Key Insights

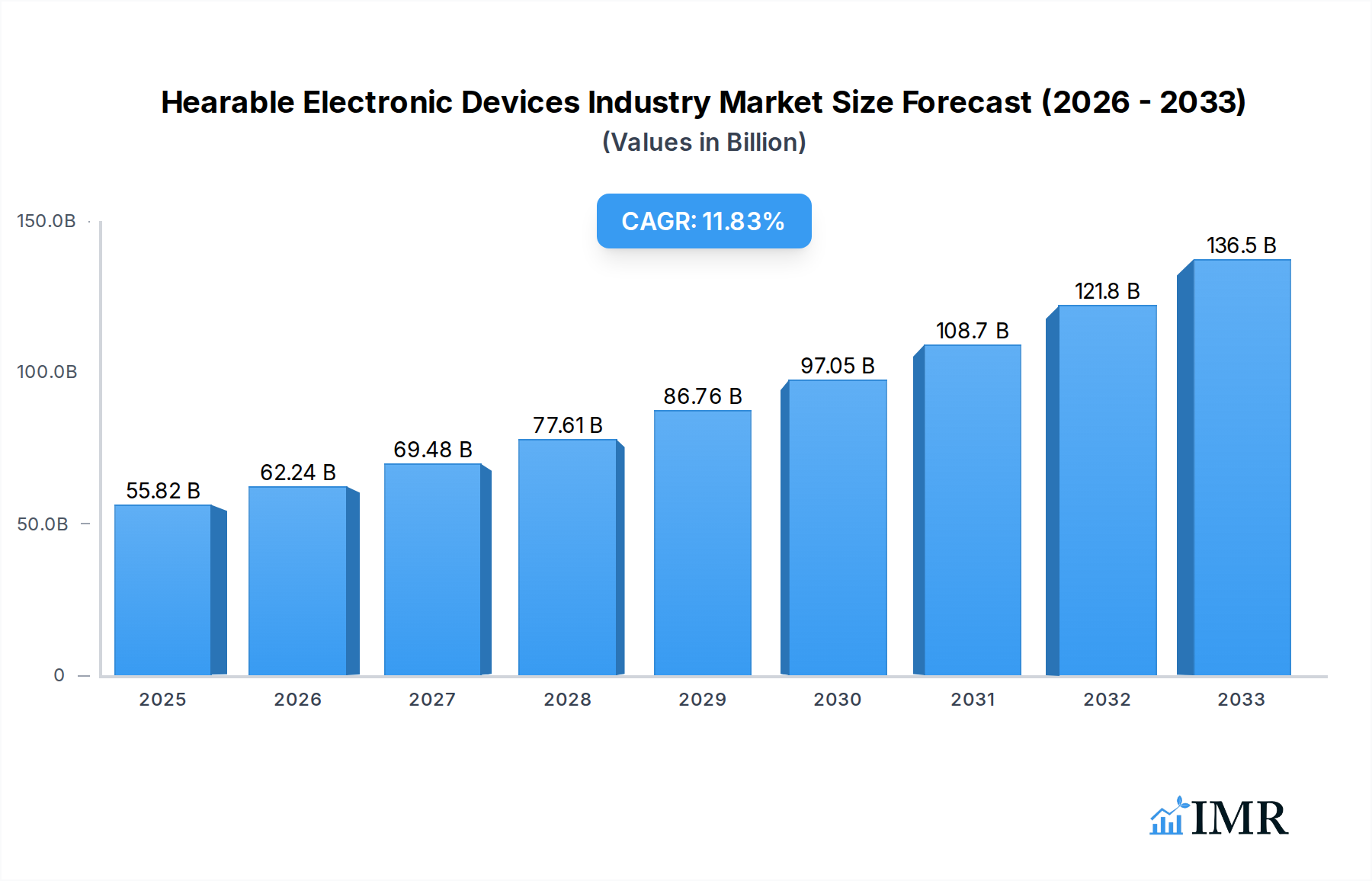

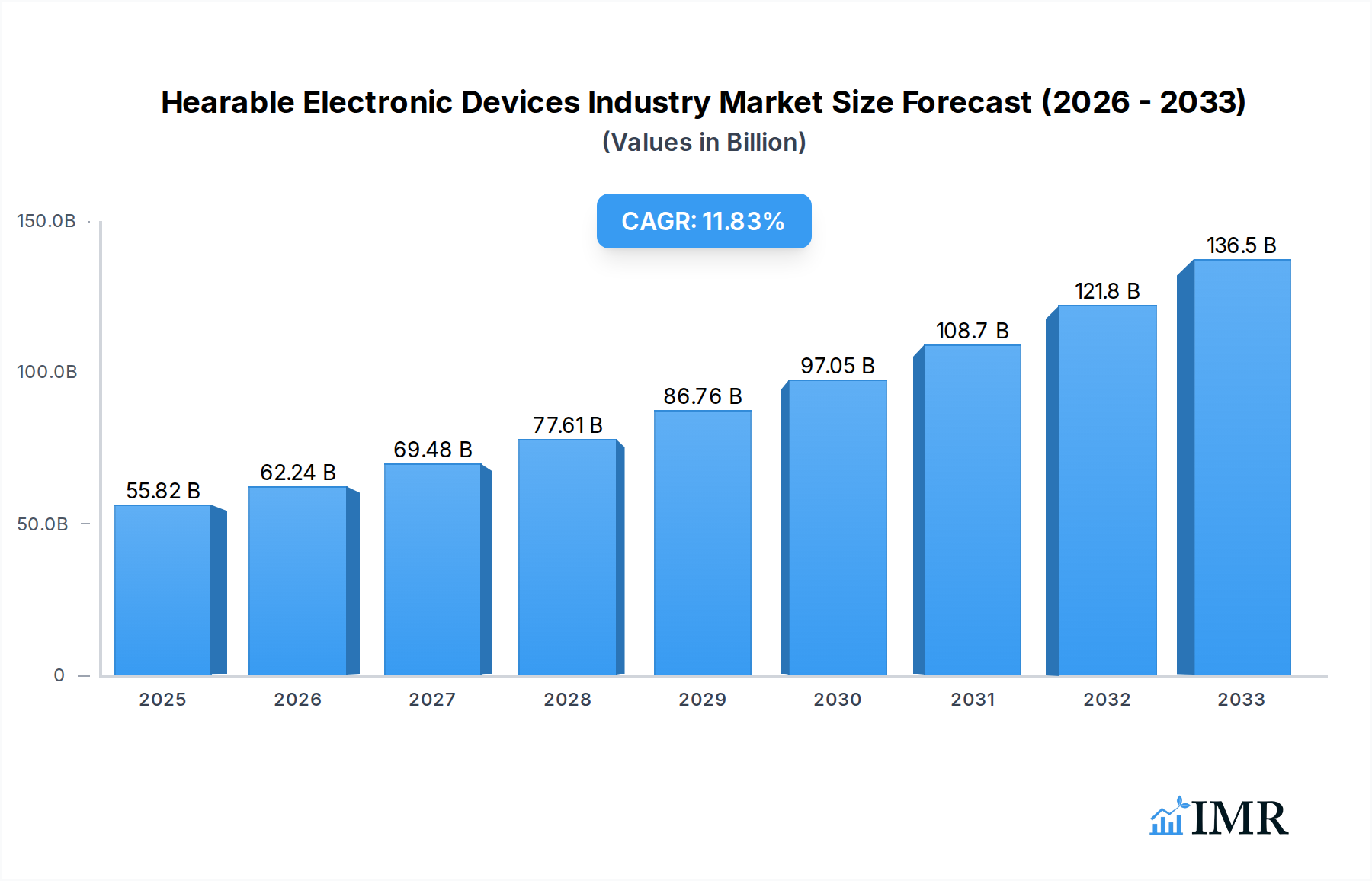

The global Hearable Electronic Devices Industry is poised for substantial growth, projected to reach a market size of $55.82 billion by 2025, driven by a remarkable CAGR of 11.62%. This robust expansion is fueled by a confluence of factors, including the increasing consumer demand for advanced audio solutions that blend entertainment, communication, and wellness. The evolving technological landscape, characterized by miniaturization, enhanced audio quality, and seamless connectivity, plays a pivotal role. Furthermore, the growing awareness and adoption of hearable devices for health monitoring, such as those with integrated hearing aid functionalities and personalized audio experiences, are significant growth catalysts. The market segmentation reveals a dynamic interplay between product types and categories, with earbuds and headsets dominating consumer preferences, while the integration of hearing aid capabilities signifies a burgeoning segment catering to an aging population and individuals with hearing impairments. The proliferation of smart devices and the growing reliance on voice-activated technology further amplify the demand for sophisticated hearable solutions.

Hearable Electronic Devices Industry Market Size (In Billion)

The competitive landscape is highly dynamic, featuring prominent players like Bose Corporation, Apple Inc. (including Beats Electronics), Samsung Electronics (Harman International), and Sony Corporation, alongside specialized hearing aid manufacturers such as ReSound (GN Group), Starkey Hearing Technologies, and Demant A/S. These companies are intensely focused on innovation, introducing products with advanced features like active noise cancellation, personalized soundscapes, real-time language translation, and integrated biometric sensors. Geographically, North America and Europe currently lead the market, owing to higher disposable incomes and early adoption rates of new technologies. However, the Asia Pacific region, particularly China and India, is expected to witness accelerated growth due to a rapidly expanding middle class, increasing urbanization, and a growing tech-savvy population. Emerging trends such as the integration of Artificial Intelligence for personalized audio experiences and the development of hearable devices as sophisticated personal assistants will continue to shape market trajectories, offering significant opportunities for sustained expansion and market leadership.

Hearable Electronic Devices Industry Company Market Share

This in-depth report delivers a strategic analysis of the global Hearable Electronic Devices industry, providing critical insights into market dynamics, growth trajectories, and competitive landscapes. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this comprehensive study is an indispensable resource for industry stakeholders, investors, and decision-makers seeking to navigate this rapidly evolving market. We analyze parent and child market segments to offer a holistic view of the hearable devices ecosystem, including premium audio solutions, true wireless earbuds, and advanced hearing aids.

Hearable Electronic Devices Industry Market Dynamics & Structure

The hearable electronic devices industry is characterized by a dynamic market structure influenced by rapid technological innovation and increasing consumer demand for connected audio and assistive listening solutions. Market concentration varies across segments, with high-end audio and premium hearables exhibiting more consolidated player bases. Key innovation drivers include advancements in miniaturization, battery efficiency, artificial intelligence for audio processing and personalization, and enhanced connectivity features like Bluetooth Low Energy and multi-point pairing. Regulatory frameworks, particularly concerning medical device classification for hearing aids and data privacy for connected hearables, play a crucial role in shaping market entry and product development. Competitive product substitutes are emerging, ranging from high-fidelity headphones to smart glasses with integrated audio. End-user demographics are expanding, encompassing younger consumers seeking lifestyle audio products and an aging population requiring advanced hearing solutions. Mergers and acquisitions (M&A) trends are active, driven by companies seeking to expand their product portfolios, gain technological expertise, and increase market share. For instance, the acquisition of Beats Electronics by Apple Inc. significantly reshaped the premium hearables market. Innovation barriers include high R&D costs, complex supply chains for specialized components, and the need for rigorous testing and certification, especially for hearing aid devices.

- Market Concentration: Moderate to high in premium audio and true wireless earbuds; fragmented in mid-range and budget segments.

- Technological Innovation Drivers: AI-powered audio enhancements, advanced noise cancellation, personalized sound profiles, seamless multi-device connectivity, extended battery life, and miniaturization.

- Regulatory Frameworks: CE marking, FDA approval for medical devices, FCC regulations for wireless communication, data privacy laws (e.g., GDPR, CCPA).

- Competitive Product Substitutes: Traditional headphones, smart speakers, specialized audio solutions for gamers and professionals.

- End-User Demographics: Millennials and Gen Z for lifestyle audio; older adults and individuals with hearing impairments for assistive devices; professionals for communication headsets.

- M&A Trends: Strategic acquisitions for technology integration, market expansion, and portfolio diversification.

Hearable Electronic Devices Industry Growth Trends & Insights

The global hearable electronic devices industry is poised for substantial growth, driven by a confluence of technological advancements, shifting consumer preferences, and increasing awareness of hearing health. The market size is projected to witness a compound annual growth rate (CAGR) of approximately 15-20% during the forecast period, reaching an estimated market value of over $150 billion by 2033. This expansion is fueled by the escalating adoption rates of true wireless stereo (TWS) earbuds, which have become mainstream due to their convenience and increasingly sophisticated features. Technological disruptions, such as the integration of advanced audio codecs, active noise cancellation (ANC) becoming a standard feature even in mid-range devices, and the emergence of hearables with health monitoring capabilities (e.g., posture tracking, heart rate monitoring), are redefining product categories. Consumer behavior shifts are profoundly impacting the market, with an increasing demand for personalized audio experiences, seamless integration with other smart devices, and a growing segment of consumers seeking hearables for both entertainment and functional purposes, including productivity and communication. The market penetration of hearables, particularly TWS earbuds, continues to rise globally, driven by decreasing price points and wider accessibility. Furthermore, the burgeoning market for advanced hearing aids, driven by an aging global population and greater acceptance of hearing assistive technologies, is a significant growth accelerator. The development of hearables that blend entertainment and health functions, such as personalized soundscapes for focus and relaxation, and advanced features for cognitive training, is creating new avenues for market expansion. The increasing integration of Artificial Intelligence (AI) and Machine Learning (ML) into hearables is enabling features like real-time language translation, intelligent noise filtering, and adaptive sound personalization, further enhancing user experience and driving demand. The "Sound of the New Age" movement, exemplified by initiatives like WS Audiology A/S's HearUSA brand, signifies a paradigm shift towards more user-centric and innovative approaches to hearing care, promising to reframe consumer perceptions and expand the market for advanced hearing solutions.

- Market Size Evolution: Projected to exceed $150 billion by 2033.

- Adoption Rates: High and accelerating for TWS earbuds, increasing for advanced hearing aids.

- Technological Disruptions: AI/ML integration, advanced ANC, health monitoring features, seamless multi-device connectivity, in-ear sensors.

- Consumer Behavior Shifts: Demand for personalization, integration with smart ecosystems, dual-purpose hearables (entertainment & health), increased health consciousness.

- Market Penetration: Rapidly growing across all major economies, especially for consumer hearables.

- CAGR: Estimated at 15-20% during the forecast period.

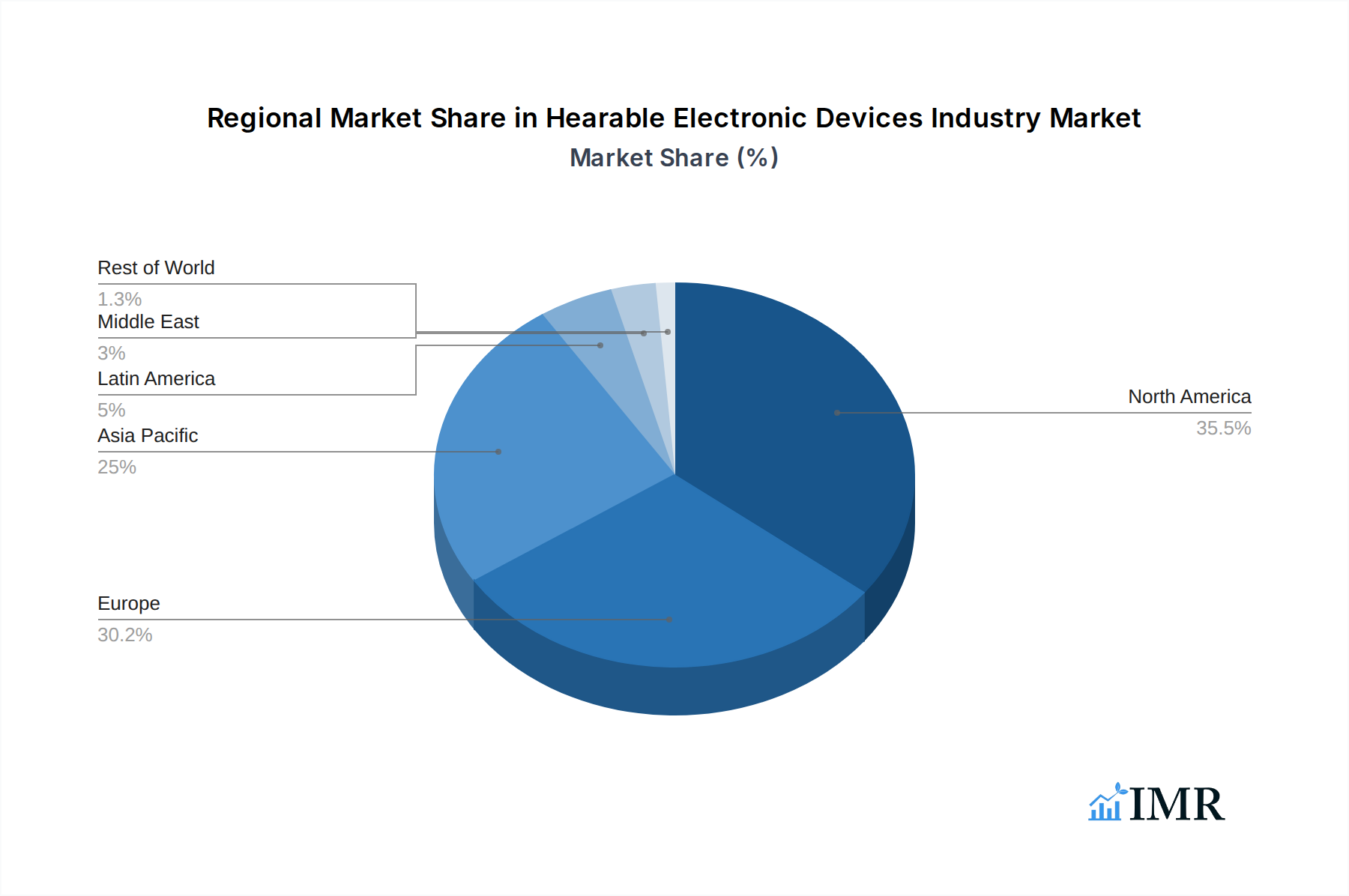

Dominant Regions, Countries, or Segments in Hearable Electronic Devices Industry

The Asia-Pacific region is emerging as a dominant force in the hearable electronic devices industry, propelled by a combination of robust economic growth, a burgeoning middle class with increasing disposable income, and a strong manufacturing base. Within this region, China stands out as a leading country, not only due to its massive consumer market but also its significant role in the production and innovation of hearable technologies. The In-Ear segment, particularly Earbuds and True Wireless Stereo (TWS) earbuds, is the primary driver of this dominance. These products have witnessed widespread adoption due to their convenience, portability, and increasingly sophisticated features at competitive price points. The high volume of TWS earbuds sold annually in Asia-Pacific, estimated to be over 150 million units in 2025, underscores its market leadership.

Key drivers contributing to Asia-Pacific's and China's dominance include:

- Economic Policies: Favorable government policies supporting the electronics manufacturing sector and R&D initiatives in advanced technologies.

- Infrastructure: Well-developed manufacturing infrastructure and efficient supply chains facilitate high-volume production and distribution.

- Consumer Demand: A large and young population with a high propensity to adopt new technologies and a growing demand for lifestyle audio devices.

- Technological Innovation Hubs: Presence of leading technology companies and research institutions driving innovation in hearable technology.

- Brand Proliferation: A diverse range of domestic and international brands catering to various price points and consumer preferences.

While the In-Ear segment, especially earbuds, leads in volume, the Hearing Aids segment, though smaller in unit volume, represents a significant growth opportunity driven by an aging population and increased awareness of hearing health. Countries like Japan and South Korea are showing strong growth in the hearing aids market due to their demographic profiles. North America and Europe remain significant markets, particularly for premium hearables and advanced hearing aid solutions, driven by higher per capita income and a mature consumer base that values quality and advanced features. However, the sheer volume and rapid growth of the consumer hearables segment in Asia-Pacific, particularly China, position it as the indisputable leader in overall market expansion and unit sales. The integration of advanced AI features and health monitoring into earbuds is further solidifying the dominance of the In-Ear segment.

- Dominant Region: Asia-Pacific.

- Leading Country: China.

- Dominant Segment (by volume): In-Ear (Earbuds and TWS).

- Key Drivers: Economic policies, manufacturing prowess, consumer demand, technological innovation.

- Market Share (In-Ear Segment in APAC): Estimated to be over 60% of global TWS earbud sales in 2025.

- Growth Potential: High for both consumer hearables and hearing aids across all major regions.

Hearable Electronic Devices Industry Product Landscape

The product landscape of hearable electronic devices is characterized by rapid innovation, offering a diverse range of functionalities beyond basic audio playback. True Wireless Stereo (TWS) earbuds dominate the consumer market, featuring advanced active noise cancellation (ANC), transparency modes, personalized sound profiles, and extended battery life. Headsets, particularly for professional and gaming use, are increasingly integrating AI-powered microphones for superior voice clarity and immersive audio experiences. In the medical technology sphere, hearing aids are witnessing significant advancements, incorporating AI for adaptive sound management, seamless Bluetooth connectivity for streaming, and discreet, personalized designs. Unique selling propositions include enhanced user experience through smart assistants, health and wellness monitoring features like posture correction and heart rate tracking, and robust water and sweat resistance for active lifestyles. Technological advancements are focusing on miniaturization, improved power efficiency, and sophisticated audio processing algorithms.

Key Drivers, Barriers & Challenges in Hearable Electronic Devices Industry

The hearable electronic devices industry is propelled by several key drivers, including the pervasive adoption of smartphones, which serve as the primary control interface for most hearables; the increasing demand for wireless audio solutions across all demographics; and advancements in battery technology enabling longer usage times. The integration of AI and machine learning for enhanced audio processing, personalization, and smart features is also a significant growth accelerator. Furthermore, the growing awareness of hearing health and the development of sophisticated, user-friendly hearing aids are expanding the market.

Conversely, the industry faces significant barriers and challenges. High research and development costs, particularly for miniaturized components and advanced AI algorithms, can be a hurdle. Supply chain disruptions for critical components, such as advanced chipsets and specialized acoustic drivers, can impact production volumes and lead times, with potential global supply chain issues impacting availability. Regulatory hurdles, especially for medical-grade hearing aids requiring stringent approvals, can slow down product launches. Intense competition among established brands and new entrants leads to price pressures, particularly in the crowded TWS earbud market. Ensuring user data privacy and security is also a growing concern, necessitating robust security measures.

Emerging Opportunities in Hearable Electronic Devices Industry

Emerging opportunities in the hearable electronic devices industry lie in the continued development of hearables with advanced health and wellness monitoring capabilities, extending beyond basic audio to include features like real-time health insights, cognitive training, and personalized well-being programs. The integration of hearables with augmented reality (AR) and virtual reality (VR) platforms presents a significant untapped market for immersive audio experiences. Furthermore, the growing demand for specialized hearables catering to specific professional needs, such as enhanced communication for remote workforces and immersive audio for content creators, offers substantial growth potential. The market for accessible and affordable hearing solutions, particularly in developing economies, remains an area ripe for innovation and market penetration.

Growth Accelerators in the Hearable Electronic Devices Industry Industry

Long-term growth in the hearable electronic devices industry is being significantly accelerated by continuous technological breakthroughs, such as advancements in ultra-low power Bluetooth connectivity, the development of more sophisticated AI chips for on-device processing, and improvements in acoustic engineering for superior sound quality and noise cancellation. Strategic partnerships between audio manufacturers, technology companies, and healthcare providers are creating new product categories and distribution channels. For example, collaborations focusing on integrating advanced hearing health features into consumer hearables are expanding the addressable market. Market expansion strategies targeting emerging economies and developing specialized product lines for niche applications are also contributing to sustained growth.

Key Players Shaping the Hearable Electronic Devices Industry Market

- Bose Corporation

- Apple Inc (Incl Beats Electronics)

- ReSound (GN Group)

- Xiaomi Corporation

- Skullcandy Inc

- Samsung Electronics Co Ltd (Harman International Industries Inc (Incl JBL)

- Sennheiser Electronic GMBH & Co

- Starkey Hearing Technologies

- Demant A/S

- WS Audiology A/S

- Sony Corporation

Notable Milestones in Hearable Electronic Devices Industry Sector

- November 2022: Starkey Partners with Special Olympics International to Bring Hearing Health Services to Athletes in Puerto Rico, providing life-changing health services and hearing instruments to Special Olympics athletes worldwide while helping make healthy hearing more inclusive of people with intellectual disabilities.

- October 2022: WS Audiology A/S announced a bold new HearUSA brand. The new brand unites 1,000 team members, 360 hearing centers, and 28 brands to introduce hearing care professionals (HCPs) and the 48 million people living with hearing loss to the 'Sound of the New Age' of hearing possibilities. HearUSA plans to open a series of reimagined hearing experience centers over the next several years that will reframe client assumptions about every aspect of hearing aids.

In-Depth Hearable Electronic Devices Industry Market Outlook

The future market outlook for hearable electronic devices is exceptionally robust, driven by a compelling blend of ongoing technological innovation and evolving consumer needs. The continued advancement of AI and sensor technology will unlock new functionalities, transforming hearables from mere audio accessories into indispensable personal health and communication hubs. Growth accelerators such as miniaturization, extended battery life, and seamless integration with the broader Internet of Things (IoT) ecosystem will further embed these devices into daily life. Strategic opportunities lie in expanding into emerging markets with tailored product offerings and in further blurring the lines between consumer audio and medical-grade hearing solutions, thereby creating entirely new market segments and increasing the overall addressable market size. The focus on personalized experiences, proactive health management, and enhanced communication will shape the next wave of innovation.

Hearable Electronic Devices Industry Segmentation

-

1. Type

- 1.1. In-Ear

- 1.2. On-Ear

- 1.3. Over-Ear

-

2. Product

- 2.1. Headsets

- 2.2. Earbuds

- 2.3. Hearing Aids

Hearable Electronic Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

- 4. Latin America

- 5. Middle East

Hearable Electronic Devices Industry Regional Market Share

Geographic Coverage of Hearable Electronic Devices Industry

Hearable Electronic Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. In-Ear

- 5.1.2. On-Ear

- 5.1.3. Over-Ear

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Headsets

- 5.2.2. Earbuds

- 5.2.3. Hearing Aids

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Hearable Electronic Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. In-Ear

- 6.1.2. On-Ear

- 6.1.3. Over-Ear

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Headsets

- 6.2.2. Earbuds

- 6.2.3. Hearing Aids

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Hearable Electronic Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. In-Ear

- 7.1.2. On-Ear

- 7.1.3. Over-Ear

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Headsets

- 7.2.2. Earbuds

- 7.2.3. Hearing Aids

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Hearable Electronic Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. In-Ear

- 8.1.2. On-Ear

- 8.1.3. Over-Ear

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Headsets

- 8.2.2. Earbuds

- 8.2.3. Hearing Aids

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Hearable Electronic Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. In-Ear

- 9.1.2. On-Ear

- 9.1.3. Over-Ear

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Headsets

- 9.2.2. Earbuds

- 9.2.3. Hearing Aids

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Hearable Electronic Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. In-Ear

- 10.1.2. On-Ear

- 10.1.3. Over-Ear

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Headsets

- 10.2.2. Earbuds

- 10.2.3. Hearing Aids

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East Hearable Electronic Devices Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. In-Ear

- 11.1.2. On-Ear

- 11.1.3. Over-Ear

- 11.2. Market Analysis, Insights and Forecast - by Product

- 11.2.1. Headsets

- 11.2.2. Earbuds

- 11.2.3. Hearing Aids

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bose Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Apple Inc (Incl Beats Electronics)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ReSound (GN Group)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Xiaomi Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Skullcandy Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Samsung Electronics Co Ltd (Harman International Industries Inc (Incl JBL)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sennheiser Electronic GMBH & Co

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Starkey Hearing Technologies

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Demant A/S

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 WS Audiology A/S

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sony Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Bose Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Hearable Electronic Devices Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Hearable Electronic Devices Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Hearable Electronic Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 4: North America Hearable Electronic Devices Industry Volume (K Unit), by Type 2025 & 2033

- Figure 5: North America Hearable Electronic Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Hearable Electronic Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Hearable Electronic Devices Industry Revenue (billion), by Product 2025 & 2033

- Figure 8: North America Hearable Electronic Devices Industry Volume (K Unit), by Product 2025 & 2033

- Figure 9: North America Hearable Electronic Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 10: North America Hearable Electronic Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 11: North America Hearable Electronic Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Hearable Electronic Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Hearable Electronic Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Hearable Electronic Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Hearable Electronic Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 16: Europe Hearable Electronic Devices Industry Volume (K Unit), by Type 2025 & 2033

- Figure 17: Europe Hearable Electronic Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Hearable Electronic Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 19: Europe Hearable Electronic Devices Industry Revenue (billion), by Product 2025 & 2033

- Figure 20: Europe Hearable Electronic Devices Industry Volume (K Unit), by Product 2025 & 2033

- Figure 21: Europe Hearable Electronic Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Europe Hearable Electronic Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 23: Europe Hearable Electronic Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Hearable Electronic Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Hearable Electronic Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Hearable Electronic Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Hearable Electronic Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 28: Asia Pacific Hearable Electronic Devices Industry Volume (K Unit), by Type 2025 & 2033

- Figure 29: Asia Pacific Hearable Electronic Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Hearable Electronic Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: Asia Pacific Hearable Electronic Devices Industry Revenue (billion), by Product 2025 & 2033

- Figure 32: Asia Pacific Hearable Electronic Devices Industry Volume (K Unit), by Product 2025 & 2033

- Figure 33: Asia Pacific Hearable Electronic Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 34: Asia Pacific Hearable Electronic Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 35: Asia Pacific Hearable Electronic Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Asia Pacific Hearable Electronic Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Hearable Electronic Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Hearable Electronic Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Latin America Hearable Electronic Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 40: Latin America Hearable Electronic Devices Industry Volume (K Unit), by Type 2025 & 2033

- Figure 41: Latin America Hearable Electronic Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 42: Latin America Hearable Electronic Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 43: Latin America Hearable Electronic Devices Industry Revenue (billion), by Product 2025 & 2033

- Figure 44: Latin America Hearable Electronic Devices Industry Volume (K Unit), by Product 2025 & 2033

- Figure 45: Latin America Hearable Electronic Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 46: Latin America Hearable Electronic Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 47: Latin America Hearable Electronic Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Latin America Hearable Electronic Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Latin America Hearable Electronic Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Latin America Hearable Electronic Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East Hearable Electronic Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 52: Middle East Hearable Electronic Devices Industry Volume (K Unit), by Type 2025 & 2033

- Figure 53: Middle East Hearable Electronic Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 54: Middle East Hearable Electronic Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 55: Middle East Hearable Electronic Devices Industry Revenue (billion), by Product 2025 & 2033

- Figure 56: Middle East Hearable Electronic Devices Industry Volume (K Unit), by Product 2025 & 2033

- Figure 57: Middle East Hearable Electronic Devices Industry Revenue Share (%), by Product 2025 & 2033

- Figure 58: Middle East Hearable Electronic Devices Industry Volume Share (%), by Product 2025 & 2033

- Figure 59: Middle East Hearable Electronic Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: Middle East Hearable Electronic Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Middle East Hearable Electronic Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East Hearable Electronic Devices Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 4: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 5: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 9: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 10: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 11: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 19: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 20: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 21: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 23: United Kingdom Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: United Kingdom Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Germany Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Germany Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: France Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: France Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 32: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 33: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 34: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 35: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: China Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: China Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Japan Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Japan Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: India Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: India Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: South Korea Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: South Korea Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Rest of Asia Pacific Hearable Electronic Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Hearable Electronic Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 48: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 49: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 50: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 51: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 52: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 53: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 54: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 55: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 56: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 57: Global Hearable Electronic Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 58: Global Hearable Electronic Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hearable Electronic Devices Industry?

The projected CAGR is approximately 11.62%.

2. Which companies are prominent players in the Hearable Electronic Devices Industry?

Key companies in the market include Bose Corporation, Apple Inc (Incl Beats Electronics), ReSound (GN Group), Xiaomi Corporation, Skullcandy Inc, Samsung Electronics Co Ltd (Harman International Industries Inc (Incl JBL), Sennheiser Electronic GMBH & Co, Starkey Hearing Technologies, Demant A/S, WS Audiology A/S, Sony Corporation.

3. What are the main segments of the Hearable Electronic Devices Industry?

The market segments include Type, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 55.82 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Affinity of the Millennial Population Towards Technologically Advanced Appliances and Rising Number of Smartphone Users; Rise in Demand for Wireless Headphones and Infotainment Devices.

6. What are the notable trends driving market growth?

Rise in Demand for Wireless Headphones and Infotainment Devices to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Optimizing Battery Life of Hearable Device.

8. Can you provide examples of recent developments in the market?

November 2022 - Starkey Partners with Special Olympics International to Bring Hearing Health Services to Athletes in Puerto Rico and provides life-changing health services and hearing instruments to Special Olympics athletes worldwide while helping make healthy hearing more inclusive of people with intellectual disabilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hearable Electronic Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hearable Electronic Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hearable Electronic Devices Industry?

To stay informed about further developments, trends, and reports in the Hearable Electronic Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence