Key Insights

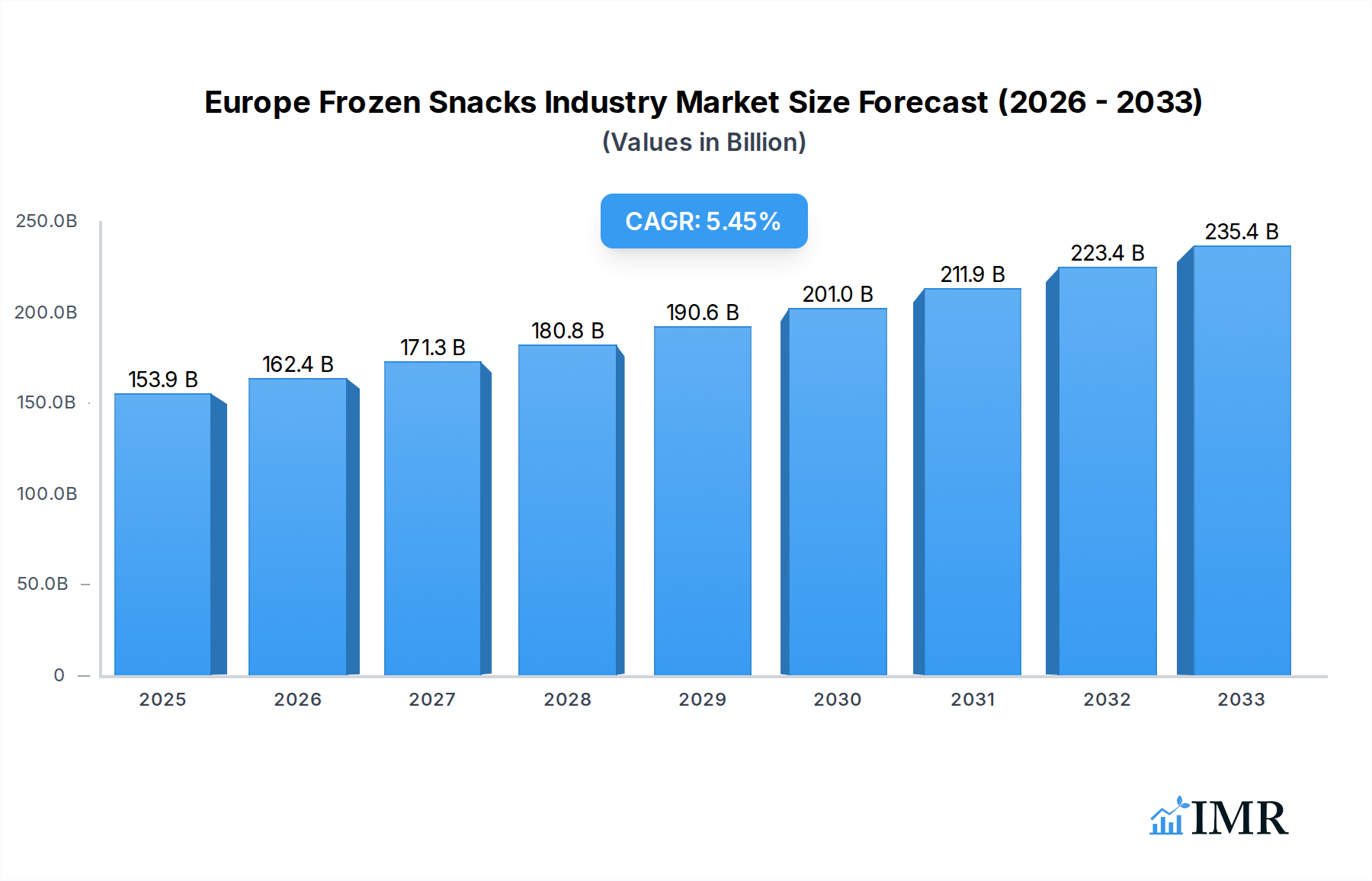

The Europe Frozen Snacks Industry is poised for robust growth, projected to reach a substantial USD 153.91 billion by 2025, driven by an anticipated Compound Annual Growth Rate (CAGR) of 5.5% over the forecast period of 2025-2033. This upward trajectory is significantly influenced by evolving consumer lifestyles, characterized by increasing demand for convenient and ready-to-eat food options. The rise of busy work schedules and smaller household sizes in Europe amplifies the appeal of frozen snacks as a quick and easy meal or snack solution. Furthermore, ongoing innovation within the industry, particularly in product development, including healthier alternatives, diverse flavor profiles, and ethically sourced ingredients, is attracting a wider consumer base and fostering market expansion. The increasing penetration of organized retail channels and the burgeoning online food delivery services are also playing a pivotal role in enhancing accessibility and boosting sales volumes across the region.

Europe Frozen Snacks Industry Market Size (In Billion)

The market segmentation reveals key areas of opportunity and consumer preference. Fruit-based snacks and potato-based snacks are expected to lead the charge, catering to both health-conscious consumers and those seeking familiar, popular options. Meat- and seafood-based snacks are also anticipated to maintain a strong presence, driven by quality advancements and premium offerings. Distribution channels are experiencing a significant shift, with hypermarkets/supermarkets continuing to dominate, but online retail stores are rapidly gaining traction, reflecting the broader e-commerce trend in food purchases. While the market benefits from strong growth drivers, challenges such as fluctuating raw material prices and the need for sustainable packaging solutions will require strategic management. Nevertheless, the overall outlook for the Europe Frozen Snacks Industry remains exceptionally positive, supported by sustained consumer demand and continuous industry adaptation.

Europe Frozen Snacks Industry Company Market Share

Europe Frozen Snacks Industry Report: Market Dynamics, Growth Trends, and Future Outlook

Unlock comprehensive insights into the burgeoning Europe Frozen Snacks Industry. This in-depth report analyzes market dynamics, growth trajectories, key players, and future opportunities, providing actionable intelligence for industry professionals. With a focus on parent and child market segments, this report offers a complete understanding of the landscape. Values are presented in billion units. Study Period: 2019–2033, Base Year: 2025, Estimated Year: 2025, Forecast Period: 2025–2033, Historical Period: 2019–2024.

Europe Frozen Snacks Industry Market Dynamics & Structure

The Europe frozen snacks market is characterized by a moderate to high degree of concentration, with leading players like Nomad Foods Limited and Dr. August Oetker KG holding significant market share. Technological innovation is a key driver, with advancements in freezing technology, packaging, and product formulation enhancing shelf life, texture, and taste. The regulatory framework, primarily focused on food safety standards and labeling requirements, plays a crucial role in shaping product development and market entry. Competitive product substitutes, such as chilled snacks and ready-to-eat meals, exert pressure, necessitating continuous product differentiation and value-added offerings. End-user demographics reveal a growing demand from busy households, young professionals, and convenience-seeking consumers, driving innovation towards healthier and more sophisticated frozen snack options. Mergers and acquisitions (M&A) remain a strategic tool for market expansion and portfolio diversification, with recent activities indicating consolidation and a focus on acquiring innovative brands.

- Market Concentration: Dominated by a few key players, with opportunities for niche market penetration.

- Technological Innovation: Focus on preservation, convenience, and enhanced sensory appeal.

- Regulatory Framework: Stringent food safety and labeling standards influence product development.

- Competitive Substitutes: Chilled snacks and ready-to-eat options pose a competitive threat.

- End-User Demographics: Growing demand from convenience-focused consumers and families.

- M&A Trends: Strategic acquisitions to gain market share and expand product portfolios.

Europe Frozen Snacks Industry Growth Trends & Insights

The Europe frozen snacks market is poised for robust growth, driven by evolving consumer lifestyles and an increasing demand for convenient, high-quality food options. The market size is projected to expand significantly, fueled by rising disposable incomes and a growing acceptance of frozen foods as healthy and nutritious alternatives. Adoption rates are accelerating, particularly for innovative product categories such as plant-based frozen snacks and premium frozen desserts. Technological disruptions, including advanced blast freezing techniques and intelligent packaging solutions, are enhancing product quality and extending shelf life, thereby boosting consumer confidence. Consumer behavior shifts towards health-conscious choices are also influencing the market, leading to a surge in demand for frozen snacks with natural ingredients, reduced sugar content, and added nutritional benefits. The CAGR for the forecast period is estimated to be between 4.5% and 5.8%, reflecting a sustained upward trend. Market penetration is expected to deepen, especially in emerging economies within Europe, as awareness and accessibility of frozen food options increase. The convenience factor remains paramount, with consumers increasingly relying on frozen snacks for quick meal solutions and on-the-go consumption. The penetration of online retail channels for frozen food purchases is also a significant growth driver, offering consumers greater accessibility and variety.

Dominant Regions, Countries, or Segments in Europe Frozen Snacks Industry

The Potato-based Snacks segment consistently emerges as the dominant force within the Europe frozen snacks industry. This segment, encompassing a wide array of products from classic fries to innovative wedges and coated potato snacks, commands a substantial market share due to its widespread appeal, versatility, and established consumer preference across various European nations.

- Key Drivers for Potato-based Snacks Dominance:

- Ubiquitous Consumer Preference: Potatoes are a staple in European diets, making potato-based snacks a familiar and comforting choice.

- Versatility in Formats and Flavors: The ability to create diverse shapes, textures, and flavor profiles caters to a broad spectrum of tastes, from traditional to exotic.

- Established Retail Presence: Potato-based frozen snacks enjoy extensive shelf space in hypermarkets and supermarkets, ensuring high visibility and accessibility.

- Industry Innovation: Manufacturers continually introduce new variants, such as healthier baked options, seasoned fries, and specialty potato products, to retain consumer interest and capture new market segments.

- Cost-Effectiveness: Potatoes are a relatively affordable raw ingredient, allowing for competitive pricing of frozen snacks, which appeals to budget-conscious consumers.

Within the broader Distribution Channel: Hypermarket/Supermarket segment, these retail giants are the primary conduits for frozen snacks reaching the end consumer. Their vast reach, extensive product assortments, and frequent promotional activities make them indispensable for driving sales volume.

- Dominance Factors for Hypermarket/Supermarket Distribution:

- Wide Reach and Accessibility: These stores are present in virtually every urban and suburban area, providing unparalleled access for consumers.

- Extensive Cold Chain Infrastructure: Hypermarkets and supermarkets are well-equipped with large freezers and refrigerators, essential for maintaining the quality and safety of frozen products.

- One-Stop Shopping Experience: Consumers can purchase frozen snacks along with other grocery items, enhancing convenience.

- Brand Visibility and Shelf Space: Leading brands vie for prominent shelf placement, driving impulse purchases and brand recognition.

- Promotional Activities and Discounts: Regular sales, discounts, and loyalty programs offered by these retailers significantly influence purchasing decisions and boost sales volumes for frozen snacks.

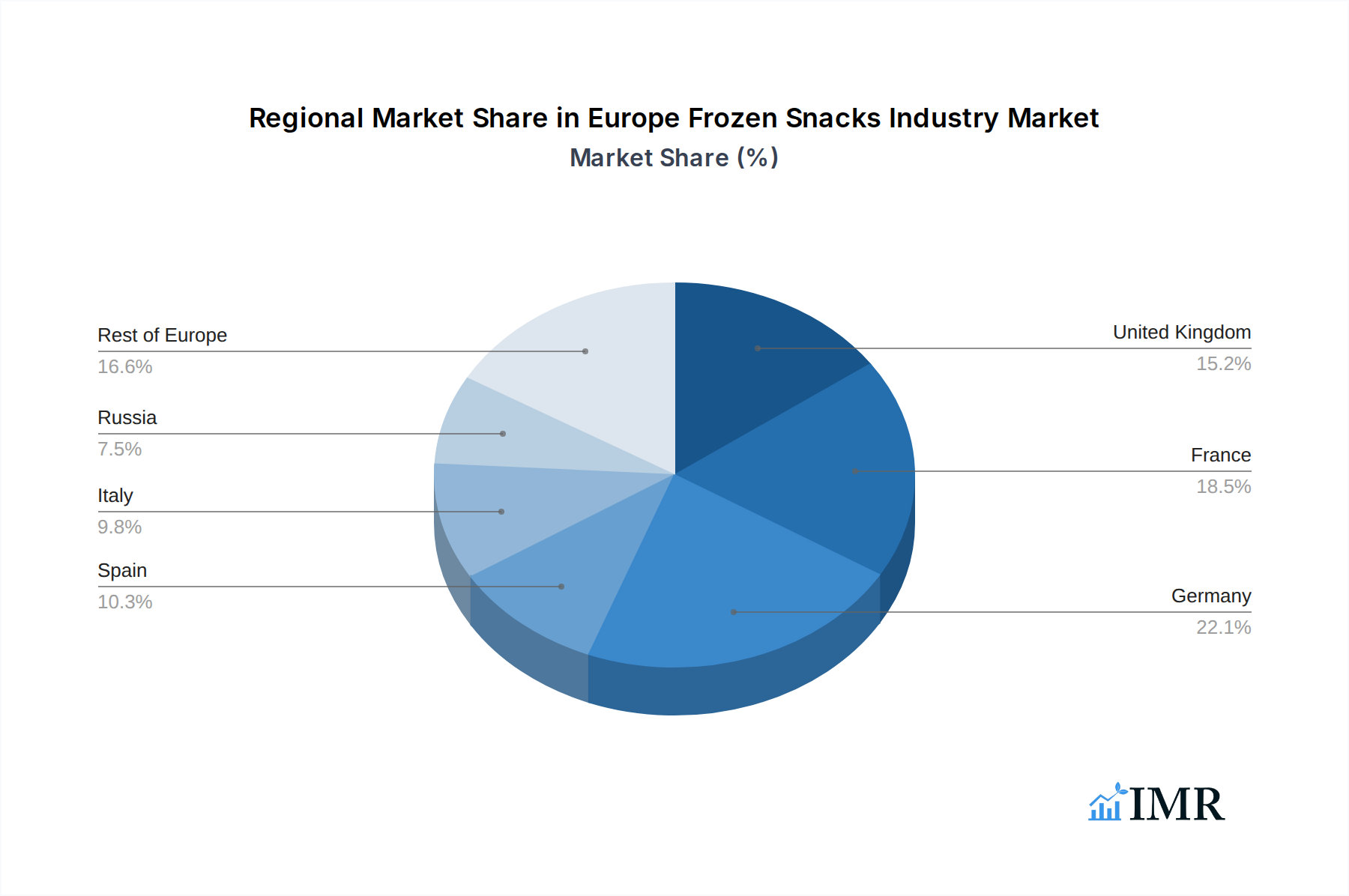

Regionally, Western Europe, particularly countries like the United Kingdom, Germany, and France, represent the most dominant markets due to higher disposable incomes, well-established retail infrastructure, and a mature consumer base accustomed to frozen food consumption.

- Dominance Factors for Western Europe:

- High Disposable Income: Affluent consumers have greater purchasing power for premium and convenience-oriented frozen snacks.

- Developed Retail Infrastructure: Extensive networks of supermarkets, hypermarkets, and specialized food retailers ensure widespread availability.

- Mature Consumer Acceptance: Frozen foods have long been a staple in Western European households, with high levels of trust and familiarity.

- Strong Food Manufacturing Base: The region hosts many leading frozen food manufacturers, driving innovation and product development.

- Growing Demand for Healthier Options: A significant portion of the population actively seeks healthier frozen snack alternatives, pushing manufacturers to innovate in this space.

Europe Frozen Snacks Industry Product Landscape

The Europe frozen snacks product landscape is marked by continuous innovation driven by evolving consumer preferences for health, convenience, and taste. From classic potato-based items and savory meat- and seafood-based options to expanding categories of fruit-based snacks and innovative "others" like vegan pastries, manufacturers are catering to diverse dietary needs and palates. Key advancements include improved freezing techniques that preserve texture and flavor, the incorporation of functional ingredients, and the development of plant-based alternatives. Performance metrics are increasingly evaluated by consumer satisfaction, nutritional value, and sustainability initiatives. Unique selling propositions often revolve around natural ingredients, allergen-free formulations, and unique flavor combinations.

Key Drivers, Barriers & Challenges in Europe Frozen Snacks Industry

The Europe frozen snacks industry is propelled by several key drivers, including the increasing demand for convenient food solutions driven by busy lifestyles, a growing consumer interest in healthier snack options, and continuous product innovation by manufacturers. Technological advancements in freezing and packaging technologies are enhancing product quality and shelf life, further stimulating growth.

- Key Drivers:

- Convenience and Time-Saving: Busy lifestyles favor quick and easy meal and snack solutions.

- Health and Wellness Trends: Growing demand for healthier, more nutritious, and plant-based frozen snacks.

- Product Innovation: Introduction of novel flavors, formats, and functional ingredients.

- Improved Freezing and Packaging Technology: Enhanced product quality, extended shelf life, and reduced waste.

However, the industry faces significant barriers and challenges. Fluctuations in raw material prices can impact profitability, while stringent food safety regulations and complex supply chains can increase operational costs and lead to potential disruptions. Intense competition from both established brands and emerging players, coupled with evolving consumer preferences for fresh alternatives, also presents considerable challenges.

- Barriers & Challenges:

- Raw Material Price Volatility: Unpredictable costs of ingredients can affect margins.

- Stringent Food Safety Regulations: Compliance with evolving standards adds complexity and cost.

- Supply Chain Complexities: Maintaining the cold chain and ensuring timely delivery across diverse regions.

- Intense Competition: Pressure from established players and new market entrants.

- Consumer Preference Shifts: Growing demand for fresh, minimally processed foods.

Emerging Opportunities in Europe Frozen Snacks Industry

Emerging opportunities within the Europe frozen snacks industry lie in the burgeoning demand for plant-based and vegan frozen snacks, catering to a growing segment of ethically conscious and health-aware consumers. The expansion of online retail channels and direct-to-consumer (DTC) models presents untapped market potential for niche brands and specialized product offerings. Furthermore, the development of "smart" frozen snacks with added health benefits, such as probiotics or fortified nutrients, aligns with current wellness trends and offers avenues for premiumization.

- Untapped Markets: Plant-based and vegan frozen snacks, specialty dietary needs.

- Innovative Applications: Functional frozen snacks with added health benefits, convenient meal solutions.

- Evolving Consumer Preferences: Demand for sustainable packaging and ethically sourced ingredients.

Growth Accelerators in the Europe Frozen Snacks Industry Industry

Long-term growth in the Europe frozen snacks industry is being accelerated by significant technological breakthroughs in cryogenic freezing and advanced atmospheric packaging, which are extending shelf life and improving product quality to near-fresh levels. Strategic partnerships between food manufacturers and technology providers are fostering the development of more sustainable production processes and innovative product formulations. Furthermore, aggressive market expansion strategies by key players into underserved Eastern European markets, coupled with a focus on product localization to meet regional taste preferences, are creating substantial growth momentum.

Key Players Shaping the Europe Frozen Snacks Industry Market

- Young's Seafood Limited

- Dr August Oetker KG

- Sudzucker AG

- Glendale Foods Limited

- Del Monte Foods Inc

- Nomad Foods Limited

- Cooperatie Koninklijke Cosun U A

- McCain Foods Limited

- Hain Celestial Group

Notable Milestones in Europe Frozen Snacks Industry Sector

- 2022/01: Nomad Foods acquires shares in a plant-based frozen food company, signaling a strategic move into the growing vegan market.

- 2023/03: McCain Foods launches an innovative range of seasoned sweet potato fries, tapping into the trend for healthier and flavorful potato snacks.

- 2023/07: Dr. August Oetker KG invests in new freezing technology to improve the texture and quality of its frozen pizza and snack offerings.

- 2024/02: Hain Celestial Group expands its gluten-free frozen snack portfolio, addressing the increasing demand from consumers with dietary restrictions.

- 2024/05: Sudzucker AG announces a partnership with a biotech firm to develop more sustainable and natural preservatives for frozen food products.

In-Depth Europe Frozen Snacks Industry Market Outlook

The outlook for the Europe frozen snacks industry remains exceptionally positive, driven by sustained consumer demand for convenience, coupled with a growing emphasis on health and wellness. Key growth accelerators include ongoing technological advancements in food preservation and the development of innovative, plant-based, and functional frozen snack options. Strategic market expansion into developing European regions and strategic partnerships aimed at enhancing sustainability and product diversification will further fuel this growth trajectory. The industry is well-positioned to capitalize on evolving consumer lifestyles, making it an attractive sector for investment and innovation in the coming years.

Europe Frozen Snacks Industry Segmentation

-

1. Type

- 1.1. Fruit-based Snacks

- 1.2. Potato-based Snacks

- 1.3. Meat- and Seafood-based Snacks

- 1.4. Others

-

2. Distribution Channel

- 2.1. Hypermarket/Supermarket

- 2.2. Convenience Stores

- 2.3. Online Retail Stores

- 2.4. Other Distribution Channels

Europe Frozen Snacks Industry Segmentation By Geography

- 1. United Kingdom

- 2. France

- 3. Germany

- 4. Spain

- 5. Italy

- 6. Russia

- 7. Rest of Europe

Europe Frozen Snacks Industry Regional Market Share

Geographic Coverage of Europe Frozen Snacks Industry

Europe Frozen Snacks Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Fruit-based Snacks

- 5.1.2. Potato-based Snacks

- 5.1.3. Meat- and Seafood-based Snacks

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Hypermarket/Supermarket

- 5.2.2. Convenience Stores

- 5.2.3. Online Retail Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. France

- 5.3.3. Germany

- 5.3.4. Spain

- 5.3.5. Italy

- 5.3.6. Russia

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Fruit-based Snacks

- 6.1.2. Potato-based Snacks

- 6.1.3. Meat- and Seafood-based Snacks

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Hypermarket/Supermarket

- 6.2.2. Convenience Stores

- 6.2.3. Online Retail Stores

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Kingdom Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Fruit-based Snacks

- 7.1.2. Potato-based Snacks

- 7.1.3. Meat- and Seafood-based Snacks

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Hypermarket/Supermarket

- 7.2.2. Convenience Stores

- 7.2.3. Online Retail Stores

- 7.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. France Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Fruit-based Snacks

- 8.1.2. Potato-based Snacks

- 8.1.3. Meat- and Seafood-based Snacks

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Hypermarket/Supermarket

- 8.2.2. Convenience Stores

- 8.2.3. Online Retail Stores

- 8.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Germany Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Fruit-based Snacks

- 9.1.2. Potato-based Snacks

- 9.1.3. Meat- and Seafood-based Snacks

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Hypermarket/Supermarket

- 9.2.2. Convenience Stores

- 9.2.3. Online Retail Stores

- 9.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Spain Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Fruit-based Snacks

- 10.1.2. Potato-based Snacks

- 10.1.3. Meat- and Seafood-based Snacks

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Hypermarket/Supermarket

- 10.2.2. Convenience Stores

- 10.2.3. Online Retail Stores

- 10.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Italy Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Fruit-based Snacks

- 11.1.2. Potato-based Snacks

- 11.1.3. Meat- and Seafood-based Snacks

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Hypermarket/Supermarket

- 11.2.2. Convenience Stores

- 11.2.3. Online Retail Stores

- 11.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Russia Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Fruit-based Snacks

- 12.1.2. Potato-based Snacks

- 12.1.3. Meat- and Seafood-based Snacks

- 12.1.4. Others

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Hypermarket/Supermarket

- 12.2.2. Convenience Stores

- 12.2.3. Online Retail Stores

- 12.2.4. Other Distribution Channels

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Rest of Europe Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Type

- 13.1.1. Fruit-based Snacks

- 13.1.2. Potato-based Snacks

- 13.1.3. Meat- and Seafood-based Snacks

- 13.1.4. Others

- 13.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 13.2.1. Hypermarket/Supermarket

- 13.2.2. Convenience Stores

- 13.2.3. Online Retail Stores

- 13.2.4. Other Distribution Channels

- 13.1. Market Analysis, Insights and Forecast - by Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Young's Seafood Limited

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 Dr August Oetker KG

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Sudzucker AG

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Glendale Foods Limited

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Del Monte Foods Inc*List Not Exhaustive

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Nomad Foods Limited

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Cooperatie Koninklijke Cosun U A

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 McCain Foods Limited

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Hain Celestial Group

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.1 Young's Seafood Limited

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Europe Frozen Snacks Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Frozen Snacks Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Europe Frozen Snacks Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 20: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 21: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 24: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Frozen Snacks Industry?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Europe Frozen Snacks Industry?

Key companies in the market include Young's Seafood Limited, Dr August Oetker KG, Sudzucker AG, Glendale Foods Limited, Del Monte Foods Inc*List Not Exhaustive, Nomad Foods Limited, Cooperatie Koninklijke Cosun U A, McCain Foods Limited, Hain Celestial Group.

3. What are the main segments of the Europe Frozen Snacks Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 153.91 billion as of 2022.

5. What are some drivers contributing to market growth?

The numerous benefits offered by collagen in the food and beverage industry.

6. What are the notable trends driving market growth?

Potato Snacks Emerged as a Prominent Segment.

7. Are there any restraints impacting market growth?

Increasing vegan population in the region.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Frozen Snacks Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Frozen Snacks Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Frozen Snacks Industry?

To stay informed about further developments, trends, and reports in the Europe Frozen Snacks Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence