Key Insights

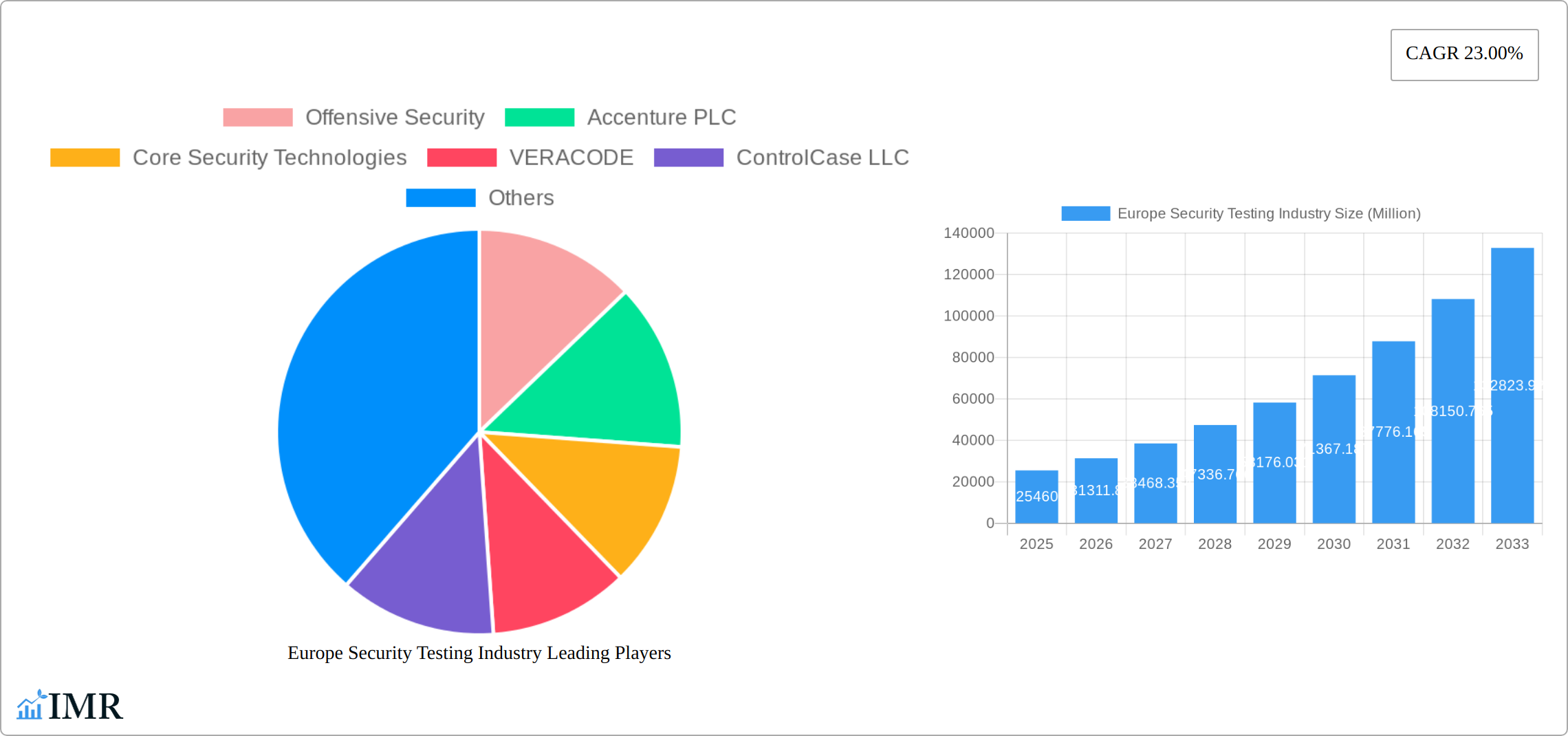

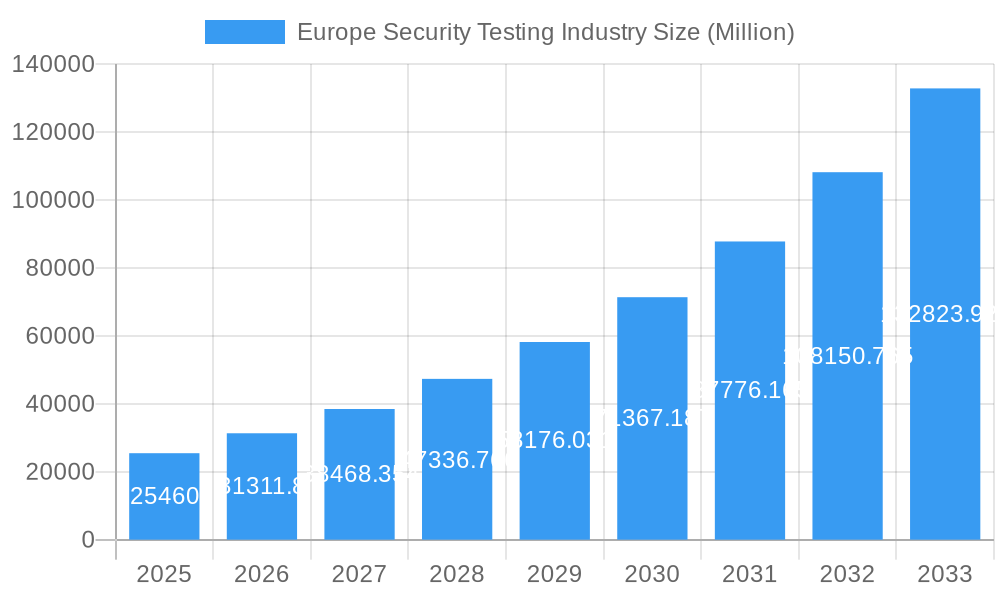

The European security testing market, valued at €25.46 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 23% from 2025 to 2033. This significant expansion is driven by several key factors. The increasing sophistication of cyber threats targeting businesses across all sectors—from BFSI and government to healthcare and retail—is fueling demand for comprehensive security testing solutions. The shift towards cloud-based infrastructure and the proliferation of mobile applications necessitate robust security measures, further driving market growth. Furthermore, stringent data privacy regulations like GDPR are compelling organizations to invest heavily in ensuring compliance through rigorous application and network security testing. The market's segmentation reveals a diverse landscape, with significant contributions from on-premise, cloud, and hybrid deployment models. Application security testing (AST), encompassing mobile, web, cloud, and enterprise application testing, dominates the type segment. SAST, DAST, IAST, and RASP testing methodologies are widely adopted, utilizing tools like web application testing tools, code review tools, and penetration testing tools. Germany, the United Kingdom, and France represent the largest national markets within Europe, reflecting their advanced digital infrastructure and robust regulatory frameworks.

Europe Security Testing Industry Market Size (In Billion)

Competition within the European security testing market is intense, with both established players like Accenture, IBM, and McAfee, and specialized firms like Veracode and Offensive Security vying for market share. The market is characterized by ongoing innovation, with new testing methodologies and tools constantly emerging to address the evolving threat landscape. While the market enjoys strong growth prospects, challenges remain. These include the skills gap in cybersecurity professionals, the high cost of implementing comprehensive security testing programs, and the complexity of integrating various testing tools and methodologies within organizations. However, the sustained growth in cybercrime and regulatory pressures ensures that the demand for robust security testing will continue to outweigh these challenges, paving the way for continued market expansion throughout the forecast period.

Europe Security Testing Industry Company Market Share

Europe Security Testing Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Europe security testing market, encompassing market size, growth trends, key players, and future outlook. With a focus on application security testing, network security testing, and various testing types (SAST, DAST, IAST, RASP), this report is an essential resource for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with 2025 as the base and estimated year.

Europe Security Testing Industry Market Dynamics & Structure

The European security testing market is a dynamic and evolving landscape, characterized by a **moderately concentrated structure** with a blend of established global leaders and agile, niche-specialized firms. This ecosystem is significantly shaped by the relentless evolution of cyber threats and the increasingly stringent, yet vital, regulatory frameworks across the continent. Technological innovation is the engine of growth, with a constant pursuit of advanced solutions to combat sophisticated attacks. Consequently, the market experiences ongoing **mergers and acquisitions (M&A) activity**, a strategic imperative for larger entities seeking to broaden their service offerings, acquire specialized expertise, and expand their geographical footprint. The accelerating adoption of cloud and hybrid deployment models further amplifies market growth, directly correlating with the escalating demand for robust application security testing across a vast spectrum of end-user industries, from critical infrastructure to emerging digital services.

- Market Concentration: Moderately concentrated, with a top 5 market share of approximately 45-55%. This indicates a significant presence of key players while allowing room for specialized competitors.

- Technological Innovation: Key drivers include the integration of AI and machine learning for predictive threat detection and automated vulnerability identification, enhanced automation for efficiency and scalability, and the pervasive adoption of DevSecOps principles for seamless security integration throughout the software development lifecycle.

- Regulatory Frameworks: The increasing stringency and enforcement of data protection regulations such as the GDPR (General Data Protection Regulation), NIS2 Directive, and emerging sector-specific compliance mandates are powerful catalysts, compelling organizations to invest in comprehensive security testing solutions.

- Competitive Substitutes: While direct substitutes are limited, organizations may leverage alternative security solutions that offer overlapping functionalities. However, dedicated security testing provides a more specialized and in-depth approach to identifying and mitigating vulnerabilities.

- End-User Demographics: Demand is robust across a diverse array of industries, including the highly regulated Banking, Financial Services, and Insurance (BFSI) sector, government agencies, critical healthcare providers, and the fast-paced IT & Telecommunications industry. Emerging sectors like IoT and FinTech are also significant contributors.

- M&A Trends: An average of 15-25 M&A deals per year during 2019-2024 reflects active consolidation. This trend is predicted to increase to 25-35 deals annually in the forecast period, underscoring the sector's maturity and the strategic importance of acquiring scale and capabilities.

Europe Security Testing Industry Growth Trends & Insights

The European security testing market experienced significant growth during the historical period (2019-2024), driven by the rising adoption of cloud computing, increasing cyber threats, and stringent data privacy regulations. The market size reached xx Million in 2024 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033). This growth is primarily fueled by the increasing adoption of application security testing, particularly web application security testing and cloud application security testing, alongside the rising demand for penetration testing services. Technological advancements, like AI and machine learning integration within security testing tools, have significantly improved testing efficiency and accuracy. Furthermore, the shift towards DevSecOps practices is accelerating the adoption of automated security testing tools, resulting in increased market penetration. Market penetration for cloud-based solutions is growing significantly, exceeding xx% in 2024 and expected to exceed xx% by 2033.

Dominant Regions, Countries, or Segments in Europe Security Testing Industry

The United Kingdom, Germany, and France represent the largest national markets within Europe, contributing to xx%, xx%, and xx% of the total market share respectively in 2024. However, the "Rest of Europe" segment shows significant growth potential, driving an overall market expansion. Application security testing constitutes the largest segment by type, holding a market share of approximately xx% in 2024, owing to the increased adoption of cloud-based applications and rising digital transformation initiatives. The BFSI and government sectors remain the dominant end-user industries, driven by stringent regulatory compliance requirements and the sensitivity of their data. The cloud deployment model exhibits the fastest growth, driven by the advantages of scalability, cost-effectiveness, and accessibility.

- Key Drivers in UK: Strong IT infrastructure, high adoption of cloud technologies.

- Key Drivers in Germany: Robust regulatory framework, emphasis on data security.

- Key Drivers in France: Increasing digitalization initiatives, government investments in cybersecurity.

- Key Drivers in Rest of Europe: Growing adoption of cloud services, rising cybersecurity awareness.

- Application Security Testing Dominance: Driven by the expanding use of web, mobile and cloud applications.

- BFSI and Government Sector Leadership: High regulatory compliance needs and sensitive data protection.

- Cloud Deployment Model Growth: Scalability, cost-effectiveness, and accessibility are major factors.

Europe Security Testing Industry Product Landscape

The European security testing market boasts a rich and diverse product landscape, offering a comprehensive suite of solutions to address the multifaceted challenges of cybersecurity. This includes sophisticated penetration testing tools for simulating real-world attacks, advanced web application security testing tools to identify vulnerabilities in online platforms, meticulous code review tools for static and dynamic analysis, and comprehensive software testing tools that embed security checks throughout the development pipeline. Technological advancements are at the forefront, with the integration of AI and machine learning significantly enhancing the accuracy and predictive capabilities of these tools. Automation is a critical differentiator, enabling increased efficiency and scalability in testing processes, particularly when integrated with DevOps pipelines for continuous security assurance. Unique selling propositions (USPs) often center on the ability to deliver ease of use, comprehensive coverage across complex architectures, and specialized functionalities tailored for specific application types, such as the unique security considerations of mobile applications or the dynamic environments of cloud-native applications.

Key Drivers, Barriers & Challenges in Europe Security Testing Industry

Key Drivers: The relentless surge in the frequency and sophistication of cyberattacks remains a primary impetus for the European security testing industry. This is further amplified by the robust and ever-evolving landscape of data privacy regulations, including the GDPR and NIS2 Directive, which mandate stringent security measures. The accelerated pace of digital transformation initiatives and the widespread adoption of cloud computing create new attack surfaces, necessitating proactive security testing. Furthermore, the increasing imperative to integrate security seamlessly into the software development lifecycle, particularly through the adoption of DevSecOps practices, is generating significant demand for advanced testing solutions.

Key Challenges: The inherent complexity of modern, interconnected software applications presents a significant hurdle, making comprehensive vulnerability identification an intricate task. A persistent shortage of highly skilled cybersecurity professionals exacerbates this challenge, limiting the capacity for effective testing and remediation. The substantial cost associated with implementing and maintaining comprehensive security testing programs can also be a barrier for some organizations. Moreover, the growing concern over supply chain vulnerabilities, the intricate and often fragmented nature of regulatory compliance, and the intense competition within the market add further layers of complexity. For instance, a reported 30-40% increase in cyberattacks targeting European businesses in 2024 has undoubtedly placed immense pressure on organizations to elevate their security testing practices to mitigate these escalating threats.

Emerging Opportunities in Europe Security Testing Industry

Untapped markets include smaller enterprises and SMEs, which are increasingly adopting cloud-based services and thus requiring enhanced security measures. Emerging opportunities include the integration of security testing with AI, IoT security testing, and the expansion of managed security services. Consumer preference for enhanced data security and privacy continues to drive the adoption of more rigorous security testing methods.

Growth Accelerators in the Europe Security Testing Industry

Strategic partnerships between security testing vendors and cloud providers are creating significant synergies. Technological breakthroughs, such as AI-powered vulnerability detection, are significantly improving testing efficiency and accuracy. Market expansion through strategic acquisitions and the development of new testing capabilities for emerging technologies (e.g., IoT, AI) are contributing significantly to market growth.

Key Players Shaping the Europe Security Testing Industry Market

- Offensive Security

- Accenture PLC

- Core Security Technologies

- VERACODE

- ControlCase LLC

- McAfee LLC

- Netcraft Ltd

- Maveric Systems

- Paladion Networks

- Cisco Systems Inc

- IBM

- Hewlett Packard Enterprise Development LP

Notable Milestones in Europe Security Testing Industry Sector

- January 2022: GrammaTech significantly enhanced its software supply chain security capabilities with the launch of a new version of its CodeSentry platform, featuring improved SBOM (Software Bill of Materials) generation and more advanced risk detection mechanisms.

- January 2022: NTT Security AppSec Solutions Inc. introduced a novel solution designed to provide dynamic application security testing (DAST) capabilities seamlessly integrated throughout the entire software development lifecycle, promoting a shift-left security approach.

In-Depth Europe Security Testing Industry Market Outlook

The European security testing market is on a trajectory for sustained and robust growth, propelled by a confluence of powerful factors. The escalating volume and sophistication of cyber threats continue to be a primary driver, compelling organizations to prioritize proactive security measures. Coupled with this, the increasing stringency and global scope of regulatory mandates are creating a persistent demand for comprehensive and compliant testing solutions. The ongoing expansion and adoption of cloud-based applications, from public to private and hybrid environments, present new attack vectors that require specialized testing expertise. Strategic investments in cutting-edge technologies such as AI-driven anomaly detection, predictive vulnerability analysis, and advanced automation will further sharpen testing capabilities, leading to more efficient and effective security outcomes. The market is also expected to witness continued consolidation through strategic partnerships and M&A activity, leading to a more mature and integrated competitive landscape. Ultimately, the prevailing focus on adopting proactive security strategies and embedding security within the development lifecycle through DevSecOps will ensure the sector's sustainable growth and foster continuous innovation, creating substantial and lucrative opportunities for all market participants.

Europe Security Testing Industry Segmentation

-

1. Deployment

- 1.1. On Premise

- 1.2. Cloud

- 1.3. Hybrid

-

2. Type

-

2.1. Network Security Testing

- 2.1.1. VPN Testing

- 2.1.2. Firewall Testing

- 2.1.3. Other Service Types

-

2.2. Application Security Testing

-

2.2.1. Application Type

- 2.2.1.1. Mobile Application Security Testing

- 2.2.1.2. Web Application Security Testing

- 2.2.1.3. Cloud Application Security Testing

- 2.2.1.4. Enterprise Application Security Testing

-

2.2.2. Testing Type

- 2.2.2.1. SAST

- 2.2.2.2. DAST

- 2.2.2.3. IAST

- 2.2.2.4. RASP

-

2.2.1. Application Type

-

2.1. Network Security Testing

-

3. Testing Tool

- 3.1. Web Application Testing Tool

- 3.2. Code Review Tool

- 3.3. Penetration Testing Tool

- 3.4. Software Testing Tool

- 3.5. Other Testing Tools

-

4. End-User Industry

- 4.1. Government

- 4.2. BFSI

- 4.3. Healthcare

- 4.4. Manufacturing

- 4.5. IT and Telecom

- 4.6. Retail

- 4.7. Other End-User Industries

Europe Security Testing Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Security Testing Industry Regional Market Share

Geographic Coverage of Europe Security Testing Industry

Europe Security Testing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 23.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. On Premise

- 5.1.2. Cloud

- 5.1.3. Hybrid

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Network Security Testing

- 5.2.1.1. VPN Testing

- 5.2.1.2. Firewall Testing

- 5.2.1.3. Other Service Types

- 5.2.2. Application Security Testing

- 5.2.2.1. Application Type

- 5.2.2.1.1. Mobile Application Security Testing

- 5.2.2.1.2. Web Application Security Testing

- 5.2.2.1.3. Cloud Application Security Testing

- 5.2.2.1.4. Enterprise Application Security Testing

- 5.2.2.2. Testing Type

- 5.2.2.2.1. SAST

- 5.2.2.2.2. DAST

- 5.2.2.2.3. IAST

- 5.2.2.2.4. RASP

- 5.2.2.1. Application Type

- 5.2.1. Network Security Testing

- 5.3. Market Analysis, Insights and Forecast - by Testing Tool

- 5.3.1. Web Application Testing Tool

- 5.3.2. Code Review Tool

- 5.3.3. Penetration Testing Tool

- 5.3.4. Software Testing Tool

- 5.3.5. Other Testing Tools

- 5.4. Market Analysis, Insights and Forecast - by End-User Industry

- 5.4.1. Government

- 5.4.2. BFSI

- 5.4.3. Healthcare

- 5.4.4. Manufacturing

- 5.4.5. IT and Telecom

- 5.4.6. Retail

- 5.4.7. Other End-User Industries

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Europe Security Testing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. On Premise

- 6.1.2. Cloud

- 6.1.3. Hybrid

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Network Security Testing

- 6.2.1.1. VPN Testing

- 6.2.1.2. Firewall Testing

- 6.2.1.3. Other Service Types

- 6.2.2. Application Security Testing

- 6.2.2.1. Application Type

- 6.2.2.1.1. Mobile Application Security Testing

- 6.2.2.1.2. Web Application Security Testing

- 6.2.2.1.3. Cloud Application Security Testing

- 6.2.2.1.4. Enterprise Application Security Testing

- 6.2.2.2. Testing Type

- 6.2.2.2.1. SAST

- 6.2.2.2.2. DAST

- 6.2.2.2.3. IAST

- 6.2.2.2.4. RASP

- 6.2.2.1. Application Type

- 6.2.1. Network Security Testing

- 6.3. Market Analysis, Insights and Forecast - by Testing Tool

- 6.3.1. Web Application Testing Tool

- 6.3.2. Code Review Tool

- 6.3.3. Penetration Testing Tool

- 6.3.4. Software Testing Tool

- 6.3.5. Other Testing Tools

- 6.4. Market Analysis, Insights and Forecast - by End-User Industry

- 6.4.1. Government

- 6.4.2. BFSI

- 6.4.3. Healthcare

- 6.4.4. Manufacturing

- 6.4.5. IT and Telecom

- 6.4.6. Retail

- 6.4.7. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Offensive Security

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Accenture PLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Core Security Technologies

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 VERACODE

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ControlCase LLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 McAfee LLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Netcraft Ltd*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Maveric Systems

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Paladion Networks

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Cisco Systems Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 IBM

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Hewlett Packard Enterprise Development LP

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Offensive Security

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Security Testing Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Security Testing Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Security Testing Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 2: Europe Security Testing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 3: Europe Security Testing Industry Revenue Million Forecast, by Testing Tool 2020 & 2033

- Table 4: Europe Security Testing Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 5: Europe Security Testing Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Security Testing Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 7: Europe Security Testing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Europe Security Testing Industry Revenue Million Forecast, by Testing Tool 2020 & 2033

- Table 9: Europe Security Testing Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 10: Europe Security Testing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United Kingdom Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Germany Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: France Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Italy Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Spain Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Netherlands Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Belgium Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Sweden Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Norway Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Poland Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Denmark Europe Security Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Security Testing Industry?

The projected CAGR is approximately 23.00%.

2. Which companies are prominent players in the Europe Security Testing Industry?

Key companies in the market include Offensive Security, Accenture PLC, Core Security Technologies, VERACODE, ControlCase LLC, McAfee LLC, Netcraft Ltd*List Not Exhaustive, Maveric Systems, Paladion Networks, Cisco Systems Inc, IBM, Hewlett Packard Enterprise Development LP.

3. What are the main segments of the Europe Security Testing Industry?

The market segments include Deployment, Type, Testing Tool, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.46 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Safety from Security Threats; Government Regulations Driving Security Needs.

6. What are the notable trends driving market growth?

Penetration Testing Tools segment is anticipated to register significant growth.

7. Are there any restraints impacting market growth?

Limited Computing Performance.

8. Can you provide examples of recent developments in the market?

January 2022 - GrammaTech, an application security testing product, and software research service provider, announced the launch of a new version of the company's CodeSentry software supply chain security platform, which enables organizations to produce a software bill of materials (SBOM) quickly. The software enables organizations to proactively detect and address risks in commercial off-the-shelf applications and third-party software and allows development teams to ensure they are delivering secure and compliant software.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Security Testing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Security Testing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Security Testing Industry?

To stay informed about further developments, trends, and reports in the Europe Security Testing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence