Key Insights

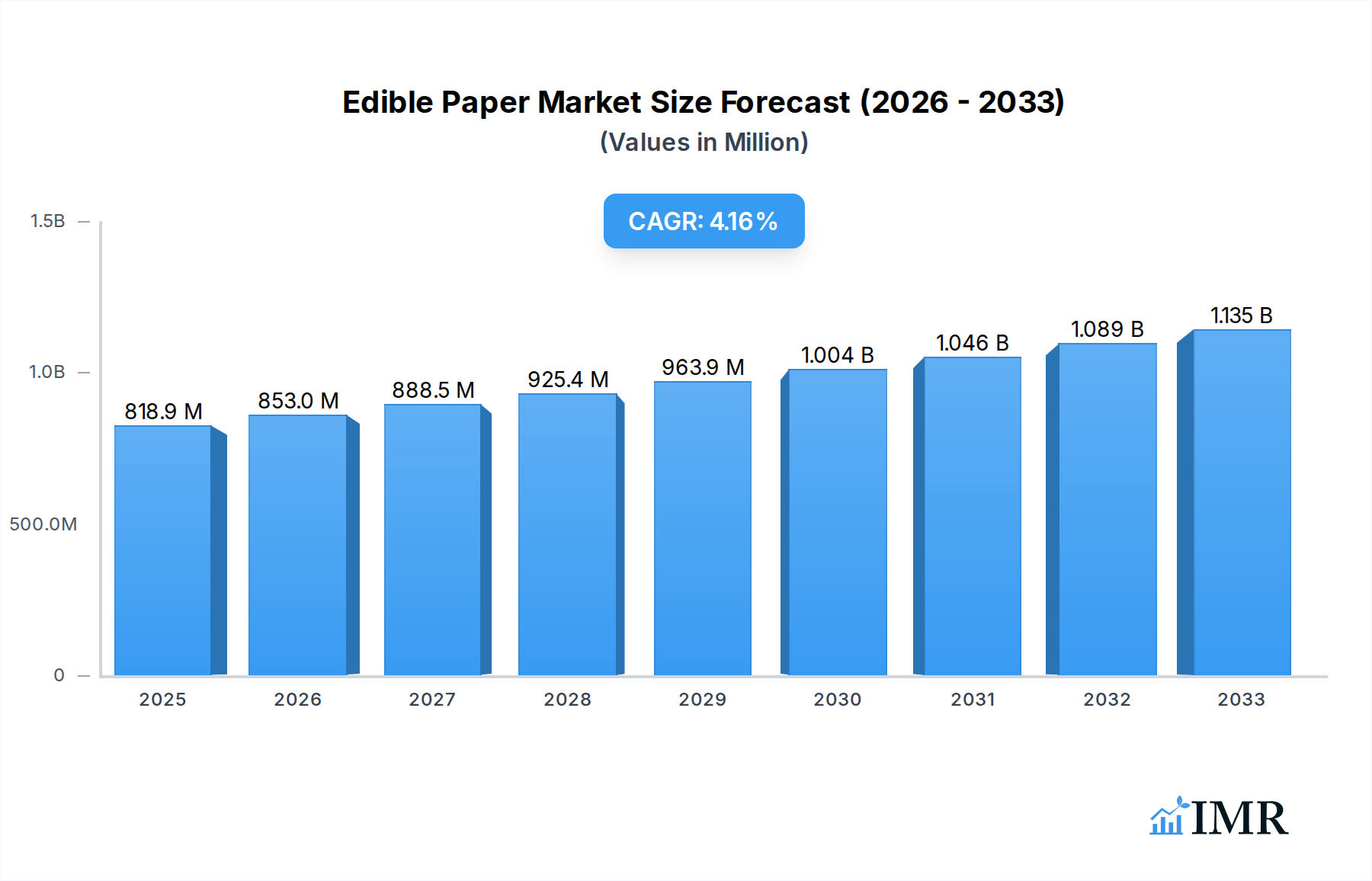

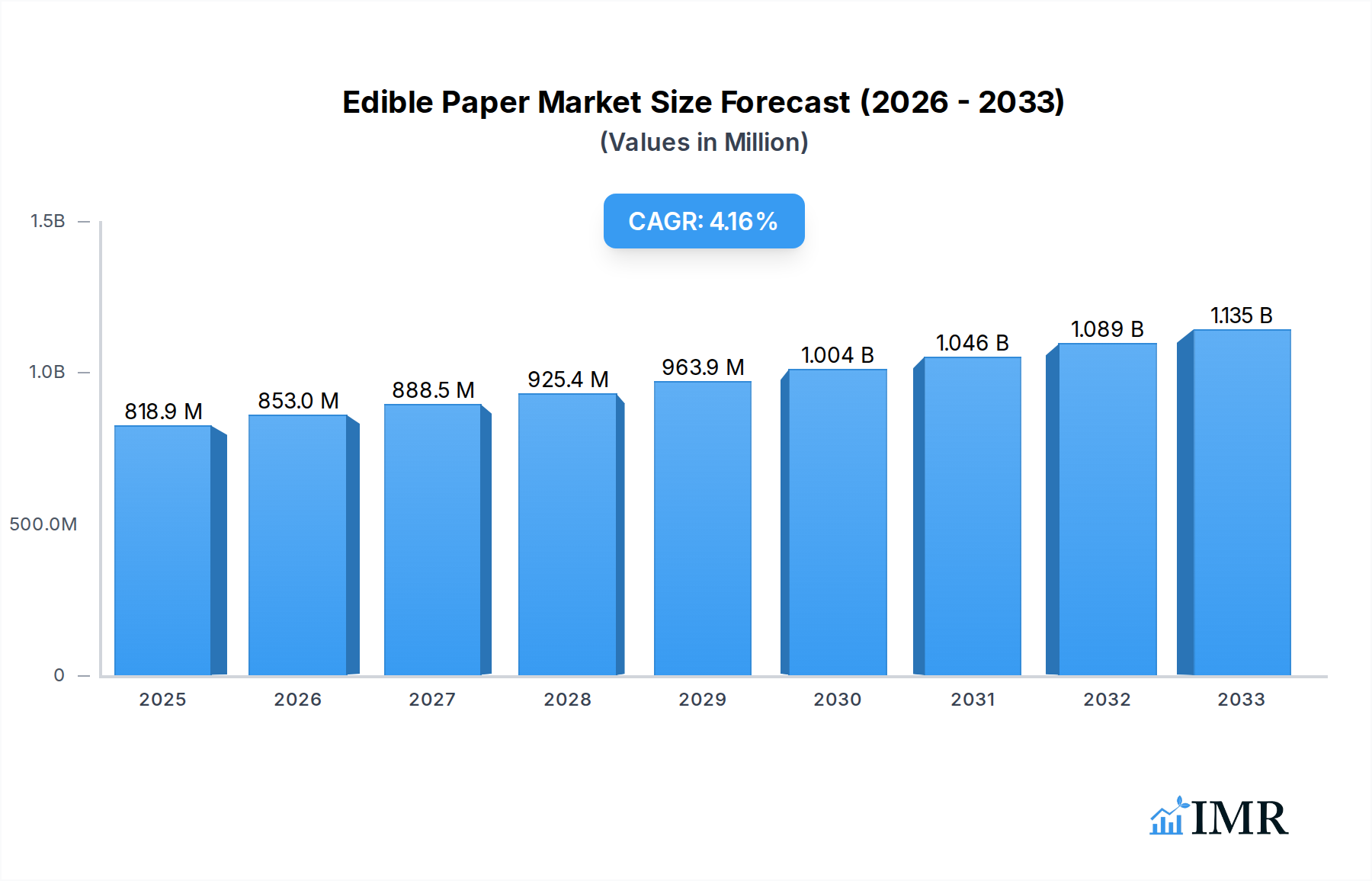

The global edible paper market is poised for robust growth, projected to reach $818.9 million by 2025. This expansion is driven by an increasing consumer demand for visually appealing and personalized food products, particularly in the bakery and confectionery sectors. The convenience and versatility of edible paper, allowing for intricate designs, logos, and custom messages on cakes, cookies, and other baked goods, are key catalysts. Furthermore, the rising popularity of DIY baking and custom cake decorating trends fuels the demand for decorative edible materials. The pharmaceutical industry also presents a growing segment, utilizing edible paper for printing medication information or for creating visually distinctive dosage forms, enhancing patient compliance. The market is witnessing a significant shift towards organic and natural ingredients, with consumers showing a preference for edible paper made from sustainable and plant-based sources. This trend is a crucial driver for market expansion, as manufacturers increasingly focus on developing and promoting organic product lines.

Edible Paper Market Size (In Million)

The market's steady CAGR of 4.2% between 2019 and 2033 underscores its stable and consistent upward trajectory. While the food industry, encompassing bakery, confectionery, and snacks, remains the dominant application, the pharmaceutical sector's growing adoption will contribute significantly to future market value. Key players are strategically focusing on product innovation, including the development of specialized edible papers with enhanced printability, texture, and flavor profiles. Geographic expansion, particularly in emerging economies within the Asia Pacific and Middle East & Africa regions, presents substantial growth opportunities. However, challenges such as fluctuating raw material prices and the need for stringent quality control to meet food safety standards could pose moderate restraints. Nevertheless, the overall outlook for the edible paper market remains highly positive, supported by evolving consumer preferences and continuous innovation within the industry.

Edible Paper Company Market Share

Here's a compelling, SEO-optimized report description for the Edible Paper market, designed for industry professionals:

Edible Paper Market: Global Analysis & Forecast (2019-2033)

Unlock critical insights into the dynamic global edible paper market. This comprehensive report delves into the intricate market structure, growth trajectories, regional dominance, and competitive landscape, providing actionable intelligence for stakeholders. Featuring data from 2019 to 2033, with a base year of 2025, this analysis covers the Food Industry, Bakery, Confectionery, Snacks, Pharmaceutical Industry, and innovative new applications. Explore the nuances of conventional vs. organic edible paper and understand the strategic moves of key players like Kokkooblate Co. Ltd, Schweitzer-Mauduit International, Inc., Primus Wafer Paper B.V., HOCH GmbH Oblatenfabrik, KOPYFORM GmbH, Fancy Flours, Inc., and CDA Products Limited.

Edible Paper Market Dynamics & Structure

The global edible paper market exhibits a moderate to high concentration, with a few key players holding significant market share. Technological innovation is a primary driver, with ongoing advancements in printing capabilities, material science for enhanced texture and stability, and the development of specialized edible inks. Regulatory frameworks, particularly concerning food safety and ingredient sourcing, play a crucial role in shaping market entry and product development. Competitive product substitutes, such as traditional frosting and fondant, are present but often lack the visual appeal and convenience offered by edible paper for intricate designs and branding. End-user demographics are increasingly influenced by a growing demand for personalized and visually appealing food products, especially within the bakery and confectionery segments. Mergers and acquisitions (M&A) are notable, signaling consolidation and strategic expansion within the industry. For instance, the estimated 15 M&A deals between 2021 and 2024 highlight this trend. Innovation barriers include the cost of advanced printing technology and the need for stringent quality control to meet diverse international food safety standards. The overall market competitiveness is driven by both product differentiation and cost-efficiency.

- Market Concentration: Moderate to high, with key players dominating specific niches.

- Technological Innovation Drivers: Advancements in printing, material science, and edible ink formulations.

- Regulatory Frameworks: Stringent food safety and ingredient sourcing regulations influence market dynamics.

- Competitive Product Substitutes: Traditional frosting, fondant, and other decorative elements.

- End-User Demographics: Growing demand for personalized, visually appealing food and pharmaceutical products.

- M&A Trends: Estimated 15 M&A deals between 2021-2024, indicating market consolidation and strategic growth.

- Innovation Barriers: High cost of advanced technology and stringent quality control requirements.

Edible Paper Growth Trends & Insights

The global edible paper market is poised for robust growth, projected to expand significantly from an estimated $250 million in 2024 to over $600 million by 2033. This upward trajectory is underpinned by a substantial Compound Annual Growth Rate (CAGR) of approximately 9.5% during the forecast period (2025–2033). Adoption rates are accelerating across various applications, driven by evolving consumer preferences for visually engaging food products and the increasing need for branding opportunities in the food and beverage sector. Technological disruptions, such as advancements in high-resolution edible printing and the development of more flexible and water-resistant edible paper substrates, are fundamentally reshaping product possibilities. Consumer behavior shifts are particularly evident in the bakery and confectionery segments, where edible paper is no longer a niche product but a standard tool for customization and artisanal creations. The pharmaceutical industry is also emerging as a significant growth area, utilizing edible paper for drug delivery systems, patient identification, and visually appealing dosage forms, with an estimated market penetration of 10% in this segment by 2028. The convenience of pre-printed edible images for cakes and cookies, coupled with the growing influence of social media on food presentation, further fuels market penetration. The demand for organic and natural ingredients is also a powerful market force, driving innovation in the organic edible paper segment, which is expected to grow at a CAGR of 12% from 2025 to 2033.

Dominant Regions, Countries, or Segments in Edible Paper

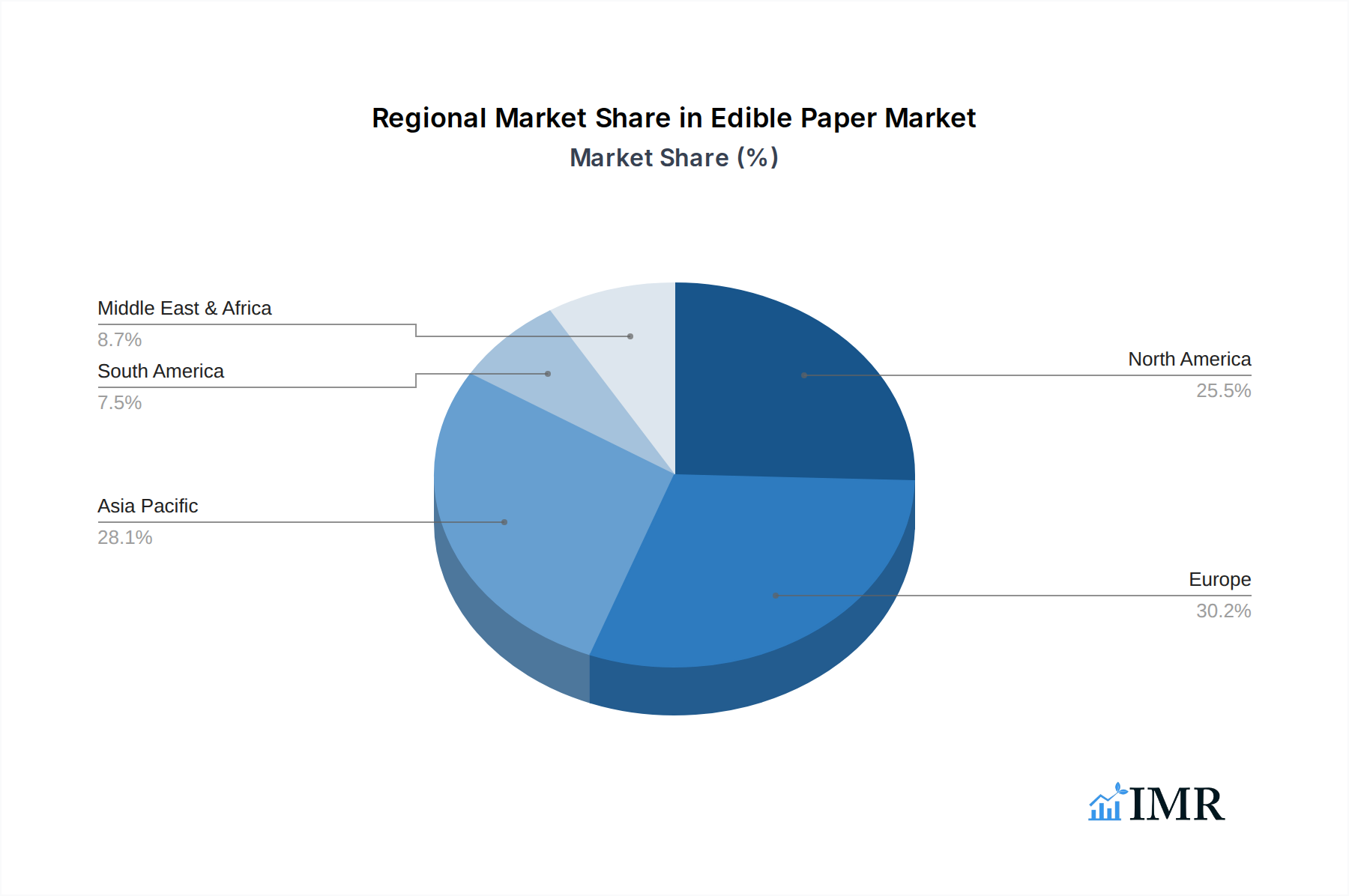

The Food Industry, particularly the Bakery and Confectionery segments, collectively drives the dominant growth in the global edible paper market. These segments are estimated to account for approximately 70% of the total market share in 2025. North America and Europe are the leading regions, contributing over 60% of the global revenue due to established confectionery markets, high disposable incomes, and a strong consumer appreciation for aesthetically pleasing food items. Within North America, the United States leads with an estimated market value of $120 million in 2025, driven by a highly developed baking industry and widespread adoption of edible decorations for custom cakes and party treats. Economic policies supporting small and medium-sized enterprises (SMEs) in the food sector also contribute to market expansion. In Europe, countries like Germany and the UK are significant contributors, with strong demand from both industrial bakeries and home bakers. The Type segment also shows a clear dominance: Conventional edible paper currently holds an estimated 85% market share due to its cost-effectiveness and widespread availability. However, the Organic edible paper segment is experiencing a rapid growth rate, driven by increasing consumer consciousness about health and sustainability, and is projected to capture a larger share of the market by 2033. The Pharmaceutical Industry segment, while smaller in its current share (estimated 5% in 2025), presents a significant growth potential, with an anticipated CAGR of 15% from 2025 to 2033, fueled by innovative applications in drug delivery and patient compliance. The market share within the food industry is further segmented with Bakery holding an estimated 40%, Confectionery 30%, and Snacks 10% in 2025.

- Dominant Application Segments:

- Food Industry (Bakery, Confectionery, Snacks) - Estimated 70% market share in 2025.

- Leading Regions:

- North America (US: Estimated $120 million market value in 2025).

- Europe (Germany, UK).

- Dominant Type Segment:

- Conventional Edible Paper - Estimated 85% market share in 2025.

- High Growth Potential Segment:

- Pharmaceutical Industry - Estimated 5% market share in 2025, with a projected 15% CAGR (2025-2033).

- Key Drivers:

- Established food and confectionery industries.

- High disposable incomes and consumer demand for visual appeal.

- Supportive economic policies for SMEs.

- Growing health and sustainability consciousness.

Edible Paper Product Landscape

The edible paper product landscape is characterized by continuous innovation aimed at enhancing functionality and aesthetic appeal. Key product innovations include ultra-thin wafer papers that offer superior flexibility and translucency, crucial for delicate cake decorations and confectionery applications. Advanced printing technologies have enabled the creation of high-resolution, vibrant edible images with exceptional color accuracy, catering to personalized branding and intricate designs. Performance metrics such as printability, durability, and flavor neutrality are paramount. Unique selling propositions often revolve around customization capabilities, such as bespoke shapes, sizes, and pre-printed designs tailored to specific client needs. Technological advancements are also focusing on improving shelf life and resistance to moisture, expanding the usability of edible paper in diverse climatic conditions and product formulations. The market is witnessing an influx of specialized products, including allergen-free and gluten-free edible papers, aligning with growing consumer dietary requirements.

Key Drivers, Barriers & Challenges in Edible Paper

Key Drivers:

- Growing demand for personalized and visually appealing food products: Consumers increasingly seek customized and Instagrammable food items, a trend perfectly addressed by edible paper.

- Technological advancements in printing and material science: High-resolution printing and improved paper durability open new application possibilities.

- Expanding applications in the pharmaceutical sector: Edible paper offers innovative solutions for drug delivery and patient-friendly medication.

- Rising popularity of DIY baking and cake decorating: Home bakers are utilizing edible paper for professional-looking results.

- Increased use in food branding and marketing: Companies are leveraging edible paper for custom logos and promotional designs.

Barriers & Challenges:

- Supply chain disruptions and raw material price volatility: Fluctuations in the cost of essential ingredients like potato starch and rice flour can impact profitability.

- Stringent and evolving food safety regulations: Compliance with varying international standards requires significant investment and ongoing adaptation.

- Competition from traditional decorative elements: Frosting, fondant, and piping techniques remain strong alternatives.

- Perceived limitations in texture and taste: Some consumers may have reservations about the mouthfeel or subtle flavors of edible paper.

- Shelf-life considerations: Moisture sensitivity can limit application in certain food products and storage conditions, estimated to affect 5% of potential applications without proper formulation.

Emerging Opportunities in Edible Paper

Emerging opportunities in the edible paper market are driven by innovation and evolving consumer trends. The pharmaceutical industry presents a significant untapped market, with potential for drug delivery systems, personalized medicine, and enhanced patient compliance through palatable and visually distinct dosage forms. The increasing global demand for vegan and plant-based food products is creating an opportunity for specialized vegan edible papers. Furthermore, advancements in biodegradable and compostable edible paper materials align with growing environmental consciousness. The integration of edible paper with smart packaging technologies for enhanced product authentication and consumer engagement is another promising avenue. Finally, exploring novel applications in educational tools (e.g., edible craft materials for children) and specialty food products beyond traditional bakery and confectionery offers untapped market potential.

Growth Accelerators in the Edible Paper Industry

Long-term growth in the edible paper industry is being significantly accelerated by several key catalysts. Technological breakthroughs in high-speed, multi-color edible printing are making customization more accessible and cost-effective for businesses of all sizes. Strategic partnerships between edible paper manufacturers and leading food brands, as well as pharmaceutical companies, are driving innovation and market penetration into new sectors. Market expansion strategies targeting emerging economies with growing middle classes and increasing disposable incomes are unlocking new consumer bases. Furthermore, the development of specialty edible papers with enhanced properties like increased heat resistance, improved print clarity, and specific dietary attributes (e.g., allergen-free, low-sugar) is broadening the product appeal and creating niche markets. Continuous research into sustainable sourcing and production methods also acts as a growth accelerator by appealing to environmentally conscious consumers and regulatory bodies.

Key Players Shaping the Edible Paper Market

- Kokkooblate Co. Ltd

- Schweitzer-Mauduit International, Inc.

- Primus Wafer Paper B.V.

- HOCH GmbH Oblatenfabrik

- KOPYFORM GmbH

- Fancy Flours, Inc.

- CDA Products Limited

Notable Milestones in Edible Paper Sector

- 2020: Launch of advanced edible printing inks with enhanced color vibrancy and longevity by KOPYFORM GmbH.

- 2021: Schweitzer-Mauduit International, Inc. acquires a key player in the specialized paper manufacturing sector, expanding its edible paper portfolio.

- 2022: Primus Wafer Paper B.V. introduces a new line of organic edible papers, meeting growing consumer demand for natural ingredients.

- 2023: Fancy Flours, Inc. expands its distribution network, making edible paper products more accessible to home bakers and small businesses across North America.

- 2024: CDA Products Limited innovates with a new, more flexible edible paper formulation designed for complex confectionery designs, with initial market trials showing a 30% improvement in application success rate.

- 2025: Anticipated increase in R&D investment by major players focusing on pharmaceutical applications, with an estimated $50 million allocated globally.

In-Depth Edible Paper Market Outlook

The future outlook for the edible paper market is exceptionally promising, driven by relentless innovation and a broadening scope of applications. Growth accelerators, including advanced printing technologies and strategic collaborations within the food and pharmaceutical industries, will continue to fuel expansion. The increasing consumer focus on personalized and visually engaging experiences, coupled with the pharmaceutical sector's exploration of novel drug delivery methods, presents substantial untapped potential. Strategic investments in research and development for sustainable materials and specialized product lines, such as allergen-free and plant-based options, will further diversify the market and cater to evolving consumer demands. The market is well-positioned for sustained, high-growth expansion, with opportunities for both established players and new entrants to capture significant value.

Edible Paper Segmentation

-

1. Application

- 1.1. Food Industry

- 1.2. Bakery

- 1.3. Confectionery

- 1.4. Snacks

- 1.5. Others

- 1.6. Pharmaceutical Industry

- 1.7. Others

-

2. Types

- 2.1. Conventional

- 2.2. Organic

Edible Paper Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Edible Paper Regional Market Share

Geographic Coverage of Edible Paper

Edible Paper REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food Industry

- 5.1.2. Bakery

- 5.1.3. Confectionery

- 5.1.4. Snacks

- 5.1.5. Others

- 5.1.6. Pharmaceutical Industry

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Conventional

- 5.2.2. Organic

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Edible Paper Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food Industry

- 6.1.2. Bakery

- 6.1.3. Confectionery

- 6.1.4. Snacks

- 6.1.5. Others

- 6.1.6. Pharmaceutical Industry

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Conventional

- 6.2.2. Organic

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Edible Paper Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food Industry

- 7.1.2. Bakery

- 7.1.3. Confectionery

- 7.1.4. Snacks

- 7.1.5. Others

- 7.1.6. Pharmaceutical Industry

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Conventional

- 7.2.2. Organic

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Edible Paper Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food Industry

- 8.1.2. Bakery

- 8.1.3. Confectionery

- 8.1.4. Snacks

- 8.1.5. Others

- 8.1.6. Pharmaceutical Industry

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Conventional

- 8.2.2. Organic

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Edible Paper Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food Industry

- 9.1.2. Bakery

- 9.1.3. Confectionery

- 9.1.4. Snacks

- 9.1.5. Others

- 9.1.6. Pharmaceutical Industry

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Conventional

- 9.2.2. Organic

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Edible Paper Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food Industry

- 10.1.2. Bakery

- 10.1.3. Confectionery

- 10.1.4. Snacks

- 10.1.5. Others

- 10.1.6. Pharmaceutical Industry

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Conventional

- 10.2.2. Organic

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Edible Paper Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food Industry

- 11.1.2. Bakery

- 11.1.3. Confectionery

- 11.1.4. Snacks

- 11.1.5. Others

- 11.1.6. Pharmaceutical Industry

- 11.1.7. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Conventional

- 11.2.2. Organic

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Kokkooblate Co. Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Schweitzer-Mauduit International

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Inc.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Primus Wafer Paper B.V.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 HOCH GmbH Oblatenfabrik

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 KOPYFORM GmbH

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Fancy Flours

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 CDA Products Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Kokkooblate Co. Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Edible Paper Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Edible Paper Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Edible Paper Revenue (million), by Application 2025 & 2033

- Figure 4: North America Edible Paper Volume (K), by Application 2025 & 2033

- Figure 5: North America Edible Paper Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Edible Paper Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Edible Paper Revenue (million), by Types 2025 & 2033

- Figure 8: North America Edible Paper Volume (K), by Types 2025 & 2033

- Figure 9: North America Edible Paper Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Edible Paper Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Edible Paper Revenue (million), by Country 2025 & 2033

- Figure 12: North America Edible Paper Volume (K), by Country 2025 & 2033

- Figure 13: North America Edible Paper Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Edible Paper Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Edible Paper Revenue (million), by Application 2025 & 2033

- Figure 16: South America Edible Paper Volume (K), by Application 2025 & 2033

- Figure 17: South America Edible Paper Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Edible Paper Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Edible Paper Revenue (million), by Types 2025 & 2033

- Figure 20: South America Edible Paper Volume (K), by Types 2025 & 2033

- Figure 21: South America Edible Paper Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Edible Paper Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Edible Paper Revenue (million), by Country 2025 & 2033

- Figure 24: South America Edible Paper Volume (K), by Country 2025 & 2033

- Figure 25: South America Edible Paper Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Edible Paper Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Edible Paper Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Edible Paper Volume (K), by Application 2025 & 2033

- Figure 29: Europe Edible Paper Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Edible Paper Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Edible Paper Revenue (million), by Types 2025 & 2033

- Figure 32: Europe Edible Paper Volume (K), by Types 2025 & 2033

- Figure 33: Europe Edible Paper Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Edible Paper Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Edible Paper Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Edible Paper Volume (K), by Country 2025 & 2033

- Figure 37: Europe Edible Paper Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Edible Paper Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Edible Paper Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Edible Paper Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Edible Paper Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Edible Paper Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Edible Paper Revenue (million), by Types 2025 & 2033

- Figure 44: Middle East & Africa Edible Paper Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Edible Paper Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Edible Paper Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Edible Paper Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Edible Paper Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Edible Paper Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Edible Paper Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Edible Paper Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Edible Paper Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Edible Paper Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Edible Paper Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Edible Paper Revenue (million), by Types 2025 & 2033

- Figure 56: Asia Pacific Edible Paper Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Edible Paper Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Edible Paper Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Edible Paper Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Edible Paper Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Edible Paper Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Edible Paper Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Edible Paper Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Edible Paper Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Edible Paper Revenue million Forecast, by Types 2020 & 2033

- Table 4: Global Edible Paper Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Edible Paper Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Edible Paper Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Edible Paper Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Edible Paper Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Edible Paper Revenue million Forecast, by Types 2020 & 2033

- Table 10: Global Edible Paper Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Edible Paper Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Edible Paper Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Edible Paper Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Edible Paper Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Edible Paper Revenue million Forecast, by Types 2020 & 2033

- Table 22: Global Edible Paper Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Edible Paper Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Edible Paper Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Edible Paper Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Edible Paper Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Edible Paper Revenue million Forecast, by Types 2020 & 2033

- Table 34: Global Edible Paper Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Edible Paper Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Edible Paper Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Edible Paper Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Edible Paper Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Edible Paper Revenue million Forecast, by Types 2020 & 2033

- Table 58: Global Edible Paper Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Edible Paper Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Edible Paper Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Edible Paper Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Edible Paper Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Edible Paper Revenue million Forecast, by Types 2020 & 2033

- Table 76: Global Edible Paper Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Edible Paper Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Edible Paper Volume K Forecast, by Country 2020 & 2033

- Table 79: China Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Edible Paper Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Edible Paper Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Edible Paper Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Edible Paper?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Edible Paper?

Key companies in the market include Kokkooblate Co. Ltd, Schweitzer-Mauduit International, Inc., Primus Wafer Paper B.V., HOCH GmbH Oblatenfabrik, KOPYFORM GmbH, Fancy Flours, Inc., CDA Products Limited.

3. What are the main segments of the Edible Paper?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 818.9 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Edible Paper," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Edible Paper report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Edible Paper?

To stay informed about further developments, trends, and reports in the Edible Paper, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence