Key Insights

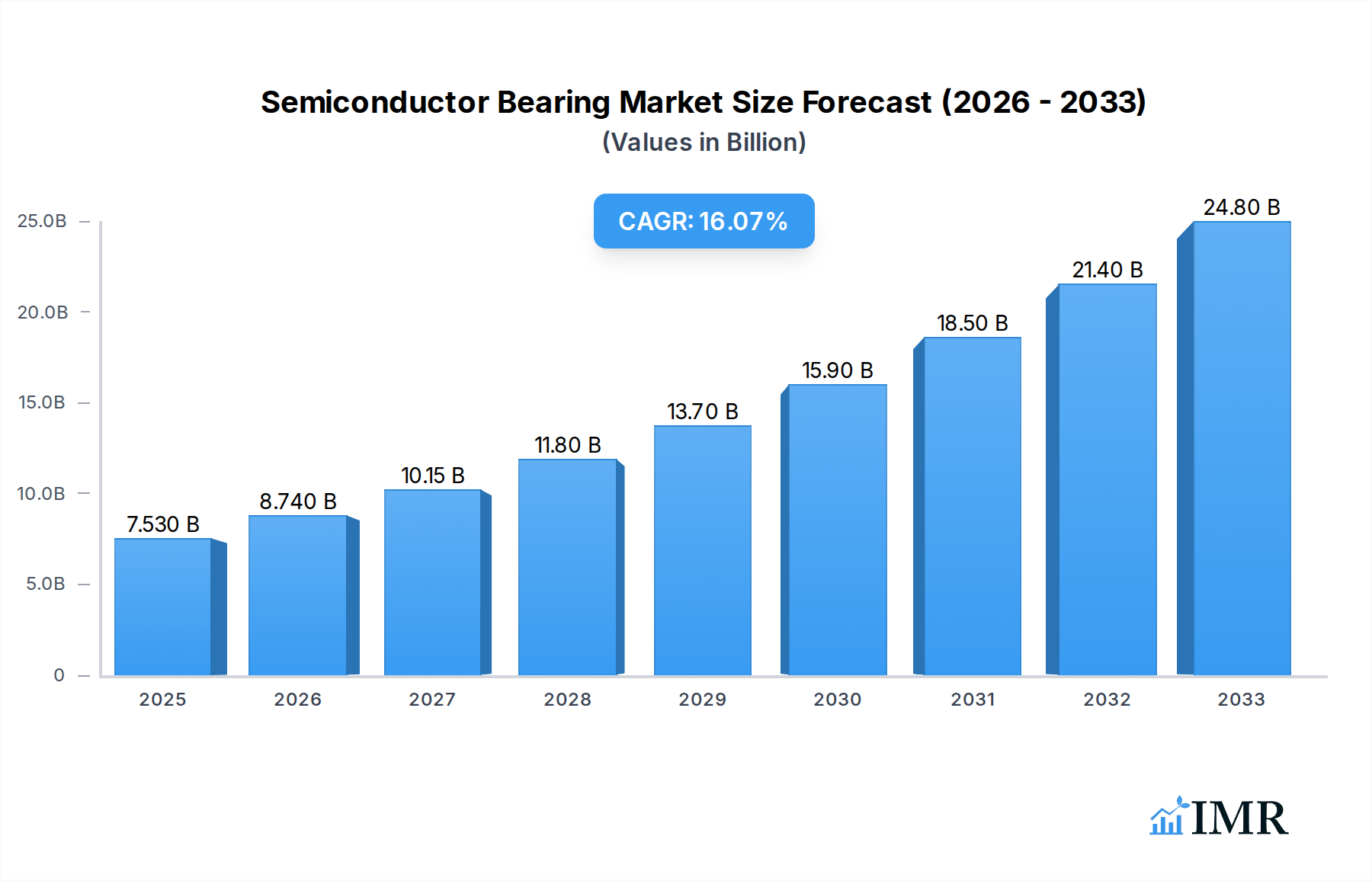

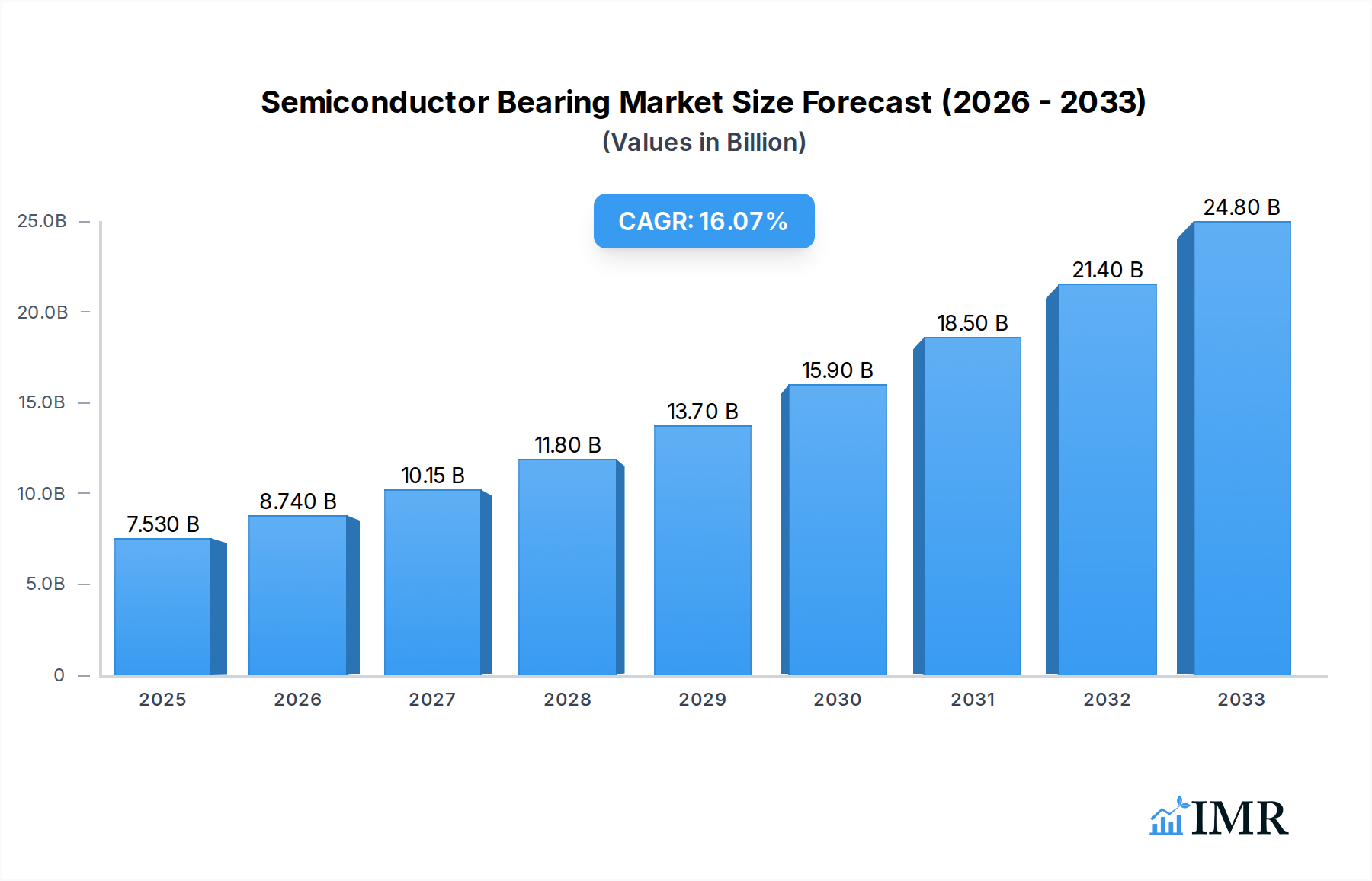

The global Semiconductor Bearing market is poised for substantial expansion, projected to reach an estimated USD 7.53 billion in 2025 with an impressive Compound Annual Growth Rate (CAGR) of 15.08%. This robust growth is primarily fueled by the escalating demand for advanced semiconductors across a multitude of industries, including automotive, consumer electronics, telecommunications, and industrial automation. The relentless pursuit of smaller, more powerful, and energy-efficient chips necessitates highly precise and reliable bearing solutions for the complex manufacturing processes involved. Furthermore, the burgeoning growth in the development and production of Flat Panel Displays (FPDs) and solar panels, both critical components in modern technology and renewable energy sectors, significantly contributes to the market's upward trajectory. The increasing sophistication of wafer handling, lithography, and assembly equipment within these sectors directly drives the demand for specialized bearings capable of withstanding extreme conditions, maintaining ultra-high purity environments, and offering exceptional rotational accuracy.

Semiconductor Bearing Market Size (In Billion)

The market is experiencing a transformative phase driven by technological advancements and evolving industry needs. Key applications like Semiconductor Chip manufacturing are at the forefront, followed closely by the FPD and Solar Panel segments. The shift towards miniaturization and increased processing power in semiconductors is a major catalyst, demanding bearings with superior material properties and design innovations. Within the types of bearings, SiN2 Ceramic Bearings are gaining prominence due to their inherent advantages in high-speed operation, corrosion resistance, and non-magnetic properties, making them ideal for cleanroom environments prevalent in semiconductor fabrication. Stainless Steel Bearings also hold a significant share, offering a balance of performance and cost-effectiveness. The market's growth is further supported by significant investments in semiconductor manufacturing facilities globally, especially in the Asia Pacific region, and a growing emphasis on renewable energy, which boosts solar panel production. The market is characterized by key players such as NSK, SKF, and NTN, who are continually innovating to meet the stringent requirements of these high-tech industries.

Semiconductor Bearing Company Market Share

Here is a compelling, SEO-optimized report description for the Semiconductor Bearing market, designed for industry professionals and maximizing search engine visibility.

Semiconductor Bearing Market Dynamics & Structure

The global semiconductor bearing market exhibits a moderately concentrated landscape, with key players like NSK, SKF, KMS Bearings, JTEKT, IKO, NTN, NHBB, Kaydon, and Schatz Bearing dominating significant market share. Technological innovation is the primary engine of growth, fueled by the relentless demand for miniaturization, increased precision, and enhanced performance in semiconductor manufacturing equipment, FPD manufacturing, and solar panel production. Stringent regulatory frameworks, particularly concerning environmental impact and material compliance, are also shaping product development and market entry. Competitive product substitutes, such as alternative bearing materials and advanced motion control systems, present a continuous challenge. End-user demographics are increasingly sophisticated, demanding higher reliability and longer operational lifespans. Mergers and acquisitions (M&A) activity, though currently moderate, is expected to increase as companies seek to consolidate expertise, expand product portfolios, and gain a competitive edge. For instance, recent M&A deals have focused on acquiring specialized bearing technologies for vacuum environments and extreme temperature applications, reflecting the evolving needs of the semiconductor industry. Innovation barriers include the high cost of R&D for advanced materials like SiN2 ceramic bearings and the complex qualification processes required for semiconductor applications. The market is projected to reach $10.2 billion by 2033.

- Market Concentration: Top 5 players hold approximately 60% market share.

- Technological Innovation Drivers: Miniaturization, precision, vacuum compatibility, high-speed operation.

- Regulatory Frameworks: RoHS, REACH compliance, cleanroom certifications.

- Competitive Product Substitutes: Magnetic bearings, air bearings, advanced lubrication systems.

- End-User Demographics: Semiconductor fabs, FPD manufacturers, solar panel producers, research institutions.

- M&A Trends: Focus on specialized technologies for vacuum and high-temperature applications.

- Innovation Barriers: High R&D costs, lengthy qualification cycles, material science challenges.

Semiconductor Bearing Growth Trends & Insights

The semiconductor bearing market has experienced robust growth from 2019–2024, a trend poised to accelerate significantly throughout the forecast period of 2025–2033. Driven by the insatiable global demand for advanced electronics, from cutting-edge semiconductor chips to high-definition flat-panel displays and expanding solar energy infrastructure, the market size has witnessed a steady upward trajectory. The base year of 2025 estimates the market at $7.5 billion, with projections indicating a Compound Annual Growth Rate (CAGR) of 7.8% from 2025 to 2033. This sustained expansion is attributed to several key factors. Firstly, the escalating complexity and miniaturization of semiconductor devices necessitate bearings with unparalleled precision, minimal friction, and exceptional durability, often in ultra-clean and vacuum environments. This drives the adoption of advanced materials like SiN2 ceramic bearings and specialized stainless steel variants. Secondly, the burgeoning FPD industry, driven by advancements in OLED and micro-LED technologies, requires highly precise motion components for intricate manufacturing processes. Thirdly, the global push towards renewable energy sources has significantly boosted the solar panel sector, creating a substantial demand for bearings in automated assembly and inspection equipment. Consumer behavior shifts are also indirectly influencing this market; the increasing adoption of smartphones, electric vehicles, and smart home devices all rely on semiconductor chips, thereby amplifying the need for efficient and reliable semiconductor manufacturing, which in turn drives demand for high-performance bearings. Technological disruptions, such as advancements in additive manufacturing for bespoke bearing components and the development of self-lubricating materials, are further optimizing performance and cost-effectiveness. Market penetration of advanced ceramic bearings is expected to grow from 15% in 2024 to 25% by 2033, reflecting their increasing importance in demanding applications. The historical period of 2019-2024 saw an average CAGR of 6.5%, laying a strong foundation for future expansion.

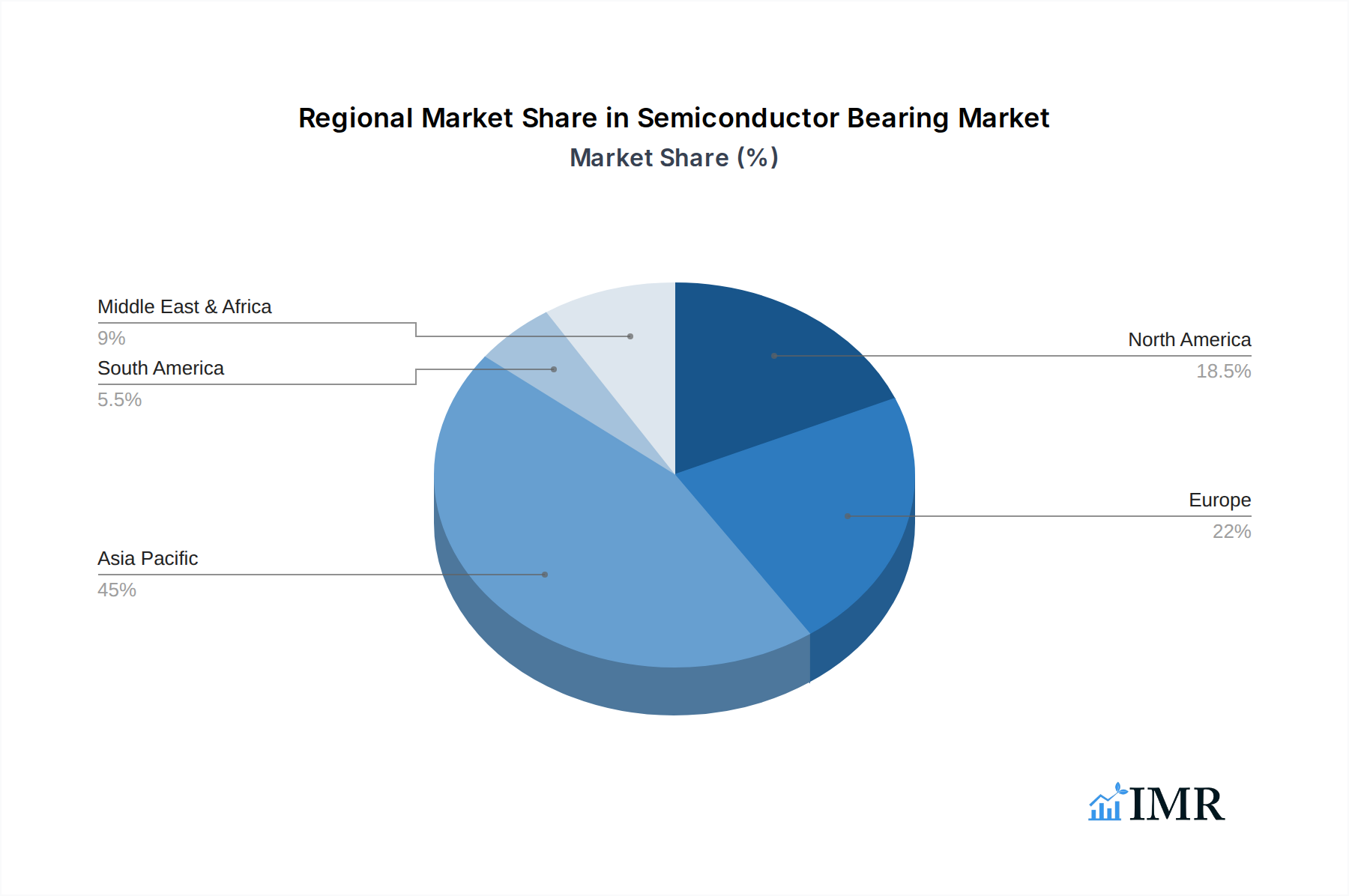

Dominant Regions, Countries, or Segments in Semiconductor Bearing

The Semiconductor Chip application segment is unequivocally the dominant force driving growth within the global semiconductor bearing market, projecting a substantial market share and exhibiting the highest growth potential. This dominance is intrinsically linked to the paramount importance of semiconductor manufacturing in the global economy. Countries like Taiwan, South Korea, the United States, and China are at the forefront of semiconductor fabrication, necessitating a massive influx of highly specialized bearings for their wafer fabrication plants (fabs) and assembly operations. Economic policies in these regions actively promote the growth of the semiconductor industry through substantial investments in research and development, tax incentives, and the establishment of advanced manufacturing infrastructure, creating a fertile ground for bearing manufacturers.

Within the application types, Stainless Steel Bearings currently hold the largest market share due to their cost-effectiveness, wide availability, and suitability for a broad range of applications. However, the growth trajectory of SiN2 Ceramic Bearings is exceptionally strong. Their superior properties, including non-magnetic behavior, electrical insulation, corrosion resistance, and the ability to operate in vacuum environments and at high temperatures without lubrication, make them indispensable for next-generation semiconductor manufacturing processes, particularly in advanced lithography and etching equipment. The market share of SiN2 Ceramic Bearings is expected to grow from 15% in 2025 to 28% by 2033.

The FPD (Flat Panel Display) segment is another significant contributor, driven by the continuous innovation in display technologies such as OLED and Micro-LED. Countries leading in FPD manufacturing, including South Korea and China, are major consumers of precision bearings. The Solar Panel segment, while smaller in comparison, is experiencing steady growth fueled by global sustainability initiatives and government policies promoting renewable energy adoption.

Key drivers for dominance in these regions and segments include:

- Concentration of Semiconductor Fabs: The clustering of major semiconductor manufacturers in specific geographical locations creates concentrated demand.

- Technological Advancement: The relentless pursuit of smaller, faster, and more powerful chips necessitates bearing technologies capable of meeting extreme precision and environmental requirements.

- Government Subsidies and Investment: Favorable economic policies and substantial government funding in key semiconductor nations directly stimulate market demand.

- Supply Chain Integration: The presence of a robust ecosystem of equipment manufacturers, material suppliers, and research institutions fosters innovation and adoption.

- Increasing Automation: Automation in FPD and solar panel manufacturing lines requires high-reliability, precision bearings for robotics and automated handling systems.

The market share of the Semiconductor Chip segment is estimated to be 55% in 2025, with a projected CAGR of 8.2% through 2033, underscoring its pivotal role in the overall market expansion.

Semiconductor Bearing Product Landscape

The semiconductor bearing product landscape is characterized by continuous innovation focused on enhancing performance under extreme operating conditions. Key product innovations include the development of hybrid ceramic bearings utilizing SiN2 balls and steel races for reduced friction and increased speed capabilities, and entirely full ceramic bearings for ultimate corrosion and contamination resistance. These bearings are engineered for ultra-high vacuum (UHV) environments, high-temperature applications (up to 400°C), and stringent cleanroom classifications (ISO Class 1). Unique selling propositions revolve around achieving nanometer-level precision, extended service life in harsh conditions, and minimized particle generation. Technological advancements are also seen in advanced lubrication techniques, such as solid lubricants and vacuum-compatible greases, and in the development of specialized coatings for enhanced wear resistance and reduced stiction. The application of these advanced bearings is critical in wafer handling robots, plasma etching chambers, deposition systems, and inspection equipment within the semiconductor industry, as well as in precision stages for FPD manufacturing.

Key Drivers, Barriers & Challenges in Semiconductor Bearing

Key Drivers:

- Exponential Growth of Semiconductor Demand: The insatiable global demand for semiconductors, driven by AI, IoT, 5G, and electric vehicles, directly fuels the need for advanced manufacturing equipment and thus, specialized bearings.

- Technological Advancements in Manufacturing: The drive towards smaller feature sizes, higher wafer throughput, and improved yields necessitates bearings with unprecedented precision, speed, and reliability.

- Expansion of the FPD and Solar Industries: The growing demand for high-resolution displays and renewable energy solutions contributes significantly to the market.

- Miniaturization and Performance Enhancement: End-users continually push for smaller, lighter, and more efficient electronic devices, requiring bearings that enable these advancements.

Barriers & Challenges:

- High Cost of R&D and Manufacturing: Developing and producing advanced materials like SiN2 ceramic bearings and ensuring ultra-high purity manufacturing processes are exceptionally costly.

- Stringent Quality Control and Qualification: The semiconductor industry has rigorous qualification processes for components, leading to long lead times and high development expenses for bearing manufacturers.

- Supply Chain Volatility: Geopolitical factors, raw material availability, and logistics challenges can disrupt the supply of critical materials and finished products.

- Intense Competition: While the market is moderately concentrated, competition from established players and emerging niche manufacturers drives down profit margins.

- Obsolescence Risk: Rapid technological advancements in end applications can lead to the obsolescence of existing bearing technologies, requiring continuous adaptation. The cost of a single advanced semiconductor bearing can range from $100 to over $1,000.

Emerging Opportunities in Semiconductor Bearing

Emerging opportunities in the semiconductor bearing sector lie in the development of self-lubricating and maintenance-free bearing solutions to reduce contamination and downtime in highly sensitive manufacturing environments. The increasing adoption of advanced robotics and automation in semiconductor, FPD, and solar panel production presents a significant opportunity for bearings designed for higher speeds and improved maneuverability. Furthermore, the burgeoning re-shoring of semiconductor manufacturing in various regions is expected to create new demand centers and necessitate localized supply chains for critical bearing components. The continuous evolution of advanced packaging technologies for semiconductors also requires innovative bearing solutions for specialized assembly equipment.

Growth Accelerators in the Semiconductor Bearing Industry

Growth accelerators in the semiconductor bearing industry are primarily driven by breakthroughs in material science, enabling the development of bearings with enhanced thermal stability, reduced friction, and superior wear resistance. Strategic partnerships between bearing manufacturers and semiconductor equipment OEMs are crucial for co-developing custom solutions that meet the evolving demands of next-generation manufacturing processes. Market expansion strategies, including the penetration of emerging geographic markets with growing semiconductor fabrication capabilities, and diversification into related high-precision industries, will further fuel long-term growth. The continuous investment in automation across all target segments also acts as a significant growth accelerator.

Key Players Shaping the Semiconductor Bearing Market

- NSK

- SKF

- KMS Bearings

- JTEKT

- IKO

- NTN

- NHBB

- Kaydon

- Schatz Bearing

Notable Milestones in Semiconductor Bearing Sector

- 2019: Launch of enhanced vacuum-compatible ceramic hybrid bearings by NSK, offering improved performance for wafer handling.

- 2020: SKF introduces new generation of sealed deep groove ball bearings with advanced lubricant for extended life in harsh environments.

- 2021: JTEKT develops high-precision angular contact ball bearings for advanced lithography equipment.

- 2022: IKO expands its range of thin-section bearings for compact semiconductor manufacturing machinery.

- 2023: NHBB announces significant capacity expansion for its high-performance ceramic bearing production to meet rising demand.

- 2024 (Early): Kaydon showcases new composite material bearings offering reduced weight and improved thermal management for robotic applications.

In-Depth Semiconductor Bearing Market Outlook

The semiconductor bearing market is poised for sustained and accelerated growth, driven by the indispensable role of semiconductors in modern technology and the relentless pursuit of manufacturing efficiency and precision. Strategic opportunities lie in catering to the increasingly specialized needs of advanced semiconductor nodes, the expansion of foldable and flexible display technologies, and the robust growth of solar energy infrastructure. The industry's future will be shaped by a commitment to cutting-edge material science, deeper collaboration with equipment manufacturers, and a keen eye on emerging geographic markets and application niches, ensuring a dynamic and expanding market for years to come, with the market expected to reach $10.2 billion by 2033.

Semiconductor Bearing Segmentation

-

1. Application

- 1.1. Semiconductor Chip

- 1.2. FPD (Flat Panel Display)

- 1.3. Solar Panel

- 1.4. Others

-

2. Types

- 2.1. Stainless Steel Bearing

- 2.2. Borosilicate Glass Bearing

- 2.3. SiN2 Ceramic Bearing

- 2.4. Others

Semiconductor Bearing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Semiconductor Bearing Regional Market Share

Geographic Coverage of Semiconductor Bearing

Semiconductor Bearing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.08% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Semiconductor Bearing Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Semiconductor Chip

- 5.1.2. FPD (Flat Panel Display)

- 5.1.3. Solar Panel

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Stainless Steel Bearing

- 5.2.2. Borosilicate Glass Bearing

- 5.2.3. SiN2 Ceramic Bearing

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Semiconductor Bearing Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Semiconductor Chip

- 6.1.2. FPD (Flat Panel Display)

- 6.1.3. Solar Panel

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Stainless Steel Bearing

- 6.2.2. Borosilicate Glass Bearing

- 6.2.3. SiN2 Ceramic Bearing

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Semiconductor Bearing Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Semiconductor Chip

- 7.1.2. FPD (Flat Panel Display)

- 7.1.3. Solar Panel

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Stainless Steel Bearing

- 7.2.2. Borosilicate Glass Bearing

- 7.2.3. SiN2 Ceramic Bearing

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Semiconductor Bearing Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Semiconductor Chip

- 8.1.2. FPD (Flat Panel Display)

- 8.1.3. Solar Panel

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Stainless Steel Bearing

- 8.2.2. Borosilicate Glass Bearing

- 8.2.3. SiN2 Ceramic Bearing

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Semiconductor Bearing Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Semiconductor Chip

- 9.1.2. FPD (Flat Panel Display)

- 9.1.3. Solar Panel

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Stainless Steel Bearing

- 9.2.2. Borosilicate Glass Bearing

- 9.2.3. SiN2 Ceramic Bearing

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Semiconductor Bearing Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Semiconductor Chip

- 10.1.2. FPD (Flat Panel Display)

- 10.1.3. Solar Panel

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Stainless Steel Bearing

- 10.2.2. Borosilicate Glass Bearing

- 10.2.3. SiN2 Ceramic Bearing

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 NSK

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 SKF

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 KMS Bearings

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 JTEKT

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 IKO

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 NTN

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 NHBB

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kaydon

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Schatz Bearing

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 NSK

List of Figures

- Figure 1: Global Semiconductor Bearing Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Semiconductor Bearing Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Semiconductor Bearing Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Semiconductor Bearing Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Semiconductor Bearing Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Semiconductor Bearing Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Semiconductor Bearing Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Semiconductor Bearing Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Semiconductor Bearing Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Semiconductor Bearing Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Semiconductor Bearing Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Semiconductor Bearing Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Semiconductor Bearing Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Semiconductor Bearing Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Semiconductor Bearing Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Semiconductor Bearing Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Semiconductor Bearing Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Semiconductor Bearing Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Semiconductor Bearing Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Semiconductor Bearing Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Semiconductor Bearing Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Semiconductor Bearing Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Semiconductor Bearing Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Semiconductor Bearing Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Semiconductor Bearing Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Semiconductor Bearing Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Semiconductor Bearing Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Semiconductor Bearing Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Semiconductor Bearing Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Semiconductor Bearing Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Semiconductor Bearing Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Bearing Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Semiconductor Bearing Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Semiconductor Bearing Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Semiconductor Bearing Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Semiconductor Bearing Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Semiconductor Bearing Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Semiconductor Bearing Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Semiconductor Bearing Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Semiconductor Bearing Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Semiconductor Bearing Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Semiconductor Bearing Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Semiconductor Bearing Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Semiconductor Bearing Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Semiconductor Bearing Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Semiconductor Bearing Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Semiconductor Bearing Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Semiconductor Bearing Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Semiconductor Bearing Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Semiconductor Bearing Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Bearing?

The projected CAGR is approximately 15.08%.

2. Which companies are prominent players in the Semiconductor Bearing?

Key companies in the market include NSK, SKF, KMS Bearings, JTEKT, IKO, NTN, NHBB, Kaydon, Schatz Bearing.

3. What are the main segments of the Semiconductor Bearing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Bearing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Bearing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Bearing?

To stay informed about further developments, trends, and reports in the Semiconductor Bearing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence