Key Insights

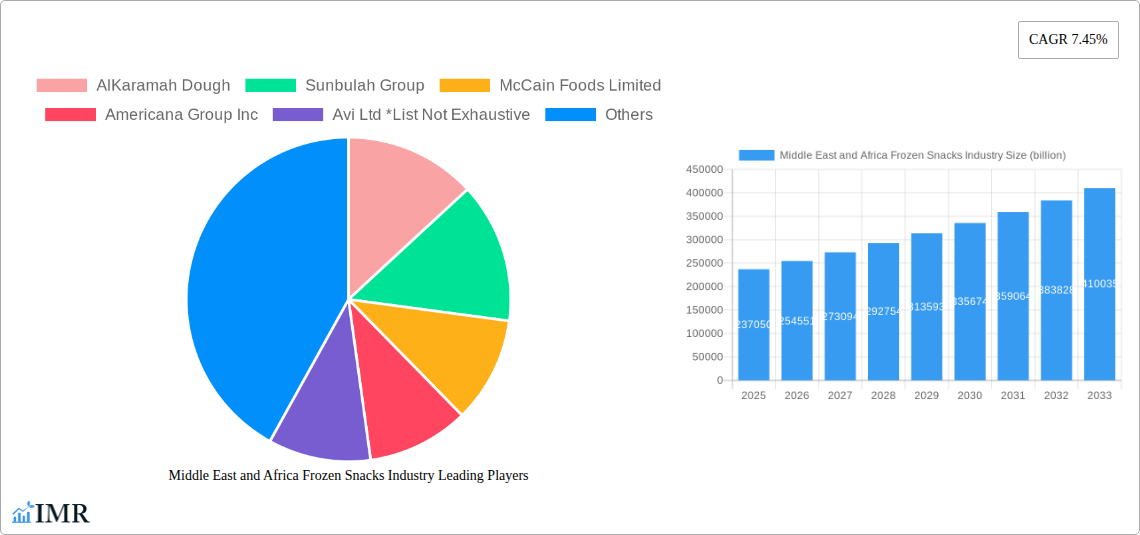

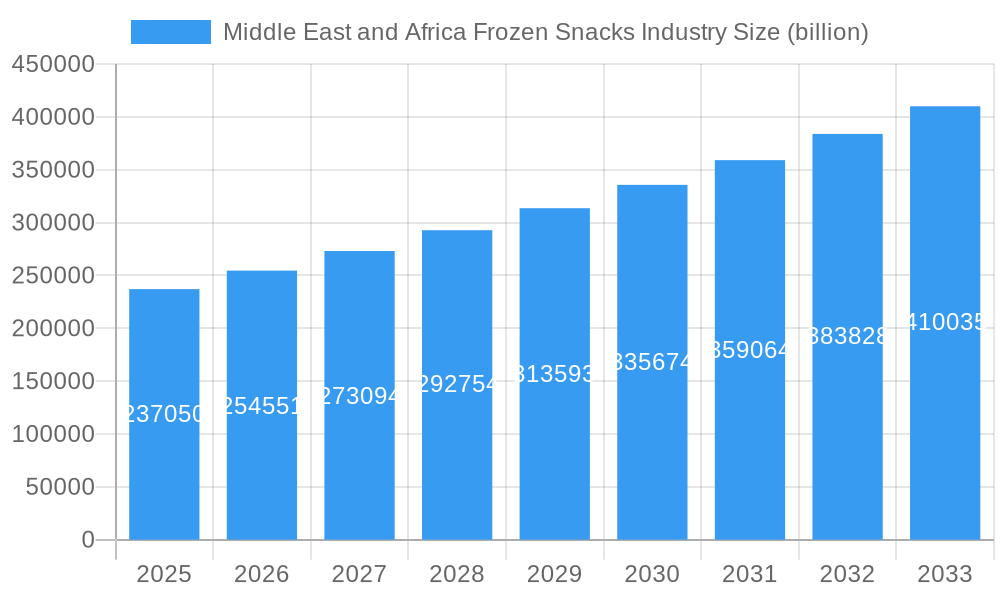

The Middle East and Africa (MEA) Frozen Snacks Industry is poised for robust expansion, with an estimated market size of $237.05 billion in 2025 and a projected Compound Annual Growth Rate (CAGR) of 7.45% through 2033. This significant growth is propelled by a confluence of evolving consumer lifestyles, increasing disposable incomes, and a rising demand for convenient, ready-to-eat food options across the region. The penetration of modern retail formats like hypermarkets and supermarkets, coupled with the burgeoning online retail sector, is further facilitating wider accessibility to frozen snack products. Key drivers fueling this market include urbanization, a growing young population with a preference for on-the-go consumption, and the increasing adoption of Western dietary habits. The "others" segment, encompassing a diverse range of innovative frozen snacks beyond traditional fruit, potato, and meat varieties, is anticipated to witness particularly strong uptake as manufacturers introduce novel products catering to evolving palates and dietary preferences.

Middle East and Africa Frozen Snacks Industry Market Size (In Billion)

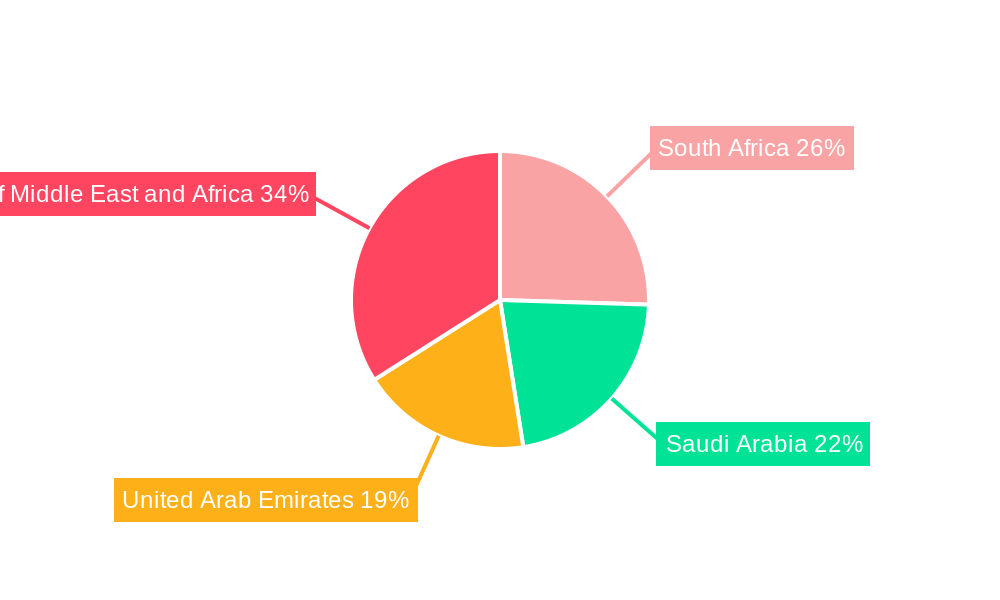

The MEA Frozen Snacks Industry is characterized by distinct regional dynamics, with South Africa, Saudi Arabia, and the United Arab Emirates emerging as key consumption hubs. The "Meat- and Seafood-based Snacks" and "Fruit-based Snacks" segments are expected to dominate the market share due to established consumer preferences and a wide array of product offerings. However, "Potato-based Snacks" are also experiencing steady growth, driven by their widespread popularity. Challenges for the industry include fluctuating raw material prices and the need for robust cold chain logistics to maintain product quality and safety, particularly in more remote areas. Nevertheless, the overall outlook remains highly positive, with strategic investments in product innovation, distribution network expansion, and marketing efforts by leading companies like McCain Foods Limited and Americana Group Inc. expected to further consolidate market growth and capitalize on unmet consumer needs.

Middle East and Africa Frozen Snacks Industry Company Market Share

Unlocking the Frozen Snacks Boom: Middle East and Africa Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Middle East and Africa Frozen Snacks Industry, forecasting robust growth from 2019-2033. Dive into market dynamics, emerging trends, and strategic opportunities within this rapidly expanding sector. Understand the competitive landscape, consumer preferences, and technological advancements shaping the future of frozen convenience food across the MEA region.

Middle East and Africa Frozen Snacks Industry Market Dynamics & Structure

The Middle East and Africa (MEA) frozen snacks market is characterized by a dynamic interplay of evolving consumer preferences, increasing disposable incomes, and expanding retail infrastructure. Market concentration is moderate, with several key players vying for dominance, but a growing number of regional and niche manufacturers are emerging. Technological innovation is a significant driver, focusing on product development for healthier options, extended shelf life, and convenient preparation methods. Regulatory frameworks, while varying across countries, are increasingly emphasizing food safety standards and labeling requirements, influencing product formulations and packaging. Competitive product substitutes include fresh snacks, ready-to-eat meals, and other convenience food options, necessitating continuous innovation and differentiation. End-user demographics reveal a growing demand from urban populations, younger consumers seeking quick meal solutions, and expatriate communities accustomed to a wider variety of frozen food products. Mergers and acquisitions (M&A) are expected to play a crucial role in market consolidation and expansion, with companies seeking to acquire complementary technologies, distribution networks, and product portfolios.

- Market Concentration: Moderate, with established global players and a growing presence of local manufacturers.

- Technological Innovation Drivers: Healthier ingredients, improved freezing techniques, advanced packaging, and ready-to-cook solutions.

- Regulatory Frameworks: Focus on food safety, quality control, and clear labeling standards across the region.

- Competitive Product Substitutes: Fresh snacks, bakery items, ready-to-eat meals, and other convenience food categories.

- End-User Demographics: Urban dwellers, millennials and Gen Z, busy professionals, and families seeking convenient meal options.

- M&A Trends: Strategic acquisitions to gain market share, access new product lines, and expand geographical reach. Potential for significant M&A activity in the coming years, driven by the attractive growth prospects.

Middle East and Africa Frozen Snacks Industry Growth Trends & Insights

The MEA frozen snacks market is poised for substantial expansion, driven by a confluence of demographic shifts, economic development, and evolving consumer lifestyles. The market size is projected to witness a significant Compound Annual Growth Rate (CAGR) from its base year value of $10.5 billion in 2025, with a forecast to reach an estimated $25.7 billion by 2033. This impressive growth trajectory is fueled by increasing urbanization, rising disposable incomes, and a growing preference for convenient food solutions among the region's burgeoning population. Adoption rates for frozen snacks are steadily increasing as consumers become more receptive to the convenience and variety offered. Technological disruptions are playing a pivotal role, with innovations in freezing technologies, product formulation (e.g., plant-based options, reduced sodium), and packaging enhancing product appeal and accessibility. Consumer behavior shifts are also a key factor; the fast-paced lifestyle in many MEA cities necessitates quick and easy meal preparation, making frozen snacks an attractive option. Furthermore, a growing awareness of food safety and quality is driving demand for well-packaged and processed frozen goods. The market penetration of frozen snacks is expected to deepen, moving beyond traditional consumption patterns to become a staple in many households across the region. The historical period (2019-2024) has laid a strong foundation, demonstrating consistent demand growth, with an estimated market size of $9.2 billion in 2024. This solid performance underscores the inherent potential and resilience of the MEA frozen snacks industry.

Dominant Regions, Countries, or Segments in Middle East and Africa Frozen Snacks Industry

The Middle East and Africa Frozen Snacks Industry is experiencing robust growth, with several key segments and geographies driving this expansion. Among the Types of frozen snacks, Potato-based Snacks are currently dominating the market, accounting for an estimated 45% of the market share in 2025, valued at approximately $4.7 billion. This dominance is attributed to their widespread popularity, versatility, and the established supply chains for potato cultivation in several MEA countries. Meat- and Seafood-based Snacks represent a significant secondary segment, holding an estimated 25% market share ($2.6 billion in 2025), driven by a strong protein-centric diet in many regions. Fruit-based snacks are a growing niche, with an estimated 15% market share ($1.6 billion), catering to evolving health consciousness.

In terms of Distribution Channels, Hypermarkets/Supermarkets are the leading channel, commanding an estimated 55% market share ($5.8 billion in 2025). Their extensive reach, product variety, and promotional activities make them the primary point of purchase for frozen snacks. Online retail stores are rapidly gaining traction, projected to capture 20% of the market share by 2025 ($2.1 billion), a testament to the growing e-commerce adoption in the region.

Geographically, Saudi Arabia is emerging as a dominant country, projected to hold approximately 30% of the total MEA frozen snacks market share by 2025, estimated at $3.2 billion. This is driven by a large and affluent population, a growing expatriate community with diverse culinary preferences, and significant investments in retail infrastructure. The United Arab Emirates is another major contributor, with an estimated 25% market share ($2.6 billion in 2025), benefiting from a highly developed retail sector and a large cosmopolitan population. South Africa follows, with an estimated 20% market share ($2.1 billion), driven by its established food processing industry and a significant consumer base. The Rest of Middle East and Africa collectively represents the remaining market share, offering substantial untapped potential for growth.

- Dominant Segments (Type):

- Potato-based Snacks: Estimated 45% market share ($4.7 billion in 2025).

- Meat- and Seafood-based Snacks: Estimated 25% market share ($2.6 billion in 2025).

- Fruit-based Snacks: Growing segment with an estimated 15% market share ($1.6 billion in 2025).

- Dominant Distribution Channels:

- Hypermarket/Supermarket: Estimated 55% market share ($5.8 billion in 2025).

- Online Retail Stores: Rapidly growing segment, projected 20% market share ($2.1 billion in 2025).

- Dominant Geographies:

- Saudi Arabia: Leading market with an estimated 30% share ($3.2 billion in 2025).

- United Arab Emirates: Significant contributor with an estimated 25% share ($2.6 billion in 2025).

- South Africa: Established market with an estimated 20% share ($2.1 billion in 2025).

Middle East and Africa Frozen Snacks Industry Product Landscape

The MEA frozen snacks market is witnessing a surge in product innovation, driven by consumer demand for healthier, more convenient, and diverse options. Manufacturers are actively developing a wider array of frozen snacks, from innovative fruit-based bites and healthier potato alternatives to premium meat and seafood preparations. Applications are expanding beyond traditional snacking occasions to encompass quick meal solutions and appetizer offerings. Performance metrics such as extended shelf life, improved taste profiles post-heating, and enhanced nutritional content are key focus areas. Unique selling propositions often revolve around natural ingredients, reduced fat and sodium content, and convenient single-serving packs. Technological advancements in freezing methods, such as Individual Quick Freezing (IQF), are preserving texture and flavor, while smart packaging solutions are enhancing consumer experience and shelf visibility.

Key Drivers, Barriers & Challenges in Middle East and Africa Frozen Snacks Industry

Key Drivers: The MEA frozen snacks industry is propelled by several significant drivers. Increasing disposable incomes and a growing middle class are boosting consumer spending on convenience food. Urbanization and fast-paced lifestyles create a demand for quick and easy meal solutions. A rising expatriate population introduces diverse palates and a familiarity with frozen food products. Advancements in cold chain logistics and retail infrastructure are improving accessibility and product availability across the region. Furthermore, a growing health consciousness is driving demand for healthier frozen snack options, such as those with reduced fat and sodium or plant-based ingredients.

Key Barriers & Challenges: Despite the positive outlook, the industry faces several hurdles. High initial investment costs for freezing technology and cold storage infrastructure can be a barrier for smaller players. Fluctuations in raw material prices, particularly for key ingredients like potatoes and meat, can impact profitability. Stringent and varying food safety regulations across different MEA countries can pose compliance challenges. Intense competition from traditional snacks and fresh food alternatives necessitates continuous product innovation and marketing efforts. Supply chain disruptions, especially in remote areas, can affect product availability and freshness. Educating consumers about the benefits and safety of frozen snacks is also an ongoing challenge in some markets.

Emerging Opportunities in Middle East and Africa Frozen Snacks Industry

Emerging opportunities in the MEA frozen snacks market lie in catering to evolving consumer preferences for healthier and more sustainable options. The demand for plant-based and vegan frozen snacks is on the rise, presenting a significant growth avenue. Innovations in functional frozen snacks, fortified with vitamins or probiotics, are expected to gain traction. Untapped markets within the African continent, with their burgeoning youth populations and increasing urbanization, offer substantial potential for market penetration. The development of region-specific flavors and product formats will be crucial for capturing local market share. Furthermore, the growing e-commerce landscape presents opportunities for direct-to-consumer sales and specialized online frozen food retailers.

Growth Accelerators in the Middle East and Africa Frozen Snacks Industry Industry

Several catalysts are accelerating the long-term growth of the MEA frozen snacks industry. Significant investments in cold chain infrastructure and logistics by governments and private entities are crucial for expanding reach and reducing post-harvest losses. Technological breakthroughs in freezing, preservation, and packaging are enhancing product quality and extending shelf life, making frozen snacks more appealing. Strategic partnerships between international frozen food manufacturers and local distributors are facilitating market entry and expansion. Government initiatives promoting food processing and manufacturing also contribute to industry growth. The continuous introduction of innovative product lines that cater to specific dietary needs and preferences will also act as a major growth accelerator.

Key Players Shaping the Middle East and Africa Frozen Snacks Industry Market

- AlKaramah Dough

- Sunbulah Group

- McCain Foods Limited

- Americana Group Inc

- Avi Ltd

- BRF SA

- Al Kabeer Group ME

- JBS SA

Notable Milestones in Middle East and Africa Frozen Snacks Industry Sector

- 2022: Sunbulah Group expands its frozen pastry and snack portfolio with new product launches catering to evolving consumer tastes.

- 2023: McCain Foods Limited strengthens its presence in the UAE with enhanced distribution networks for its potato-based frozen snacks.

- 2024 (Q1): Americana Group Inc announces strategic investments in expanding its frozen food production capacity to meet growing regional demand.

- 2024 (Q2): Al Kabeer Group ME introduces a range of innovative meat-based frozen snacks targeting health-conscious consumers.

- 2024 (Q3): BRF SA explores new market entry strategies in North African countries for its frozen convenience foods.

In-Depth Middle East and Africa Frozen Snacks Industry Market Outlook

The future outlook for the Middle East and Africa frozen snacks industry is exceptionally bright, driven by sustained economic development, rapid urbanization, and a growing demand for convenient, high-quality food options. Growth accelerators such as continuous technological advancements in food processing and preservation, coupled with significant investments in cold chain infrastructure, will further bolster market expansion. Strategic partnerships and an increasing focus on product innovation, particularly in healthier and plant-based alternatives, will cater to diverse consumer needs and preferences. The expanding e-commerce sector will also unlock new avenues for market reach and direct consumer engagement. The MEA frozen snacks market is poised for significant value creation, presenting lucrative opportunities for both established players and emerging entrants to capitalize on this dynamic and rapidly evolving landscape.

Middle East and Africa Frozen Snacks Industry Segmentation

-

1. Type

- 1.1. Fruit-based Snacks

- 1.2. Potato-based Snacks

- 1.3. Meat- and Seafood-based Snacks

- 1.4. Others

-

2. Distribution Channel

- 2.1. Hypermarket/Supermarket

- 2.2. Convenience Stores

- 2.3. Online Retail Stores

- 2.4. Other Distribution Channels

-

3. Geography

- 3.1. South Africa

- 3.2. Saudi Arabia

- 3.3. United Arab Emirates

- 3.4. Rest of Middle East and Africa

Middle East and Africa Frozen Snacks Industry Segmentation By Geography

- 1. South Africa

- 2. Saudi Arabia

- 3. United Arab Emirates

- 4. Rest of Middle East and Africa

Middle East and Africa Frozen Snacks Industry Regional Market Share

Geographic Coverage of Middle East and Africa Frozen Snacks Industry

Middle East and Africa Frozen Snacks Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.45% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Fruit-based Snacks

- 5.1.2. Potato-based Snacks

- 5.1.3. Meat- and Seafood-based Snacks

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Hypermarket/Supermarket

- 5.2.2. Convenience Stores

- 5.2.3. Online Retail Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. South Africa

- 5.3.2. Saudi Arabia

- 5.3.3. United Arab Emirates

- 5.3.4. Rest of Middle East and Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. South Africa

- 5.4.2. Saudi Arabia

- 5.4.3. United Arab Emirates

- 5.4.4. Rest of Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Middle East and Africa Frozen Snacks Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Fruit-based Snacks

- 6.1.2. Potato-based Snacks

- 6.1.3. Meat- and Seafood-based Snacks

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Hypermarket/Supermarket

- 6.2.2. Convenience Stores

- 6.2.3. Online Retail Stores

- 6.2.4. Other Distribution Channels

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. South Africa

- 6.3.2. Saudi Arabia

- 6.3.3. United Arab Emirates

- 6.3.4. Rest of Middle East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South Africa Middle East and Africa Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Fruit-based Snacks

- 7.1.2. Potato-based Snacks

- 7.1.3. Meat- and Seafood-based Snacks

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Hypermarket/Supermarket

- 7.2.2. Convenience Stores

- 7.2.3. Online Retail Stores

- 7.2.4. Other Distribution Channels

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. South Africa

- 7.3.2. Saudi Arabia

- 7.3.3. United Arab Emirates

- 7.3.4. Rest of Middle East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Saudi Arabia Middle East and Africa Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Fruit-based Snacks

- 8.1.2. Potato-based Snacks

- 8.1.3. Meat- and Seafood-based Snacks

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Hypermarket/Supermarket

- 8.2.2. Convenience Stores

- 8.2.3. Online Retail Stores

- 8.2.4. Other Distribution Channels

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. South Africa

- 8.3.2. Saudi Arabia

- 8.3.3. United Arab Emirates

- 8.3.4. Rest of Middle East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. United Arab Emirates Middle East and Africa Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Fruit-based Snacks

- 9.1.2. Potato-based Snacks

- 9.1.3. Meat- and Seafood-based Snacks

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Hypermarket/Supermarket

- 9.2.2. Convenience Stores

- 9.2.3. Online Retail Stores

- 9.2.4. Other Distribution Channels

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. South Africa

- 9.3.2. Saudi Arabia

- 9.3.3. United Arab Emirates

- 9.3.4. Rest of Middle East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of Middle East and Africa Middle East and Africa Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Fruit-based Snacks

- 10.1.2. Potato-based Snacks

- 10.1.3. Meat- and Seafood-based Snacks

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Hypermarket/Supermarket

- 10.2.2. Convenience Stores

- 10.2.3. Online Retail Stores

- 10.2.4. Other Distribution Channels

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. South Africa

- 10.3.2. Saudi Arabia

- 10.3.3. United Arab Emirates

- 10.3.4. Rest of Middle East and Africa

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 AlKaramah Dough

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Sunbulah Group

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 McCain Foods Limited

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Americana Group Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Avi Ltd *List Not Exhaustive

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 BRF SA

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Al Kabeer Group ME

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 JBS SA

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.1 AlKaramah Dough

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Frozen Snacks Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Frozen Snacks Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 7: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 19: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: Middle East and Africa Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Frozen Snacks Industry?

The projected CAGR is approximately 7.45%.

2. Which companies are prominent players in the Middle East and Africa Frozen Snacks Industry?

Key companies in the market include AlKaramah Dough, Sunbulah Group, McCain Foods Limited, Americana Group Inc, Avi Ltd *List Not Exhaustive, BRF SA, Al Kabeer Group ME, JBS SA.

3. What are the main segments of the Middle East and Africa Frozen Snacks Industry?

The market segments include Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 237.05 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Functional and Fortified Food; Multi-functionality and Wide Application of Riboflavin.

6. What are the notable trends driving market growth?

Increase in Demand for Ready-To-Cook Meat Products.

7. Are there any restraints impacting market growth?

Low Stability of Riboflavin on Exposure to Light and Heat.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Frozen Snacks Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Frozen Snacks Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Frozen Snacks Industry?

To stay informed about further developments, trends, and reports in the Middle East and Africa Frozen Snacks Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence