Key Insights

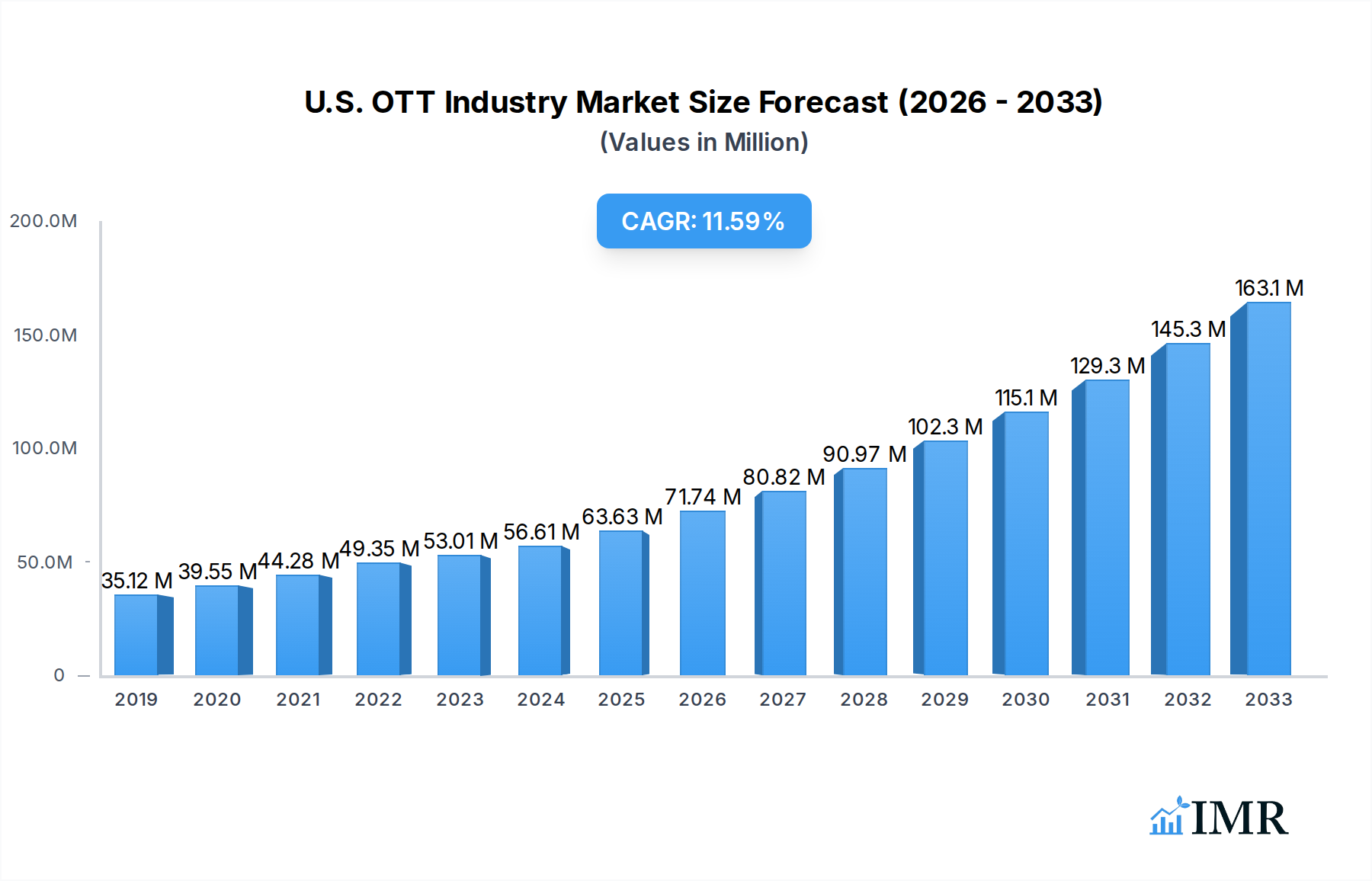

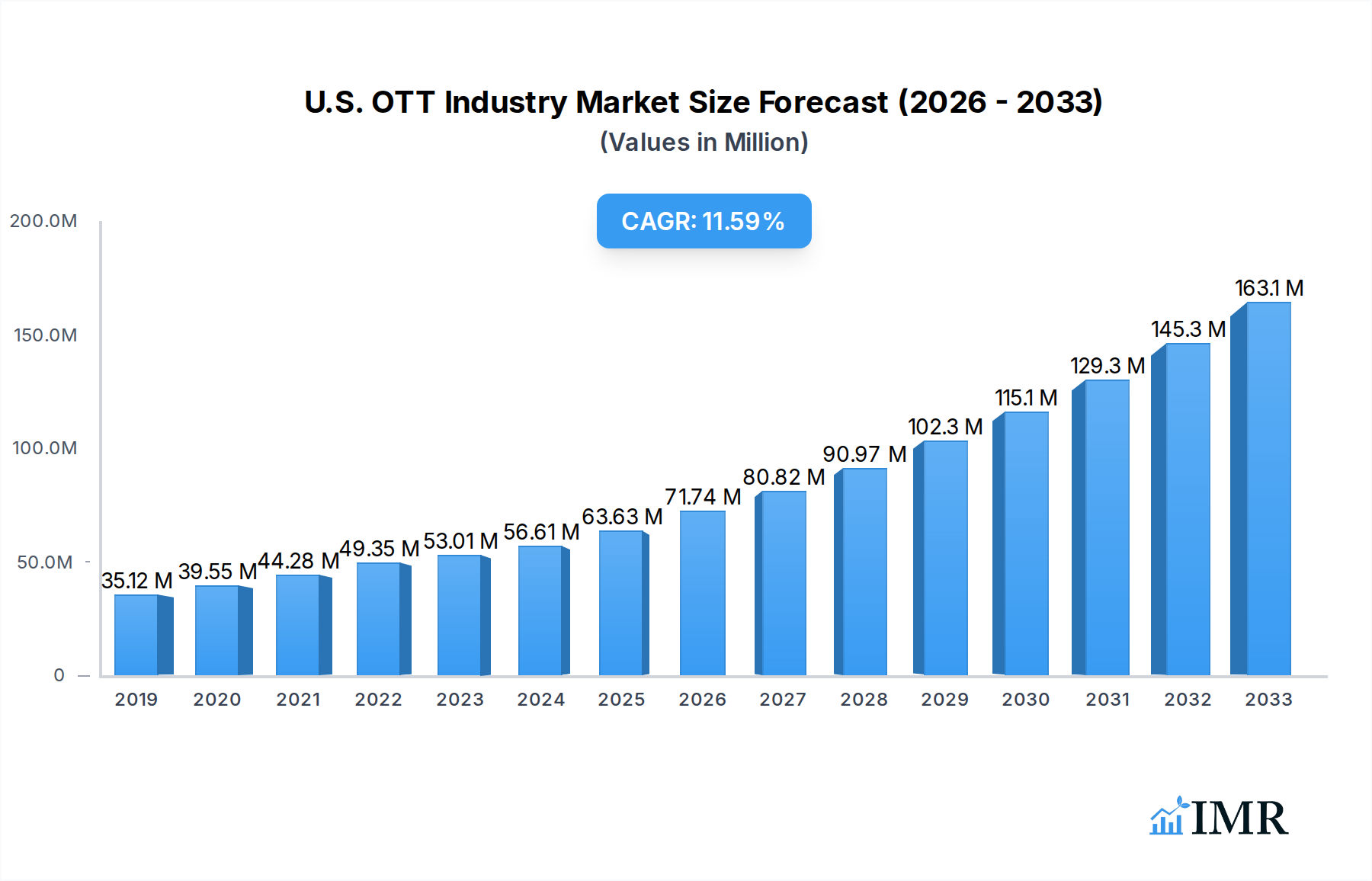

The U.S. Over-The-Top (OTT) industry is poised for substantial growth, projected to reach an impressive $56.61 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 12.56%. This robust expansion is fueled by several key drivers, including the increasing consumer demand for flexible and on-demand entertainment, the proliferation of smart devices enabling seamless streaming, and the continuous innovation in content creation and delivery by major players like Netflix, Disney+, and Amazon Prime Video. The shift from traditional linear television to digital streaming platforms is a defining trend, with consumers actively seeking personalized viewing experiences and diverse content libraries. This dynamic environment encourages constant investment in original programming and advanced technologies, further solidifying the OTT market's trajectory.

U.S. OTT Industry Market Size (In Million)

Despite the optimistic outlook, the U.S. OTT market is not without its challenges. Subscription fatigue, where consumers feel overwhelmed by the sheer number of streaming services and their associated costs, represents a significant restraint. The increasing competition among established giants and emerging players necessitates a strategic focus on differentiation through unique content offerings and competitive pricing models. Furthermore, the evolving regulatory landscape and the ongoing battle for content licensing rights can introduce complexities and potential disruptions. However, the inherent advantages of OTT, such as accessibility, affordability, and a vast array of choices, are expected to outweigh these restraints, propelling the market forward. The segmentation of the market into Subscription Video on Demand (SVoD), Transactional Video on Demand (TVoD), and Advertising Video on Demand (AVoD) reflects the diverse consumer preferences and monetization strategies within this vibrant ecosystem.

U.S. OTT Industry Company Market Share

U.S. OTT Industry Report: Market Size, Growth Forecast, and Key Trends (2019-2033)

This comprehensive report provides an in-depth analysis of the U.S. Over-The-Top (OTT) industry, encompassing market dynamics, growth trends, key players, and future outlook. With a study period spanning from 2019 to 2033, this research offers invaluable insights for industry professionals, investors, and stakeholders seeking to understand the evolving landscape of video streaming in the United States. The report focuses on critical segments such as SVoD (Subscription Video On Demand), TVoD (Transactional Video On Demand), and AVoD (Advertising-based Video On Demand), presenting all quantitative values in millions of units.

U.S. OTT Industry Market Dynamics & Structure

The U.S. OTT industry is characterized by dynamic market concentration, driven by rapid technological innovation and evolving consumer preferences. While the market exhibits high growth potential, it also faces increasing competitive pressures from both established giants and emerging players. Regulatory frameworks are continuously adapting to address issues of content moderation, data privacy, and fair competition, influencing market entry and operational strategies for companies like Netflix, Disney+, YouTube (Google LLC), Amazon Prime Video, and HBO Max (AT&T Inc). Technological innovation, particularly in areas like artificial intelligence for content recommendation and immersive viewing experiences, acts as a primary driver, pushing the boundaries of what OTT platforms can offer. Competitive product substitutes, including traditional linear television and other forms of digital entertainment, necessitate continuous innovation and strategic differentiation. End-user demographics are increasingly diverse, with a growing demand for personalized content, flexible subscription models, and multi-device accessibility. Mergers and acquisitions (M&A) trends highlight a consolidation phase, as companies aim to expand their content libraries, acquire new user bases, and strengthen their market positions. For instance, the acquisition of Animal Logic by Netflix underscores the strategic importance of securing intellectual property and expanding production capabilities.

- Market Concentration: A mix of large, established players and a long tail of niche providers, with increasing consolidation through M&A.

- Technological Innovation: AI-powered personalization, 4K/8K streaming, and interactive content are key development areas.

- Regulatory Frameworks: Evolving regulations around data privacy, content classification, and anti-trust concerns impact market operations.

- Competitive Product Substitutes: Traditional TV, gaming, and social media compete for consumer attention and subscription spending.

- End-User Demographics: Growing demand from younger demographics for on-demand content and flexibility, alongside an aging population seeking accessible interfaces.

- M&A Trends: Strategic acquisitions to gain content rights, technological capabilities, and market share.

U.S. OTT Industry Growth Trends & Insights

The U.S. OTT industry has witnessed unprecedented growth over the historical period of 2019-2024, driven by the widespread adoption of high-speed internet, the proliferation of smart devices, and a significant shift in consumer viewing habits. The convenience and vast content libraries offered by platforms such as Sling TV LLC, Disney+, YouTube, Netflix, CBS All Access (Viacomcbs Inc.), Roku, Amazon Prime Video, Apple Inc., and HBO Max have propelled market penetration to new heights. The base year of 2025 is anticipated to see the market continue its upward trajectory, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025-2033. This sustained growth is fueled by an increasing number of households subscribing to multiple OTT services, a trend known as "bundling" or "stacking," as consumers seek diverse content offerings across various genres and providers.

Technological disruptions have been pivotal, with advancements in streaming quality, such as 4K and HDR, enhancing the viewing experience and driving upgrades. Furthermore, the rise of AVoD services, offering free, ad-supported content, has broadened accessibility and attracted a new segment of price-sensitive consumers, complementing the established SVoD and TVoD models. Consumer behavior has fundamentally shifted, with a preference for on-demand viewing over scheduled programming. This has led to a surge in original content production by major players, creating a competitive content arms race. The integration of OTT services into smart TVs, gaming consoles, and mobile devices has further cemented their place in daily entertainment consumption. The market penetration in 2025 is estimated to reach XX million households, with this figure expected to grow to XX million by 2033. The average revenue per user (ARPU) is also projected to see a steady increase, driven by premium subscription tiers and the growing adoption of transactional video on demand for newer movie releases. The overall market size, estimated at $XX billion in 2025, is forecast to reach $XX billion by 2033, underscoring the immense economic significance of the U.S. OTT industry. The increasing affordability of streaming devices and the expansion of broadband infrastructure are expected to further accelerate adoption rates in underserved regions.

Dominant Regions, Countries, or Segments in U.S. OTT Industry

Within the dynamic U.S. OTT industry, the Subscription Video On Demand (SVoD) segment consistently emerges as the dominant force driving market growth. This dominance is attributed to a confluence of factors including deeply ingrained consumer habits, the widespread availability of high-quality original content, and the perceived value proposition of unlimited, ad-free viewing for a fixed monthly fee. Leading players such as Netflix, Disney+, Amazon Prime Video, and HBO Max have invested billions in exclusive programming, original series, and blockbuster movies, creating a strong competitive moat and fostering significant subscriber loyalty. The estimated market share of SVoD in the U.S. OTT landscape for 2025 stands at a commanding XX%, with projections indicating a continued stronghold through 2033.

The economic policies in the United States, characterized by robust consumer spending power and a high disposable income, have been instrumental in supporting the growth of SVoD services. Furthermore, the nation's advanced digital infrastructure, including widespread broadband internet penetration and the ubiquitous presence of smart devices, provides the essential foundation for seamless streaming experiences. The competitive landscape within SVoD is intense, with companies vying for subscriber attention through diverse content strategies. For example, Disney+ has leveraged its vast intellectual property from Marvel, Star Wars, and Pixar to attract families, while Netflix continues to diversify its offerings across genres and international markets. Amazon Prime Video benefits from its integration with the broader Amazon ecosystem, offering added value to Prime members.

While TVoD and AVoD segments are crucial components of the overall OTT ecosystem, SVoD’s predictable revenue streams and ability to cultivate deep subscriber relationships solidify its leading position. TVoD, though important for newer releases and niche content, faces competition from SVoD’s all-you-can-eat model. AVoD, while expanding rapidly and making content accessible to a wider audience, often struggles to command the same ARPU as premium SVoD tiers. The growth potential for SVoD remains substantial, driven by ongoing content innovation, international expansion, and the development of new monetization strategies, such as ad-supported premium tiers and bundled offerings with other entertainment services. The sheer scale of content libraries, coupled with effective marketing and user acquisition strategies, ensures SVoD's continued leadership in the foreseeable future.

- Dominant Segment: Subscription Video On Demand (SVoD)

- Key Drivers for SVoD Dominance:

- Content Libraries: Extensive original and licensed content from major studios.

- Consumer Habits: Established preference for on-demand, ad-free viewing.

- Economic Factors: High disposable income and consumer spending power in the U.S.

- Technological Infrastructure: Widespread broadband access and smart device penetration.

- Value Proposition: Perceived value of unlimited access for a fixed monthly fee.

- Market Share (Estimated 2025): SVoD: XX%

- Growth Potential: Continued expansion through content diversification, strategic partnerships, and evolving monetization models.

U.S. OTT Industry Product Landscape

The U.S. OTT industry's product landscape is defined by a relentless pursuit of innovative streaming experiences and diverse content delivery models. Platforms are continuously enhancing their user interfaces for intuitive navigation and personalized content discovery through advanced AI algorithms. Key product innovations include the widespread adoption of 4K Ultra HD and High Dynamic Range (HDR) streaming, delivering unparalleled visual fidelity. Many services are also experimenting with interactive content, offering viewers greater engagement opportunities. The performance metrics for these products are largely measured by subscriber acquisition and retention rates, average viewing hours per user, and content engagement levels. Unique selling propositions often revolve around exclusive original series, vast movie libraries, and unique user experience features, setting companies like Apple Inc. and CBS All Access apart in a crowded market. Technological advancements are also focused on optimizing streaming quality across varying network conditions and expanding device compatibility, ensuring accessibility on smart TVs, mobile devices, and gaming consoles.

Key Drivers, Barriers & Challenges in U.S. OTT Industry

Key Drivers: The U.S. OTT industry is propelled by several key drivers, including the ever-increasing demand for on-demand content, the ubiquitous availability of high-speed internet and smart devices, and the continuous innovation in content creation and distribution. The shift in consumer behavior towards personalized and flexible entertainment consumption further fuels this growth. Technological advancements, such as 5G deployment and improved streaming codecs, are also crucial catalysts.

Barriers & Challenges: Despite its robust growth, the industry faces significant barriers and challenges. Market saturation and intense competition lead to high customer acquisition costs and subscriber churn. The increasing cost of content production and licensing presents a major financial strain. Regulatory scrutiny, particularly concerning data privacy and content moderation, poses ongoing hurdles. Supply chain issues, though less direct than in physical goods, can impact the availability of specialized streaming hardware and related infrastructure components. Furthermore, the increasing number of subscription services leads to "subscription fatigue" among consumers, creating a barrier to entry for new services and a retention challenge for existing ones. The estimated impact of these challenges on market growth is significant, potentially reducing the projected CAGR by XX% if not effectively managed.

Emerging Opportunities in U.S. OTT Industry

Emerging opportunities within the U.S. OTT industry lie in the burgeoning AVoD segment, driven by a growing segment of price-sensitive consumers and advertisers seeking targeted reach. The expansion of interactive content formats, including shoppable videos and live commerce integration, presents a novel monetization avenue. Furthermore, the untapped potential of niche content streaming services catering to specific demographics or interests (e.g., educational, wellness, esports) offers a pathway for differentiation and growth. The increasing adoption of 8K streaming and augmented reality (AR) enhanced viewing experiences represents a future frontier for immersive entertainment, creating new product development opportunities.

Growth Accelerators in the U.S. OTT Industry Industry

Several factors are acting as significant growth accelerators for the U.S. OTT industry. The strategic bundling of services, often through partnerships with telecommunication providers and other entertainment platforms, is increasing subscriber acquisition and reducing churn. Continued investment in high-quality, original content remains a primary accelerator, drawing in new subscribers and retaining existing ones. The ongoing expansion of broadband infrastructure, especially in rural and underserved areas, opens up new markets for OTT services. Furthermore, technological advancements in streaming technology, such as improved compression algorithms and adaptive bitrate streaming, enhance the viewing experience and drive wider adoption across various devices and network conditions, thereby accelerating overall market penetration.

Key Players Shaping the U.S. OTT Industry Market

- Sling TV L L C

- Disney+

- YouTube (Google LLC)

- Netflix

- CBS All Acess (Viacomcbs Inc )

- Roku

- Amazon Prime Video

- Apple Inc

- HBO Max (AT&T Inc )

Notable Milestones in U.S. OTT Industry Sector

- Jul 2022: Netflix acquired Animal Logic, the world's leading independent animation studio. This acquisition is expected to speed up Netflix's development of end-to-end animation production abilities. Netflix Animation and Animal Logic together are anticipated to form a worldwide creative production team as well as an animation studio that will create some of Netflix's most popular animated feature titles.

- Apr 2022: Roku and Amazon extended their distribution arrangement for some more years. The agreement allows the customers to continue using Roku devices to access the Prime Video and IMDb TV applications.

In-Depth U.S. OTT Industry Market Outlook

The future outlook for the U.S. OTT industry is exceptionally promising, with growth accelerators poised to further expand its market potential. The ongoing evolution of content creation, including the integration of AI in storytelling and the rise of interactive narratives, will captivate audiences and drive engagement. Strategic partnerships between content providers, device manufacturers, and telecommunication companies will continue to unlock new distribution channels and revenue streams. The increasing focus on personalization and niche content will allow for deeper market penetration and cater to a wider array of consumer preferences. As broadband speeds increase and new technologies like immersive audio and advanced VR/AR experiences mature, the OTT landscape is set to transform into an even more dynamic and engaging entertainment ecosystem, promising sustained growth and significant opportunities for innovation and investment.

U.S. OTT Industry Segmentation

-

1. Type

- 1.1. SVoD

- 1.2. TVoD

- 1.3. AVoD

U.S. OTT Industry Segmentation By Geography

- 1. U.S.

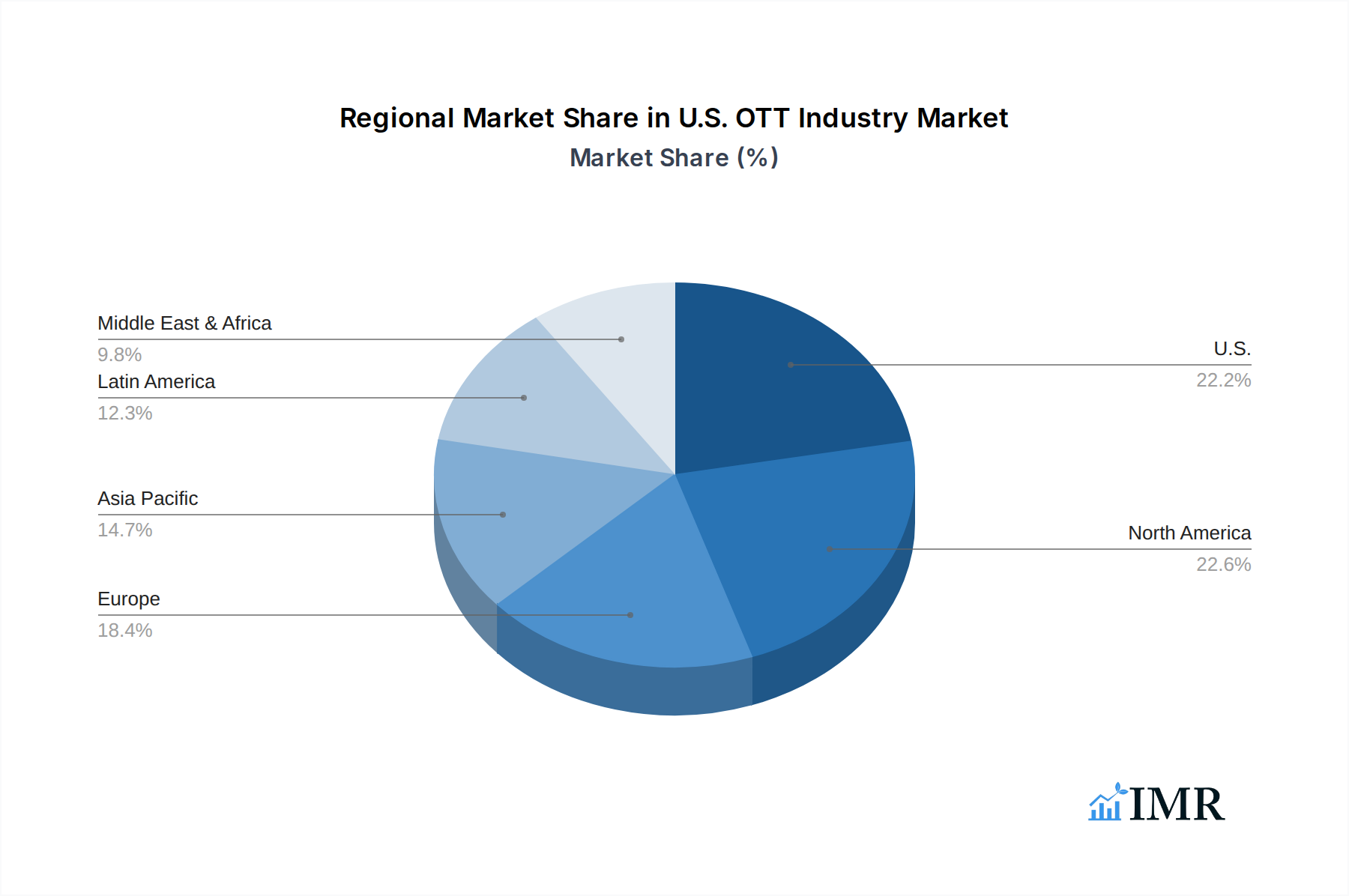

U.S. OTT Industry Regional Market Share

Geographic Coverage of U.S. OTT Industry

U.S. OTT Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. SVoD

- 5.1.2. TVoD

- 5.1.3. AVoD

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. U.S.

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. U.S. OTT Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. SVoD

- 6.1.2. TVoD

- 6.1.3. AVoD

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sling TV L L C

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Disney+

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 YouTube (Google LLC)*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Netflix

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 CBS All Acess (Viacomcbs Inc )

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Roku

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Amazon Prime Video

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Apple Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 HBO Max (AT&T Inc )

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Sling TV L L C

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: U.S. OTT Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: U.S. OTT Industry Share (%) by Company 2025

List of Tables

- Table 1: U.S. OTT Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: U.S. OTT Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: U.S. OTT Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: U.S. OTT Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the U.S. OTT Industry?

The projected CAGR is approximately 12.56%.

2. Which companies are prominent players in the U.S. OTT Industry?

Key companies in the market include Sling TV L L C, Disney+, YouTube (Google LLC)*List Not Exhaustive, Netflix, CBS All Acess (Viacomcbs Inc ), Roku, Amazon Prime Video, Apple Inc, HBO Max (AT&T Inc ).

3. What are the main segments of the U.S. OTT Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 56.61 Million as of 2022.

5. What are some drivers contributing to market growth?

High Penetration of Smart TV and the Presence of Major OTT Providers have Contributed to the Growth of OTT Adoption in the Region; Market Consolidation to Result in Emphasis on Collaboration and Partnerships.

6. What are the notable trends driving market growth?

High Penetration of Smart TV Witnesses a Significant Growth.

7. Are there any restraints impacting market growth?

Growing Threat of Video Content Piracy and Security Threat of User Database Due to Spyware.

8. Can you provide examples of recent developments in the market?

Jul 2022: Netflix acquired Animal Logic, the world's leading independent animation studio. This acquisition is expected to speed up Netflix's development of end-to-end animation production abilities. Netflix Animation and Animal Logic together are anticipated to form a worldwide creative production team as well as an animation studio that will create some of Netflix's most popular animated feature titles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "U.S. OTT Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the U.S. OTT Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the U.S. OTT Industry?

To stay informed about further developments, trends, and reports in the U.S. OTT Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence