Key Insights

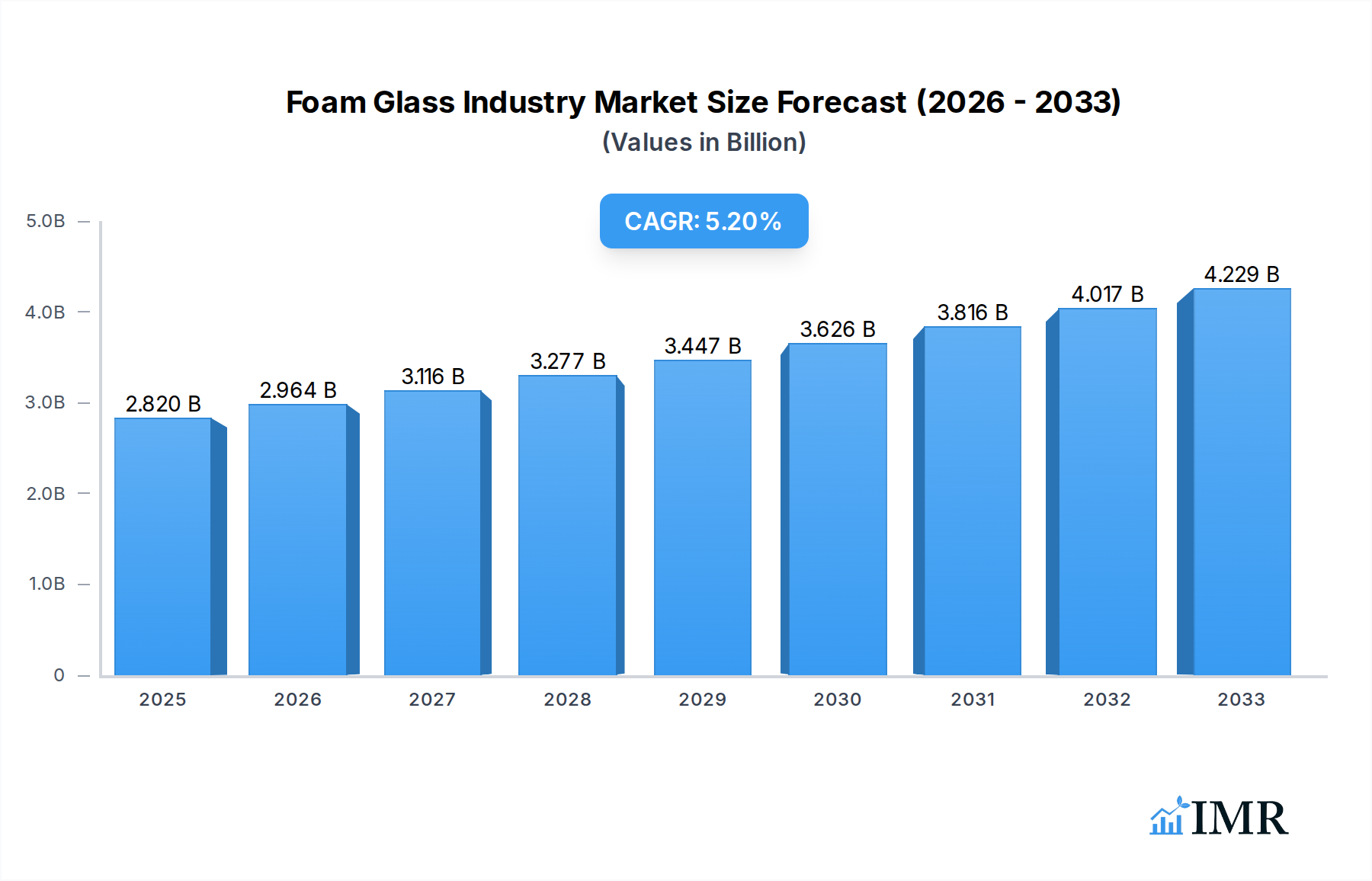

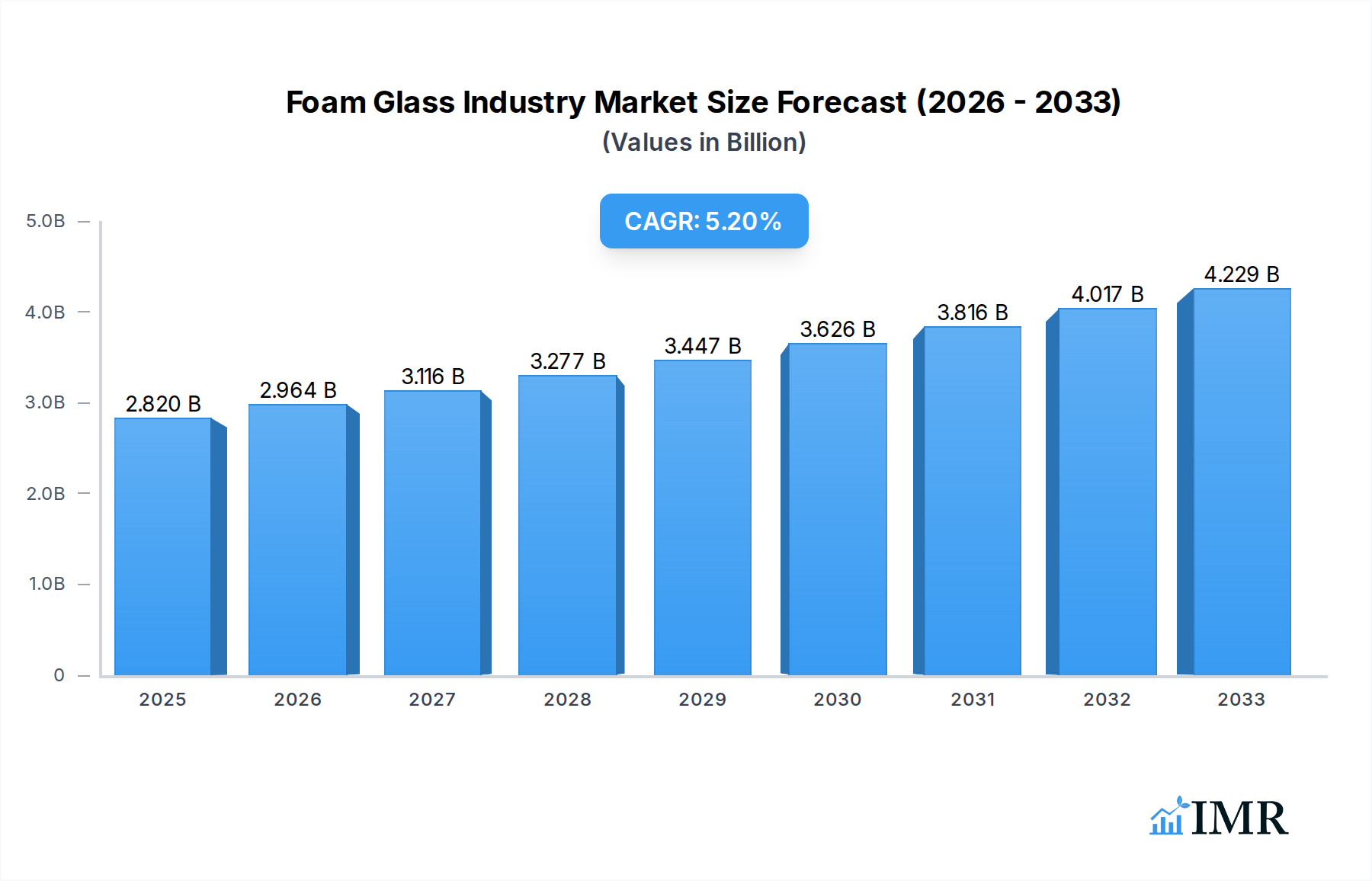

The global Foam Glass market is poised for robust expansion, projected to reach USD 2.82 billion in 2025 and grow at a significant Compound Annual Growth Rate (CAGR) of 5.04% through 2033. This upward trajectory is primarily fueled by escalating demand for advanced insulation materials across various end-user industries. The commercial and residential sectors, in particular, are witnessing increased adoption of foam glass due to its superior thermal performance, fire resistance, and moisture impermeability, aligning with stringent building codes and growing environmental consciousness. The industrial segment also contributes substantially, with foam glass finding applications in chemical plants, food processing facilities, and HVAC systems where its durability and inertness are crucial. Key drivers include the growing emphasis on energy efficiency in buildings, the need for sustainable construction practices, and the inherent advantages of foam glass over traditional insulation materials. These factors are creating a fertile ground for market players to innovate and expand their offerings.

Foam Glass Industry Market Size (In Billion)

The market's dynamism is further shaped by evolving trends such as the development of innovative manufacturing processes that enhance foam glass properties and reduce production costs. The increasing focus on circular economy principles is also driving research into recycled content for foam glass production. However, the market encounters certain restraints. The relatively higher initial cost compared to some conventional insulation materials can be a deterrent for price-sensitive projects. Additionally, the complex manufacturing process and the requirement for specialized handling can pose challenges for widespread adoption in certain regions. Despite these hurdles, the inherent benefits of foam glass, including its long lifespan and environmental friendliness, are expected to outweigh these limitations, ensuring sustained market growth. Strategic investments in research and development, coupled with targeted marketing efforts, will be crucial for companies to capitalize on the burgeoning opportunities in this sector.

Foam Glass Industry Company Market Share

Foam Glass Industry: Comprehensive Market Analysis & Future Outlook (2019–2033)

This in-depth report provides a comprehensive analysis of the global Foam Glass Industry, a rapidly evolving sector critical for sustainable construction, insulation, and specialized industrial applications. The study encompasses a detailed examination of market dynamics, growth trends, regional dominance, product innovations, key drivers, challenges, emerging opportunities, and the strategic landscape shaped by leading companies. Covering the historical period from 2019 to 2024, the base year of 2025, and a forecast period extending to 2033, this report offers invaluable insights for stakeholders seeking to navigate and capitalize on the burgeoning foam glass market. We analyze both parent market (building insulation materials) and child market (specific foam glass applications) to provide a holistic view of market potential. All monetary values are presented in USD Billion.

Foam Glass Industry Market Dynamics & Structure

The global Foam Glass Industry is characterized by a moderately concentrated market structure, with a mix of established global players and emerging regional manufacturers. Technological innovation is a primary driver, particularly in enhancing insulation performance, fire resistance, and eco-friendly production processes. The increasing demand for sustainable and energy-efficient building materials globally is further fueling innovation in this sector. Regulatory frameworks, such as stringent building codes promoting energy conservation and the use of recycled materials, are creating a favorable environment for foam glass adoption. Competitive product substitutes, including traditional insulation materials like mineral wool, polystyrene foam, and polyisocyanurate, present ongoing competition, but foam glass's unique properties like non-combustibility and water resistance are differentiating factors. End-user demographics are shifting towards environmentally conscious consumers and developers seeking long-term performance and reduced operational costs. Mergers and acquisitions (M&A) trends are observed as companies aim to expand their product portfolios, geographical reach, and technological capabilities.

- Market Concentration: A few key players hold significant market share, but the presence of numerous smaller manufacturers indicates potential for market fragmentation and niche specialization.

- Technological Innovation Drivers: Focus on improving thermal conductivity, increasing compressive strength, developing lightweight variants, and integrating recycled glass content.

- Regulatory Frameworks: Building energy efficiency standards, fire safety regulations, and mandates for sustainable construction materials are key influences.

- Competitive Product Substitutes: Mineral wool, XPS, EPS, PIR, and spray foam are key competitors; differentiation lies in unique properties and life-cycle cost.

- End-User Demographics: Growing demand from green building initiatives, commercial developers focused on LEED certifications, and homeowners prioritizing energy savings.

- M&A Trends: Strategic acquisitions to gain market access, acquire new technologies, and consolidate production capabilities.

Foam Glass Industry Growth Trends & Insights

The Foam Glass Industry is poised for substantial growth, driven by an escalating global demand for high-performance, sustainable insulation solutions. The market size is projected to expand significantly from an estimated USD 3.5 billion in 2025 to USD 6.2 billion by 2033, reflecting a Compound Annual Growth Rate (CAGR) of approximately 7.5%. This robust growth trajectory is underpinned by increasing awareness of energy efficiency, stricter environmental regulations, and the superior performance characteristics of foam glass compared to traditional insulation materials. Adoption rates are accelerating, particularly in regions with aggressive climate action plans and a strong focus on green building certifications.

Technological disruptions are playing a crucial role, with advancements in manufacturing processes leading to improved product consistency, reduced production costs, and the development of specialized foam glass products for diverse applications. For instance, innovations in creating finer cell structures are enhancing thermal insulation capabilities, while advancements in additives are improving fire retardancy and mechanical strength. Consumer behavior is also shifting, with a growing preference for durable, non-toxic, and environmentally responsible building materials. Developers and homeowners are increasingly valuing the long-term benefits of foam glass, including its longevity, resistance to moisture and pests, and its contribution to a healthier indoor environment. The child market focusing on high-performance insulation in demanding applications like industrial piping and cryogenic storage is experiencing particularly rapid expansion. The parent market for overall building insulation continues to see foam glass gain traction as a premium, sustainable alternative.

- Market Size Evolution: Projected to grow from USD 3.5 billion in 2025 to USD 6.2 billion by 2033.

- CAGR: Anticipated at 7.5% over the forecast period, indicating strong market expansion.

- Adoption Rates: Increasing adoption driven by sustainability mandates and energy efficiency goals.

- Technological Disruptions: Innovations in production, material science, and application-specific formulations are key.

- Consumer Behavior Shifts: Growing demand for eco-friendly, durable, and healthy building materials.

- Market Penetration: Expanding penetration into new construction and retrofitting projects globally.

- Forecasting Accuracy: Based on robust analysis of historical data, industry trends, and expert insights.

Dominant Regions, Countries, or Segments in Foam Glass Industry

The Closed Cell segment is currently the dominant force within the Foam Glass Industry, accounting for an estimated 65% of the total market share in 2025. This dominance is attributed to its superior insulation properties, excellent moisture resistance, and high compressive strength, making it ideal for a wide range of demanding applications. The Commercial end-user industry represents the largest segment, contributing approximately 50% to the global market revenue in 2025. This is driven by large-scale construction projects, the increasing focus on energy-efficient buildings, and the demand for durable, fire-resistant insulation materials in commercial spaces.

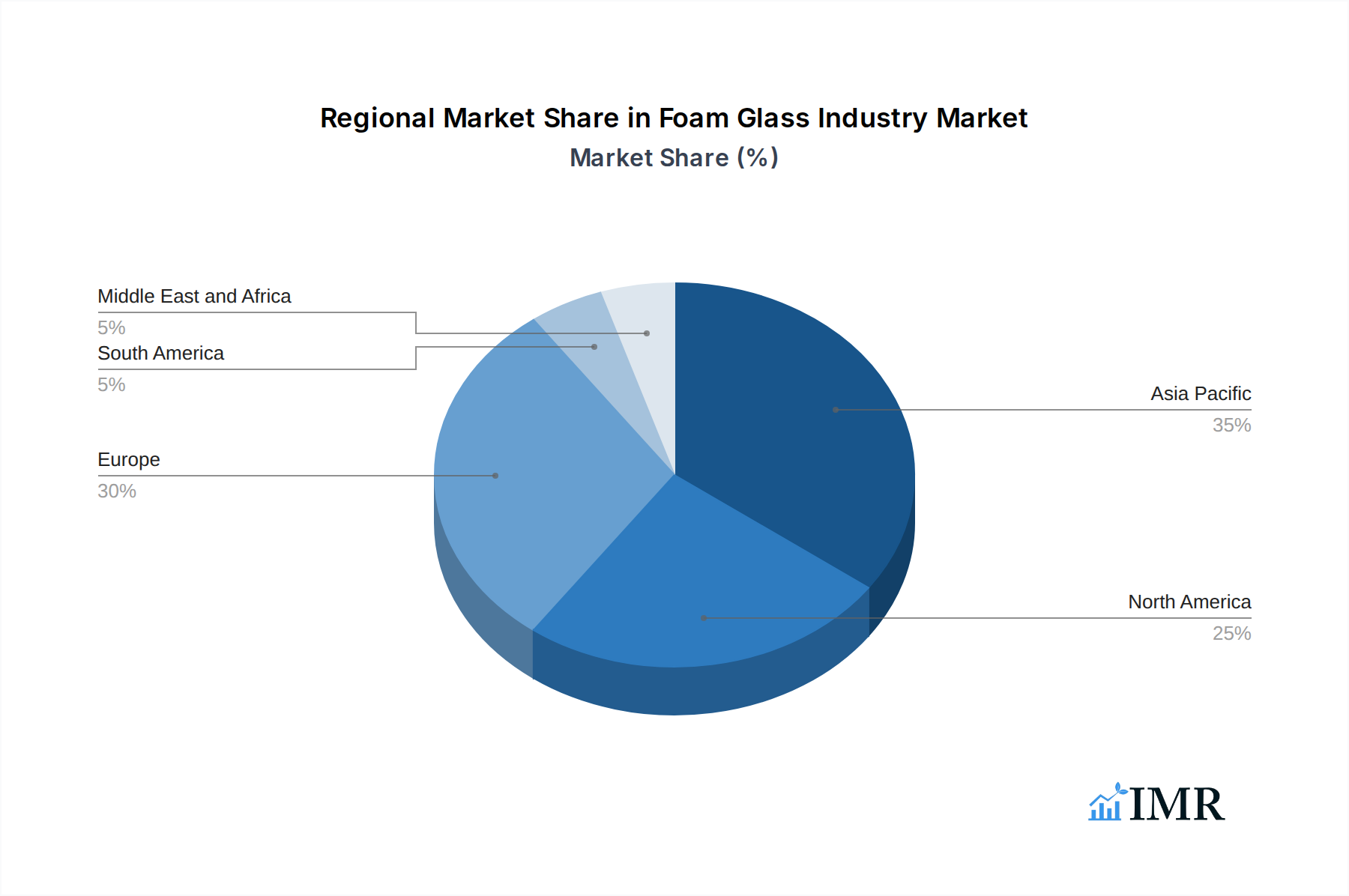

Regionally, Europe is expected to maintain its leading position in the Foam Glass Industry throughout the forecast period, driven by stringent environmental regulations, widespread adoption of energy-efficient building standards, and a strong commitment to sustainability. Countries like Germany, with established manufacturers and a mature market for insulation materials, are key contributors. The Industrial end-user industry is also a significant growth driver, particularly in sectors like chemical processing, oil and gas, and pharmaceuticals, where extreme temperature control and chemical resistance are paramount.

- Dominant Segment (Type): Closed Cell

- Market Share (2025): Approximately 65%.

- Key Drivers: Superior thermal insulation, excellent moisture barrier, high compressive strength, suitability for diverse environmental conditions.

- Dominant Segment (End-user Industry): Commercial

- Market Share (2025): Approximately 50%.

- Key Drivers: Large-scale construction, green building initiatives, demand for energy efficiency and fire safety in corporate, retail, and hospitality sectors.

- Dominant Region: Europe

- Key Drivers: Strict energy efficiency codes (e.g., EPBD), government incentives for sustainable construction, high consumer awareness, established manufacturing base.

- Leading Countries: Germany, France, United Kingdom, Scandinavia.

- Growth Potential: Emerging markets in Asia-Pacific and North America are exhibiting strong growth potential due to increasing infrastructure development and rising environmental consciousness.

- Market Share Analysis: Detailed breakdown of regional and segment market shares is available within the full report.

Foam Glass Industry Product Landscape

The Foam Glass Industry product landscape is marked by continuous innovation, focusing on enhanced performance and broader applicability. Key product innovations include advanced formulations for higher compressive strength, superior thermal resistance (lower lambda values), and improved fireproofing capabilities. Unique selling propositions of modern foam glass products lie in their inherent non-combustibility, zero moisture absorption, rodent and insect resistance, and dimensional stability, making them ideal for challenging environments. Technological advancements are also enabling the production of lightweight foam glass aggregates for concrete and other building materials, offering a sustainable and performance-enhancing alternative to traditional aggregates. Applications are expanding beyond traditional insulation to include acoustic panels, decorative elements, and specialized industrial uses like pipe insulation in cryogenic applications.

Key Drivers, Barriers & Challenges in Foam Glass Industry

Key Drivers:

- Growing Demand for Energy Efficiency: Escalating global focus on reducing energy consumption in buildings and industrial processes.

- Stringent Environmental Regulations: Government mandates and building codes promoting sustainable materials and energy conservation.

- Superior Product Performance: Non-combustibility, zero moisture absorption, durability, and chemical resistance offer a competitive edge.

- Increasing Use of Recycled Materials: Foam glass production often utilizes recycled glass, aligning with circular economy principles.

- Technological Advancements: Improved manufacturing processes and product formulations enhance performance and cost-effectiveness.

Barriers & Challenges:

- Higher Initial Cost: Compared to some conventional insulation materials, the upfront cost of foam glass can be a deterrent.

- Manufacturing Complexity: Production processes require specialized equipment and expertise, potentially limiting entry for new players.

- Awareness and Education: A need for greater awareness among architects, builders, and consumers about the benefits of foam glass.

- Supply Chain Constraints: Sourcing of raw materials and efficient distribution networks can pose challenges.

- Competition from Established Materials: Existing market penetration of mineral wool and foam plastics presents strong competition.

- Energy Intensity of Production: While the end product is energy-efficient, the manufacturing process itself can be energy-intensive.

Emerging Opportunities in Foam Glass Industry

Emerging opportunities in the Foam Glass Industry are manifold, driven by evolving market demands and technological frontiers. The growing trend of sustainable and "green" construction presents a significant avenue for expansion, as foam glass aligns perfectly with these principles. Untapped markets in developing economies with increasing infrastructure investments and a rising focus on energy efficiency offer substantial growth potential. Innovative applications are emerging in areas such as lightweight insulating concrete, advanced fire-resistant building panels, and specialized insulation for renewable energy infrastructure (e.g., solar farms, wind turbines). Furthermore, the increasing demand for durable and low-maintenance materials in the face of climate change impacts (e.g., extreme weather events) positions foam glass as a superior solution.

Growth Accelerators in the Foam Glass Industry Industry

Several key catalysts are accelerating the growth of the Foam Glass Industry. Technological breakthroughs in production efficiency and material science are continuously improving the cost-effectiveness and performance of foam glass products, making them more competitive. Strategic partnerships between manufacturers and construction firms, as well as collaborations with research institutions, are fostering innovation and accelerating product development. Market expansion strategies, including entering new geographical regions and targeting underserved application segments, are crucial growth drivers. The increasing emphasis on life-cycle assessment and the circular economy principles further bolsters the appeal of foam glass due to its durability and recyclability, acting as significant growth accelerators for the industry.

Key Players Shaping the Foam Glass Industry Market

- Refaglass

- Misapor AG

- PINOSKLO cellular glass

- ICM Glass Kaluga LLC

- Owens Corning

- GEOCELL Schaumglas GmbH

- AeroAggregates of North America LLC

- Glapor Werk Mitterteich GmbH

- Glevel

- Styro Ltd

- Anhui Huichang New Material Co Ltd

- Ningbo Yoyo Foam Glass Co Ltd

- Zhejiang Zhenshen Insulation Technology Corp

- Polydros SA

- Uusioaines Oy

(List Not Exhaustive)

Notable Milestones in Foam Glass Industry Sector

- 2021: Launch of a new generation of ultra-lightweight foam glass aggregates by AeroAggregates of North America LLC, improving ease of handling and reducing structural load.

- 2022: GEOCELL Schaumglas GmbH expands its production capacity to meet the surging demand for high-performance insulation in the European construction market.

- 2023: Refaglass introduces advanced foam glass boards with enhanced fire resistance ratings, catering to stricter safety regulations in commercial construction.

- Q1 2024: Misapor AG announces a partnership with a leading architectural firm to explore innovative design applications of foam glass in sustainable urban development projects.

- 2024: ICM Glass Kaluga LLC begins exporting its specialized foam glass products to new markets in Eastern Europe, capitalizing on growing industrial insulation needs.

- 2024: Owens Corning invests in research and development to explore hybrid foam glass solutions that combine insulation with acoustic properties.

- 2025 (Projected): Glapor Werk Mitterteich GmbH is expected to unveil a new manufacturing process that significantly reduces energy consumption and carbon footprint.

- 2025 (Projected): A significant increase in M&A activity is anticipated as larger players seek to acquire innovative smaller companies or expand their market share.

In-Depth Foam Glass Industry Market Outlook

The future outlook for the Foam Glass Industry is exceptionally positive, driven by a confluence of global trends and inherent product advantages. The increasing imperative for sustainable construction, coupled with stringent energy efficiency regulations worldwide, ensures a sustained and growing demand for high-performance insulation materials. Foam glass, with its unique combination of thermal insulation, fire resistance, moisture impermeability, and durability, is exceptionally well-positioned to capture a significant share of this expanding market. Growth accelerators, including continuous technological advancements in production and material properties, coupled with strategic market expansion by key players, will further propel industry expansion. The industry is set to witness further innovation in application-specific products and a deepening penetration into both residential and industrial sectors, solidifying its role as a crucial component of modern, sustainable infrastructure.

Foam Glass Industry Segmentation

-

1. Type

- 1.1. Open Cell

- 1.2. Closed Cell

- 1.3. Other Types

-

2. End-user Industry

- 2.1. Commercial

- 2.2. Residential

- 2.3. Industrial

Foam Glass Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Foam Glass Industry Regional Market Share

Geographic Coverage of Foam Glass Industry

Foam Glass Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Open Cell

- 5.1.2. Closed Cell

- 5.1.3. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Commercial

- 5.2.2. Residential

- 5.2.3. Industrial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Foam Glass Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Open Cell

- 6.1.2. Closed Cell

- 6.1.3. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Commercial

- 6.2.2. Residential

- 6.2.3. Industrial

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Asia Pacific Foam Glass Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Open Cell

- 7.1.2. Closed Cell

- 7.1.3. Other Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Commercial

- 7.2.2. Residential

- 7.2.3. Industrial

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. North America Foam Glass Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Open Cell

- 8.1.2. Closed Cell

- 8.1.3. Other Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Commercial

- 8.2.2. Residential

- 8.2.3. Industrial

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Foam Glass Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Open Cell

- 9.1.2. Closed Cell

- 9.1.3. Other Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Commercial

- 9.2.2. Residential

- 9.2.3. Industrial

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Foam Glass Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Open Cell

- 10.1.2. Closed Cell

- 10.1.3. Other Types

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Commercial

- 10.2.2. Residential

- 10.2.3. Industrial

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Foam Glass Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Open Cell

- 11.1.2. Closed Cell

- 11.1.3. Other Types

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Commercial

- 11.2.2. Residential

- 11.2.3. Industrial

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Refaglass

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Misapor AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 PINOSKLO cellular glass

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ICM Glass Kaluga LLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Owens Corning

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GEOCELL Schaumglas GmbH

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 AeroAggregates of North America LLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Glapor Werk Mitterteich GmbH

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Glevel

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Styro Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Anhui Huichang New Material Co Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ningbo Yoyo Foam Glass Co Ltd

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Zhejiang Zhenshen Insulation Technology Corp *List Not Exhaustive

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Polydros SA

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Uusioaines Oy

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Refaglass

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Foam Glass Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Foam Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: Asia Pacific Foam Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific Foam Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Foam Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Foam Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Foam Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Foam Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: North America Foam Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Foam Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: North America Foam Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Foam Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Foam Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Foam Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe Foam Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Foam Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe Foam Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Foam Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Foam Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Foam Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: South America Foam Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Foam Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: South America Foam Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: South America Foam Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Foam Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Foam Glass Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Foam Glass Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Foam Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Foam Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Foam Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Foam Glass Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Foam Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Foam Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Foam Glass Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Foam Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Foam Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Foam Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Foam Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global Foam Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Foam Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Foam Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 19: Global Foam Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Foam Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: France Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Foam Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 27: Global Foam Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Foam Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Foam Glass Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 33: Global Foam Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Foam Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Foam Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Foam Glass Industry?

The projected CAGR is approximately 5.04%.

2. Which companies are prominent players in the Foam Glass Industry?

Key companies in the market include Refaglass, Misapor AG, PINOSKLO cellular glass, ICM Glass Kaluga LLC, Owens Corning, GEOCELL Schaumglas GmbH, AeroAggregates of North America LLC, Glapor Werk Mitterteich GmbH, Glevel, Styro Ltd, Anhui Huichang New Material Co Ltd, Ningbo Yoyo Foam Glass Co Ltd, Zhejiang Zhenshen Insulation Technology Corp *List Not Exhaustive, Polydros SA, Uusioaines Oy.

3. What are the main segments of the Foam Glass Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.82 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Demand From the Industrial Sector; Other Drivers.

6. What are the notable trends driving market growth?

Industrial Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

; High Capital Investment; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Foam Glass Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Foam Glass Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Foam Glass Industry?

To stay informed about further developments, trends, and reports in the Foam Glass Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence