Key Insights

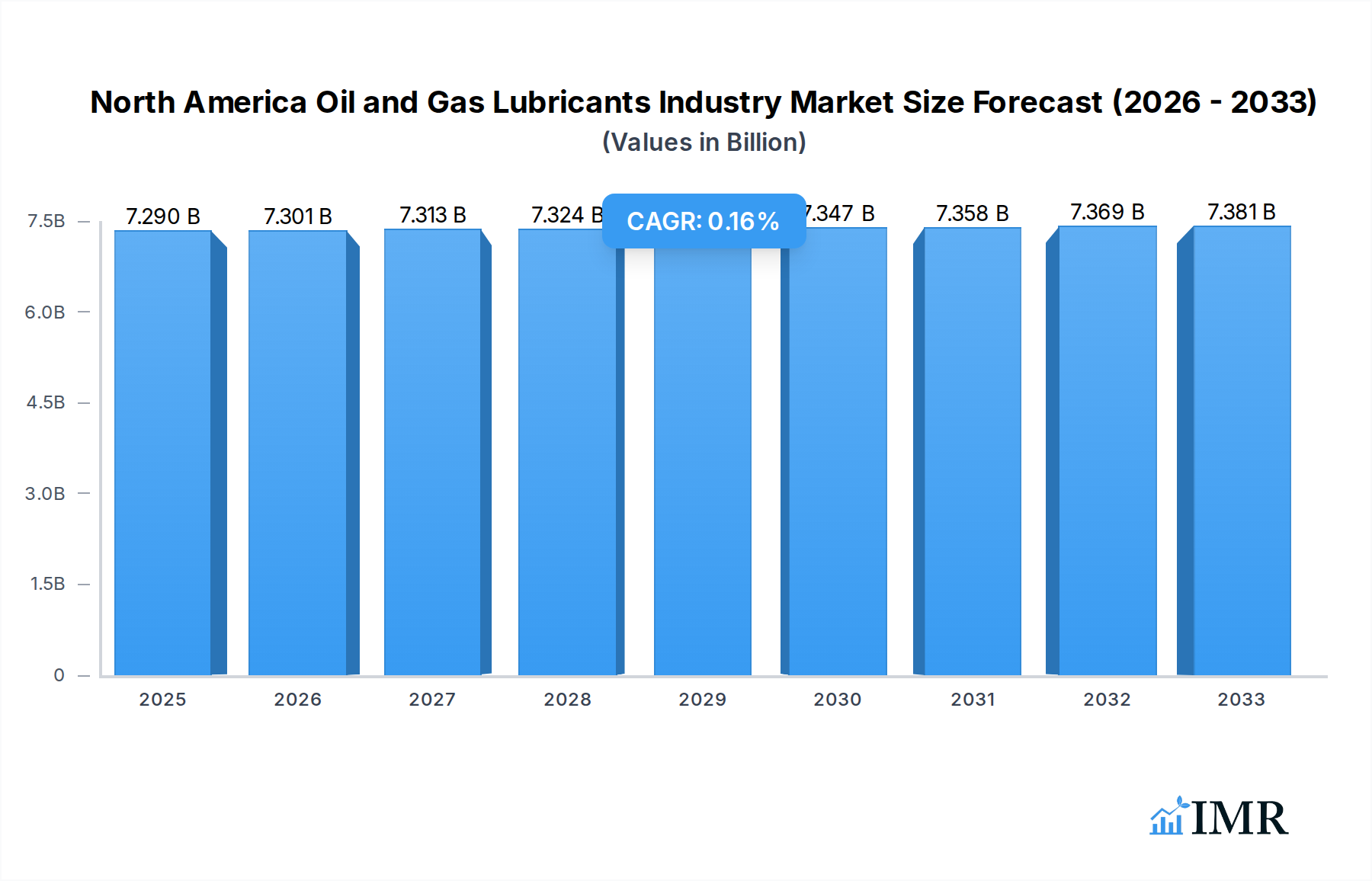

The North American oil and gas lubricants market is poised for a period of modest growth, driven by essential operational needs across the sector. The market size for 2025 is estimated at $7,290 million, with a projected Compound Annual Growth Rate (CAGR) of 0.16% through 2033. This steady expansion is primarily fueled by the consistent demand for high-performance lubricants that ensure the efficient and extended lifespan of critical machinery in upstream exploration and production, midstream transportation, and downstream refining operations. Factors such as the ongoing need to maintain aging infrastructure, coupled with technological advancements in lubricant formulations offering improved protection and efficiency, are key drivers. The prevalence of both onshore and offshore operations, particularly in regions like the United States and Canada, contributes significantly to the market's stability.

North America Oil and Gas Lubricants Industry Market Size (In Billion)

Despite the overall slow growth, specific segments are expected to demonstrate resilience and offer opportunities. Engine oils and hydraulic fluids remain dominant product categories due to their indispensable role in powering and controlling a vast array of equipment. The United States, with its extensive oil and gas reserves and sophisticated infrastructure, commands the largest market share. While the industry faces challenges such as increasing environmental regulations and the growing adoption of electric vehicles which could impact demand in the long term for certain lubricant types, the fundamental necessity of specialized lubricants for the ongoing extraction, processing, and distribution of hydrocarbons ensures continued market relevance. Innovations in biodegradable lubricants and synthetic formulations are also emerging trends that could shape future market dynamics.

North America Oil and Gas Lubricants Industry Company Market Share

North America Oil and Gas Lubricants Industry Report Description

Unlock unparalleled insights into the North America Oil and Gas Lubricants Industry with this comprehensive market intelligence report. Covering the extensive Study Period of 2019–2033, with a Base Year of 2025 and a robust Forecast Period of 2025–2033, this report offers a deep dive into market dynamics, growth drivers, competitive landscape, and emerging opportunities.

This definitive research delves into critical segments, including Location (Onshore, Offshore), Product Type (Grease, Coolant/Anti-freezer, Engine Oils, Hydraulic Fluids, Other Product Types), Sector (Upstream, Midstream, Downstream), and Geography (United States, Canada, Mexico). Gain a granular understanding of the parent market and its vital child markets, essential for strategic decision-making in the dynamic North American energy sector.

High-traffic keywords such as "North America Oil and Gas Lubricants," "Lubricant Market Share," "Hydraulic Fluids Demand," "Engine Oils Forecast," "Upstream Lubricants," "Midstream Lubricant Solutions," "Downstream Lubricant Market," "Onshore Lubricant Applications," "Offshore Lubricant Needs," "Lubricant Industry Trends," "Oil and Gas Lubricant Companies," and "Lubricant Market Size United States" are intricately woven into this report to ensure maximum search engine visibility and reach industry professionals actively seeking this specialized information.

The report features an in-depth analysis of key players including BP PLC, Chevron Corporation, Eni S p A, Exxon Mobil Corporation, Lubrication Engineers Inc, LUKOIL, Petro-Canada Lubricants Inc, Shell PLC, Schlumberger Limited, SKF, TotalEnergies SE, and Valvoline Inc (List Not Exhaustive). Discover strategic moves, market positioning, and their impact on the broader industry.

North America Oil and Gas Lubricants Industry Market Dynamics & Structure

The North America oil and gas lubricants market exhibits a moderately concentrated structure, with a few major players holding significant market share. This concentration is driven by substantial capital investment requirements, established distribution networks, and the need for advanced R&D capabilities. Technological innovation is a primary driver, with ongoing advancements in synthetic lubricants offering superior performance, extended drain intervals, and enhanced fuel efficiency, crucial for optimizing operations in demanding upstream, midstream, and downstream applications. Regulatory frameworks, particularly those concerning environmental impact and emissions, are increasingly shaping product development, pushing for more eco-friendly and sustainable lubricant formulations. Competitive product substitutes, such as biodegradable lubricants and advanced material coatings, are emerging but have yet to fully displace traditional oil-based lubricants in many critical applications due to cost and performance considerations. End-user demographics are shifting towards a greater demand for specialized lubricants that can withstand extreme temperatures and pressures inherent in offshore and deep-well drilling operations. Mergers and acquisitions (M&A) are a notable trend, as companies seek to expand their product portfolios, geographic reach, and technological expertise. For instance, the strategic acquisition of Allied Reliability by Shell PLC in December 2022 underscores this trend, aimed at bolstering its industrial lubricant offerings and service capabilities.

- Market Concentration: Dominated by a few key multinational corporations with established brand presence and distribution.

- Technological Innovation Drivers: Development of synthetic lubricants, bio-based formulations, and specialized additives for enhanced performance and sustainability.

- Regulatory Frameworks: Increasingly stringent environmental regulations driving the adoption of low-emission and biodegradable lubricant solutions.

- Competitive Product Substitutes: Emerging bio-lubricants and advanced coatings, though facing adoption challenges due to performance and cost factors.

- End-User Demographics: Growing demand for high-performance lubricants in extreme environments and for energy-efficient operations.

- M&A Trends: Strategic acquisitions and mergers to gain market share, acquire new technologies, and expand service offerings.

North America Oil and Gas Lubricants Industry Growth Trends & Insights

The North America oil and gas lubricants market is poised for robust growth, projected to experience a healthy Compound Annual Growth Rate (CAGR) throughout the forecast period. This expansion is intrinsically linked to the sustained activity in the upstream sector, particularly in the exploration and production of unconventional resources like shale oil and gas, which necessitate high-performance lubricants for drilling equipment and extraction machinery. The midstream sector, with its extensive pipeline networks, also presents a consistent demand for lubricants essential for the smooth operation of compressors, pumps, and other vital infrastructure. Furthermore, the downstream segment, encompassing refining and petrochemical operations, continues to require a wide array of specialized lubricants to maintain the efficiency and longevity of complex processing units.

Technological disruptions are playing a pivotal role in reshaping the market. The increasing adoption of advanced synthetic lubricants, formulated with sophisticated additive packages, is enhancing equipment reliability, reducing maintenance costs, and improving energy efficiency across all segments of the oil and gas value chain. These advanced lubricants offer superior thermal stability, oxidative resistance, and wear protection compared to conventional mineral oils, making them indispensable for modern, high-pressure, and high-temperature operating environments. Consumer behavior shifts within the industry are also influencing demand. There is a growing preference for lubricants that offer extended service life, thereby minimizing downtime and operational disruptions, and for products that align with increasing environmental sustainability goals. This is leading to a greater demand for bio-based and biodegradable lubricants, especially in environmentally sensitive regions or applications.

The market penetration of high-performance lubricants is steadily increasing as companies recognize the long-term cost savings and operational benefits associated with their use. For instance, the transition from conventional engine oils to synthetic variants in heavy-duty diesel engines used in exploration and transportation fleets is a significant trend. Furthermore, the development of specialized hydraulic fluids that can withstand extreme pressure and temperature variations is crucial for the efficient functioning of sophisticated drilling rigs and offshore platforms. The report estimates the North America oil and gas lubricants market to reach approximately USD 28.5 billion in 2025, with projections indicating a steady climb to over USD 35 billion by 2033, driven by these evolving trends and sustained energy demand. The increasing focus on operational efficiency and asset protection will continue to fuel the demand for premium lubricant solutions.

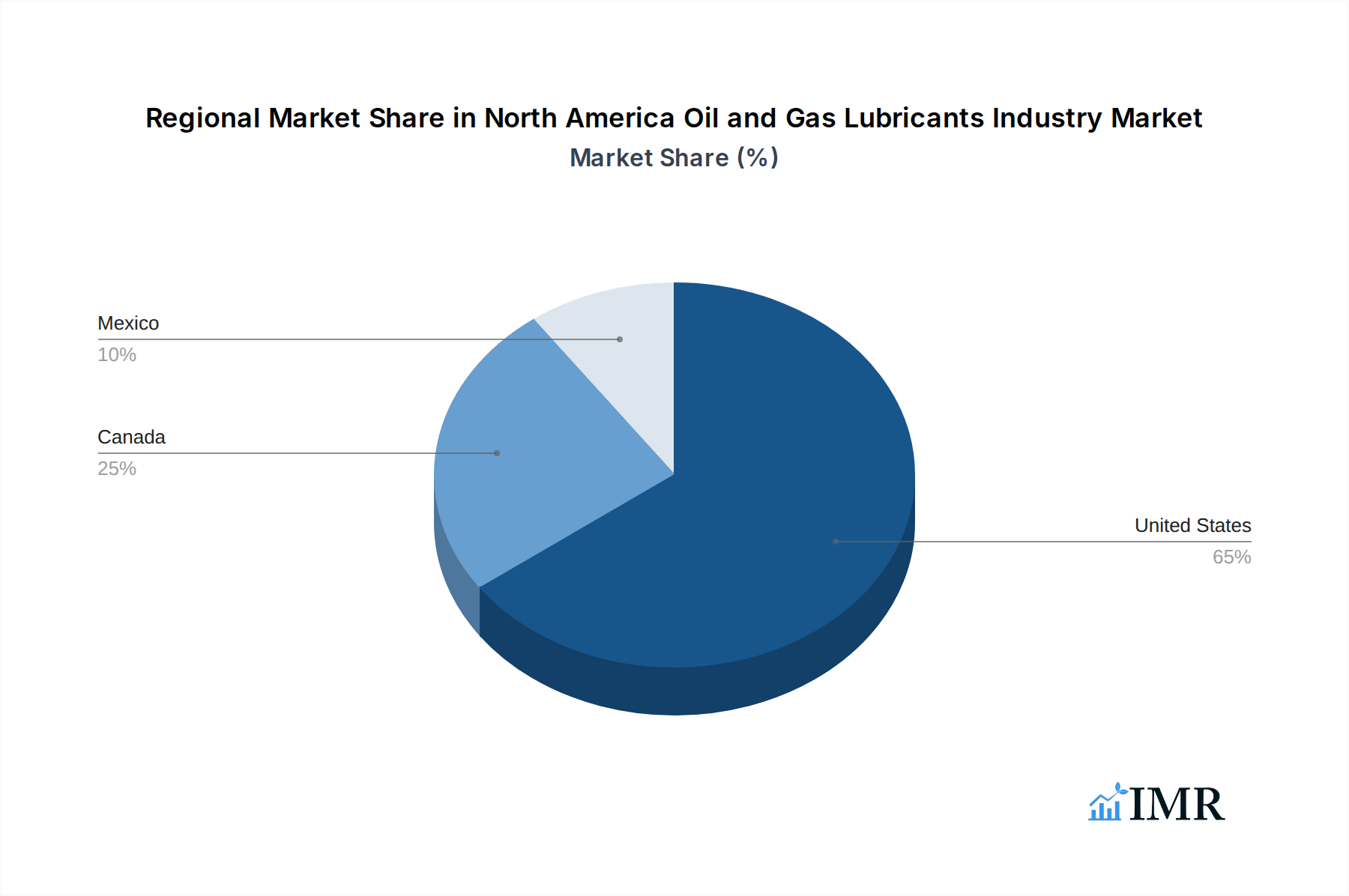

Dominant Regions, Countries, or Segments in North America Oil and Gas Lubricants Industry

The United States unequivocally dominates the North America oil and gas lubricants market, driven by its vast and active energy sector. This dominance is multifaceted, stemming from its status as a leading producer of oil and natural gas, with extensive upstream operations, particularly in shale plays like the Permian Basin and the Marcellus Shale. The sheer scale of drilling, extraction, and processing activities necessitates a colossal demand for a diverse range of lubricants. The US also boasts a mature midstream infrastructure of pipelines and storage facilities, along with a significant refining capacity in its downstream sector, all of which are substantial consumers of lubricants.

Within the US, the Onshore location segment is the primary driver of lubricant demand. The proliferation of horizontal drilling and hydraulic fracturing techniques has intensified the need for high-performance lubricants that can withstand the rigors of continuous operation in challenging terrestrial environments. This includes specialized engine oils for drilling rigs and transport vehicles, hydraulic fluids for excavation and pumping equipment, and greases for bearings and machinery components.

Considering product types, Engine Oils represent a significant segment due to the extensive use of internal combustion engines in exploration vehicles, trucks, and stationary power generation units across the upstream and midstream operations. Hydraulic Fluids are also crucial, powering the complex machinery and equipment used in drilling, production, and transportation. The Upstream sector is the largest contributor to overall lubricant consumption, reflecting the capital-intensive nature of exploration and extraction activities. The relentless pursuit of new reserves and enhanced recovery techniques in regions like the Gulf of Mexico (for offshore) and across onshore basins ensures a continuous demand for specialized upstream lubricants.

Canada, with its significant oil sands operations and natural gas production, particularly in Alberta, also represents a substantial market. Its cold climate necessitates specialized winter-grade lubricants. Mexico, while having a long history in oil production, is undergoing a revitalization of its energy sector, presenting growing opportunities for lubricant suppliers. The interplay of economic policies promoting energy independence, substantial infrastructure investments, and the technological advancement in extraction methods within these countries collectively solidify the dominance of the US and support the overall growth of the North American lubricants market. The market share of the United States in this sector is estimated to be over 65%, with Canada following with approximately 25%, and Mexico contributing the remaining 10%.

- Dominant Geography: United States, accounting for over 65% of the market share.

- Key Location Segment: Onshore, driven by extensive drilling and extraction activities.

- Major Product Type: Engine Oils, critical for operational fleets and machinery.

- Leading Sector: Upstream, due to the high demand for lubricants in exploration and production.

- Key Drivers: Robust exploration and production activities, extensive midstream infrastructure, and advanced refining capabilities.

North America Oil and Gas Lubricants Industry Product Landscape

The product landscape for North America oil and gas lubricants is characterized by a strong emphasis on innovation, performance enhancement, and environmental compliance. The development of advanced synthetic lubricants, including Group IV (PAO) and Group V base oils, is a significant trend. These lubricants offer superior viscosity-temperature characteristics, excellent thermal and oxidative stability, and reduced volatility, leading to longer drain intervals and reduced oil consumption. Specialized formulations for extreme operating conditions, such as high-temperature, high-pressure, and corrosive environments found in deep-well drilling and offshore platforms, are increasingly in demand. Additive technology is also a key area of development, with advanced packages providing enhanced anti-wear, anti-corrosion, detergency, and dispersancy properties, crucial for protecting expensive equipment and maintaining optimal operational efficiency. The push for sustainability is also driving the adoption of biodegradable and bio-based lubricants, particularly for applications with a higher risk of environmental release.

Key Drivers, Barriers & Challenges in North America Oil and Gas Lubricants Industry

Key Drivers:

The North America oil and gas lubricants industry is propelled by several key drivers. Sustained upstream activity, including exploration and production, especially in shale plays, directly fuels the demand for lubricants. Technological advancements in drilling and extraction equipment necessitate high-performance lubricants that can operate under extreme conditions. The expanding midstream infrastructure, requiring lubricants for pipelines, pumps, and compressors, provides a stable demand base. Furthermore, increasing emphasis on equipment longevity, reduced maintenance costs, and operational efficiency incentivizes the adoption of premium and synthetic lubricants. Growing environmental consciousness and regulatory pressures are also driving the development and adoption of more sustainable, biodegradable lubricant options.

- Upstream Activity: Continued exploration and production, particularly shale oil and gas.

- Technological Advancements: Sophisticated equipment requiring high-performance lubrication.

- Midstream Infrastructure Growth: Expansion and maintenance of pipelines and transportation networks.

- Operational Efficiency Focus: Demand for lubricants that reduce downtime and maintenance costs.

- Environmental Regulations: Push for eco-friendly and biodegradable lubricant solutions.

Barriers & Challenges:

Despite the growth, the industry faces several barriers and challenges. Fluctuations in crude oil prices can directly impact exploration and production budgets, subsequently affecting lubricant demand. Intense competition from both established global players and emerging regional manufacturers can lead to price pressures and margin erosion. The high cost of advanced synthetic lubricants, while offering long-term benefits, can be a barrier to adoption for smaller operators or in price-sensitive segments. Supply chain disruptions, amplified by geopolitical events and natural disasters, can affect the availability and cost of raw materials and finished products. Stringent and evolving environmental regulations, while a driver for innovation, also present compliance challenges and can increase R&D and production costs.

- Price Volatility of Crude Oil: Directly impacts E&P budgets and lubricant demand.

- Intense Competition: Price wars and market saturation among various players.

- High Cost of Premium Lubricants: Barrier for some segments and smaller operators.

- Supply Chain Vulnerabilities: Disruptions impacting raw material availability and logistics.

- Regulatory Compliance: Evolving environmental standards and their associated costs.

Emerging Opportunities in North America Oil and Gas Lubricants Industry

Emerging opportunities in the North America oil and gas lubricants industry lie in the growing demand for specialized lubricants catering to niche applications and evolving operational needs. The push towards digitalization and the use of IoT sensors for predictive maintenance in oilfield equipment is creating opportunities for smart lubricants that can provide real-time performance data. Furthermore, the expansion of offshore renewable energy installations, such as offshore wind farms, presents a new frontier for lubricant manufacturers, requiring specialized marine-grade lubricants. The increasing focus on decarbonization within the energy sector is also fostering innovation in lubricants for alternative fuels and electric vehicle applications within the broader industrial context. Untapped markets in remote exploration regions and the development of tailored solutions for emerging extraction technologies also offer significant growth potential.

Growth Accelerators in the North America Oil and Gas Lubricants Industry Industry

Several catalysts are accelerating the growth of the North America oil and gas lubricants industry. Technological breakthroughs in additive chemistry and base oil formulations are continuously enhancing lubricant performance, extending equipment life, and improving energy efficiency. Strategic partnerships between lubricant manufacturers and equipment OEMs (Original Equipment Manufacturers) are crucial for co-developing lubricants that are perfectly optimized for specific machinery, thereby increasing adoption rates. Market expansion strategies, including entry into underserved geographic regions within North America and the development of comprehensive service packages (e.g., oil analysis, condition monitoring), are also acting as significant growth accelerators. The ongoing investment in advanced extraction technologies and the sustained need for reliable operations in both conventional and unconventional oil and gas production will continue to fuel this growth.

Key Players Shaping the North America Oil and Gas Lubricants Industry Market

- BP PLC

- Chevron Corporation

- Eni S p A

- Exxon Mobil Corporation

- Lubrication Engineers Inc

- LUKOIL

- Petro-Canada Lubricants Inc

- Shell PLC

- Schlumberger Limited

- SKF

- TotalEnergies SE

- Valvoline Inc

Notable Milestones in North America Oil and Gas Lubricants Industry Sector

- December 2022: Shell acquired Allied Reliability, significantly expanding its North American lubricants business. This move aligns with Shell's global strategy to enhance its premium product offerings and industrial sector presence, integrating complementary services to create a stronger value proposition for customers.

- August 2022: Valvoline Inc. announced the sale of its global products business, including its lubricants segment, to Saudi Aramco for USD 2.65 billion in cash. This strategic divestiture allowed Valvoline to increase its focus on its rapidly growing retail services unit.

In-Depth North America Oil and Gas Lubricants Industry Market Outlook

The future market outlook for the North America oil and gas lubricants industry is exceptionally promising, underpinned by persistent global energy demand and ongoing technological evolution. Growth accelerators, including the continuous innovation in high-performance synthetic lubricants and the increasing demand for environmentally responsible formulations, will shape market dynamics. Strategic partnerships between lubricant producers and oilfield service companies are expected to deepen, fostering the development of integrated solutions that enhance operational efficiency and asset protection. The expansion into emerging applications, such as lubricants for carbon capture technologies and the evolving needs of the renewable energy sector integrated with traditional oil and gas operations, presents significant strategic opportunities. Continued investment in infrastructure and exploration activities across the United States, Canada, and Mexico will ensure sustained demand, making this a dynamic and lucrative market for stakeholders.

North America Oil and Gas Lubricants Industry Segmentation

-

1. Location

- 1.1. Onshore

- 1.2. Offshore

-

2. Product Type

- 2.1. Grease

- 2.2. Coolant/Anti-freezer

- 2.3. Engine Oils

- 2.4. Hydraulic Fluids

- 2.5. Other Product Types

-

3. Sector

- 3.1. Upstream

- 3.2. Midstream

- 3.3. Downstream

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Mexico

North America Oil and Gas Lubricants Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Oil and Gas Lubricants Industry Regional Market Share

Geographic Coverage of North America Oil and Gas Lubricants Industry

North America Oil and Gas Lubricants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Location

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Grease

- 5.2.2. Coolant/Anti-freezer

- 5.2.3. Engine Oils

- 5.2.4. Hydraulic Fluids

- 5.2.5. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Sector

- 5.3.1. Upstream

- 5.3.2. Midstream

- 5.3.3. Downstream

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Location

- 6. Global North America Oil and Gas Lubricants Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Location

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Grease

- 6.2.2. Coolant/Anti-freezer

- 6.2.3. Engine Oils

- 6.2.4. Hydraulic Fluids

- 6.2.5. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by Sector

- 6.3.1. Upstream

- 6.3.2. Midstream

- 6.3.3. Downstream

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Location

- 7. United States North America Oil and Gas Lubricants Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Location

- 7.1.1. Onshore

- 7.1.2. Offshore

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Grease

- 7.2.2. Coolant/Anti-freezer

- 7.2.3. Engine Oils

- 7.2.4. Hydraulic Fluids

- 7.2.5. Other Product Types

- 7.3. Market Analysis, Insights and Forecast - by Sector

- 7.3.1. Upstream

- 7.3.2. Midstream

- 7.3.3. Downstream

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Location

- 8. Canada North America Oil and Gas Lubricants Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Location

- 8.1.1. Onshore

- 8.1.2. Offshore

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Grease

- 8.2.2. Coolant/Anti-freezer

- 8.2.3. Engine Oils

- 8.2.4. Hydraulic Fluids

- 8.2.5. Other Product Types

- 8.3. Market Analysis, Insights and Forecast - by Sector

- 8.3.1. Upstream

- 8.3.2. Midstream

- 8.3.3. Downstream

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Location

- 9. Mexico North America Oil and Gas Lubricants Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Location

- 9.1.1. Onshore

- 9.1.2. Offshore

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Grease

- 9.2.2. Coolant/Anti-freezer

- 9.2.3. Engine Oils

- 9.2.4. Hydraulic Fluids

- 9.2.5. Other Product Types

- 9.3. Market Analysis, Insights and Forecast - by Sector

- 9.3.1. Upstream

- 9.3.2. Midstream

- 9.3.3. Downstream

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. United States

- 9.4.2. Canada

- 9.4.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Location

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 BP PLC

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Chevron Corporation

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Eni S p A

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Exxon Mobil Corporation

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Lubrication Engineers Inc

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 LUKOIL

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Petro-Canada Lubricants Inc

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Shell PLC

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Schlumberger Limited

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 SKF

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 TotalEnergies SE

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Valvoline Inc *List Not Exhaustive

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.1 BP PLC

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global North America Oil and Gas Lubricants Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: United States North America Oil and Gas Lubricants Industry Revenue (million), by Location 2025 & 2033

- Figure 3: United States North America Oil and Gas Lubricants Industry Revenue Share (%), by Location 2025 & 2033

- Figure 4: United States North America Oil and Gas Lubricants Industry Revenue (million), by Product Type 2025 & 2033

- Figure 5: United States North America Oil and Gas Lubricants Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: United States North America Oil and Gas Lubricants Industry Revenue (million), by Sector 2025 & 2033

- Figure 7: United States North America Oil and Gas Lubricants Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 8: United States North America Oil and Gas Lubricants Industry Revenue (million), by Geography 2025 & 2033

- Figure 9: United States North America Oil and Gas Lubricants Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 10: United States North America Oil and Gas Lubricants Industry Revenue (million), by Country 2025 & 2033

- Figure 11: United States North America Oil and Gas Lubricants Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Canada North America Oil and Gas Lubricants Industry Revenue (million), by Location 2025 & 2033

- Figure 13: Canada North America Oil and Gas Lubricants Industry Revenue Share (%), by Location 2025 & 2033

- Figure 14: Canada North America Oil and Gas Lubricants Industry Revenue (million), by Product Type 2025 & 2033

- Figure 15: Canada North America Oil and Gas Lubricants Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Canada North America Oil and Gas Lubricants Industry Revenue (million), by Sector 2025 & 2033

- Figure 17: Canada North America Oil and Gas Lubricants Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 18: Canada North America Oil and Gas Lubricants Industry Revenue (million), by Geography 2025 & 2033

- Figure 19: Canada North America Oil and Gas Lubricants Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 20: Canada North America Oil and Gas Lubricants Industry Revenue (million), by Country 2025 & 2033

- Figure 21: Canada North America Oil and Gas Lubricants Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Mexico North America Oil and Gas Lubricants Industry Revenue (million), by Location 2025 & 2033

- Figure 23: Mexico North America Oil and Gas Lubricants Industry Revenue Share (%), by Location 2025 & 2033

- Figure 24: Mexico North America Oil and Gas Lubricants Industry Revenue (million), by Product Type 2025 & 2033

- Figure 25: Mexico North America Oil and Gas Lubricants Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 26: Mexico North America Oil and Gas Lubricants Industry Revenue (million), by Sector 2025 & 2033

- Figure 27: Mexico North America Oil and Gas Lubricants Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 28: Mexico North America Oil and Gas Lubricants Industry Revenue (million), by Geography 2025 & 2033

- Figure 29: Mexico North America Oil and Gas Lubricants Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 30: Mexico North America Oil and Gas Lubricants Industry Revenue (million), by Country 2025 & 2033

- Figure 31: Mexico North America Oil and Gas Lubricants Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Location 2020 & 2033

- Table 2: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 3: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Sector 2020 & 2033

- Table 4: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 5: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Location 2020 & 2033

- Table 7: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 8: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Sector 2020 & 2033

- Table 9: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 10: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Country 2020 & 2033

- Table 11: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Location 2020 & 2033

- Table 12: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 13: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Sector 2020 & 2033

- Table 14: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 15: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Location 2020 & 2033

- Table 17: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 18: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Sector 2020 & 2033

- Table 19: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 20: Global North America Oil and Gas Lubricants Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Oil and Gas Lubricants Industry?

The projected CAGR is approximately 3.7%.

2. Which companies are prominent players in the North America Oil and Gas Lubricants Industry?

Key companies in the market include BP PLC, Chevron Corporation, Eni S p A, Exxon Mobil Corporation, Lubrication Engineers Inc, LUKOIL, Petro-Canada Lubricants Inc, Shell PLC, Schlumberger Limited, SKF, TotalEnergies SE, Valvoline Inc *List Not Exhaustive.

3. What are the main segments of the North America Oil and Gas Lubricants Industry?

The market segments include Location, Product Type, Sector, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 186.1 million as of 2022.

5. What are some drivers contributing to market growth?

Growing Interest towards Unconventional Reserves; Technological Advancement Leading to Higher Well Production Rates.

6. What are the notable trends driving market growth?

Offshore Exploration is Expected to Experience the Highest Growth.

7. Are there any restraints impacting market growth?

Growing Interest towards Unconventional Reserves; Technological Advancement Leading to Higher Well Production Rates.

8. Can you provide examples of recent developments in the market?

In December 2022, Shell acquired Allied Reliability, expanding its North American lubricants business. This is in line with its global lubricants strategy of expanding its premium product offering and presence in the industrial sector and providing complementary services to provide a strong value proposition to its customers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Oil and Gas Lubricants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Oil and Gas Lubricants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Oil and Gas Lubricants Industry?

To stay informed about further developments, trends, and reports in the North America Oil and Gas Lubricants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence