Key Insights into the Ammunition Market

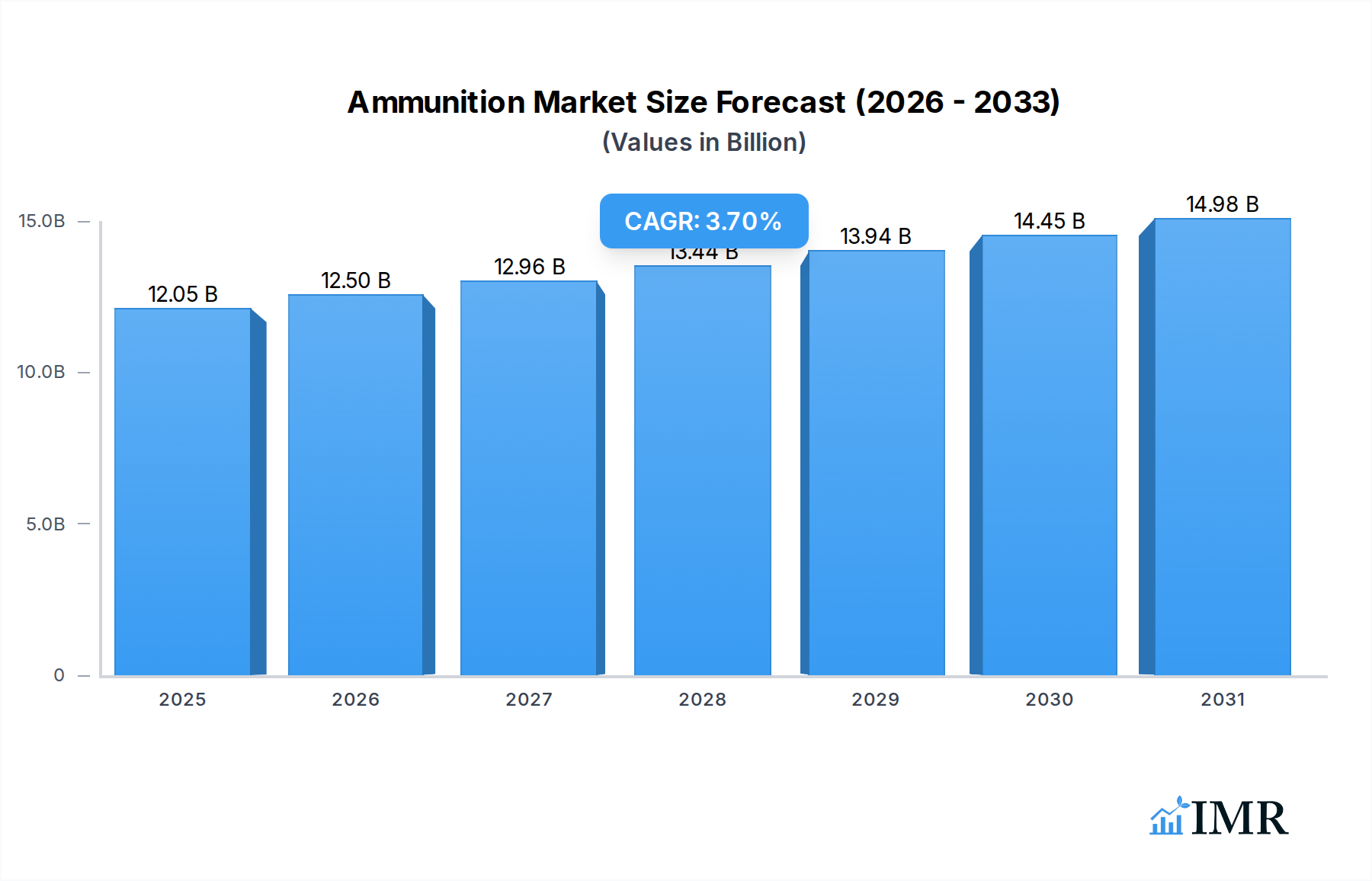

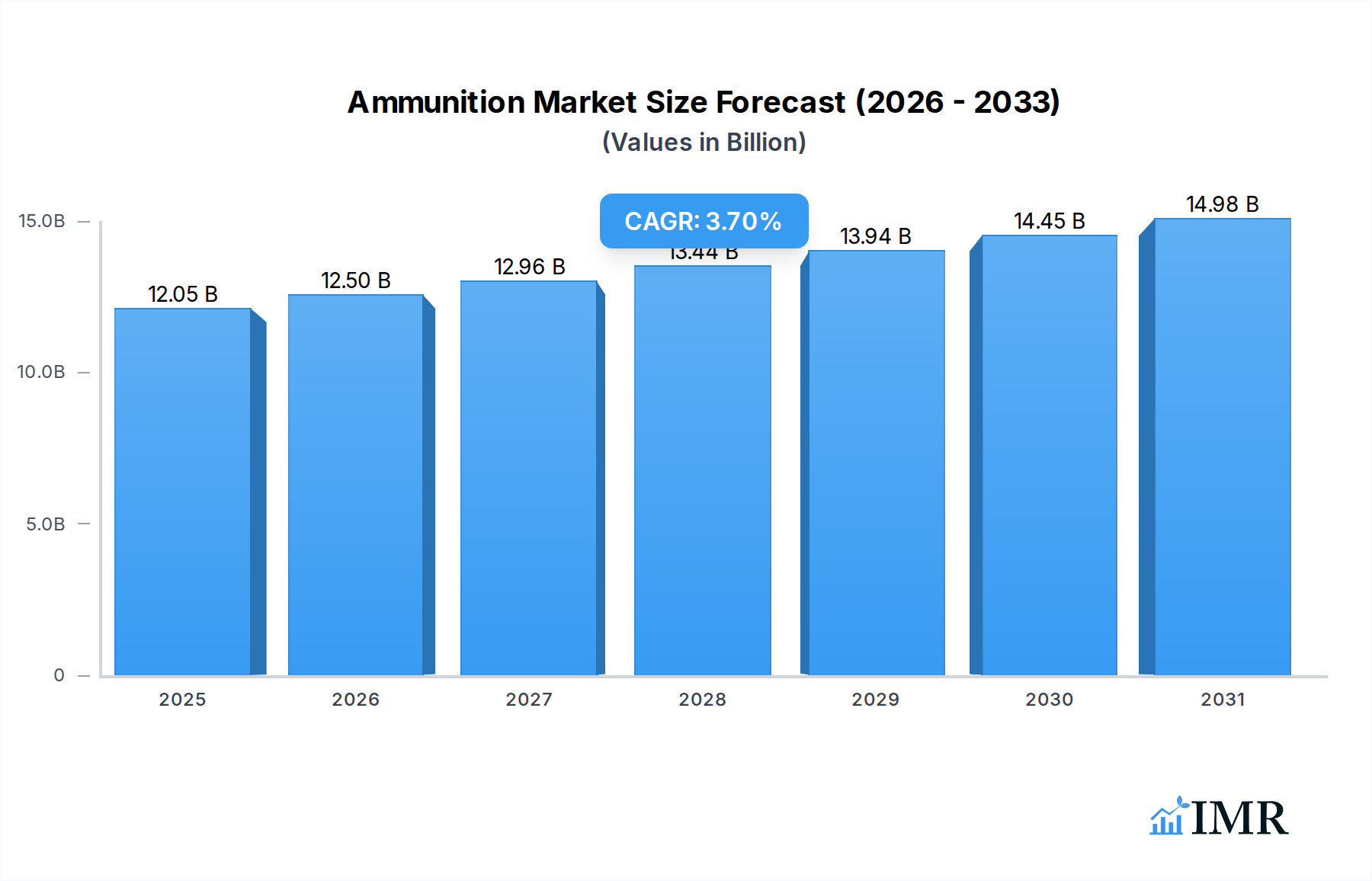

The Global Ammunition Market, valued at approximately $11620 million in the base year, is projected to reach an estimated $16,732.8 million by 2034, expanding at a robust Compound Annual Growth Rate (CAGR) of 3.7%. This significant growth trajectory is primarily driven by escalating geopolitical tensions and modernizing defense capabilities across nations. Increased defense spending globally fuels demand for advanced and specialized ammunition tailored for land, naval, and airborne platforms. The dynamism of the broader Defense Technology Market acts as a pivotal macro tailwind, spurring innovation in projectile design, guidance systems, and material science, all directly impacting ammunition efficacy and versatility. Governments are committing to substantial, long-term procurement programs, reinforcing market stability and ensuring strategic readiness.

Ammunition Market Size (In Billion)

Concurrently, the civilian sector presents a strong demand impetus, largely fueled by the burgeoning interest in hunting and shooting sports. This segment consistently drives demand for reliable, high-performance ammunition, encompassing a wide array of calibers and types, including specialized Shotgun Ammunition. Manufacturers are strategically responding to consumer preferences for enhanced precision, reliability, and, increasingly, environmentally conscious products. Innovations in propellant chemistry, highlighted by developments in the Propellants Market, and the integration of advanced materials, prominent within the Advanced Materials Market, are pivotal in meeting these evolving demands, leading to lighter, more accurate, and safer ammunition solutions. For instance, the shift towards lead-free projectiles is a testament to the industry's response to environmental concerns.

Ammunition Company Market Share

Furthermore, the persistent global threat of terrorism and evolving internal security challenges compel homeland security and law enforcement agencies to maintain high operational readiness. This translates into a consistent procurement cycle for tactical and training ammunition, forming a resilient demand base insulated from broader economic fluctuations. Supply chain resilience, following disruptions, and strategic investments in regional manufacturing are stabilizing production and improving market access. The consistent availability of critical raw materials, such as those within the Brass Market, is essential for sustaining production volumes. While the Ammunition Market navigates stringent regulatory frameworks and the inherent volatility of raw material prices, the fundamental drivers rooted in national security, along with the enduring popularity of recreational shooting, are expected to largely mitigate these challenges. This ensures the market’s continued expansion to 2034, with evolving global dynamics and consumer preferences shaping future innovation and competitive landscapes.

Small Caliber Dominance in Ammunition Market

The Small Caliber Ammunition Market segment stands as the undisputed leader within the broader Ammunition Market, commanding a substantial and consistently growing revenue share due to its unparalleled applicability across military, law enforcement, and civilian sectors globally. This dominance is not merely a reflection of sheer volume but also of its integral role in foundational defense doctrines, daily policing operations, and a vast array of recreational and competitive shooting activities. Small caliber rounds, typically encompassing a range from .17 HMR up to .50 BMG, represent the most frequently deployed and consumed ammunition type across all user groups. Their ubiquitous presence stems from critical factors including inherent compatibility with the immense installed base of existing Firearms Market products worldwide, significantly lower manufacturing costs per unit compared to medium or large caliber systems, and remarkable versatility across diverse operational environments.

In the military domain, small caliber ammunition forms the indispensable backbone of infantry operations and light vehicle armaments. Standardized cartridges like 5.56x45mm NATO and 7.62x51mm NATO are fundamental for rifles, carbines, and machine guns, making their procurement a continuous, high-volume, and mission-critical requirement for armed forces across the globe. Modernization efforts within military forces involve not just new weapons platforms but also the development and deployment of enhanced small caliber munitions, with a rigorous focus on improved accuracy, ballistic consistency, penetration capabilities against modern body armor, and reduced soldier load through weight reduction. These advancements contribute significantly to the overall effectiveness of the Defense Technology Market. Similarly, law enforcement agencies heavily rely on a core set of small caliber cartridges, primarily 9mm, .40 S&W, and .45 ACP, for their standard issue sidearms and patrol rifles. The consistent need for training, duty, and specialized tactical ammunition ensures a steady and predictable demand stream from this vital sector, driven by personnel turnover and ongoing training mandates.

The global proliferation of Firearms Market products in the civilian sector also significantly bolsters the Small Caliber Ammunition Market. Millions of enthusiasts participate actively in target shooting, competitive sports, and self-defense training, alongside a large demographic of hunters who utilize a specific range of small caliber rifle and handgun cartridges for various game, contributing to the vibrant Hunting and Shooting Sports Market. This exceptionally diverse civilian base demands a broad spectrum of small caliber offerings, ranging from inexpensive bulk rounds for recreational practice to highly specialized, precision-engineered cartridges designed for competitive shooting accuracy or specific hunting applications.

Key players in the broader Ammunition Market are, therefore, heavily invested in the small caliber segment. Companies like Northrop Grumman Corporation, General Dynamics Corporation, and Nammo AS frequently secure large, multi-year government contracts for military-grade small caliber ammunition, focusing intensively on performance, reliability, and strict compliance with national and international defense standards. On the civilian side, manufacturers such as Hornady Manufacturing, Inc., Ammo Inc., and CBC Global Ammunition diligently cater to this diverse consumer base, emphasizing innovation in bullet design, consistent manufacturing quality, and competitive pricing strategies. The segment's market share is not only growing in absolute terms but also exhibits robust consolidation, with larger manufacturers continually acquiring smaller, specialized producers to expand their product portfolios and enhance technological capabilities. Technological advancements, such as the development of lightweight polymer-cased ammunition to reduce weight burdens on soldiers, or enhanced armor-piercing capabilities for military applications, are primarily concentrated within the Small Caliber Ammunition Market, pushing the boundaries of material science, manufacturing precision, and safety standards. This high volume of demand, broad spectrum of application, and continuous innovation firmly cement the Small Caliber Ammunition Market's position as the dominant and most dynamically evolving segment within the overall Ammunition Market.

Strategic Drivers and Constraints in the Ammunition Market

The Ammunition Market’s trajectory is shaped by a confluence of potent drivers and notable constraints. A primary driver is the pervasive geopolitical instability globally, characterized by ongoing regional conflicts and heightened security concerns. This environment compels nations to increase defense budgets and modernize military inventories. For instance, global defense spending reportedly surpassed $2.2 trillion in 2022, with a significant portion allocated to procurement and sustainment of military ammunition, directly fueling demand for specialized cartridges, grenades, and artillery rounds. This robust governmental expenditure underscores the critical role of ammunition in national security strategies and its direct impact on the Defense Technology Market.

Another significant driver stems from the robust and growing Hunting and Shooting Sports Market. Civilian demand, driven by an expanding base of recreational shooters, competitive sportspersons, and hunters, contributes substantially to market revenue. Data indicates a consistent uptick in participation in shooting sports over the past decade, with millions of registered firearm owners engaging in activities that require a continuous supply of ammunition, including various types of Shotgun Ammunition. This segment is particularly sensitive to product innovation, with demand for specialized hunting loads and high-precision target ammunition fostering competition. Technological advancements, especially in the Propellants Market and through the integration of Advanced Materials Market solutions, are also critical drivers. Innovations leading to enhanced ballistic performance, reduced environmental impact (e.g., lead-free projectiles), and lighter-weight ammunition systems are increasingly valued by both military and civilian end-users. For example, advancements in Brass Market alloys contribute to more durable casing.

However, the market faces significant constraints. Stringent regulatory frameworks govern the manufacturing, sale, distribution, and ownership of ammunition across various jurisdictions. These regulations, often varying widely, create complex compliance challenges for manufacturers and distributors, potentially increasing operational costs and limiting market access. Environmental regulations, specifically concerning the use of heavy metals like lead in projectiles, are pushing manufacturers to invest heavily in R&D for sustainable alternatives, which can be costly and time-consuming. Furthermore, the volatility of raw material prices, particularly for metals like copper, zinc (for Brass Market), and lead, alongside specific chemical components for the Explosives Market, can significantly impact production costs and profit margins. Supply chain disruptions also pose a constraint, affecting the timely availability of critical components and thus impacting manufacturing schedules. Navigating these complex regulatory and supply chain environments remains a continuous challenge for participants in the Ammunition Market.

Competitive Ecosystem of Ammunition Market

The Ammunition Market is characterized by a mix of large defense contractors, specialized ammunition manufacturers, and diverse regional players, all vying for market share through innovation, strategic partnerships, and robust supply chain management. The competitive landscape is shaped by the stringent quality requirements of military contracts and the dynamic demands of the civilian market.

- Ammo Inc.: A rapidly growing entity known for innovative ammunition and components, focusing on military, law enforcement, and civilian markets through strategic acquisitions and product diversification.

- Arsenal JSCo.: A major Bulgarian producer of small arms and artillery systems, offering a broad range of ammunition for military and law enforcement customers globally.

- BAE Systems PLC: A multinational defense, security, and aerospace company with significant ammunition manufacturing capabilities, providing integrated solutions for land, naval, and air forces, emphasizing advanced precision munitions.

- CBC Global Ammunition: A leading global manufacturer with brands like Magtech and Sellier & Bellot, offering a comprehensive ammunition portfolio across military, law enforcement, and sporting sectors.

- Denel SOC Ltd.: A state-owned South African defense conglomerate involved in designing and manufacturing military products, including a range of ammunition systems for local and international markets.

- Northrop Grumman Corporation: A prominent American aerospace and defense technology company, contributing to the Ammunition Market through advanced ordnance, precision-guided munitions, and components for various weapon systems.

- General Dynamics Corporation: A global aerospace and defense company with a significant footprint in combat vehicles and armaments, supplying a wide array of ammunition, including tank rounds and small arms cartridges, to defense forces.

- Hanwha Corporation: A major South Korean conglomerate with substantial defense operations, producing a broad spectrum of conventional and advanced ammunition, including artillery shells and smart munitions.

- Hornady Manufacturing, Inc.: An American company renowned for producing high-quality bullets, ammunition, and reloading components primarily for civilian hunting, shooting sports, and law enforcement markets.

- Leonardo S.p.A.: An Italian multinational specializing in aerospace, defense, and security, contributing to the Ammunition Market through its land and naval defense systems, offering advanced artillery and naval munitions.

- Nammo AS: A leading Nordic defense company specializing in ammunition, rocket motors, and energetic materials, providing high-performance solutions for military and civilian applications globally.

- Poongsan Corporation: A South Korean manufacturing company with a significant defense division producing a comprehensive range of small, medium, and large caliber ammunition for military use.

- MESKO S.A.: A Polish defense company specializing in the production of ammunition and missiles for the Polish Armed Forces and international clients, covering various calibers and applications.

Recent Developments & Milestones in Ammunition Market

The Ammunition Market is continually evolving, driven by technological advancements, strategic partnerships, and a focus on enhanced performance and environmental compliance. Recent milestones reflect a concerted effort by key players to innovate across product lines and operational efficiencies.

- April 2024: Major defense contractors unveiled new generations of lightweight, polymer-cased Small Caliber Ammunition, promising significant weight reduction for infantry units and improved logistical efficiency across military supply chains. These advancements are leveraging insights from the Advanced Materials Market.

- February 2024: Several European ammunition manufacturers announced a joint venture to enhance the production capacity of standard NATO-compliant ammunition, aiming to bolster strategic reserves and reduce reliance on non-European suppliers amidst increasing geopolitical tensions.

- December 2023: A leading manufacturer launched a new line of lead-free hunting ammunition, specifically designed for the Hunting and Shooting Sports Market, responding to growing environmental regulations and consumer demand for eco-friendlier alternatives. This development also highlights trends within the Propellants Market for more sustainable formulations.

- September 2023: Key players in the Brass Market for ammunition components reported significant investments in recycling technologies, aiming to create a more circular economy for spent casings and reduce reliance on virgin raw materials.

- July 2023: Advancements in smart ammunition technologies, including guided projectiles for large caliber systems, were showcased at a major defense expo, indicating a future trend towards increased precision and reduced collateral damage, impacting the broader Defense Technology Market.

- May 2023: Regulatory bodies in North America introduced new standards for the safe storage and transportation of ammunition components, particularly for Explosives Market materials, leading to updated compliance requirements for manufacturers and distributors.

- March 2023: A collaborative R&D initiative between academic institutions and industry leaders was announced, focusing on developing biodegradable shotgun wads and casings for Shotgun Ammunition, aiming to minimize environmental impact in shooting ranges and hunting grounds.

- January 2023: Investments were made by a prominent ammunition producer in automated quality control systems, enhancing the consistency and reliability of their manufacturing processes, crucial for both military specifications and civilian market trust.

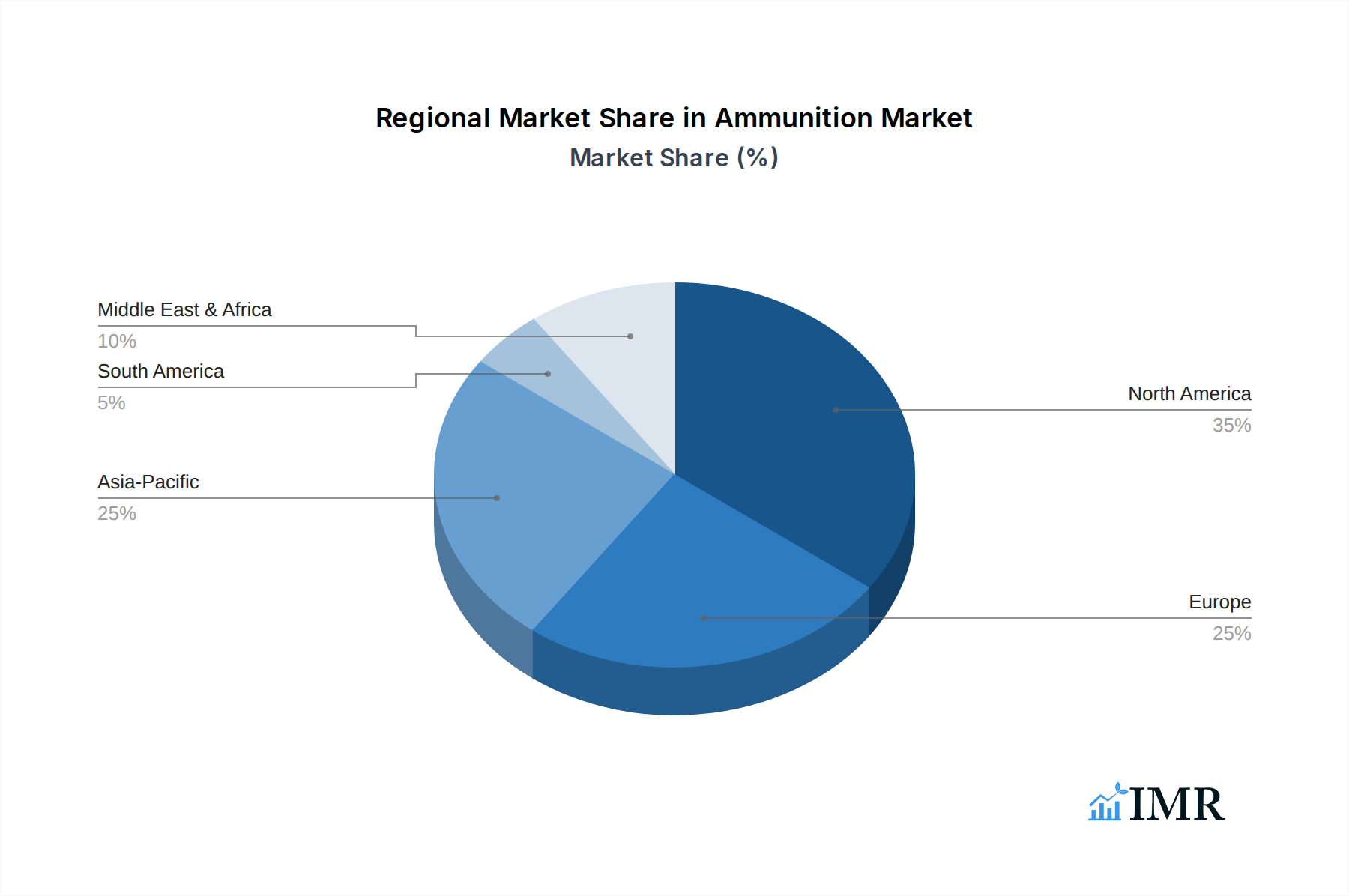

Regional Market Breakdown for Ammunition Market

The Ammunition Market exhibits significant regional variations in demand, growth drivers, and competitive dynamics. Each major region contributes uniquely to the global landscape, shaped by geopolitical factors, economic conditions, and cultural preferences.

North America holds a substantial revenue share in the global Ammunition Market, primarily driven by robust civilian demand. The United States, in particular, boasts a large population of firearm owners, active participation in the Hunting and Shooting Sports Market, and a strong self-defense culture. Defense spending by the US and Canada also contributes significantly. While mature, this market continues to grow steadily due to consistent recreational shooting and law enforcement procurement. The region is a key innovator in Small Caliber Ammunition Market development.

The Asia Pacific region is projected to be the fastest-growing market for ammunition. This rapid expansion is fueled by escalating geopolitical tensions, border disputes, and extensive military modernization programs in countries like China, India, and South Korea. These nations are heavily investing in indigenous production capabilities and advanced weapon systems, leading to a surge in demand for all caliber types, including specialized Shotgun Ammunition for security forces. Economic growth in the region also contributes to a growing civilian market, albeit under stricter regulations compared to North America. The increasing focus on internal security further augments demand from homeland security agencies.

Europe represents a mature yet strategically important market. Demand is characterized by ongoing defense modernization efforts among NATO members, replenishing stockpiles, and enhancing interoperability. While civilian ownership is generally lower and more regulated than in North America, there is a consistent market for sport shooting and hunting. The region also faces pressures to adopt more environmentally friendly ammunition, influencing R&D towards lead-free options and developments in the Propellants Market. Countries like Germany, France, and the UK are significant consumers and producers.

The Middle East & Africa region demonstrates strong demand for ammunition, primarily driven by persistent regional conflicts, internal security challenges, and counter-terrorism operations. Countries in the GCC and North Africa are making substantial investments in defense capabilities, leading to high-volume procurement of military-grade ammunition. This market is highly influenced by geopolitical dynamics and external military aid, making it a critical, albeit volatile, demand center within the global Ammunition Market. The focus is heavily on military and security agency procurement.

Finally, South America presents a developing market with growth primarily linked to national defense upgrades and efforts to combat organized crime. Brazil and Argentina are key players in terms of defense expenditure and local manufacturing capabilities. Civilian market growth is modest and highly sensitive to economic stability and evolving firearms legislation. The region shows potential for future expansion as defense budgets continue to adjust to regional security needs.

Ammunition Regional Market Share

Sustainability & ESG Pressures on Ammunition Market

The Ammunition Market is facing increasing scrutiny and pressure from sustainability mandates and Environmental, Social, and Governance (ESG) criteria. Environmental regulations, particularly concerning lead contamination, are a primary driver for change. Lead, a traditional component in bullets and primers, poses significant ecological risks in shooting ranges and hunting grounds. Consequently, there is a strong push towards lead-free ammunition alternatives, utilizing materials like copper, tungsten, and bismuth. This shift necessitates substantial R&D investment by manufacturers, impacting product development within the Small Caliber Ammunition Market and other segments. Compliance with strict hazardous waste disposal guidelines for manufacturing byproducts and spent materials, including those from the Brass Market and Explosives Market, is also becoming more rigorous, increasing operational costs.

Carbon footprint reduction and circular economy principles are also gaining traction. Ammunition producers are exploring ways to minimize energy consumption in manufacturing, optimize logistics, and develop recycling programs for spent casings. The development of biodegradable components, such as shotgun wads and casings for Shotgun Ammunition, represents a move towards reducing non-biodegradable waste. ESG investors are increasingly evaluating companies based on their environmental stewardship, ethical sourcing of raw materials, and responsible manufacturing practices. This pressure influences corporate strategies, encouraging transparency and the adoption of higher sustainability standards throughout the supply chain. Companies that proactively address these concerns are better positioned to secure long-term contracts, attract ethical investment, and maintain a positive public image in the evolving Ammunition Market. The integration of advanced materials, often from the Advanced Materials Market, is key to these sustainable transitions.

Customer Segmentation & Buying Behavior in Ammunition Market

Customer segmentation within the Ammunition Market is diverse, encompassing distinct end-user groups with unique purchasing criteria, price sensitivities, and procurement channels. Understanding these segments is crucial for manufacturers to tailor product offerings and market strategies effectively.

The Armed Forces segment represents the largest and most strategic customer base. Their purchasing criteria are dominated by performance, reliability, interoperability with existing weapon systems (especially for Firearms Market products), and adherence to strict military specifications. Price sensitivity is lower than in civilian markets, but long-term cost-effectiveness and proven combat efficacy are paramount. Procurement occurs through large-scale government contracts, often involving multi-year agreements and direct negotiations with major defense contractors. Demand is driven by defense budgets, modernization programs, and geopolitical requirements, directly impacting the Defense Technology Market.

Homeland Security Agencies & Police & Law Enforcement Agencies form another critical segment. Their purchasing decisions prioritize reliability, specific ballistic performance for duty use, and consistent training rounds. Safety features and compliance with national law enforcement standards are vital. While somewhat price-sensitive, quality and dependability outweigh minimal cost savings. Procurement typically involves approved vendor lists, tenders, and framework agreements, with specialized distributors often facilitating sales.

The Civilian Users segment is highly fragmented and diverse, comprising hunters, sport shooters, and individuals seeking ammunition for self-defense. This segment is characterized by a wide range of purchasing criteria: hunters prioritize accuracy, terminal performance, and ethical harvesting; sport shooters demand consistency, precision, and competitive pricing for bulk practice rounds; and self-defense users seek reliability and effectiveness. Price sensitivity is generally higher, especially for recreational use, yet quality and brand reputation play a significant role. Procurement channels include specialized firearms dealers, sporting goods stores, big-box retailers, and online platforms, reflecting the varied nature of the Hunting and Shooting Sports Market. Notable shifts include an increased preference for lead-free alternatives and high-performance tactical rounds for personal protection.

Ammunition Segmentation

-

1. Product Type

- 1.1. Centerfire Ammunition

- 1.2. Rimfire Ammunition

- 1.3. Shotgun Ammunition

-

2. Caliber

- 2.1. Small Caliber

- 2.2. Medium Caliber

- 2.3. Large Caliber

-

3. Material

- 3.1. Brass

- 3.2. Steel

- 3.3. Lead

- 3.4. Aluminum

- 3.5. Composites

-

4. Platform

- 4.1. Land

- 4.2. Naval

- 4.3. Airborne

-

5. End User

- 5.1. Armed Forces

- 5.2. Homeland Security Agencies

- 5.3. Police & Law Enforcement Agencies

- 5.4. Civilian Users

Ammunition Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ammunition Regional Market Share

Geographic Coverage of Ammunition

Ammunition REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Centerfire Ammunition

- 5.1.2. Rimfire Ammunition

- 5.1.3. Shotgun Ammunition

- 5.2. Market Analysis, Insights and Forecast - by Caliber

- 5.2.1. Small Caliber

- 5.2.2. Medium Caliber

- 5.2.3. Large Caliber

- 5.3. Market Analysis, Insights and Forecast - by Material

- 5.3.1. Brass

- 5.3.2. Steel

- 5.3.3. Lead

- 5.3.4. Aluminum

- 5.3.5. Composites

- 5.4. Market Analysis, Insights and Forecast - by Platform

- 5.4.1. Land

- 5.4.2. Naval

- 5.4.3. Airborne

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Armed Forces

- 5.5.2. Homeland Security Agencies

- 5.5.3. Police & Law Enforcement Agencies

- 5.5.4. Civilian Users

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Ammunition Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Centerfire Ammunition

- 6.1.2. Rimfire Ammunition

- 6.1.3. Shotgun Ammunition

- 6.2. Market Analysis, Insights and Forecast - by Caliber

- 6.2.1. Small Caliber

- 6.2.2. Medium Caliber

- 6.2.3. Large Caliber

- 6.3. Market Analysis, Insights and Forecast - by Material

- 6.3.1. Brass

- 6.3.2. Steel

- 6.3.3. Lead

- 6.3.4. Aluminum

- 6.3.5. Composites

- 6.4. Market Analysis, Insights and Forecast - by Platform

- 6.4.1. Land

- 6.4.2. Naval

- 6.4.3. Airborne

- 6.5. Market Analysis, Insights and Forecast - by End User

- 6.5.1. Armed Forces

- 6.5.2. Homeland Security Agencies

- 6.5.3. Police & Law Enforcement Agencies

- 6.5.4. Civilian Users

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Ammunition Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Centerfire Ammunition

- 7.1.2. Rimfire Ammunition

- 7.1.3. Shotgun Ammunition

- 7.2. Market Analysis, Insights and Forecast - by Caliber

- 7.2.1. Small Caliber

- 7.2.2. Medium Caliber

- 7.2.3. Large Caliber

- 7.3. Market Analysis, Insights and Forecast - by Material

- 7.3.1. Brass

- 7.3.2. Steel

- 7.3.3. Lead

- 7.3.4. Aluminum

- 7.3.5. Composites

- 7.4. Market Analysis, Insights and Forecast - by Platform

- 7.4.1. Land

- 7.4.2. Naval

- 7.4.3. Airborne

- 7.5. Market Analysis, Insights and Forecast - by End User

- 7.5.1. Armed Forces

- 7.5.2. Homeland Security Agencies

- 7.5.3. Police & Law Enforcement Agencies

- 7.5.4. Civilian Users

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. South America Ammunition Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Centerfire Ammunition

- 8.1.2. Rimfire Ammunition

- 8.1.3. Shotgun Ammunition

- 8.2. Market Analysis, Insights and Forecast - by Caliber

- 8.2.1. Small Caliber

- 8.2.2. Medium Caliber

- 8.2.3. Large Caliber

- 8.3. Market Analysis, Insights and Forecast - by Material

- 8.3.1. Brass

- 8.3.2. Steel

- 8.3.3. Lead

- 8.3.4. Aluminum

- 8.3.5. Composites

- 8.4. Market Analysis, Insights and Forecast - by Platform

- 8.4.1. Land

- 8.4.2. Naval

- 8.4.3. Airborne

- 8.5. Market Analysis, Insights and Forecast - by End User

- 8.5.1. Armed Forces

- 8.5.2. Homeland Security Agencies

- 8.5.3. Police & Law Enforcement Agencies

- 8.5.4. Civilian Users

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Ammunition Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Centerfire Ammunition

- 9.1.2. Rimfire Ammunition

- 9.1.3. Shotgun Ammunition

- 9.2. Market Analysis, Insights and Forecast - by Caliber

- 9.2.1. Small Caliber

- 9.2.2. Medium Caliber

- 9.2.3. Large Caliber

- 9.3. Market Analysis, Insights and Forecast - by Material

- 9.3.1. Brass

- 9.3.2. Steel

- 9.3.3. Lead

- 9.3.4. Aluminum

- 9.3.5. Composites

- 9.4. Market Analysis, Insights and Forecast - by Platform

- 9.4.1. Land

- 9.4.2. Naval

- 9.4.3. Airborne

- 9.5. Market Analysis, Insights and Forecast - by End User

- 9.5.1. Armed Forces

- 9.5.2. Homeland Security Agencies

- 9.5.3. Police & Law Enforcement Agencies

- 9.5.4. Civilian Users

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East & Africa Ammunition Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Centerfire Ammunition

- 10.1.2. Rimfire Ammunition

- 10.1.3. Shotgun Ammunition

- 10.2. Market Analysis, Insights and Forecast - by Caliber

- 10.2.1. Small Caliber

- 10.2.2. Medium Caliber

- 10.2.3. Large Caliber

- 10.3. Market Analysis, Insights and Forecast - by Material

- 10.3.1. Brass

- 10.3.2. Steel

- 10.3.3. Lead

- 10.3.4. Aluminum

- 10.3.5. Composites

- 10.4. Market Analysis, Insights and Forecast - by Platform

- 10.4.1. Land

- 10.4.2. Naval

- 10.4.3. Airborne

- 10.5. Market Analysis, Insights and Forecast - by End User

- 10.5.1. Armed Forces

- 10.5.2. Homeland Security Agencies

- 10.5.3. Police & Law Enforcement Agencies

- 10.5.4. Civilian Users

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Asia Pacific Ammunition Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Centerfire Ammunition

- 11.1.2. Rimfire Ammunition

- 11.1.3. Shotgun Ammunition

- 11.2. Market Analysis, Insights and Forecast - by Caliber

- 11.2.1. Small Caliber

- 11.2.2. Medium Caliber

- 11.2.3. Large Caliber

- 11.3. Market Analysis, Insights and Forecast - by Material

- 11.3.1. Brass

- 11.3.2. Steel

- 11.3.3. Lead

- 11.3.4. Aluminum

- 11.3.5. Composites

- 11.4. Market Analysis, Insights and Forecast - by Platform

- 11.4.1. Land

- 11.4.2. Naval

- 11.4.3. Airborne

- 11.5. Market Analysis, Insights and Forecast - by End User

- 11.5.1. Armed Forces

- 11.5.2. Homeland Security Agencies

- 11.5.3. Police & Law Enforcement Agencies

- 11.5.4. Civilian Users

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ammo Inc.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Arsenal JSCo.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 BAE Systems PLC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 CBC Global Ammunition

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Denel SOC Ltd.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Northrop Grumman Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 General Dynamics Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hanwha Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hornady Manufacturing Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Leonardo S.p.A.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Nammo AS

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Poongsan Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 MESKO S.A.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Others

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Ammo Inc.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ammunition Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 3: North America Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 5: North America Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 6: North America Ammunition Revenue (million), by Material 2025 & 2033

- Figure 7: North America Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 8: North America Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 9: North America Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 10: North America Ammunition Revenue (million), by End User 2025 & 2033

- Figure 11: North America Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 12: North America Ammunition Revenue (million), by Country 2025 & 2033

- Figure 13: North America Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 15: South America Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: South America Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 17: South America Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 18: South America Ammunition Revenue (million), by Material 2025 & 2033

- Figure 19: South America Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 20: South America Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 21: South America Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 22: South America Ammunition Revenue (million), by End User 2025 & 2033

- Figure 23: South America Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 24: South America Ammunition Revenue (million), by Country 2025 & 2033

- Figure 25: South America Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 27: Europe Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Europe Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 29: Europe Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 30: Europe Ammunition Revenue (million), by Material 2025 & 2033

- Figure 31: Europe Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 32: Europe Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 33: Europe Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 34: Europe Ammunition Revenue (million), by End User 2025 & 2033

- Figure 35: Europe Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 36: Europe Ammunition Revenue (million), by Country 2025 & 2033

- Figure 37: Europe Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 39: Middle East & Africa Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 40: Middle East & Africa Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 41: Middle East & Africa Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 42: Middle East & Africa Ammunition Revenue (million), by Material 2025 & 2033

- Figure 43: Middle East & Africa Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 44: Middle East & Africa Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 45: Middle East & Africa Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 46: Middle East & Africa Ammunition Revenue (million), by End User 2025 & 2033

- Figure 47: Middle East & Africa Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 48: Middle East & Africa Ammunition Revenue (million), by Country 2025 & 2033

- Figure 49: Middle East & Africa Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 51: Asia Pacific Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 52: Asia Pacific Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 53: Asia Pacific Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 54: Asia Pacific Ammunition Revenue (million), by Material 2025 & 2033

- Figure 55: Asia Pacific Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 56: Asia Pacific Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 57: Asia Pacific Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 58: Asia Pacific Ammunition Revenue (million), by End User 2025 & 2033

- Figure 59: Asia Pacific Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 60: Asia Pacific Ammunition Revenue (million), by Country 2025 & 2033

- Figure 61: Asia Pacific Ammunition Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 2: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 3: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 4: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 5: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 6: Global Ammunition Revenue million Forecast, by Region 2020 & 2033

- Table 7: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 8: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 9: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 10: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 11: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 12: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 13: United States Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Canada Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Mexico Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 17: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 18: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 19: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 20: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 21: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 22: Brazil Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Argentina Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 26: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 27: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 28: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 29: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 30: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Germany Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: France Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Italy Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Spain Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Russia Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Benelux Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Nordics Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 41: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 42: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 43: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 44: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 45: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 46: Turkey Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 47: Israel Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: GCC Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 49: North Africa Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: South Africa Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 53: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 54: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 55: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 56: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 57: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 58: China Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 59: India Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 60: Japan Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 61: South Korea Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 63: Oceania Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Ammunition Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ammunition?

The projected CAGR is approximately 3.7%.

2. Which companies are prominent players in the Ammunition?

Key companies in the market include Ammo Inc., Arsenal JSCo., BAE Systems PLC, CBC Global Ammunition, Denel SOC Ltd., Northrop Grumman Corporation, General Dynamics Corporation, Hanwha Corporation, Hornady Manufacturing, Inc., Leonardo S.p.A., Nammo AS, Poongsan Corporation, MESKO S.A., Others.

3. What are the main segments of the Ammunition?

The market segments include Product Type, Caliber, Material, Platform, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 11620 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ammunition," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ammunition report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ammunition?

To stay informed about further developments, trends, and reports in the Ammunition, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence