Key Insights

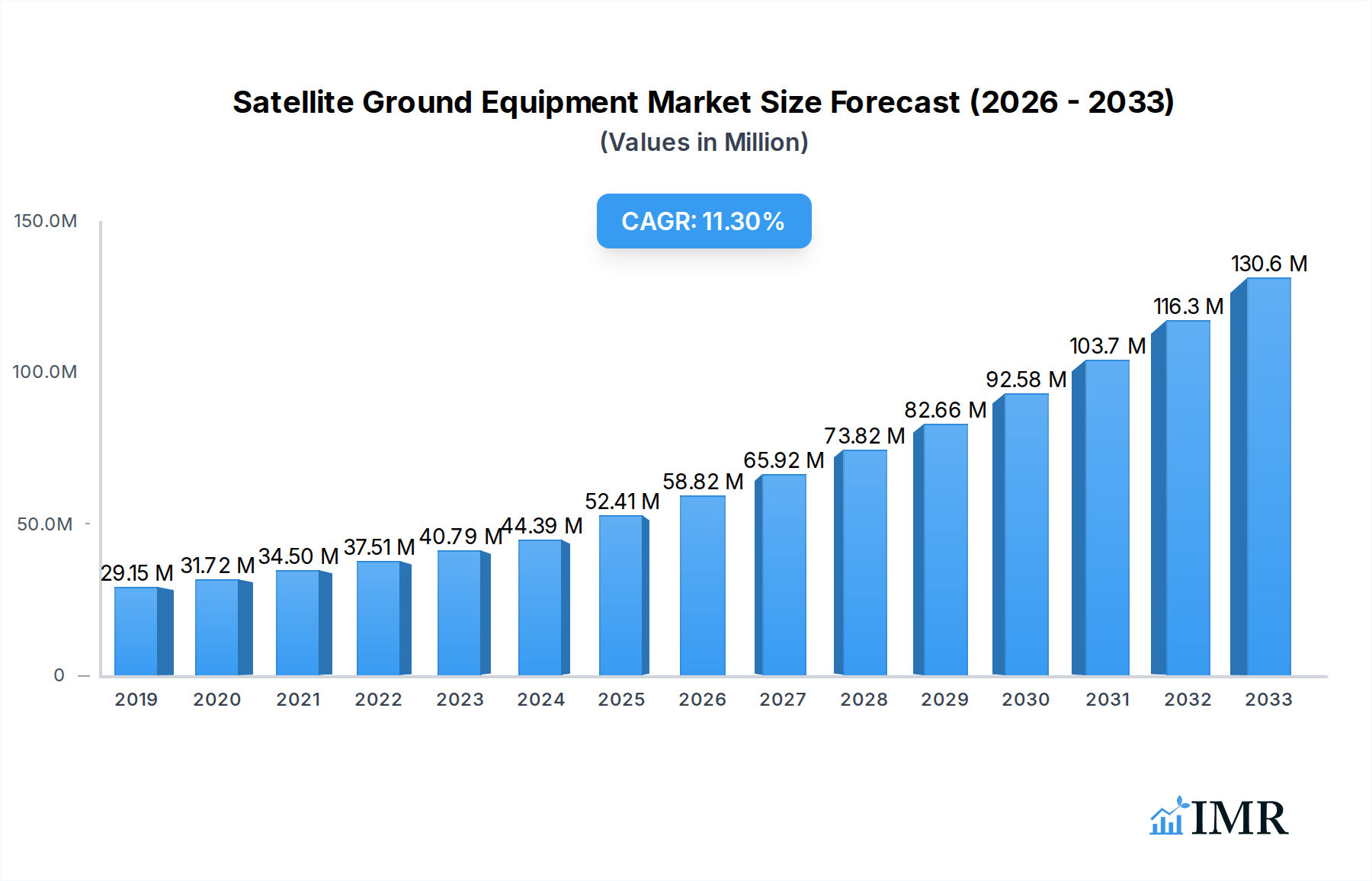

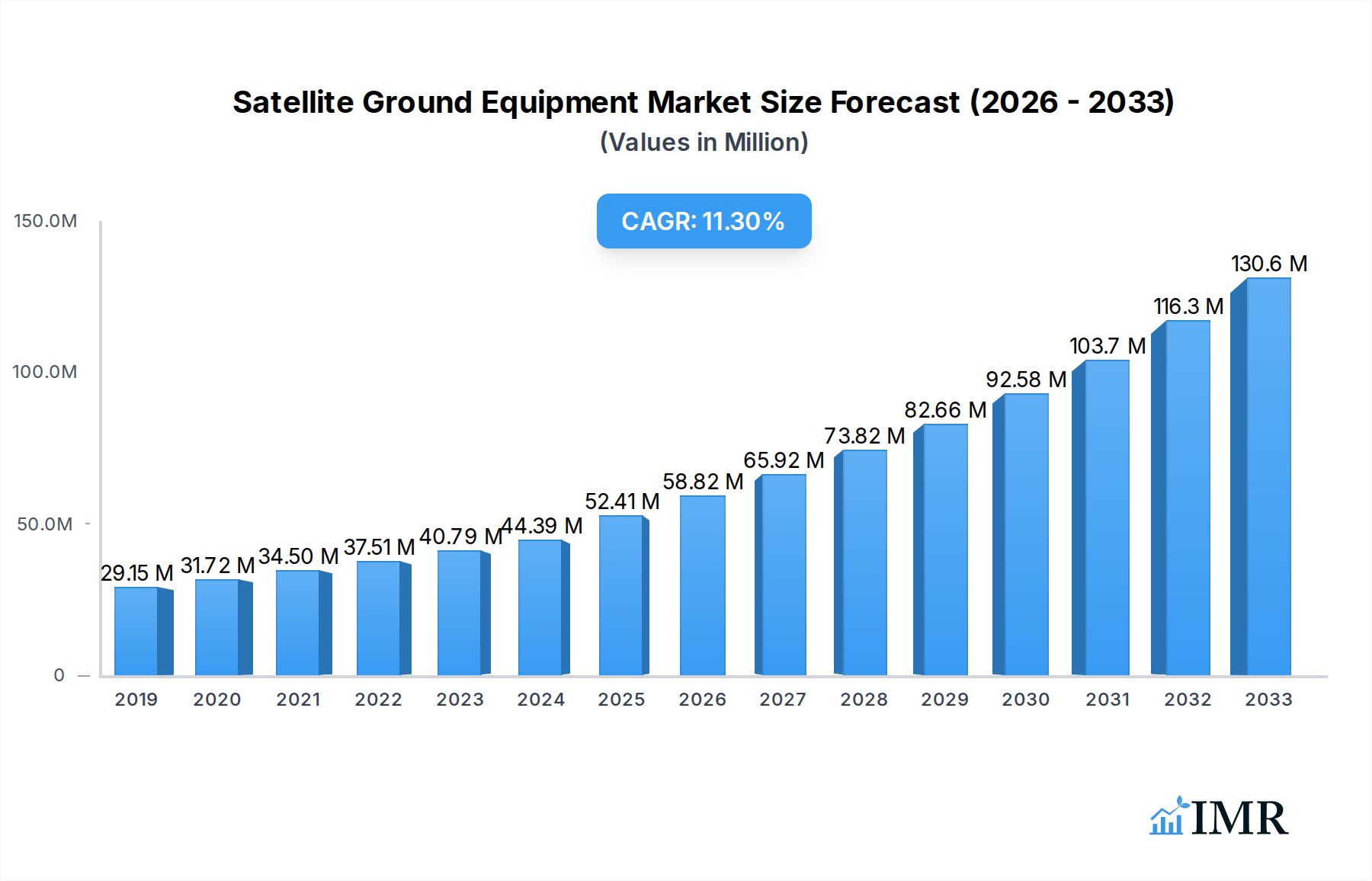

The global Satellite Ground Equipment Market is poised for significant expansion, projected to reach a substantial $52.41 million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 12.12% during the forecast period of 2025-2033. This robust growth is primarily fueled by the escalating demand for enhanced connectivity across various sectors, including maritime, defense and government, enterprises, and the dynamic media and entertainment industries. The increasing reliance on satellite technology for reliable and ubiquitous communication, especially in remote or underserved areas, serves as a major catalyst. Furthermore, advancements in satellite technology, such as the proliferation of Low Earth Orbit (LEO) constellations and the development of more sophisticated and compact ground equipment, are driving innovation and adoption. The defense and government sectors are key beneficiaries, leveraging satellite ground equipment for secure communication, surveillance, and critical mission operations.

Satellite Ground Equipment Market Market Size (In Million)

The market's trajectory is further shaped by a confluence of evolving trends and strategic initiatives. The integration of artificial intelligence (AI) and machine learning (ML) into ground station operations is optimizing network management and data processing, leading to increased efficiency and cost-effectiveness. The growing adoption of Software-Defined Networking (SDN) and Network Function Virtualization (NFV) is enhancing the flexibility and agility of satellite ground infrastructure. While the market demonstrates strong upward momentum, certain restraints warrant consideration. High initial investment costs for advanced ground equipment and the ongoing need for specialized technical expertise can pose challenges for widespread adoption, particularly for smaller enterprises. However, the continuous innovation in user-friendly interfaces and service-based models is expected to mitigate these barriers, ensuring sustained growth and wider accessibility of satellite ground equipment solutions.

Satellite Ground Equipment Market Company Market Share

Comprehensive Satellite Ground Equipment Market Report: Insights, Trends, and Future Outlook (2019–2033)

This in-depth report provides a strategic analysis of the global Satellite Ground Equipment Market, meticulously examining its growth trajectory, competitive landscape, and future potential. Covering the period from 2019 to 2033, with a base year of 2025, this report leverages extensive market intelligence to deliver actionable insights for stakeholders. We delve into parent and child markets, offering a granular understanding of the forces shaping this dynamic sector. The report presents all values in Million units, ensuring clarity and precision.

Satellite Ground Equipment Market Market Dynamics & Structure

The Satellite Ground Equipment Market is characterized by a moderately concentrated structure, with key players investing heavily in technological innovation and strategic acquisitions to secure market share. The proliferation of Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) satellite constellations is a primary driver, necessitating advanced ground station technologies for continuous connectivity and high-speed data transfer. Regulatory frameworks, particularly concerning spectrum allocation and orbital debris, play a crucial role in shaping market entry and operational strategies. Competitive product substitutes, such as terrestrial fiber optic networks and 5G infrastructure, present a challenge, especially in highly developed urban areas. However, the unparalleled reach and resilience of satellite communication ensure sustained demand in remote and underserved regions. End-user demographics are increasingly diverse, spanning defense, maritime, enterprise, and media sectors, each with unique requirements for bandwidth, latency, and reliability. Mergers and acquisitions are on the rise as companies seek to consolidate capabilities and expand their global footprint. For instance, the ongoing integration of new satellite services requires significant investment in ground infrastructure, fostering a climate of M&A activity aimed at acquiring specialized technology and market access.

- Market Concentration: Moderate, with significant investment in R&D and infrastructure by leading entities.

- Technological Innovation Drivers: LEO/MEO constellation deployment, demand for higher data throughput, and advancements in phased-array antennas and software-defined radios.

- Regulatory Frameworks: Spectrum licensing, international agreements on satellite operations, and cybersecurity standards.

- Competitive Product Substitutes: Terrestrial broadband, 5G networks, and optical fiber.

- End-User Demographics: Growing demand from Defense and Government, Maritime, Enterprise, and Media and Entertainment sectors.

- M&A Trends: Consolidation of ground station networks, acquisition of specialized technology providers, and partnerships for service integration.

Satellite Ground Equipment Market Growth Trends & Insights

The Satellite Ground Equipment Market is poised for substantial growth, driven by an escalating demand for global connectivity, robust data transmission capabilities, and the increasing deployment of next-generation satellite constellations. The market size is projected to expand significantly, fueled by a robust CAGR over the forecast period. Adoption rates for advanced ground station equipment, including ultra-high throughput ground stations and sophisticated antenna systems, are accelerating as industries recognize the critical role of satellite communication in their operations. Technological disruptions, such as the development of software-defined satellites and the integration of artificial intelligence in ground segment management, are reshaping the market. These advancements are enabling more efficient spectrum utilization, reduced latency, and enhanced network flexibility. Consumer behavior shifts, particularly the growing reliance on cloud services, the Internet of Things (IoT), and the need for reliable communication in remote areas, are further propelling market expansion. The ongoing evolution of NGSO constellations, offering broader coverage and higher bandwidth, directly translates to increased demand for scalable and adaptable ground infrastructure. Market penetration is expected to deepen across various end-user verticals, with Defense and Government sectors leading due to critical communication needs, followed closely by the burgeoning Maritime and Enterprise segments seeking to enhance their operational efficiency and global reach. The increasing demand for Earth Observation data and its timely dissemination also contributes to the growth of the ground segment infrastructure.

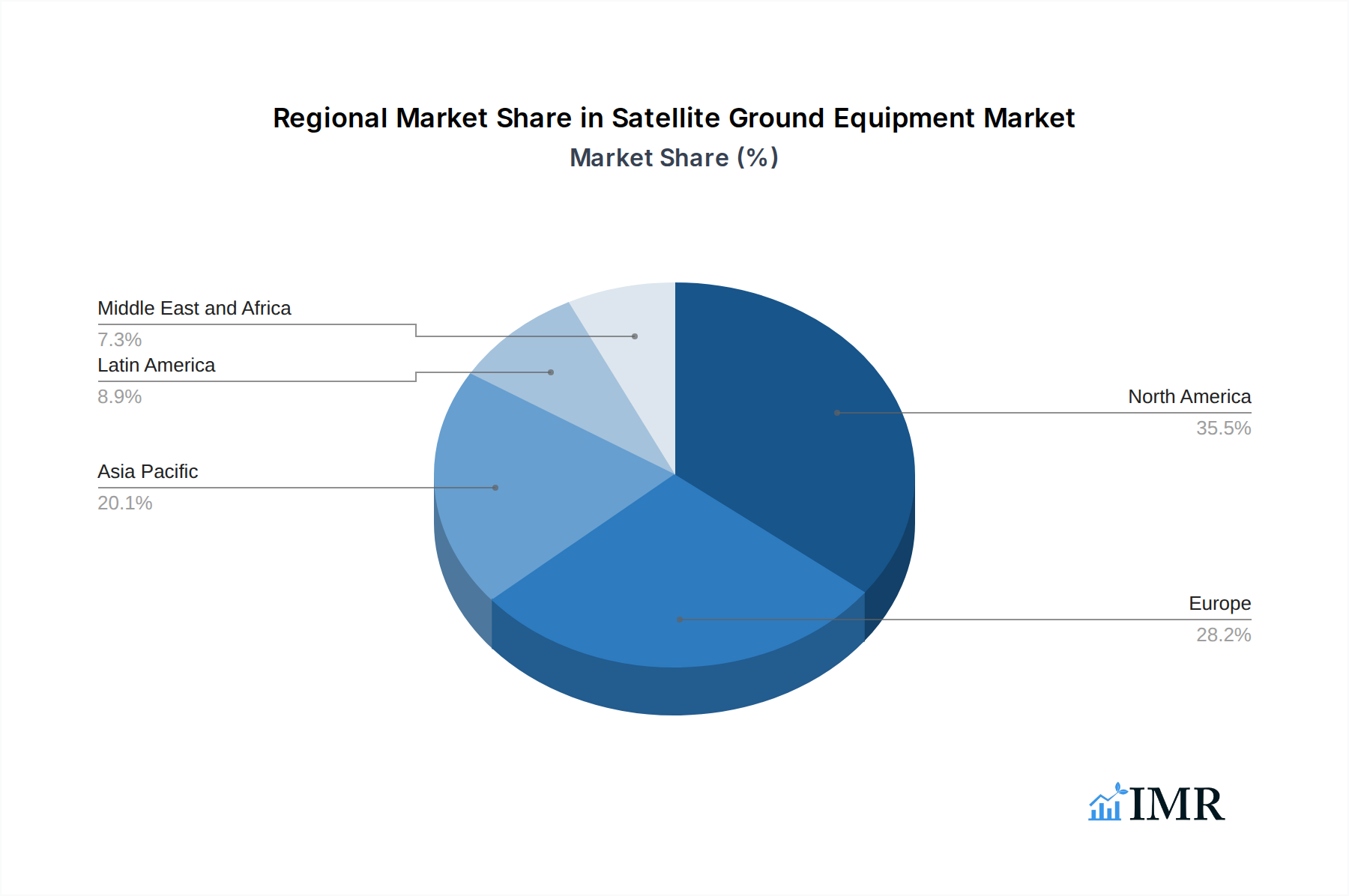

Dominant Regions, Countries, or Segments in Satellite Ground Equipment Market

The Satellite Ground Equipment Market exhibits strong growth drivers across multiple regions and segments. Globally, North America currently stands as a dominant force, primarily due to its advanced technological infrastructure, significant investments in space exploration and defense, and the presence of leading satellite operators and technology providers. The United States, in particular, is a hub for innovation in satellite technology and ground segment development, with substantial government funding and private sector investment fueling market expansion. Key drivers in this region include the robust Defense and Government sector's reliance on secure and resilient satellite communication, the booming enterprise sector adopting satellite solutions for connectivity and IoT applications, and the increasing deployment of LEO constellations for global broadband services.

In terms of segments, the Ground Equipment segment, which encompasses antennas, modems, receivers, transmitters, and associated hardware, is expected to lead market growth. This is a direct consequence of the massive build-out of new satellite constellations and the need for upgraded or new ground stations to communicate with them. The increasing adoption of advanced antenna technologies like phased arrays and electronically steered antennas, capable of tracking multiple satellites simultaneously and offering higher data rates, is a significant factor.

The Defense and Government end-user vertical also represents a dominant segment, driven by the critical need for secure, reliable, and global communication for military operations, intelligence gathering, and disaster management. The ongoing geopolitical landscape further accentuates the demand for resilient satellite-based communication solutions.

Key drivers within these dominant regions and segments include:

- Technological Advancements: Continuous innovation in antenna technology, signal processing, and modulation schemes.

- Government Initiatives: Strategic investments in national space programs and defense communications.

- Increased Satellite Constellation Deployments: Proliferation of LEO, MEO, and GEO constellations requiring extensive ground infrastructure.

- Demand for High-Throughput Data: Growing needs for broadband internet, Earth observation data, and IoT connectivity.

- Infrastructure Development: Expansion and modernization of ground station networks to support new satellite services.

The market share for Ground Equipment is projected to be substantial, with its growth intrinsically linked to the deployment phases of new satellite constellations. Similarly, the Defense and Government segment commands a significant portion of the market due to the high value and critical nature of satellite communication for national security and public services.

Satellite Ground Equipment Market Product Landscape

The product landscape of the Satellite Ground Equipment Market is characterized by rapid innovation focused on enhancing performance, efficiency, and flexibility. Leading product developments include high-throughput ground antennas, such as electronically steered phased array antennas, capable of seamless tracking of multiple satellites and supporting extremely high data rates, often exceeding 100 Gbps. Advanced modems and satellite terminals are being developed with sophisticated modulation and coding schemes to maximize spectral efficiency and minimize latency, crucial for real-time applications. Software-defined ground equipment is gaining traction, allowing for greater adaptability and on-the-fly reconfiguration to support evolving satellite constellations and service requirements. Furthermore, solutions for small satellite ground stations and portable terminals are emerging, catering to niche applications and rapid deployment scenarios. The performance metrics focus on increasing data throughput, reducing latency, improving signal-to-noise ratio (SNR), and enhancing power efficiency.

Key Drivers, Barriers & Challenges in Satellite Ground Equipment Market

Key Drivers:

The Satellite Ground Equipment Market is propelled by several significant forces. The escalating demand for global broadband connectivity, particularly in underserved regions, is a primary driver. The exponential growth of the Internet of Things (IoT) necessitates ubiquitous and reliable communication, which satellites are uniquely positioned to provide. The ongoing deployment of large LEO and MEO satellite constellations is a monumental catalyst, requiring extensive ground infrastructure for tracking, data reception, and network management. Furthermore, the defense and government sectors' continuous need for secure, resilient, and long-range communication solutions ensures sustained demand for advanced satellite ground equipment. Technological advancements, such as the development of phased-array antennas and software-defined radios, are enabling higher data rates and greater flexibility, making satellite communication more competitive.

Key Barriers & Challenges:

Despite robust growth, the market faces several barriers and challenges. The high initial capital investment required for establishing and upgrading ground station infrastructure can be a significant hurdle, particularly for smaller operators. Regulatory complexities related to spectrum licensing and international coordination for satellite operations can create delays and increase operational costs. The intense competition from rapidly advancing terrestrial communication technologies, such as 5G and fiber optics, poses a threat, especially in densely populated areas where terrestrial solutions offer lower latency and potentially lower costs. Supply chain disruptions and the reliance on specialized components can also impact production timelines and costs. Finally, the cybersecurity landscape presents a constant challenge, requiring continuous investment in robust security measures to protect sensitive data transmitted and managed through ground equipment. The global market size for satellite ground equipment, while growing, faces competition from well-established terrestrial alternatives, impacting market penetration in certain developed regions.

Emerging Opportunities in Satellite Ground Equipment Market

Emerging opportunities within the Satellite Ground Equipment Market are abundant and diverse. The burgeoning demand for Earth Observation (EO) data, driven by climate monitoring, precision agriculture, and urban planning, is creating a need for more efficient ground stations capable of handling large data volumes. The expansion of satellite-based IoT services, for applications ranging from asset tracking in remote logistics to environmental sensing, presents a significant growth avenue. The development of integrated terrestrial and non-terrestrial networks (INTs) offers opportunities for ground equipment that can seamlessly manage hybrid communication environments. Furthermore, the increasing use of satellites for backhaul services, connecting remote cellular towers or underserved areas, is a rapidly growing segment. The rise of small satellite constellations and the associated need for distributed ground station networks, potentially leveraging cloud-based infrastructure, also represent a promising frontier.

Growth Accelerators in the Satellite Ground Equipment Market Industry

Several factors are acting as significant growth accelerators for the Satellite Ground Equipment Market. The relentless innovation in satellite technology, particularly the move towards higher frequency bands and more sophisticated antenna designs, directly stimulates the demand for advanced ground segment solutions. Strategic partnerships between satellite operators, ground station providers, and end-users are crucial for developing tailored solutions and expanding market reach. The increasing adoption of cloud-native architectures and virtualization in ground segment operations is enhancing scalability and reducing operational costs, thereby accelerating market adoption. Furthermore, government initiatives focused on promoting space-based connectivity and national security through satellite communications are providing substantial impetus. The growing trend of miniaturization and cost reduction in satellite components is also democratizing access to space, leading to a broader base of potential ground equipment customers.

Key Players Shaping the Satellite Ground Equipment Market Market

- ST Engineering iDirect

- L3Harris Technologies Inc

- Iridium Communications Inc

- Inmarsat Global Limited

- Thales Group

- KVH Industries Inc

- Thuraya Telecommunications Company

- Orbcomm Inc

- Cobham SATCOM (Cobham Limited)

- Gilat Satellite Networks Ltd

- Advantech Wireless Technologies Inc (Baylin Technologies)

- ViaSat Inc

Notable Milestones in Satellite Ground Equipment Market Sector

- February 2023: CobhamSatcom and RBC Signals, a global satellite data communication solutions provider, announced an extended agreement to deploy CobhamSatcom's adaptable Tracker 6000 and 3700 series ground stations worldwide. The collaborative partnership between the two parties would dramatically expand RBC Signals' vast owned and partner ground network, providing integrated communication services to NGSO missions and constellations for Earth Observation, IoT, and Space Situational Awareness.

- February 2023: China Aerospace Science and Technology Corporation (CASC) announced the successful launch of the Zhongxing-26 communications satellite. Based on the DFH-4E satellite bus, the satellite is China's first, providing a speed of more than 100 gigabits per second (Gbps).

In-Depth Satellite Ground Equipment Market Market Outlook

The outlook for the Satellite Ground Equipment Market is exceptionally positive, driven by a confluence of technological advancements, increasing global connectivity demands, and strategic market expansion. Growth accelerators, including the relentless pursuit of higher data throughput by satellite constellations and the expanding applications of satellite technology across diverse sectors, are setting a strong trajectory. The market is set to witness continued innovation in ground station hardware and software, focusing on enhanced efficiency, lower latency, and seamless integration with terrestrial networks. Strategic partnerships and ongoing mergers and acquisitions will further consolidate the market, fostering a dynamic competitive landscape. The future holds immense potential for the Satellite Ground Equipment Market to play an indispensable role in connecting the world, facilitating critical services, and enabling the next wave of space-based innovation.

Satellite Ground Equipment Market Segmentation

-

1. Type

- 1.1. Ground Equipment

- 1.2. Service

-

2. End-user Vertical

- 2.1. Maritime

- 2.2. Defense and Government

- 2.3. Enterprises

- 2.4. Media and Entertainment

- 2.5. Other End-user Verticals

Satellite Ground Equipment Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Satellite Ground Equipment Market Regional Market Share

Geographic Coverage of Satellite Ground Equipment Market

Satellite Ground Equipment Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.12% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Ground Equipment

- 5.1.2. Service

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Maritime

- 5.2.2. Defense and Government

- 5.2.3. Enterprises

- 5.2.4. Media and Entertainment

- 5.2.5. Other End-user Verticals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Satellite Ground Equipment Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Ground Equipment

- 6.1.2. Service

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. Maritime

- 6.2.2. Defense and Government

- 6.2.3. Enterprises

- 6.2.4. Media and Entertainment

- 6.2.5. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Satellite Ground Equipment Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Ground Equipment

- 7.1.2. Service

- 7.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.2.1. Maritime

- 7.2.2. Defense and Government

- 7.2.3. Enterprises

- 7.2.4. Media and Entertainment

- 7.2.5. Other End-user Verticals

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Satellite Ground Equipment Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Ground Equipment

- 8.1.2. Service

- 8.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.2.1. Maritime

- 8.2.2. Defense and Government

- 8.2.3. Enterprises

- 8.2.4. Media and Entertainment

- 8.2.5. Other End-user Verticals

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Satellite Ground Equipment Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Ground Equipment

- 9.1.2. Service

- 9.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.2.1. Maritime

- 9.2.2. Defense and Government

- 9.2.3. Enterprises

- 9.2.4. Media and Entertainment

- 9.2.5. Other End-user Verticals

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Satellite Ground Equipment Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Ground Equipment

- 10.1.2. Service

- 10.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.2.1. Maritime

- 10.2.2. Defense and Government

- 10.2.3. Enterprises

- 10.2.4. Media and Entertainment

- 10.2.5. Other End-user Verticals

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Satellite Ground Equipment Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Ground Equipment

- 11.1.2. Service

- 11.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.2.1. Maritime

- 11.2.2. Defense and Government

- 11.2.3. Enterprises

- 11.2.4. Media and Entertainment

- 11.2.5. Other End-user Verticals

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ST Engineering iDirect

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 L3Harris Technologies Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Iridium Communications Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Inmarsat Global Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Thales Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 KVH Industries Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Thuraya Telecommunications Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Orbcomm Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Cobham SATCOM (Combham Limited)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Gilat Satellite Networks Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Advantech Wireless Technologies Inc (Baylin Technologies)

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 ViaSat Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 ST Engineering iDirect

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Satellite Ground Equipment Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Satellite Ground Equipment Market Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Satellite Ground Equipment Market Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Satellite Ground Equipment Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 5: North America Satellite Ground Equipment Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 6: North America Satellite Ground Equipment Market Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Satellite Ground Equipment Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Satellite Ground Equipment Market Revenue (Million), by Type 2025 & 2033

- Figure 9: Europe Satellite Ground Equipment Market Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Satellite Ground Equipment Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 11: Europe Satellite Ground Equipment Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 12: Europe Satellite Ground Equipment Market Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Satellite Ground Equipment Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Satellite Ground Equipment Market Revenue (Million), by Type 2025 & 2033

- Figure 15: Asia Pacific Satellite Ground Equipment Market Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Satellite Ground Equipment Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 17: Asia Pacific Satellite Ground Equipment Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 18: Asia Pacific Satellite Ground Equipment Market Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Satellite Ground Equipment Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Satellite Ground Equipment Market Revenue (Million), by Type 2025 & 2033

- Figure 21: Latin America Satellite Ground Equipment Market Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Satellite Ground Equipment Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Latin America Satellite Ground Equipment Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Latin America Satellite Ground Equipment Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Satellite Ground Equipment Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Satellite Ground Equipment Market Revenue (Million), by Type 2025 & 2033

- Figure 27: Middle East and Africa Satellite Ground Equipment Market Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Satellite Ground Equipment Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 29: Middle East and Africa Satellite Ground Equipment Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 30: Middle East and Africa Satellite Ground Equipment Market Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Satellite Ground Equipment Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Satellite Ground Equipment Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Satellite Ground Equipment Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 3: Global Satellite Ground Equipment Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Satellite Ground Equipment Market Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Global Satellite Ground Equipment Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 6: Global Satellite Ground Equipment Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Satellite Ground Equipment Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Satellite Ground Equipment Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 9: Global Satellite Ground Equipment Market Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Satellite Ground Equipment Market Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Global Satellite Ground Equipment Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global Satellite Ground Equipment Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Satellite Ground Equipment Market Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Satellite Ground Equipment Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 15: Global Satellite Ground Equipment Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Satellite Ground Equipment Market Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Global Satellite Ground Equipment Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 18: Global Satellite Ground Equipment Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Satellite Ground Equipment Market?

The projected CAGR is approximately 12.12%.

2. Which companies are prominent players in the Satellite Ground Equipment Market?

Key companies in the market include ST Engineering iDirect, L3Harris Technologies Inc, Iridium Communications Inc, Inmarsat Global Limited, Thales Group, KVH Industries Inc, Thuraya Telecommunications Company, Orbcomm Inc, Cobham SATCOM (Combham Limited), Gilat Satellite Networks Ltd, Advantech Wireless Technologies Inc (Baylin Technologies), ViaSat Inc.

3. What are the main segments of the Satellite Ground Equipment Market?

The market segments include Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 52.41 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Internet of Things (IoT) and Autonomous Systems; Increasing Demand for Satellite Based Services.

6. What are the notable trends driving market growth?

Defense and Government is Expected to Hold Significant Share of the Market.

7. Are there any restraints impacting market growth?

Interference in Transmission of Data.

8. Can you provide examples of recent developments in the market?

February 2023 - CobhamSatcom and RBC Signals, a global satellite data communication solutions provider, announced an extended agreement to deploy CobhamSatcom's adaptable Tracker 6000 and 3700 series ground stations worldwide. The collaborative partnership between the two parties would dramatically expand RBC Signals' vast owned and partner ground network, providing integrated communication services to NGSO missions and constellations for Earth Observation, IoT, and Space Situational Awareness.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Satellite Ground Equipment Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Satellite Ground Equipment Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Satellite Ground Equipment Market?

To stay informed about further developments, trends, and reports in the Satellite Ground Equipment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence