Key Insights

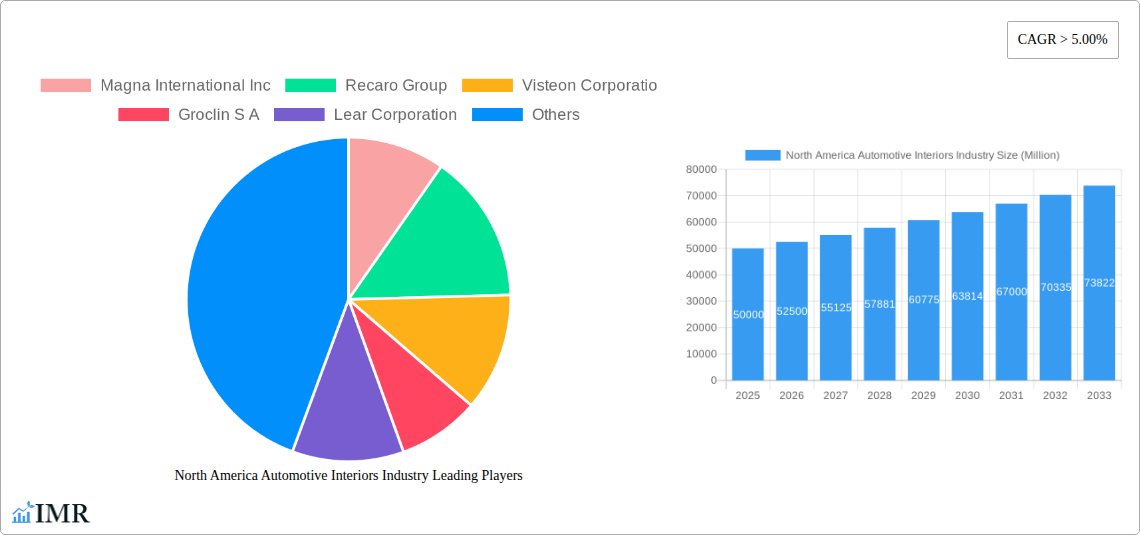

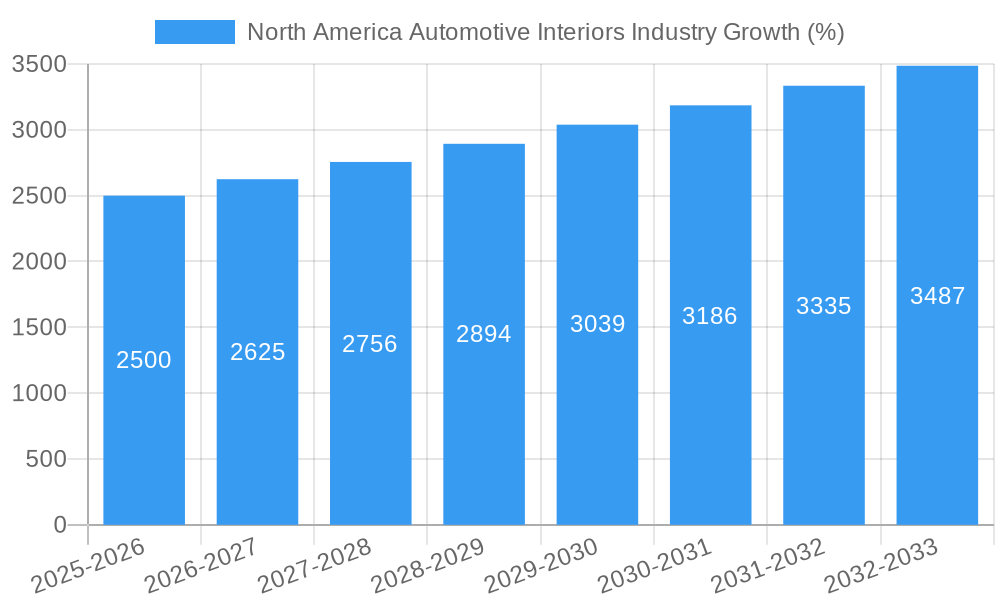

The North American automotive interiors market is experiencing robust growth, driven by increasing vehicle production, rising consumer demand for enhanced comfort and luxury features, and the integration of advanced technologies. The market, valued at approximately $50 billion in 2025, is projected to maintain a Compound Annual Growth Rate (CAGR) exceeding 5% through 2033. This expansion is fueled by several key trends, including the rising popularity of SUVs and light trucks, which typically feature more elaborate interiors, and the growing adoption of advanced driver-assistance systems (ADAS) and in-car infotainment systems. The demand for sustainable and eco-friendly materials is also shaping the market, with manufacturers increasingly incorporating recycled and bio-based components. Segment-wise, passenger cars currently dominate the market share, but commercial vehicles are expected to witness faster growth due to increased investment in fleet modernization and enhanced driver experience. Within components, infotainment systems and instrument panels hold significant market shares, although interior lighting and other advanced features are witnessing substantial growth, driven by technological advancements and consumer preferences. The competitive landscape is marked by the presence of both Tier-1 automotive suppliers and specialized component manufacturers, leading to intense innovation and competitive pricing.

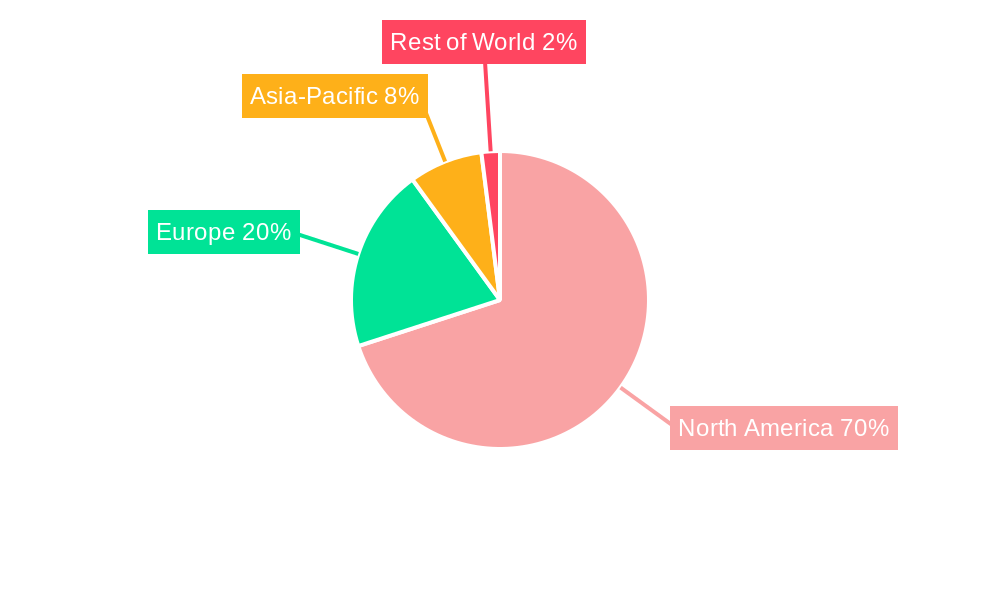

Geographic segmentation reveals the United States as the largest market within North America, followed by Canada. However, the Rest of North America region also presents significant growth potential, driven by increasing automotive production and rising disposable incomes. Despite the positive outlook, the market faces some challenges. Supply chain disruptions, fluctuations in raw material prices, and economic uncertainties represent potential restraints to growth. However, the long-term outlook remains positive, driven by the sustained demand for vehicles and the ongoing integration of sophisticated interior features within the automotive landscape. Major players like Magna International, Lear Corporation, and Faurecia are investing heavily in research and development to stay ahead of the competition and meet evolving consumer needs. This combination of strong growth drivers, technological advancements, and ongoing investments positions the North American automotive interiors market for continued expansion in the coming years.

North America Automotive Interiors Industry: Market Analysis and Forecast (2019-2033)

This comprehensive report provides an in-depth analysis of the North America automotive interiors market, covering the period 2019-2033. With a focus on key segments, leading players, and emerging trends, this report is an essential resource for industry professionals, investors, and strategic decision-makers. The study utilizes data from the historical period (2019-2024), a base year of 2025, and an estimated year of 2025 to project the forecast period (2025-2033). Market values are presented in million units.

North America Automotive Interiors Industry Market Dynamics & Structure

The North American automotive interiors market is characterized by a moderately consolidated structure with several major players controlling a significant market share. Magna International Inc., Lear Corporation, and Adient PLC are among the dominant players, each holding a substantial portion of the overall market. Market concentration is expected to remain relatively stable during the forecast period, although strategic acquisitions and partnerships could lead to some shifts in market share. Technological innovation, particularly in areas such as advanced driver-assistance systems (ADAS) and connected car technologies, is a primary driver of growth. Stringent regulatory frameworks concerning safety and emissions standards also influence market dynamics, pushing manufacturers towards the adoption of innovative materials and technologies. The market also faces competition from substitute products, especially in the infotainment segment, as technology allows integration of smartphone features. Consumer preferences for customization and enhanced comfort are shaping demand, while mergers and acquisitions (M&A) activities are reshaping the competitive landscape. The average annual volume of M&A deals within the industry between 2019 and 2024 was approximately xx.

- Market Concentration: Moderately consolidated, with top 3 players holding xx% market share in 2024.

- Technological Innovation: Focus on lightweight materials, sustainable interiors, and advanced features.

- Regulatory Landscape: Stringent safety and emission regulations driving innovation.

- Competitive Substitutes: Smartphone integration and alternative infotainment systems posing challenges.

- M&A Activity: xx deals annually on average between 2019-2024, leading to market consolidation and strategic shifts.

North America Automotive Interiors Industry Growth Trends & Insights

The North American automotive interiors market experienced consistent growth from 2019 to 2024, driven by factors such as rising vehicle production and increasing demand for advanced features. The market size expanded from xx million units in 2019 to xx million units in 2024, registering a CAGR of xx%. This growth is anticipated to continue during the forecast period, albeit at a slightly moderated pace due to economic uncertainties and supply chain disruptions. The adoption rate of advanced interior features, such as augmented reality head-up displays and personalized ambient lighting, is accelerating, fueled by increasing consumer preference for enhanced in-car experiences. Technological disruptions, such as the increasing integration of software and electronics into vehicle interiors, are reshaping the industry landscape. Consumer behavior shifts towards sustainability and personalization are also creating new opportunities for innovative material solutions and customization options.

The market is expected to reach xx million units by 2033, with a projected CAGR of xx% from 2025 to 2033. Market penetration of advanced features is expected to reach xx% by 2033.

Dominant Regions, Countries, or Segments in North America Automotive Interiors Industry

The United States dominates the North American automotive interiors market, accounting for approximately xx% of the total market in 2024. This dominance is primarily driven by its large automotive manufacturing base, high vehicle sales, and strong consumer demand for advanced features. Canada contributes a significant share, while the Rest of North America represents a smaller, yet growing, segment. Within vehicle types, passenger cars constitute the largest segment, reflecting the higher volume of passenger vehicle production in the region. The infotainment system segment holds the largest share among component types due to the rising popularity of connected car features and advanced infotainment systems.

By Country:

- United States: Largest market share due to high vehicle production and strong consumer demand.

- Canada: Significant contributor due to its automotive industry and proximity to the US market.

- Rest of North America: Smaller market with growth potential.

By Vehicle Type:

- Passenger Cars: Largest segment driven by high production volume.

- Commercial Vehicles: Smaller but growing segment, driven by demand for specialized features.

By Component Type:

- Infotainment System: Largest segment due to increasing demand for connected car features.

- Instrument Panels: Significant segment driven by safety and regulatory requirements.

- Interior Lighting: Growing segment due to rising adoption of ambient and functional lighting.

- Others: Includes seats, trim, and other components.

North America Automotive Interiors Industry Product Landscape

The automotive interiors product landscape is characterized by a wide range of components and features, offering a spectrum of functionalities and aesthetics. Innovations include lightweight, sustainable materials, advanced driver-assistance system (ADAS) integration for enhanced safety and convenience, and sophisticated infotainment systems integrating cloud-based services and personalized entertainment options. Key performance metrics include durability, safety compliance, ergonomic design, and integration capabilities with other vehicle systems. Unique selling propositions often include customization, improved comfort, and integration of advanced technology, offering manufacturers a competitive edge in this dynamic market.

Key Drivers, Barriers & Challenges in North America Automotive Interiors Industry

Key Drivers: Technological advancements, particularly in materials science and electronics, are driving innovation in automotive interiors. Growing consumer demand for comfort, luxury, and personalized features fuels market growth. Government regulations promoting safety and environmental sustainability are shaping product development. The increasing adoption of electric and autonomous vehicles presents significant growth opportunities.

Key Challenges: Supply chain disruptions, particularly concerning the availability of raw materials and electronic components, pose a significant challenge. Fluctuating commodity prices impact production costs, affecting profitability. Intense competition from established and emerging players creates pressure on pricing and margins. Meeting increasingly stringent safety and environmental standards requires significant investment in research and development.

Emerging Opportunities in North America Automotive Interiors Industry

Emerging opportunities include the growing demand for sustainable and eco-friendly interior materials, the integration of augmented reality (AR) and virtual reality (VR) technologies for enhanced user experiences, and the development of personalized and customizable interior designs to cater to individual preferences. Untapped markets lie in the growth of electric vehicles and autonomous driving technologies, creating opportunities for innovative interior layouts and functionalities. Evolving consumer preferences towards more sustainable options create opportunities for manufacturers to adopt eco-friendly materials and manufacturing processes.

Growth Accelerators in the North America Automotive Interiors Industry

Several factors will accelerate growth in the coming years. Technological breakthroughs in areas such as lightweighting, advanced materials, and AI-powered features will enhance the value proposition of automotive interiors. Strategic partnerships between automotive manufacturers and interior component suppliers will foster innovation and efficiency. Expanding into emerging markets within North America and integrating with smart city infrastructure will broaden market reach and stimulate demand.

Key Players Shaping the North America Automotive Interiors Industry Market

- Magna International Inc.

- Recaro Group

- Visteon Corporation

- Groclin S A

- Lear Corporation

- Faurecia

- Adient PLC

- Pioneer Corporation

- Grammer AG

- Panasonic Corporation

Notable Milestones in North America Automotive Interiors Industry Sector

- 2020, Q3: Lear Corporation launches a new line of sustainable interior components.

- 2021, Q1: Magna International Inc. announces a significant investment in autonomous driving technology integration.

- 2022, Q4: Adient PLC acquires a smaller competitor, expanding its market share.

- 2023, Q2: Faurecia introduces a new generation of lightweight and durable seating systems.

- 2024, Q1: Visteon Corporation partners with a technology company to develop advanced infotainment systems.

In-Depth North America Automotive Interiors Industry Market Outlook

The North American automotive interiors market is poised for continued growth, driven by technological innovation, evolving consumer preferences, and the expansion of the electric vehicle market. Strategic opportunities lie in developing sustainable, customizable, and technologically advanced interior solutions. Focus on lightweighting, enhancing safety features, and creating superior user experiences will be key to success in this competitive market. The market's future growth hinges on the successful integration of advanced technologies and the ability of manufacturers to meet the evolving demands of consumers for sustainable and personalized vehicle interiors.

North America Automotive Interiors Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Component Type

- 2.1. Infotainment System

- 2.2. Instrument Panels

- 2.3. Interior Lighting

- 2.4. Others

North America Automotive Interiors Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Automotive Interiors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Exponential Increase in Automotive Sector

- 3.3. Market Restrains

- 3.3.1. Digitization of R&D Operations in Automotive Sector

- 3.4. Market Trends

- 3.4.1. Electric Vehicles will Fuel the Growth of Market.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Automotive Interiors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Component Type

- 5.2.1. Infotainment System

- 5.2.2. Instrument Panels

- 5.2.3. Interior Lighting

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. United States North America Automotive Interiors Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Automotive Interiors Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Automotive Interiors Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Automotive Interiors Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Magna International Inc

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Recaro Group

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Visteon Corporatio

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Groclin S A

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Lear Corporation

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Faurecia

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Adient PLC

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Pioneer Corporation

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Grammer AG

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Panasonic Corporation

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Magna International Inc

List of Figures

- Figure 1: North America Automotive Interiors Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Automotive Interiors Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Automotive Interiors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Automotive Interiors Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 3: North America Automotive Interiors Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 4: North America Automotive Interiors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: North America Automotive Interiors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States North America Automotive Interiors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada North America Automotive Interiors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico North America Automotive Interiors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America North America Automotive Interiors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: North America Automotive Interiors Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 11: North America Automotive Interiors Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 12: North America Automotive Interiors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: United States North America Automotive Interiors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Automotive Interiors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Automotive Interiors Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Interiors Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the North America Automotive Interiors Industry?

Key companies in the market include Magna International Inc, Recaro Group, Visteon Corporatio, Groclin S A, Lear Corporation, Faurecia, Adient PLC, Pioneer Corporation, Grammer AG, Panasonic Corporation.

3. What are the main segments of the North America Automotive Interiors Industry?

The market segments include Vehicle Type, Component Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Exponential Increase in Automotive Sector.

6. What are the notable trends driving market growth?

Electric Vehicles will Fuel the Growth of Market..

7. Are there any restraints impacting market growth?

Digitization of R&D Operations in Automotive Sector.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Interiors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Interiors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Interiors Industry?

To stay informed about further developments, trends, and reports in the North America Automotive Interiors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence