Key Insights

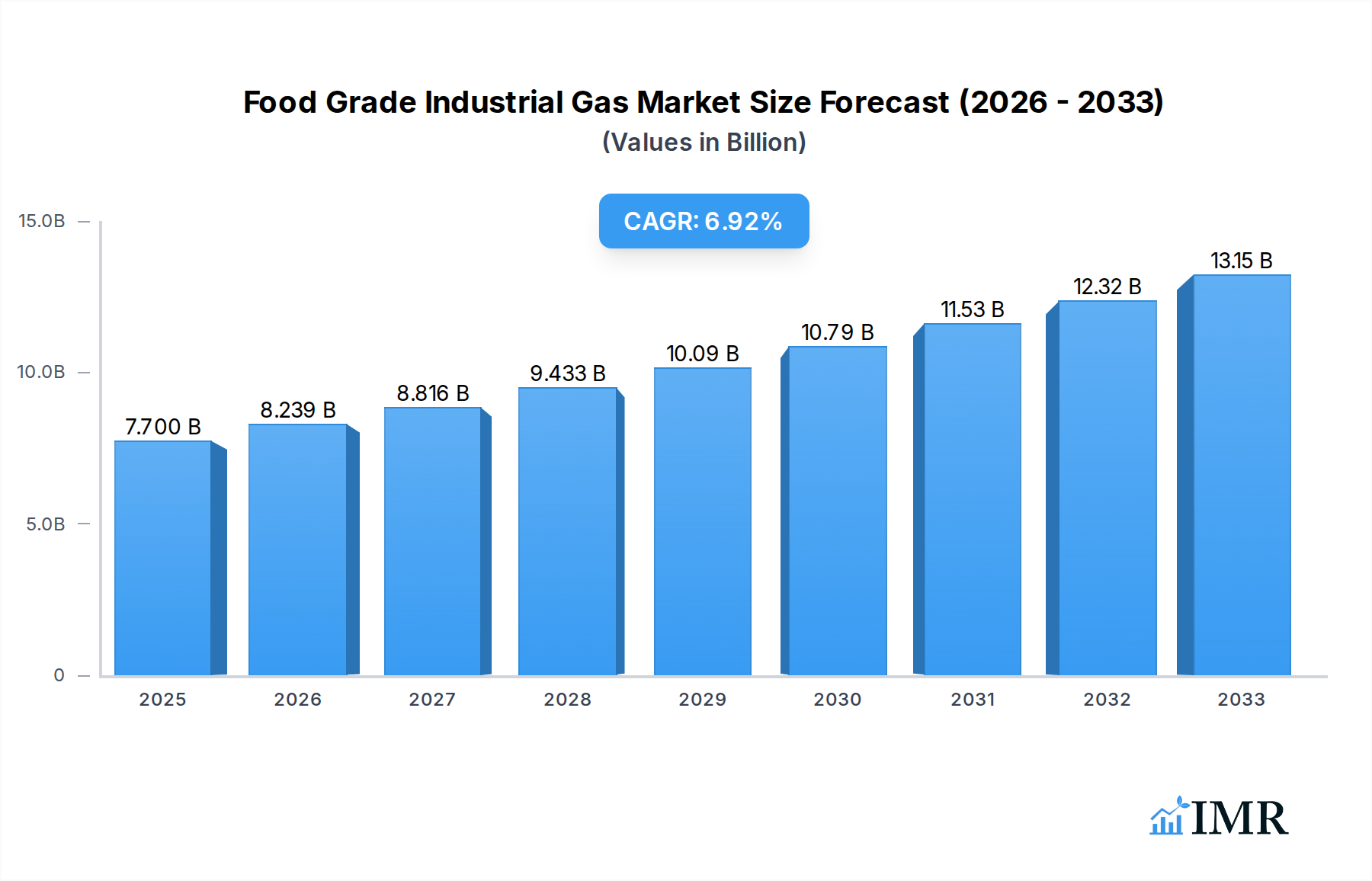

The Food Grade Industrial Gas market is poised for significant expansion, projected to reach an estimated $7.7 billion in 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 7% over the forecast period. This growth is largely fueled by the increasing demand for enhanced food preservation techniques, a rising emphasis on product quality and shelf-life extension, and the burgeoning global processed food industry. The application segment of Freezing & Chilling is a primary growth engine, directly benefiting from advancements in cryogenic freezing technologies that ensure optimal food quality and safety. Packaging applications also represent a substantial contributor, with modified atmosphere packaging (MAP) becoming increasingly prevalent to maintain freshness and extend the distribution reach of perishable goods.

Food Grade Industrial Gas Market Size (In Billion)

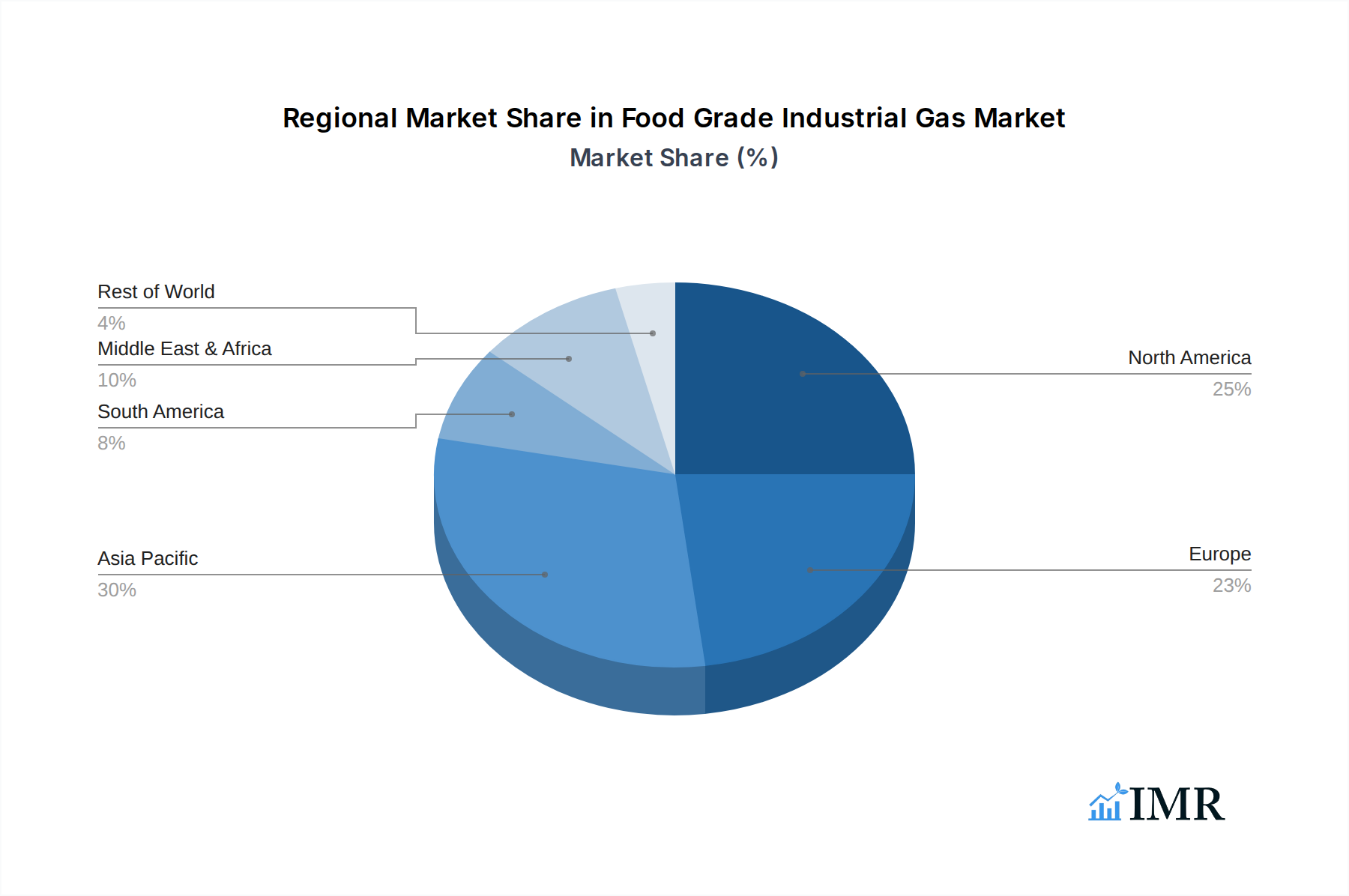

Emerging economies, particularly in the Asia Pacific and Middle East & Africa regions, are expected to exhibit the highest growth rates due to rapid industrialization, a growing middle class, and increasing consumer preference for packaged and processed food items. While the market is characterized by strong demand, challenges such as stringent regulatory compliance regarding gas purity and potential fluctuations in raw material prices for gas production could present moderate restraints. Key players like Air Liquide, Air Products & Chemicals, and Linde Group are actively investing in research and development to offer innovative gas solutions and expand their global manufacturing and distribution networks to cater to the escalating demand across diverse food applications.

Food Grade Industrial Gas Company Market Share

Here's the SEO-optimized report description for Food Grade Industrial Gas, structured and detailed as requested.

Food Grade Industrial Gas Market Dynamics & Structure

The global Food Grade Industrial Gas market is characterized by a moderate to high concentration, with major players like Air Liquide, Linde Group, Air Products & Chemicals, and Praxair Inc. dominating significant market shares. Technological innovation is a key driver, particularly in enhancing gas purity, developing novel delivery systems, and improving efficiency in applications like modified atmosphere packaging (MAP) and cryogenic freezing. Regulatory frameworks, set by bodies such as the FDA and EFSA, play a crucial role in dictating purity standards and permissible usage, influencing product development and market entry. Competitive product substitutes, while limited in direct functional replacement for core gases like CO2 and N2, can emerge in niche applications through alternative preservation techniques. End-user demographics reveal a growing demand from emerging economies and an increasing sophistication in processed and convenience food sectors. Merger and acquisition trends are evident, with larger entities consolidating their market presence and expanding their geographical reach to capitalize on growing demand. The M&A landscape is shaped by the pursuit of economies of scale, access to new technologies, and diversification of product portfolios. Innovation barriers include the substantial capital investment required for high-purity gas production and stringent regulatory compliance.

- Market Concentration: Dominated by a few key multinational corporations, alongside regional and specialized providers.

- Technological Innovation Drivers: Focus on purity, efficiency, advanced delivery systems, and novel applications.

- Regulatory Frameworks: Strict standards for food safety and quality influencing product development and market access.

- Competitive Product Substitutes: Limited direct replacements, but alternative preservation methods can pose indirect competition.

- End-User Demographics: Growth driven by processed food manufacturers, convenience food sector, and emerging markets.

- M&A Trends: Consolidation for market share, geographical expansion, and technological acquisition.

- Innovation Barriers: High capital costs for production, stringent quality control, and extensive regulatory approvals.

Food Grade Industrial Gas Growth Trends & Insights

The Food Grade Industrial Gas market is poised for substantial expansion, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% between 2025 and 2033. This robust growth trajectory is underpinned by a confluence of factors, including evolving consumer preferences towards safer, longer-lasting, and high-quality food products, alongside advancements in food processing technologies. The base year of 2025 signifies a dynamic market with established demand patterns and emerging growth engines. The historical period of 2019-2024 has laid the groundwork for this expansion, with increasing awareness of the benefits of food-grade industrial gases in preservation, packaging, and culinary applications.

The adoption rates for these gases are on an upward trend, particularly in regions with developing food supply chains and a burgeoning middle class. Technological disruptions are continuously shaping the market, with innovations in cryogenic freezing and chilling offering superior quality retention and reduced spoilage rates for perishable goods. Modified Atmosphere Packaging (MAP), a key application, is experiencing significant penetration as it extends shelf life, maintains freshness, and reduces the need for chemical preservatives, aligning with growing consumer demand for cleaner labels. Carbonation, another vital segment, continues to see steady demand driven by the beverage industry's innovation in flavored and functional drinks.

Consumer behavior shifts are profoundly impacting the market. There's a growing emphasis on food safety and traceability, making the controlled atmospheres provided by industrial gases increasingly valuable. Furthermore, the convenience food sector’s expansion directly correlates with the demand for packaging solutions that extend shelf life and maintain product integrity during transit and retail display. The estimated market size for food-grade industrial gases in 2025 is projected to be around $35.2 billion, with significant contributions from carbon dioxide, nitrogen, and oxygen. The forecast period (2025-2033) anticipates this figure to ascend, driven by the continuous need for efficient food preservation and processing techniques. The parent market, encompassing all industrial gases, provides a broader context of market scale, while the child market, specifically food-grade applications, highlights the specialized and growing demand within this sector. The increasing integration of these gases into advanced food manufacturing processes is a testament to their indispensable role in the modern food industry.

Dominant Regions, Countries, or Segments in Food Grade Industrial Gas

The global Food Grade Industrial Gas market is significantly influenced by the application segment of Freezing & Chilling, which is anticipated to be a dominant growth driver. This segment’s prominence is fueled by the increasing demand for frozen foods, convenience meals, and the need to maintain the freshness and quality of perishable goods throughout the supply chain. The Carbon Dioxide type is also a major contributor, largely due to its extensive use in carbonation for beverages and in cryogenic applications for rapid freezing and chilling.

In terms of regional dominance, North America and Europe currently lead the market, owing to their well-established food processing industries, stringent food safety regulations, and high consumer spending on quality and convenience food products. However, the Asia-Pacific region is exhibiting the fastest growth rate. This surge is propelled by a rapidly expanding population, increasing disposable incomes, a growing middle class with a preference for processed and packaged foods, and significant investments in modernizing food production and distribution infrastructure. Countries like China, India, and Southeast Asian nations are key to this regional expansion.

The Packaging segment, particularly Modified Atmosphere Packaging (MAP), is another critical application driving growth. MAP utilizes nitrogen and carbon dioxide to create an optimal atmosphere within food packaging, extending shelf life and preserving product quality without chemical additives. This aligns perfectly with evolving consumer preferences for healthier, cleaner-label products. The Oxygen type, while not as dominant as CO2 or Nitrogen in terms of volume for food-grade applications, plays a crucial role in certain packaging applications, particularly for red meats, where it helps maintain their desirable red color.

The dominance of these segments and regions is further amplified by several factors:

- Economic Policies: Favorable trade agreements and government initiatives promoting food processing and export in emerging economies accelerate market penetration.

- Infrastructure Development: Investments in cold chain logistics, modern food manufacturing plants, and efficient gas distribution networks are crucial enablers.

- Consumer Behavior: A rising awareness of food safety, a demand for longer shelf life, and the increasing consumption of ready-to-eat and convenient food options directly boost the demand for food-grade industrial gases.

- Technological Advancements: Innovations in gas production, purification, and delivery systems cater to the specific needs of the food industry, enhancing efficiency and product quality.

- Market Share & Growth Potential: The Freezing & Chilling application, driven by global demand for frozen and chilled products, holds a substantial market share and continues to exhibit strong growth potential. Similarly, the Asia-Pacific region, with its vast population and burgeoning food industry, represents the highest growth potential for the forecast period.

Food Grade Industrial Gas Product Landscape

The product landscape for Food Grade Industrial Gases is defined by its purity and specialized applications. Key offerings include high-purity Carbon Dioxide (CO2) for beverage carbonation, food freezing, and Modified Atmosphere Packaging (MAP); Nitrogen (N2) for inerting, freezing, chilling, and MAP; and Oxygen (O2) for specific MAP applications and active packaging. Emerging "Others" like Hydrogen (H2) are finding niche roles in hydrogenation processes and potentially in specialized food preservation. Innovations focus on achieving ultra-high purities (e.g., 99.999% and above) to meet stringent food safety standards and developing more efficient delivery systems, such as liquid cylinders and on-site generation units. Unique selling propositions include consistent quality, reliable supply chains, and tailored gas mixtures for specific food products. Technological advancements are also leading to improved gas blending capabilities for customized MAP solutions, enhancing product shelf life and visual appeal.

Key Drivers, Barriers & Challenges in Food Grade Industrial Gas

Key Drivers:

- Growing Demand for Processed & Packaged Foods: An increasing global consumer preference for convenience, longer shelf-life, and consistently high-quality food products directly fuels the need for industrial gases in preservation and packaging.

- Advancements in Food Preservation Technologies: Innovations in cryogenic freezing, chilling, and Modified Atmosphere Packaging (MAP) leverage industrial gases to improve food quality, reduce spoilage, and extend shelf life, aligning with consumer demand for healthier options.

- Stringent Food Safety Regulations: Global regulatory bodies mandate high standards for food safety and quality, encouraging the adoption of pure and reliable industrial gas solutions for production and preservation.

- Expansion of the Beverage Industry: The continuous innovation in carbonated beverages, including functional drinks and craft beverages, drives significant demand for food-grade carbon dioxide.

Barriers & Challenges:

- Supply Chain Volatility and Logistics: Ensuring a consistent and reliable supply of high-purity gases, especially to remote locations or during peak demand, presents logistical challenges and can lead to price fluctuations.

- High Capital Investment for Production: Setting up and maintaining facilities for producing high-purity food-grade industrial gases requires significant capital expenditure, acting as a barrier to entry for smaller players.

- Regulatory Compliance Costs: Adhering to diverse and evolving food safety regulations across different geographies incurs substantial compliance costs for manufacturers.

- Price Sensitivity of End-Users: While quality is paramount, the food industry can be price-sensitive, leading to pressure on gas suppliers to offer competitive pricing.

- Competition from Alternative Preservation Methods: While not direct replacements, advancements in other preservation technologies could, in some niche applications, pose indirect competition.

Emerging Opportunities in Food Grade Industrial Gas

Emerging opportunities in the Food Grade Industrial Gas market are centered around the growing demand for sustainable and natural food preservation methods, the expansion of the plant-based food sector, and advancements in smart packaging solutions. The increasing consumer focus on reduced food waste presents a significant opportunity for gases like nitrogen and carbon dioxide in extending shelf life and maintaining product integrity. The rapid growth of the ready-to-eat and meal kit delivery services also requires efficient preservation techniques, a role well-suited for industrial gases. Furthermore, untapped markets in developing economies, with their burgeoning middle classes and increasing adoption of Western dietary habits, offer substantial growth potential. The development of specialized gas mixtures for novel food products and the integration of industrial gas applications into advanced food manufacturing automation systems are also key areas for future expansion.

Growth Accelerators in the Food Grade Industrial Gas Industry

Several key catalysts are accelerating growth in the Food Grade Industrial Gas industry. Technological breakthroughs in cryogenic freezing are enabling faster and more efficient preservation, maintaining the texture and nutritional value of foods better than traditional methods. Strategic partnerships between industrial gas suppliers and food manufacturers are leading to the development of tailored solutions, optimizing gas usage for specific products and processes. Market expansion strategies, particularly in emerging economies, driven by increasing urbanization and a growing middle class with higher disposable incomes, are opening new avenues for demand. The development of on-site gas generation systems for large-scale food processors is also reducing logistical complexities and enhancing supply chain reliability, further boosting adoption.

Key Players Shaping the Food Grade Industrial Gas Market

- Air Liquide

- Air Products & Chemicals

- Linde Group

- Praxair Inc.

- Airgas

- Matheson Tri-Gas

- Messer Group

- SOL-SPa

- Emirates Industrial Gases

- Gulf CRYO

- AHG

- Taiyo Nippon Sanso

Notable Milestones in Food Grade Industrial Gas Sector

- 2019: Increased adoption of advanced Modified Atmosphere Packaging (MAP) technologies across Europe and North America for fresh produce and meat.

- 2020: Growth in cryogenic freezing applications for plant-based meat alternatives to maintain texture and appeal.

- 2021: Significant investments in expanding production capacity for high-purity food-grade carbon dioxide to meet rising beverage demand.

- 2022: Emergence of novel gas mixtures for extending the shelf life of ready-to-eat meals and convenience foods.

- 2023: Focus on sustainable gas sourcing and delivery methods to reduce the environmental footprint of food processing.

- 2024: Increased integration of AI and IoT for real-time monitoring and optimization of gas usage in food production lines.

In-Depth Food Grade Industrial Gas Market Outlook

The future of the Food Grade Industrial Gas market is exceptionally bright, driven by an intensified global focus on food safety, quality, and waste reduction. Growth accelerators such as ongoing innovations in cryogenic technologies and the expansion of the ready-to-eat food sector will continue to propel demand. Strategic partnerships between gas providers and food manufacturers will unlock new application potentials and optimize existing ones. The Asia-Pacific region, with its rapidly expanding food industry and increasing consumer sophistication, represents a significant area for future market expansion. The development of on-site generation solutions and the growing emphasis on sustainable gas production will further solidify the indispensable role of these gases in the global food supply chain, promising sustained growth and new opportunities.

Food Grade Industrial Gas Segmentation

-

1. Application

- 1.1. Freezing & Chilling

- 1.2. Packaging

- 1.3. Carbonation

- 1.4. Others

-

2. Type

- 2.1. Carbon Dioxide

- 2.2. Nitrogen

- 2.3. Oxygen

- 2.4. Others(Hydrogen and Argon)

Food Grade Industrial Gas Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Grade Industrial Gas Regional Market Share

Geographic Coverage of Food Grade Industrial Gas

Food Grade Industrial Gas REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Freezing & Chilling

- 5.1.2. Packaging

- 5.1.3. Carbonation

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Carbon Dioxide

- 5.2.2. Nitrogen

- 5.2.3. Oxygen

- 5.2.4. Others(Hydrogen and Argon)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Food Grade Industrial Gas Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Freezing & Chilling

- 6.1.2. Packaging

- 6.1.3. Carbonation

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Carbon Dioxide

- 6.2.2. Nitrogen

- 6.2.3. Oxygen

- 6.2.4. Others(Hydrogen and Argon)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Food Grade Industrial Gas Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Freezing & Chilling

- 7.1.2. Packaging

- 7.1.3. Carbonation

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Carbon Dioxide

- 7.2.2. Nitrogen

- 7.2.3. Oxygen

- 7.2.4. Others(Hydrogen and Argon)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Food Grade Industrial Gas Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Freezing & Chilling

- 8.1.2. Packaging

- 8.1.3. Carbonation

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Carbon Dioxide

- 8.2.2. Nitrogen

- 8.2.3. Oxygen

- 8.2.4. Others(Hydrogen and Argon)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Food Grade Industrial Gas Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Freezing & Chilling

- 9.1.2. Packaging

- 9.1.3. Carbonation

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Carbon Dioxide

- 9.2.2. Nitrogen

- 9.2.3. Oxygen

- 9.2.4. Others(Hydrogen and Argon)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Food Grade Industrial Gas Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Freezing & Chilling

- 10.1.2. Packaging

- 10.1.3. Carbonation

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Carbon Dioxide

- 10.2.2. Nitrogen

- 10.2.3. Oxygen

- 10.2.4. Others(Hydrogen and Argon)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Food Grade Industrial Gas Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Freezing & Chilling

- 11.1.2. Packaging

- 11.1.3. Carbonation

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Carbon Dioxide

- 11.2.2. Nitrogen

- 11.2.3. Oxygen

- 11.2.4. Others(Hydrogen and Argon)

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Air Liquide

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Air Products & Chemicals

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Linde Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Praxair Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Airgas

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Matheson Tri-Gas

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Messer Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 SOL-SPa

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Emirates Industrial Gases

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Gulf CRYO

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 AHG

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Taiyo Nippon Sanso

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Air Liquide

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Food Grade Industrial Gas Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Food Grade Industrial Gas Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Food Grade Industrial Gas Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Food Grade Industrial Gas Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Food Grade Industrial Gas Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Food Grade Industrial Gas Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Food Grade Industrial Gas Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Food Grade Industrial Gas Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Food Grade Industrial Gas Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Food Grade Industrial Gas Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Food Grade Industrial Gas Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Food Grade Industrial Gas Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Food Grade Industrial Gas Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Food Grade Industrial Gas Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Food Grade Industrial Gas Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Food Grade Industrial Gas Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Food Grade Industrial Gas Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Food Grade Industrial Gas Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Food Grade Industrial Gas Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Food Grade Industrial Gas Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Food Grade Industrial Gas Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Food Grade Industrial Gas Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Food Grade Industrial Gas Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Food Grade Industrial Gas Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Food Grade Industrial Gas Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Food Grade Industrial Gas Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Food Grade Industrial Gas Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Food Grade Industrial Gas Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Food Grade Industrial Gas Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Food Grade Industrial Gas Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Grade Industrial Gas Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Grade Industrial Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Food Grade Industrial Gas Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Food Grade Industrial Gas Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Food Grade Industrial Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Food Grade Industrial Gas Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Food Grade Industrial Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Food Grade Industrial Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Food Grade Industrial Gas Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Food Grade Industrial Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Food Grade Industrial Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Food Grade Industrial Gas Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Food Grade Industrial Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Food Grade Industrial Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Food Grade Industrial Gas Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Food Grade Industrial Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Food Grade Industrial Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Food Grade Industrial Gas Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Food Grade Industrial Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Food Grade Industrial Gas Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Grade Industrial Gas?

The projected CAGR is approximately 7%.

2. Which companies are prominent players in the Food Grade Industrial Gas?

Key companies in the market include Air Liquide, Air Products & Chemicals, Linde Group, Praxair Inc, Airgas, Matheson Tri-Gas, Messer Group, SOL-SPa, Emirates Industrial Gases, Gulf CRYO, AHG, Taiyo Nippon Sanso.

3. What are the main segments of the Food Grade Industrial Gas?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Grade Industrial Gas," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Grade Industrial Gas report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Grade Industrial Gas?

To stay informed about further developments, trends, and reports in the Food Grade Industrial Gas, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence