Key Insights

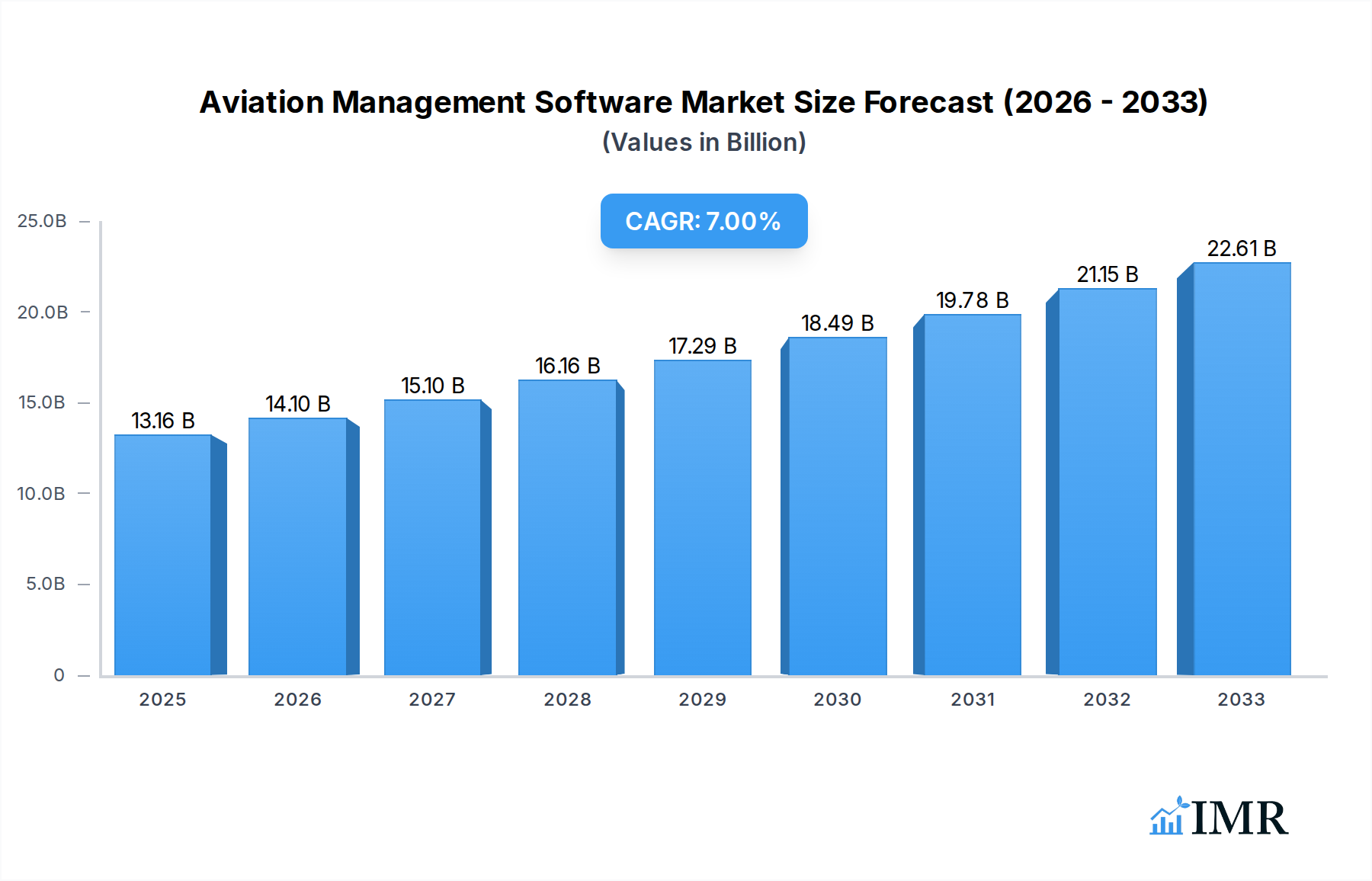

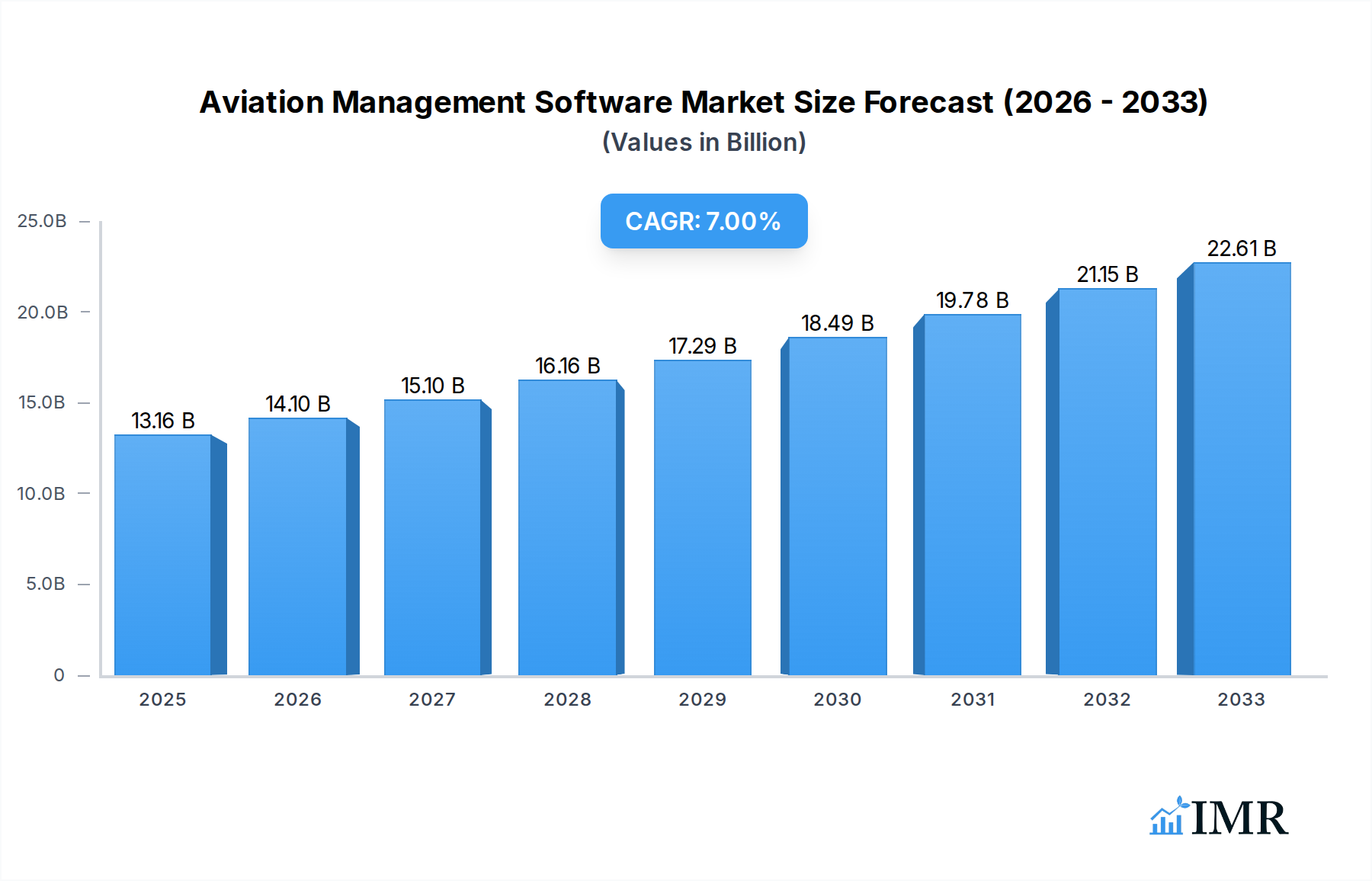

The global Aviation Management Software market is poised for substantial growth, estimated to reach USD 13.16 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of 7.1% through 2033. This expansion is fueled by an increasing need for operational efficiency, enhanced passenger experience, and stringent regulatory compliance across the aviation sector. Key drivers include the growing complexity of air traffic management, the demand for real-time data analytics to optimize flight operations, and the critical importance of robust passenger and baggage tracking systems. The market is segmented by application into Aeronautics, Airports, and Others, with Airports representing a significant area of adoption due to their reliance on integrated management solutions. Furthermore, the software types encompass Passenger Management, Luggage Management, Data Management, and Others, each addressing distinct operational challenges. The continuous digital transformation within the aviation industry is compelling airlines and airports to invest in advanced software solutions for better resource allocation, improved safety, and streamlined workflows, thereby driving market demand.

Aviation Management Software Market Size (In Billion)

The market's growth trajectory is further supported by emerging trends such as the integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance and personalized passenger services, the adoption of cloud-based solutions for scalability and accessibility, and the increasing focus on cybersecurity to protect sensitive aviation data. However, certain restraints, such as the high initial investment costs for sophisticated software systems and the complexity of integrating new technologies with legacy infrastructure, may temper the pace of adoption in some segments. Despite these challenges, the relentless pursuit of operational excellence and the ever-present need to enhance passenger satisfaction and security will continue to propel the Aviation Management Software market forward. Geographically, North America and Europe currently lead in market adoption, driven by well-established aviation infrastructure and significant investment in technology. The Asia Pacific region, with its rapidly expanding air travel market, is anticipated to exhibit the highest growth potential in the coming years.

Aviation Management Software Company Market Share

Unlocking the Skies: Comprehensive Report on the Global Aviation Management Software Market

Unlock unparalleled insights into the dynamic Aviation Management Software market with this in-depth report. Covering the period from 2019–2033, with a base year of 2025, this research provides a granular analysis of market structure, growth trends, regional dominance, product landscape, key drivers, emerging opportunities, and future outlook. Discover how advancements in passenger management, luggage management, data management, and other critical applications are reshaping the aviation industry, from aeronautics to airports. This report is an essential resource for stakeholders seeking to navigate the complexities of this rapidly evolving sector, understand competitive landscapes, and capitalize on future growth.

Aviation Management Software Market Dynamics & Structure

The global Aviation Management Software market is characterized by a moderate to high level of concentration, driven by a confluence of technological innovation and increasing regulatory demands. Key drivers include the perpetual pursuit of operational efficiency, enhanced passenger experience, and stringent safety protocols within the aviation ecosystem. The market benefits from significant technological advancements in areas such as AI-powered analytics, cloud computing, and IoT integration, which are enabling more sophisticated software solutions. Regulatory frameworks, including those for air traffic control, passenger data privacy (like GDPR and its global equivalents), and security, also play a crucial role in shaping software development and adoption. Competitive product substitutes are evolving, with integrated platforms offering a broader suite of functionalities gaining traction over standalone solutions. End-user demographics are increasingly diverse, encompassing major airlines, regional carriers, airports of all sizes, air traffic control organizations, and MRO (Maintenance, Repair, and Overhaul) providers. Mergers and acquisitions (M&A) activity, while not constant, is a recurring theme, indicating a consolidation drive as larger players acquire innovative technologies or expand their market reach. For instance, the past few years have seen strategic acquisitions aimed at bolstering capabilities in areas like route optimization and predictive maintenance. The estimated market value for the Aviation Management Software market stands at $18.2 billion in 2025, with the parent market valued at $250 billion and the child market (specific niche software within aviation management) at $12.5 billion.

- Market Concentration: Moderate to High, with a few key players holding significant market share.

- Technological Innovation Drivers: AI/ML for predictive analytics, cloud-based solutions, IoT integration for real-time data, blockchain for enhanced security.

- Regulatory Frameworks: ICAO regulations, national aviation authorities' mandates, data privacy laws, passenger rights legislation.

- Competitive Product Substitutes: Shift towards integrated aviation management suites, increasing competition from specialized solution providers.

- End-User Demographics: Airlines (commercial, cargo, charter), Airports (full-service, regional), Air Navigation Service Providers (ANSPs), MRO companies, regulatory bodies.

- M&A Trends: Strategic acquisitions to gain market share, acquire innovative technologies, and expand service offerings. Deal volumes in the last three years are estimated at 25 major transactions, with an average deal value of $150 million.

Aviation Management Software Growth Trends & Insights

The Aviation Management Software market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 8.5% from 2025 to 2033. This robust expansion is fueled by a sustained increase in air travel demand and the critical need for airlines and airports to optimize operations, enhance passenger satisfaction, and ensure unparalleled safety and security. The market size is expected to reach $35.6 billion by 2033, up from an estimated $18.2 billion in 2025. Adoption rates for advanced aviation management solutions are accelerating, driven by the tangible benefits they offer, including reduced operational costs, improved resource allocation, and streamlined passenger journeys. Technological disruptions are a constant theme, with the integration of Artificial Intelligence (AI) and Machine Learning (ML) transforming everything from flight scheduling and predictive maintenance to passenger flow management and personalized customer service. The widespread adoption of cloud-based platforms is further democratizing access to sophisticated tools, enabling even smaller operators to leverage powerful analytics and management capabilities. Consumer behavior shifts are also playing a pivotal role; passengers increasingly expect seamless digital experiences, from booking and check-in to baggage tracking and in-flight services. This demand for enhanced customer engagement is pushing aviation stakeholders to invest in software that can deliver personalized interactions and real-time information. The parent market is projected to grow to $380 billion by 2033, with the child market reaching $22.1 billion.

- Market Size Evolution: Significant projected growth from $18.2 billion in 2025 to $35.6 billion by 2033.

- Adoption Rates: Steadily increasing across all segments, driven by cost-efficiency and passenger experience imperatives.

- Technological Disruptions: AI/ML for predictive maintenance and personalized passenger services, blockchain for enhanced security and transparency, advanced data analytics for operational optimization.

- Consumer Behavior Shifts: Demand for seamless digital experiences, real-time information, and personalized services.

- CAGR (2025-2033): Estimated at 8.5%.

- Market Penetration: Increasing across airlines, airports, and ANSPs, with a growing emphasis on integrated solutions.

Dominant Regions, Countries, or Segments in Aviation Management Software

The Airports segment, within the Application category, is emerging as a dominant force driving growth in the global Aviation Management Software market. This dominance is attributed to the complex operational demands faced by modern airports, which serve as critical nodes in the global aviation network. Airports are investing heavily in advanced software solutions to manage passenger flow, optimize gate assignments, streamline baggage handling, enhance security screening, and improve overall operational efficiency. The increasing number of smart airport initiatives worldwide further amplifies this trend. North America and Europe currently lead in terms of market share due to established aviation infrastructure, significant investment in technology, and a strong regulatory environment that mandates advanced management systems. However, the Asia-Pacific region is exhibiting the highest growth potential, propelled by rapid expansion in air travel, the development of new mega-airports, and government initiatives to modernize aviation infrastructure.

Within the Types segment, Data Management Software is experiencing robust demand, as airports and airlines increasingly recognize the strategic value of their operational and passenger data. This includes software for flight data management, operational control, revenue management, and customer relationship management. The ability to collect, analyze, and act upon vast amounts of data is crucial for optimizing operations and improving passenger experience.

- Dominant Application Segment: Airports, driven by the need for integrated operational management and passenger facilitation.

- Key Drivers: Smart airport initiatives, increasing passenger traffic, demand for real-time operational visibility, security enhancements.

- Market Share: Airports segment accounts for an estimated 45% of the total Aviation Management Software market in 2025.

- Growth Potential: High, particularly in emerging economies with expanding airport infrastructure.

- Leading Region: North America and Europe (current market share leaders), with Asia-Pacific showing the fastest growth trajectory.

- Dominance Factors: Advanced technological adoption, strong regulatory frameworks, significant investment capacity.

- Key Type Segment: Data Management Software, crucial for operational optimization and informed decision-making.

- Market Share: Data Management Software holds approximately 30% of the market share within the Types segment.

- Growth Potential: Driven by the increasing volume and complexity of aviation data.

- Underlying Drivers: Economic policies supporting aviation growth, infrastructure development, and the constant pursuit of operational excellence and passenger satisfaction.

Aviation Management Software Product Landscape

The Aviation Management Software product landscape is characterized by a strong emphasis on integrated solutions that streamline complex aviation operations. Innovations are focused on enhancing real-time data processing, predictive analytics, and user-friendly interfaces. Passenger Management Software is evolving to offer personalized experiences, from self-service check-in kiosks and mobile boarding passes to AI-powered virtual assistants and dynamic rebooking capabilities. Luggage Management Software is leveraging technologies like RFID and advanced tracking systems to reduce lost or delayed baggage, significantly improving customer satisfaction. Data Management Software is at the core of these advancements, providing robust platforms for collecting, analyzing, and visualizing operational data, enabling better decision-making in areas like flight planning, resource allocation, and maintenance scheduling. Unique selling propositions often revolve around modularity, scalability, interoperability with existing systems, and adherence to stringent aviation security and data privacy standards. Technological advancements are continuously pushing the boundaries, with solutions incorporating AI for demand forecasting, real-time operational adjustments, and personalized passenger engagement. The market is projected to reach $35.6 billion by 2033.

Key Drivers, Barriers & Challenges in Aviation Management Software

The Aviation Management Software market is propelled by several key drivers. Technological advancements, particularly in AI, ML, and cloud computing, are enabling more sophisticated and efficient software solutions. The ever-increasing demand for air travel necessitates enhanced operational efficiency and passenger experience, driving investment in management software. Furthermore, stringent regulatory requirements for safety, security, and data privacy mandate the adoption of compliant software.

- Key Drivers:

- Technological Innovation: AI/ML for predictive maintenance, route optimization, and passenger analytics.

- Growing Air Travel Demand: Increased passenger and cargo volumes require efficient management.

- Regulatory Compliance: Mandates for safety, security, and data protection.

- Operational Efficiency: Drive to reduce costs and improve resource utilization.

However, the market also faces significant barriers and challenges. High implementation costs and the complexity of integrating new software with legacy systems can be deterrents. The specialized nature of aviation software requires skilled personnel for development and maintenance, leading to talent shortages. Security concerns and the need for robust data protection in a highly sensitive industry are constant challenges.

- Key Barriers & Challenges:

- High Implementation Costs: Significant upfront investment for software and integration.

- Legacy System Integration: Difficulty in seamlessly integrating new solutions with existing infrastructure.

- Talent Shortage: Demand for specialized aviation IT professionals exceeds supply.

- Data Security & Privacy Concerns: Protecting sensitive passenger and operational data from cyber threats.

- Regulatory Hurdles: Evolving and complex regulations requiring continuous software adaptation.

- Supply Chain Disruptions: While less direct for software, impact on hardware availability can indirectly affect deployment.

Emerging Opportunities in Aviation Management Software

Emerging opportunities in the Aviation Management Software market are largely centered around the increasing adoption of AI and IoT across the aviation value chain. The development of hyper-personalized passenger experiences, driven by advanced data analytics and AI, presents a significant avenue for growth. Predictive maintenance solutions, leveraging IoT sensors and ML algorithms, offer airlines the opportunity to drastically reduce downtime and maintenance costs. Furthermore, the burgeoning demand for sustainable aviation practices is creating opportunities for software that can optimize fuel efficiency and reduce carbon emissions. The expansion of drone management and Urban Air Mobility (UAM) systems also opens up new frontiers for specialized aviation management software.

- Untapped Markets: Drone fleet management, Urban Air Mobility (UAM) operations, space logistics management.

- Innovative Applications: AI-driven disruption management, biometric passenger processing, proactive cybersecurity solutions for aviation systems.

- Evolving Consumer Preferences: Demand for seamless, digital-first passenger journeys and personalized in-flight experiences.

Growth Accelerators in the Aviation Management Software Industry

Several catalysts are accelerating the growth of the Aviation Management Software industry. Technological breakthroughs, particularly in AI, machine learning, and cloud computing, are continuously enabling more powerful and efficient solutions. Strategic partnerships between software providers and airlines or airports are fostering co-creation and tailored solutions, driving adoption and innovation. Market expansion strategies, including targeting emerging economies with rapidly growing air travel sectors and developing specialized software for niche aviation segments, are also key growth accelerators. The increasing focus on sustainability within the aviation industry is also driving demand for software that can optimize fuel efficiency and reduce environmental impact.

Key Players Shaping the Aviation Management Software Market

- FLIGHTGLOBAL

- GMV

- Harris

- HICO-ICS

- National Instruments

- NAVBLUE

- RESA Airport Data Systems

- ROCKWELL COLLINS

- SITA

- TOPSYSTEM SYSTEMHAUS

- InterSystems

- ISO Software Systeme

- Isode

- J2 Aircraft Dynamics

- Levarti

- LPT-it

- LTB400 Aviation Software

- Brock Solutions

- Amadeus IT Group

- ASQ

- IDS INGEGNERIA DEI SISTEMI

- Ikusi

- INDRA

- Casper

- CHAMP Cargosystems

- Cargoflash Infotech

- Damarel Systems International

- DASSAULT SYSTEMES

- ESP Global Services

- Avtura

Notable Milestones in Aviation Management Software Sector

- 2019: Increased adoption of AI for predictive maintenance by major airlines, leading to reduced unscheduled downtime.

- 2020: Expansion of cloud-based passenger management systems to enhance remote check-in and boarding capabilities during the global pandemic.

- 2021: Launch of advanced data analytics platforms by key players, offering deeper insights into operational efficiency and passenger behavior.

- 2022: Strategic acquisitions of smaller, specialized software companies by larger aviation IT providers to broaden their solution portfolios.

- 2023: Growing emphasis on cybersecurity solutions within aviation management software to combat evolving cyber threats.

- 2024: Introduction of integrated systems combining passenger, baggage, and operational management for seamless airport operations.

In-Depth Aviation Management Software Market Outlook

The future outlook for the Aviation Management Software market is exceptionally promising, driven by a continuous wave of technological innovation and the insatiable demand for efficient, safe, and passenger-centric air travel. Growth accelerators such as the pervasive integration of AI for predictive analytics, hyper-personalization of passenger journeys through data-driven insights, and the widespread adoption of IoT devices for real-time operational monitoring will continue to shape the market. Strategic partnerships and collaborative efforts between technology providers, airlines, and airports will foster the development of next-generation solutions, while expansion into emerging markets and niche segments like drone management and UAM will unlock new revenue streams. The overarching trend towards sustainable aviation practices will further stimulate the demand for software that can optimize resource utilization and minimize environmental impact, positioning the Aviation Management Software market for sustained and robust growth.

Aviation Management Software Segmentation

-

1. Application

- 1.1. Aeronautics

- 1.2. Airports

- 1.3. Others

-

2. Types

- 2.1. Passenger Management Software

- 2.2. Luggage Management Software

- 2.3. Data Management Software

- 2.4. Others

Aviation Management Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

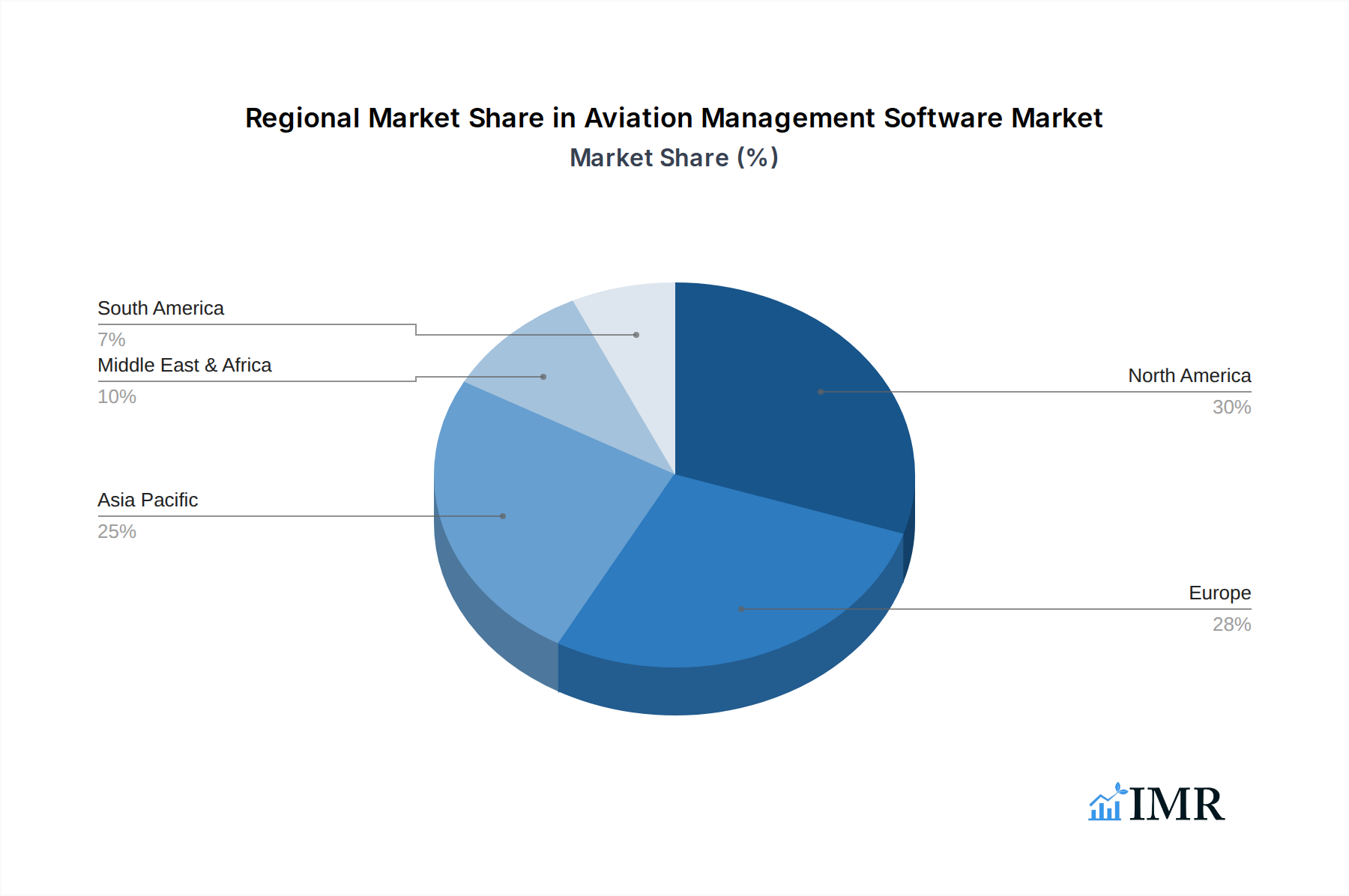

Aviation Management Software Regional Market Share

Geographic Coverage of Aviation Management Software

Aviation Management Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Aviation Management Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aeronautics

- 5.1.2. Airports

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Passenger Management Software

- 5.2.2. Luggage Management Software

- 5.2.3. Data Management Software

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Aviation Management Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aeronautics

- 6.1.2. Airports

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Passenger Management Software

- 6.2.2. Luggage Management Software

- 6.2.3. Data Management Software

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Aviation Management Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aeronautics

- 7.1.2. Airports

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Passenger Management Software

- 7.2.2. Luggage Management Software

- 7.2.3. Data Management Software

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Aviation Management Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aeronautics

- 8.1.2. Airports

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Passenger Management Software

- 8.2.2. Luggage Management Software

- 8.2.3. Data Management Software

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Aviation Management Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aeronautics

- 9.1.2. Airports

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Passenger Management Software

- 9.2.2. Luggage Management Software

- 9.2.3. Data Management Software

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Aviation Management Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aeronautics

- 10.1.2. Airports

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Passenger Management Software

- 10.2.2. Luggage Management Software

- 10.2.3. Data Management Software

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 FLIGHTGLOBAL

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 GMV

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Harris

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 HICO-ICS

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 National Instruments

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 NAVBLUE

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 RESA Airport Data Systems

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ROCKWELL COLLINS

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 SITA

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 TOPSYSTEM SYSTEMHAUS

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 InterSystems

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ISO Software Systeme

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Isode

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 J2 Aircraft Dynamics

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Levarti

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 LPT-it

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 LTB400 Aviation Software

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Brock Solutions

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Amadeus IT Group

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 ASQ

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 IDS INGEGNERIA DEI SISTEMI

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Ikusi

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 INDRA

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Casper

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 CHAMP Cargosystems

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Cargoflash Infotech

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Damarel Systems International

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 DASSAULT SYSTEMES

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 ESP Global Services

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Avtura

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.1 FLIGHTGLOBAL

List of Figures

- Figure 1: Global Aviation Management Software Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Aviation Management Software Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Aviation Management Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aviation Management Software Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Aviation Management Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aviation Management Software Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Aviation Management Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aviation Management Software Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Aviation Management Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aviation Management Software Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Aviation Management Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aviation Management Software Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Aviation Management Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aviation Management Software Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Aviation Management Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aviation Management Software Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Aviation Management Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aviation Management Software Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Aviation Management Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aviation Management Software Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aviation Management Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aviation Management Software Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aviation Management Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aviation Management Software Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aviation Management Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aviation Management Software Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Aviation Management Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aviation Management Software Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Aviation Management Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aviation Management Software Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Aviation Management Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aviation Management Software Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Aviation Management Software Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Aviation Management Software Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Aviation Management Software Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Aviation Management Software Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Aviation Management Software Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Aviation Management Software Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Aviation Management Software Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Aviation Management Software Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Aviation Management Software Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Aviation Management Software Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Aviation Management Software Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Aviation Management Software Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Aviation Management Software Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Aviation Management Software Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Aviation Management Software Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Aviation Management Software Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Aviation Management Software Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aviation Management Software Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aviation Management Software?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the Aviation Management Software?

Key companies in the market include FLIGHTGLOBAL, GMV, Harris, HICO-ICS, National Instruments, NAVBLUE, RESA Airport Data Systems, ROCKWELL COLLINS, SITA, TOPSYSTEM SYSTEMHAUS, InterSystems, ISO Software Systeme, Isode, J2 Aircraft Dynamics, Levarti, LPT-it, LTB400 Aviation Software, Brock Solutions, Amadeus IT Group, ASQ, IDS INGEGNERIA DEI SISTEMI, Ikusi, INDRA, Casper, CHAMP Cargosystems, Cargoflash Infotech, Damarel Systems International, DASSAULT SYSTEMES, ESP Global Services, Avtura.

3. What are the main segments of the Aviation Management Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.16 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aviation Management Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aviation Management Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aviation Management Software?

To stay informed about further developments, trends, and reports in the Aviation Management Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence