Key Insights

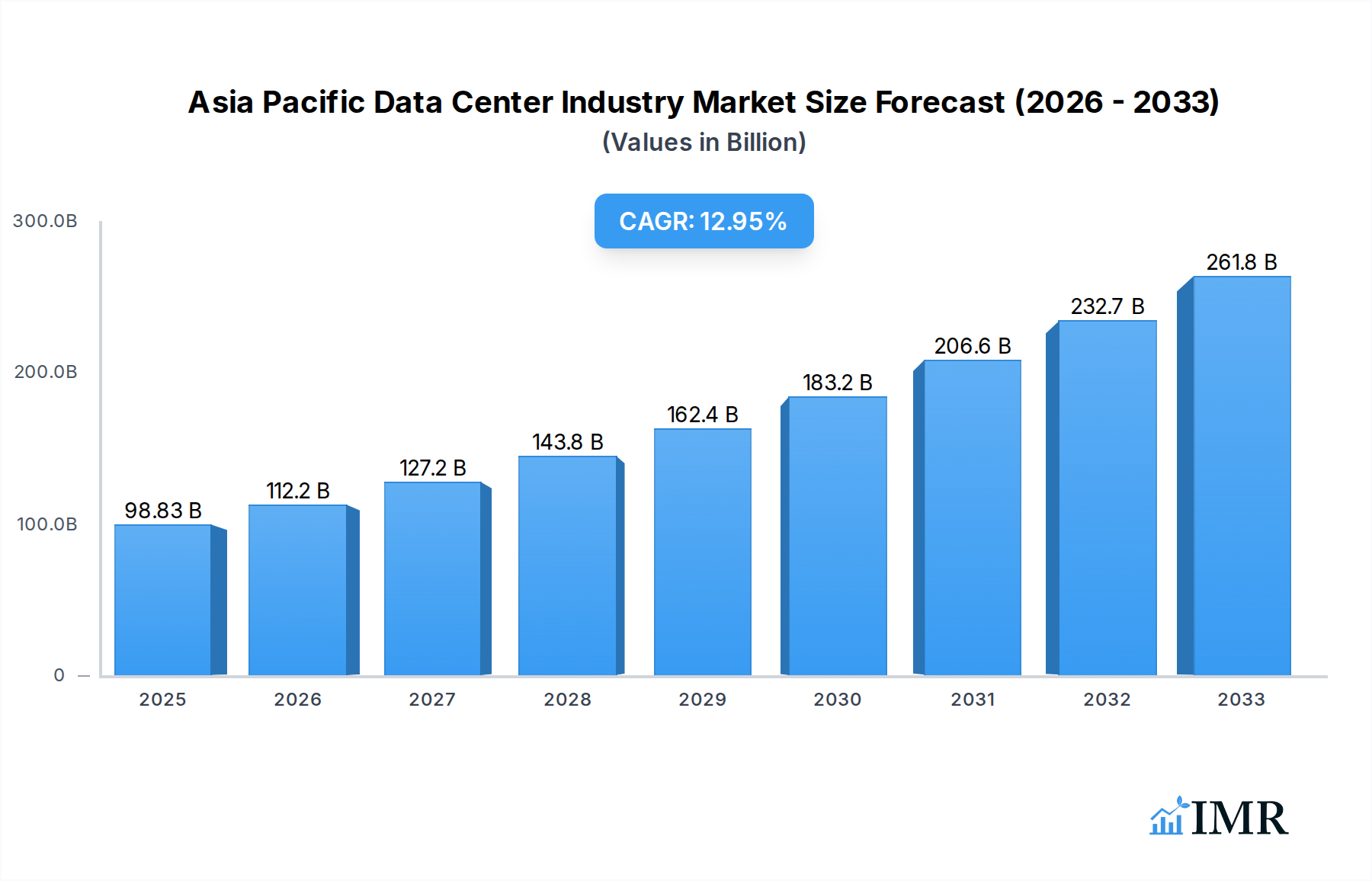

The Asia Pacific Data Center Industry is poised for remarkable expansion, with a projected market size of 98,834.9 million USD in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 13.7%, indicating a dynamic and rapidly evolving landscape. The region's burgeoning digital economy, fueled by increasing internet penetration, smartphone adoption, and the widespread use of cloud services, is a primary catalyst for this surge. Furthermore, the escalating demand for data processing and storage from critical sectors like BFSI, e-commerce, and telecommunications is driving significant investment in data center infrastructure. The expansion of hyperscale and colocation facilities is central to meeting this demand, with a growing preference for larger data center sizes such as massive and mega facilities to accommodate the immense data volumes. Governments across the Asia Pacific are also playing a crucial role through initiatives promoting digitalization and the development of smart cities, further accelerating data center deployment.

Asia Pacific Data Center Industry Market Size (In Billion)

The industry is characterized by several key trends that are shaping its trajectory. The increasing adoption of advanced technologies like AI and IoT is generating unprecedented data volumes, necessitating more sophisticated and scalable data center solutions. The migration of businesses towards cloud-based services, both public and private, is a significant driver, pushing the demand for reliable and high-performance data center capacity. The shift towards more energy-efficient and sustainable data center operations is also gaining momentum, driven by environmental concerns and regulatory pressures. Key players such as STT GDC Pte Ltd, Equinix Inc, and Digital Realty Trust Inc are actively investing in expanding their presence and capabilities across the region, particularly in major hubs like China, Japan, and India. Despite the optimistic outlook, challenges such as rising operational costs and the availability of skilled talent require strategic attention to ensure sustained growth and market leadership.

Asia Pacific Data Center Industry Company Market Share

Asia Pacific Data Center Industry Report: Market Dynamics, Growth Trends, and Key Player Insights (2019-2033)

Report Description:

Dive into the dynamic Asia Pacific data center industry with our comprehensive market research report. Spanning from 2019 to 2033, this in-depth analysis provides critical insights into market dynamics, growth trajectories, and key players shaping the future of digital infrastructure in the region. Leveraging a robust dataset with a base year of 2025 and a forecast period extending to 2033, this report is an indispensable resource for industry professionals, investors, and strategists seeking to navigate the burgeoning data center landscape. Discover critical trends, dominant regions, technological innovations, and emerging opportunities across all market segments, including Colocation Type (Hyperscale, Retail, Wholesale), Data Center Size (Large, Massive, Medium, Mega, Small), Tier Type (Tier 1 and 2, Tier 3, Tier 4), and End User segments (BFSI, Cloud, E-Commerce, Government, Manufacturing, Media & Entertainment, Telecom, Other End User). Understand the competitive environment, key drivers, barriers, and strategic initiatives of leading companies such as STT GDC Pte Ltd, Space DC Pte Ltd, Equinix Inc, NEXTDC Ltd, Princeton Digital Group, Keppel DC REIT Management Pte Ltd, Digital Realty Trust Inc, AirTrunk Operating Pty Ltd, Chindata Group Holdings Ltd, Canberra Data Centers, NTT Ltd, and KT Corporation. All quantitative values are presented in million units for clarity and actionable insights.

Asia Pacific Data Center Industry Market Dynamics & Structure

The Asia Pacific data center market is characterized by intense competition and rapid evolution, driven by escalating digital transformation and increasing data consumption. Market concentration is high in key hubs like Singapore, Tokyo, and Sydney, attracting significant investment from global and regional players. Technological innovation is a primary driver, with advancements in AI, IoT, and 5G demanding higher computing power and lower latency solutions. However, these innovations also present challenges, including the need for significant capital investment in advanced cooling, power, and network infrastructure. Regulatory frameworks vary across countries, with some actively promoting data center development through favorable policies while others impose stricter data localization requirements. Competitive product substitutes are limited to alternative cloud solutions and on-premise data centers, but the increasing demand for specialized services like edge computing is fostering new sub-segments. End-user demographics are diverse, with Cloud providers and BFSI sectors being major consumers, followed by E-Commerce and Telecom. Mergers and acquisitions (M&A) trends are significant, with larger players acquiring smaller entities to expand their geographic footprint and service offerings. For instance, the acquisition of smaller colocation providers by hyperscalers and large data center operators has been a notable trend. Innovation barriers include the high cost of land, energy procurement complexities, and the skilled workforce shortage for specialized roles.

- Market Concentration: Dominated by key hubs like Singapore, Tokyo, and Sydney.

- Technological Innovation Drivers: AI, IoT, 5G adoption driving demand for advanced infrastructure.

- Regulatory Frameworks: Varied policies across the region, impacting data localization and development.

- Competitive Landscape: Intense competition among established players and new entrants, with cloud solutions as primary alternatives.

- End-User Dominance: Cloud, BFSI, E-Commerce, and Telecom sectors are key demand drivers.

- M&A Trends: Strategic acquisitions for market expansion and service consolidation.

- Innovation Barriers: High capital expenditure, energy procurement challenges, and talent scarcity.

Asia Pacific Data Center Industry Growth Trends & Insights

The Asia Pacific data center industry is poised for unprecedented growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033, reaching a market size of over USD 150,000 million by 2033. This expansion is fueled by the relentless surge in data generation from digital services, cloud computing adoption, and the proliferation of connected devices across the region. Hyperscale data centers, catering to the massive demands of global cloud providers, represent a significant portion of this growth, driven by strategic investments in new build-outs and expansions. The adoption rate of colocation services, particularly wholesale and retail colocation, is also steadily increasing as businesses seek scalable, reliable, and cost-effective solutions for their IT infrastructure. Technological disruptions, such as the widespread implementation of AI and machine learning, are further accelerating demand for high-density computing power and advanced cooling systems, pushing the boundaries of data center design and efficiency. Consumer behavior shifts, with an increasing reliance on digital platforms for entertainment, commerce, and communication, are directly translating into higher data traffic and, consequently, greater demand for data center capacity. Emerging markets within Southeast Asia and India are demonstrating particularly strong growth potential, driven by government initiatives to promote digital economies and attract foreign investment. The market penetration of advanced data center technologies is expected to deepen, with a growing focus on sustainability, renewable energy integration, and optimized power utilization efficiency (PUE). Furthermore, the increasing complexity of IT workloads necessitates more sophisticated networking capabilities and edge computing deployments, creating new opportunities for specialized data center operators. The market size was estimated at USD 60,000 million in 2025. The historical market size was USD 45,000 million in 2024.

Dominant Regions, Countries, or Segments in Asia Pacific Data Center Industry

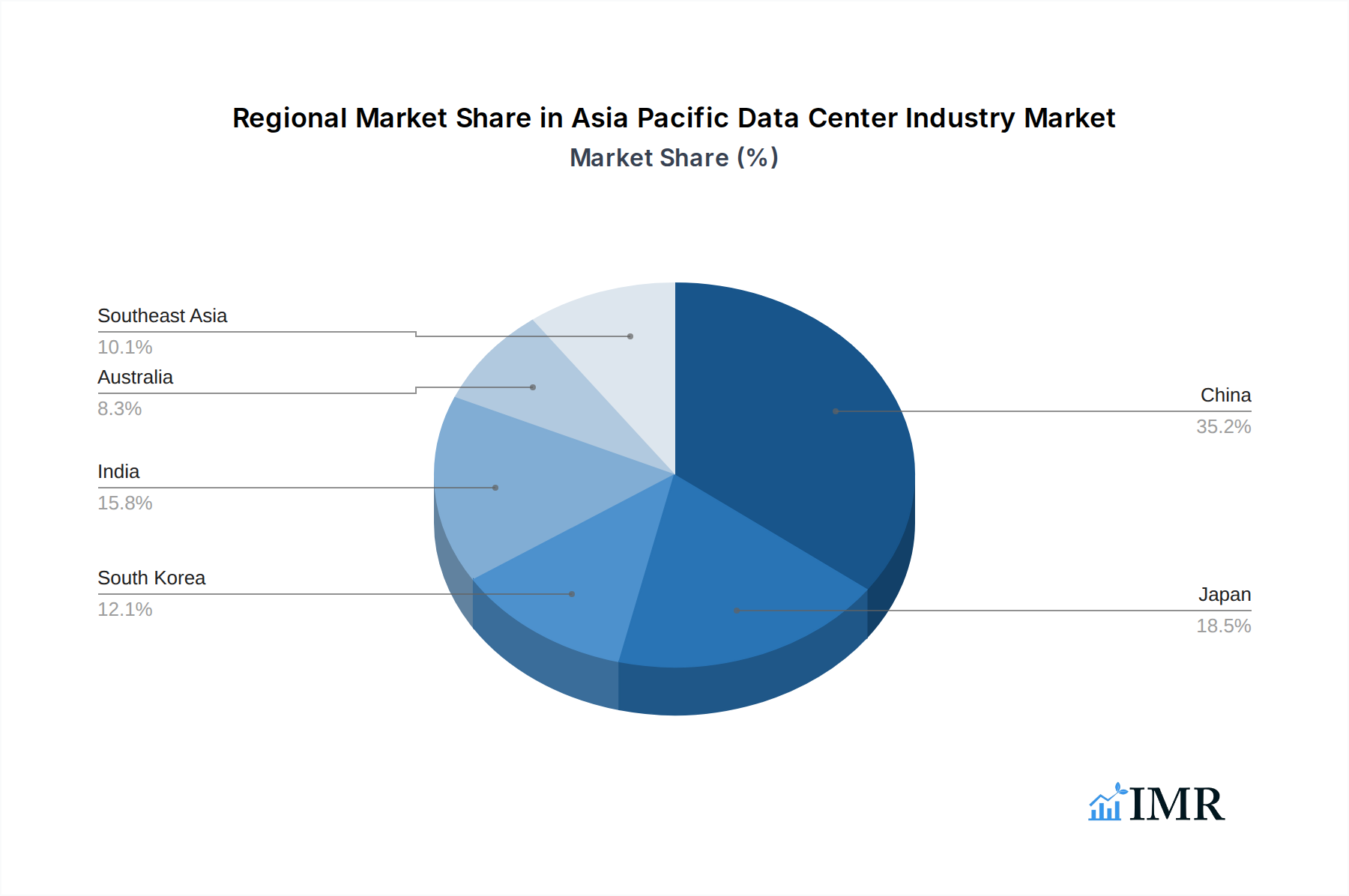

The Asia Pacific data center industry is witnessing robust growth across multiple segments, with Hyperscale colocation emerging as the dominant force, significantly outperforming Retail and Wholesale segments in terms of capacity deployment and investment. This dominance is primarily attributed to the insatiable demand from global cloud giants like Amazon Web Services, Microsoft Azure, and Google Cloud, who are expanding their regional footprints to cater to the burgeoning digital economies. Within Data Center Size, Massive and Mega facilities are increasingly prevalent, reflecting the scale of hyperscale operations and their need for vast power and cooling infrastructure. These large-scale deployments often necessitate Tier 3 and Tier 4 certifications to ensure high availability and fault tolerance, critical for mission-critical workloads. Geographically, Singapore continues to be a leading market, leveraging its strategic location, robust connectivity, and favorable business environment. However, countries like Australia, Japan, and increasingly, India and South Korea, are rapidly gaining prominence. Australia's strong economic growth and increasing cloud adoption, coupled with government support for digital infrastructure, are key drivers. Japan's mature digital ecosystem and significant enterprise demand contribute to its sustained growth. India, with its vast population and rapid digitization, presents immense long-term potential. The Cloud end-user segment is the primary driver of this hyperscale and massive data center growth, consuming over 40% of the market's capacity. This is closely followed by E-Commerce and Telecommunications, both experiencing substantial growth due to increased online retail activity and the rollout of 5G networks, respectively. Government adoption of cloud services and digital initiatives also contributes significantly, driving demand for secure and compliant data storage and processing. The BFSI sector, while a traditional large consumer, is increasingly adopting hybrid cloud strategies, leveraging colocation for enhanced flexibility and disaster recovery.

- Dominant Segment: Hyperscale Colocation Type.

- Predominant Data Center Sizes: Massive and Mega.

- Key Tier Types: Tier 3 and Tier 4, essential for reliability.

- Leading Geographic Markets: Singapore, Australia, Japan, India, and South Korea.

- Primary End User: Cloud, followed by E-Commerce, Telecom, and BFSI.

- Key Drivers for Dominance:

- Massive investments from global cloud providers.

- Exponential growth in data generation and digital services.

- Government initiatives promoting digital economies and infrastructure development.

- Increasing demand for low-latency services enabled by edge computing.

- Expansion of 5G networks requiring localized data processing.

- Market Share Insights: Hyperscale segment is estimated to hold over 50% of the market's current capacity deployment. Cloud end-user segment accounts for approximately 40% of the total data center capacity demand.

Asia Pacific Data Center Industry Product Landscape

The Asia Pacific data center industry product landscape is increasingly sophisticated, featuring innovations focused on energy efficiency, high-density computing, and enhanced connectivity. Liquid cooling solutions are gaining traction for high-performance computing (HPC) and AI workloads, offering superior thermal management capabilities compared to traditional air cooling. Modular data center designs are enabling faster deployment and scalability, catering to the dynamic needs of businesses. Advanced power distribution units (PDUs) and uninterruptible power supplies (UPS) with higher efficiency ratings and improved battery backup are standard. Network infrastructure is evolving with the adoption of higher bandwidth switches and fiber optic cabling, supporting the demands of 5G and cloud services. Cybersecurity solutions, including physical and digital security measures, are integral to data center offerings, ensuring data integrity and protection against threats. The trend towards sustainability is driving the adoption of renewable energy integration technologies and intelligent building management systems to optimize resource consumption.

Key Drivers, Barriers & Challenges in Asia Pacific Data Center Industry

Key Drivers:

The Asia Pacific data center industry is propelled by several formidable drivers. The relentless surge in data creation and consumption, fueled by digitalization, cloud adoption, and the proliferation of IoT devices, is a primary catalyst. Government initiatives across the region promoting digital transformation and smart city development provide significant impetus. The expansion of 5G networks necessitates localized data processing, driving demand for edge and hyperscale facilities. Strategic investments from global technology giants and private equity firms underscore the sector's robust growth potential. Furthermore, increasing demand for advanced computing capabilities for AI and machine learning applications is creating new opportunities.

Barriers & Challenges:

Despite the optimistic outlook, the industry faces significant barriers and challenges. The escalating cost of land and construction in prime urban locations presents a major hurdle. Procuring sufficient and reliable power, especially from renewable sources, remains a complex undertaking in many markets. Navigating diverse and evolving regulatory landscapes, including data localization laws and environmental standards, can be burdensome. A shortage of skilled professionals in areas like data center engineering and operations adds to the operational challenges. Intense competition, particularly in mature markets, can put pressure on pricing and profit margins. Supply chain disruptions for critical hardware and equipment can also lead to project delays and cost overruns. The average cost of land for data center development in prime Asian markets has increased by approximately 15% year-on-year.

Emerging Opportunities in Asia Pacific Data Center Industry

Emerging opportunities in the Asia Pacific data center industry are abundant and diverse. The burgeoning adoption of Artificial Intelligence (AI) and Machine Learning (ML) is creating significant demand for specialized high-density computing and GPU-accelerated infrastructure, offering lucrative avenues for tailored data center solutions. The expansion of the Internet of Things (IoT) across various industries, from manufacturing to smart cities, is driving the need for distributed edge data centers closer to data sources, enabling real-time processing and reducing latency. Untapped markets in Southeast Asia and certain developing economies within the region present substantial growth potential, driven by increasing internet penetration and digital economic initiatives. The growing emphasis on sustainability and green computing is opening doors for data centers powered by renewable energy sources and incorporating advanced energy-efficient technologies. Furthermore, the increasing demand for specialized data hosting for industries like genomics and scientific research, requiring high-performance computing and stringent security, represents a niche but high-value opportunity. The projected market for edge data centers in Asia Pacific is expected to grow at a CAGR of over 18% through 2030.

Growth Accelerators in the Asia Pacific Data Center Industry Industry

Several catalysts are accelerating long-term growth in the Asia Pacific data center industry. Technological breakthroughs in areas such as advanced cooling systems (e.g., immersion cooling) and highly efficient power management are enabling the development of more powerful and sustainable data centers. Strategic partnerships between data center operators, cloud providers, and telecommunications companies are crucial for expanding network reach and service offerings, creating integrated ecosystems. Market expansion strategies, including significant investments in new build-outs and acquisitions in high-growth regions, are broadening the industry's footprint. The increasing adoption of digital transformation initiatives by governments and enterprises across the region is a sustained driver of demand. Furthermore, the development of smart grids and the integration of renewable energy sources are making data center operations more sustainable and cost-effective.

Key Players Shaping the Asia Pacific Data Center Industry Market

- STT GDC Pte Ltd

- Space DC Pte Ltd

- Equinix Inc

- NEXTDC Ltd

- Princeton Digital Group

- Keppel DC REIT Management Pte Ltd

- Digital Realty Trust Inc

- AirTrunk Operating Pty Ltd

- Chindata Group Holdings Ltd

- Canberra Data Centers

- NTT Ltd

- KT Corporation

Notable Milestones in Asia Pacific Data Center Industry Sector

- December 2022: HGC Global Communications established an agreement with Digital Realty to boost customers’ edge connectivity. Under the agreement, Digital Realty will use edgeX by HGC services for over-the-top (OTT) customers in its three Singapore data centres, enhancing connectivity and service delivery.

- November 2022: Equinix announced its 15th international business exchange (IBX) data centre in Tokyo, Japan, named TY15. This initial investment of USD 115 million signifies a major expansion of Equinix's presence in Japan, with the first phase providing approximately 1,200 cabinets and a full build-out capacity of 3,700 cabinets, addressing growing demand for digital infrastructure.

- September 2022: NTT Ltd announced the commencement of construction for its sixth data centre in Cyberjaya, Malaysia, known as Cyberjaya 6 (CBJ6). With an initial investment of over USD 50 million, this expansion, along with Cyberjaya 5 (CBJ5), will bring a combined facility load of 22MW across 200,000 sq ft., strengthening NTT's footprint in the region and catering to increased demand.

In-Depth Asia Pacific Data Center Industry Market Outlook

The Asia Pacific data center industry is set for sustained and robust growth, driven by a confluence of powerful market forces. The ongoing digital transformation across all sectors, coupled with the exponential rise in data generation, will continue to fuel demand for scalable and high-performance infrastructure. Strategic investments in hyperscale facilities and the burgeoning edge computing sector are key indicators of future expansion. Emerging economies are poised to become significant data center hubs, offering substantial growth potential. The industry's focus on sustainability and the integration of renewable energy will not only address environmental concerns but also present economic advantages. Partnerships and strategic alliances will play a crucial role in expanding service offerings and market reach, fostering a more interconnected digital ecosystem. The market is expected to witness continued consolidation through M&A activities, leading to a more mature and competitive landscape. The overall outlook is highly positive, indicating significant opportunities for stakeholders to capitalize on the region's digital evolution. The projected market value for the Asia Pacific data center industry is expected to exceed USD 150,000 million by 2033.

Asia Pacific Data Center Industry Segmentation

-

1. Data Center Size

- 1.1. Large

- 1.2. Massive

- 1.3. Medium

- 1.4. Mega

- 1.5. Small

-

2. Tier Type

- 2.1. Tier 1 and 2

- 2.2. Tier 3

- 2.3. Tier 4

-

3. Absorption

- 3.1. Non-Utilized

- 3.2. Colocation Type

- 3.3. Hyperscale

- 3.4. Retail

- 3.5. Wholesale

-

4. End User

- 4.1. BFSI

- 4.2. Cloud

- 4.3. E-Commerce

- 4.4. Government

- 4.5. Manufacturing

- 4.6. Media & Entertainment

- 4.7. Telecom

- 4.8. Other End User

Asia Pacific Data Center Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Data Center Industry Regional Market Share

Geographic Coverage of Asia Pacific Data Center Industry

Asia Pacific Data Center Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Data Center Size

- 5.1.1. Large

- 5.1.2. Massive

- 5.1.3. Medium

- 5.1.4. Mega

- 5.1.5. Small

- 5.2. Market Analysis, Insights and Forecast - by Tier Type

- 5.2.1. Tier 1 and 2

- 5.2.2. Tier 3

- 5.2.3. Tier 4

- 5.3. Market Analysis, Insights and Forecast - by Absorption

- 5.3.1. Non-Utilized

- 5.3.2. Colocation Type

- 5.3.3. Hyperscale

- 5.3.4. Retail

- 5.3.5. Wholesale

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. BFSI

- 5.4.2. Cloud

- 5.4.3. E-Commerce

- 5.4.4. Government

- 5.4.5. Manufacturing

- 5.4.6. Media & Entertainment

- 5.4.7. Telecom

- 5.4.8. Other End User

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Data Center Size

- 6. Asia Pacific Data Center Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Data Center Size

- 6.1.1. Large

- 6.1.2. Massive

- 6.1.3. Medium

- 6.1.4. Mega

- 6.1.5. Small

- 6.2. Market Analysis, Insights and Forecast - by Tier Type

- 6.2.1. Tier 1 and 2

- 6.2.2. Tier 3

- 6.2.3. Tier 4

- 6.3. Market Analysis, Insights and Forecast - by Absorption

- 6.3.1. Non-Utilized

- 6.3.2. Colocation Type

- 6.3.3. Hyperscale

- 6.3.4. Retail

- 6.3.5. Wholesale

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. BFSI

- 6.4.2. Cloud

- 6.4.3. E-Commerce

- 6.4.4. Government

- 6.4.5. Manufacturing

- 6.4.6. Media & Entertainment

- 6.4.7. Telecom

- 6.4.8. Other End User

- 6.1. Market Analysis, Insights and Forecast - by Data Center Size

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 STT GDC Pte Ltd5 4 LIST OF COMPANIES STUDIE

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Space DC Pte Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Equinix Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 NEXTDC Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Princeton Digital Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Keppel DC REIT Management Pte Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Digital Realty Trust Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 AirTrunk Operating Pty Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Chindata Group Holdings Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Canberra Data Centers

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 NTT Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 KT Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 STT GDC Pte Ltd5 4 LIST OF COMPANIES STUDIE

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Data Center Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Data Center Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Data Center Industry Revenue million Forecast, by Data Center Size 2020 & 2033

- Table 2: Asia Pacific Data Center Industry Volume K Unit Forecast, by Data Center Size 2020 & 2033

- Table 3: Asia Pacific Data Center Industry Revenue million Forecast, by Tier Type 2020 & 2033

- Table 4: Asia Pacific Data Center Industry Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 5: Asia Pacific Data Center Industry Revenue million Forecast, by Absorption 2020 & 2033

- Table 6: Asia Pacific Data Center Industry Volume K Unit Forecast, by Absorption 2020 & 2033

- Table 7: Asia Pacific Data Center Industry Revenue million Forecast, by End User 2020 & 2033

- Table 8: Asia Pacific Data Center Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 9: Asia Pacific Data Center Industry Revenue million Forecast, by Region 2020 & 2033

- Table 10: Asia Pacific Data Center Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: Asia Pacific Data Center Industry Revenue million Forecast, by Data Center Size 2020 & 2033

- Table 12: Asia Pacific Data Center Industry Volume K Unit Forecast, by Data Center Size 2020 & 2033

- Table 13: Asia Pacific Data Center Industry Revenue million Forecast, by Tier Type 2020 & 2033

- Table 14: Asia Pacific Data Center Industry Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 15: Asia Pacific Data Center Industry Revenue million Forecast, by Absorption 2020 & 2033

- Table 16: Asia Pacific Data Center Industry Volume K Unit Forecast, by Absorption 2020 & 2033

- Table 17: Asia Pacific Data Center Industry Revenue million Forecast, by End User 2020 & 2033

- Table 18: Asia Pacific Data Center Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 19: Asia Pacific Data Center Industry Revenue million Forecast, by Country 2020 & 2033

- Table 20: Asia Pacific Data Center Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 21: China Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: China Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Japan Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Japan Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: South Korea Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: India Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: India Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Australia Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Australia Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: New Zealand Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: New Zealand Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Indonesia Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Indonesia Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Malaysia Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Malaysia Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Singapore Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Singapore Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Thailand Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Thailand Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Vietnam Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Vietnam Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Philippines Asia Pacific Data Center Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Philippines Asia Pacific Data Center Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Data Center Industry?

The projected CAGR is approximately 13.7%.

2. Which companies are prominent players in the Asia Pacific Data Center Industry?

Key companies in the market include STT GDC Pte Ltd5 4 LIST OF COMPANIES STUDIE, Space DC Pte Ltd, Equinix Inc, NEXTDC Ltd, Princeton Digital Group, Keppel DC REIT Management Pte Ltd, Digital Realty Trust Inc, AirTrunk Operating Pty Ltd, Chindata Group Holdings Ltd, Canberra Data Centers, NTT Ltd, KT Corporation.

3. What are the main segments of the Asia Pacific Data Center Industry?

The market segments include Data Center Size, Tier Type, Absorption, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 98834.9 million as of 2022.

5. What are some drivers contributing to market growth?

Rise of E-Commerce; Flourishing Startup Culture.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Slow Penetration Rate in Developing Countries.

8. Can you provide examples of recent developments in the market?

December 2022: HGC Global Communications has established an agreement with Digital Realty to boost customers’ edge connectivity. Under the agreement, Digital Realty will use edgeX by HGC services for over-the-top (OTT) customers in its three Singapore data centres.November 2022: Equinix announced its 15th international business exchange (IBX) data centre in Tokyo, Japan. The company said that it has made an initial investment of USD 115 million on the new data centre, touted TY15. The first phase of TY15 will provide an initial capacity of approximately 1,200 cabinets, and 3,700 cabinets when fully built out.September 2022: NTT Ltd announced the commencement of the construction of its sixth data centre in Cyberjaya. NTT plans to initially invest over USD 50 million in the sixth data centre, which is also known as Cyberjaya 6 (CBJ6). Further, CBJ6 and CBJ5 will have a total facility load of 22MW, spanning a combined 200,000 sq ft.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Data Center Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Data Center Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Data Center Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Data Center Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence