Commercial Flours Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Commercial Flours Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Commercial Flours Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Commercial Flours Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Commercial Flours Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Commercial Flours Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Commercial Flours Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Commercial Flours Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Commercial Flours Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Commercial Flours Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Commercial Flours Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Commercial Flours Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Commercial Flours Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Commercial Flours Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Commercial Flours Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Commercial Flours Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Commercial Flours Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Commercial Flours Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Commercial Flours Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Commercial Flours Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Commercial Flours Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Commercial Flours Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Commercial Flours Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Commercial Flours Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Commercial Flours Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Commercial Flours Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Commercial Flours Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Commercial Flours Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Commercial Flours Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Commercial Flours Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Commercial Flours Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Commercial Flours Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Commercial Flours Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Commercial Flours Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Commercial Flours Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Commercial Flours Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Commercial Flours Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Commercial Flours Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Commercial Flours Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Commercial Flours Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Flours?

The projected CAGR is approximately 5.9%.

2. Which companies are prominent players in the Commercial Flours?

Key companies in the market include Cargill, ARDENT MILLS, ADM, General Mills, Riviana Foods, ConAgra Foods, Bartlett and Company, The Mennel Milling Company, Bob's Red Mill Natural Foods, Bay State Milling Company, Hodgson Mill, King Arthur Flour Company, The Hain Celestial Group, Grain Craft, The White Lily Foods Company, Wheat Montana, North Dakota Mill, Miller Milling Company, Ingredion Incorporated, Bunge Limited.

3. What are the main segments of the Commercial Flours?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 78.15 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Commercial Flours," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Commercial Flours report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Commercial Flours?

To stay informed about further developments, trends, and reports in the Commercial Flours, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence