Key Insights

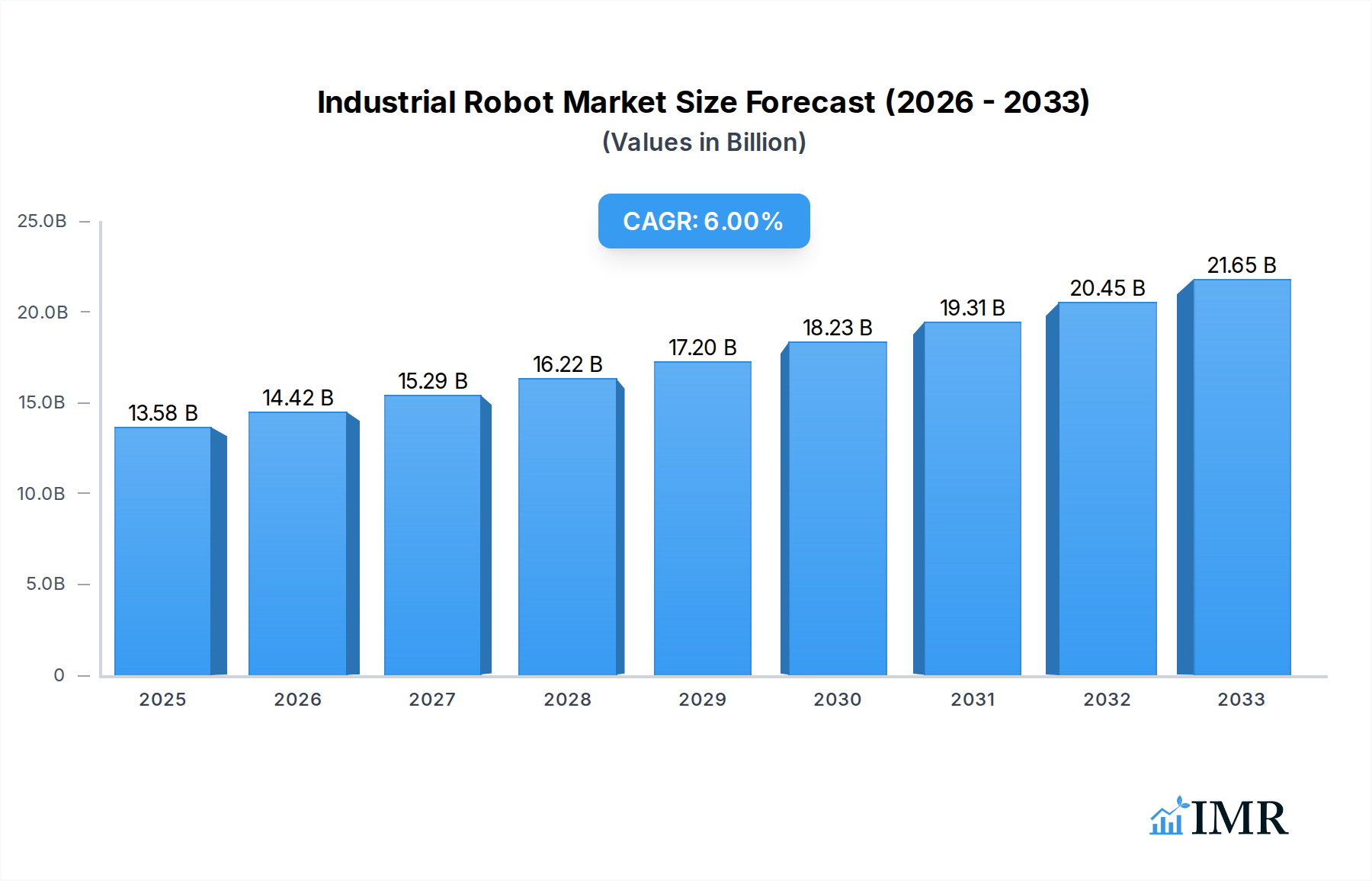

The global Industrial Robot market is poised for significant expansion, projected to reach $13,580 million by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 6.2% throughout the forecast period of 2025-2033. This substantial growth is primarily fueled by the increasing demand for automation across diverse manufacturing sectors, driven by the imperative to enhance productivity, improve product quality, and address labor shortages. The automotive industry continues to be a leading adopter, leveraging robots for complex assembly, welding, and painting tasks. Simultaneously, the electrical and electronics sector is witnessing a surge in robotic integration for intricate and high-precision manufacturing processes. Furthermore, the chemical, rubber, and plastic industries are increasingly recognizing the benefits of robotic automation in handling hazardous materials and optimizing production lines. The expanding adoption of articulated robots, known for their versatility, and SCARA robots, valued for their speed and precision in planar movements, underscores the market's trajectory towards more sophisticated and specialized robotic solutions.

Industrial Robot Market Size (In Billion)

The market landscape is characterized by intense competition among established players and emerging innovators, fostering continuous advancements in robotic technology. Innovations in collaborative robots (cobots), designed to work alongside human operators, are opening new avenues for automation in smaller enterprises and intricate assembly tasks. The focus on developing smarter, more adaptable, and user-friendly robotic systems, coupled with advancements in AI and machine learning for enhanced decision-making capabilities, will further accelerate market penetration. Key restraints, such as the high initial investment costs and the need for skilled personnel for programming and maintenance, are gradually being mitigated by the development of more cost-effective solutions and the increasing availability of training programs. The growth is expected to be particularly strong in the Asia Pacific region, driven by China's dominant manufacturing ecosystem and the rapid industrialization of other Asian nations, followed by Europe and North America, which are actively pursuing Industry 4.0 initiatives.

Industrial Robot Company Market Share

Industrial Robot Market Report: Navigating Automation's Next Frontier (2019-2033)

This comprehensive report delves into the dynamic industrial robot market, forecasting growth from 2025 to 2033. We analyze key automation trends, robotics adoption, and the burgeoning demand for collaborative robots and cobots. With a deep dive into the parent market of manufacturing automation and the child market of specialized robotic solutions, this study equips industry professionals with critical insights into market size, segmentation, and future trajectories.

Industrial Robot Market Dynamics & Structure

The global industrial robot market exhibits a moderately consolidated structure, with leading players like FANUC, KUKA, ABB, and Yaskawa (Motoman) holding significant market share. This concentration is driven by high capital investment, proprietary technology, and established distribution networks. Technological innovation remains a primary driver, fueled by advancements in AI, machine learning for predictive maintenance, and enhanced sensor technologies that enable robots to perform more complex tasks with greater precision. Regulatory frameworks, particularly concerning safety standards and data privacy, are evolving and can influence market entry and product development. Competitive product substitutes include advancements in semi-automation and the increasing sophistication of non-robotic machinery. End-user demographics are shifting towards embracing automation across a wider spectrum of industries, from traditional manufacturing to emerging sectors. Merger and acquisition (M&A) trends are observable as larger players seek to consolidate market position and acquire innovative technologies. For instance, recent M&A activities indicate a strategic focus on acquiring expertise in AI-driven robotics and software integration.

- Market Concentration: Dominated by a few key global players, with emerging regional contenders gaining traction.

- Technological Innovation Drivers: AI integration, enhanced vision systems, IoT connectivity, and human-robot collaboration advancements.

- Regulatory Frameworks: Increasing focus on safety, interoperability standards, and ethical AI deployment.

- Competitive Product Substitutes: Sophisticated automation software, advanced tooling, and improved manual assembly processes.

- End-User Demographics: Growing adoption in SMEs, driven by cost-effectiveness and flexibility of newer robotic solutions.

- M&A Trends: Strategic acquisitions for technology integration, market expansion, and portfolio diversification. Estimated M&A deal volume in the last two years: 12.xx million units.

Industrial Robot Growth Trends & Insights

The industrial robot market is projected for robust growth, driven by increasing factory automation initiatives and the pursuit of enhanced productivity and efficiency. The market size is expected to expand significantly, with adoption rates accelerating across diverse manufacturing sectors. Technological disruptions, such as the rise of AI-powered robots capable of learning and adapting, are reshaping operational paradigms. Consumer behavior shifts, including the demand for customized products and faster delivery times, further necessitate the flexibility and speed offered by industrial robots. The cobot market, a significant segment within industrial robotics, is experiencing particularly rapid expansion due to its ease of integration, collaborative nature, and lower initial investment compared to traditional industrial robots.

The global industrial robot market is anticipated to witness a Compound Annual Growth Rate (CAGR) of approximately 12.xx% between 2025 and 2033. This growth trajectory is underpinned by several critical factors:

- Increasing Demand for Automation: Manufacturers worldwide are investing heavily in automation to offset labor shortages, improve product quality, and reduce operational costs. This is particularly evident in regions with rising labor wages and aging workforces.

- Technological Advancements: The continuous evolution of robotics technology, including improved dexterity, enhanced sensing capabilities, and greater AI integration, is expanding the application scope of industrial robots into more complex and previously inaccessible tasks. This includes advancements in machine vision for quality control and adaptive path planning.

- Growth of the Collaborative Robot (Cobot) Segment: Cobots are democratizing automation, making it accessible to small and medium-sized enterprises (SMEs) due to their ease of programming, inherent safety features for human interaction, and lower price points. This segment is expected to outpace the growth of traditional industrial robots.

- Industry 4.0 and Smart Manufacturing Initiatives: The widespread adoption of Industry 4.0 principles, focusing on interconnectedness, data analytics, and intelligent automation, is a major catalyst for industrial robot deployment. Robots are integral to building smart factories that are more efficient, flexible, and data-driven.

- Shift Towards Reshoring and Nearshoring: Geopolitical shifts and supply chain vulnerabilities have prompted many companies to reconsider their manufacturing footprints. Industrial robots play a crucial role in making domestic manufacturing competitive by improving efficiency and reducing reliance on global labor markets.

- Expansion into New Application Areas: Beyond traditional automotive and electronics manufacturing, industrial robots are finding increasing applications in sectors like food and beverage, pharmaceuticals, logistics, and even agriculture, driven by the need for precision, hygiene, and efficiency.

- Government Support and Incentives: Many governments are actively promoting industrial automation through subsidies, tax incentives, and research grants, further accelerating market adoption.

The estimated market penetration of industrial robots in developed economies is already significant, with emerging economies showing substantial growth potential as they invest in modernizing their manufacturing infrastructure. Consumer behavior is also indirectly influencing the market, as the demand for personalized products and faster fulfillment necessitates more agile and automated production lines. The robotics as a service (RaaS) model is also emerging as a growth accelerator, lowering the barrier to entry for businesses looking to leverage automation without significant upfront capital expenditure. The industrial automation market as a whole is witnessing this transformative wave, with robots at its core.

Dominant Regions, Countries, or Segments in Industrial Robot

The Electrical and Electronics segment is a dominant force driving growth within the industrial robot market. This sector's insatiable demand for precision, speed, and high-volume production for components like semiconductors, printed circuit boards, and consumer electronics makes it a prime adopter of robotic solutions. The intricate assembly processes and the need for minimal human intervention to ensure purity and accuracy in semiconductor manufacturing, for example, highlight the indispensable role of industrial robots. Furthermore, the rapid pace of technological innovation in the electronics industry necessitates flexible automation that can be quickly reconfigured for new product lines.

Key Drivers for Dominance:

- High-Value Production and Miniaturization: The production of intricate electronic components requires extremely precise and repeatable movements, which industrial robots excel at.

- Labor Intensity and Skill Shortages: The high labor requirements for electronics assembly, coupled with global skill shortages in specialized manufacturing roles, push manufacturers towards automation.

- Quality Control and Defect Reduction: Robots equipped with advanced vision systems can perform meticulous quality inspections, significantly reducing defect rates and ensuring product reliability.

- Fast Product Lifecycles: The rapid evolution of electronic devices demands agile manufacturing processes. Robots can be reprogrammed and redeployed quickly to accommodate new product designs and variations, supporting shorter product lifecycles.

- Safety and Ergonomics: Automation of hazardous or ergonomically challenging tasks, such as handling delicate components or repetitive assembly, improves worker safety and well-being.

Within this segment, Articulated Robots and SCARA Robots are particularly prevalent. Articulated robots, with their multi-axis capabilities, are ideal for complex assembly, welding, and material handling tasks. SCARA robots, known for their speed and precision in the X-Y plane, are widely used for pick-and-place operations and light assembly tasks common in electronics manufacturing.

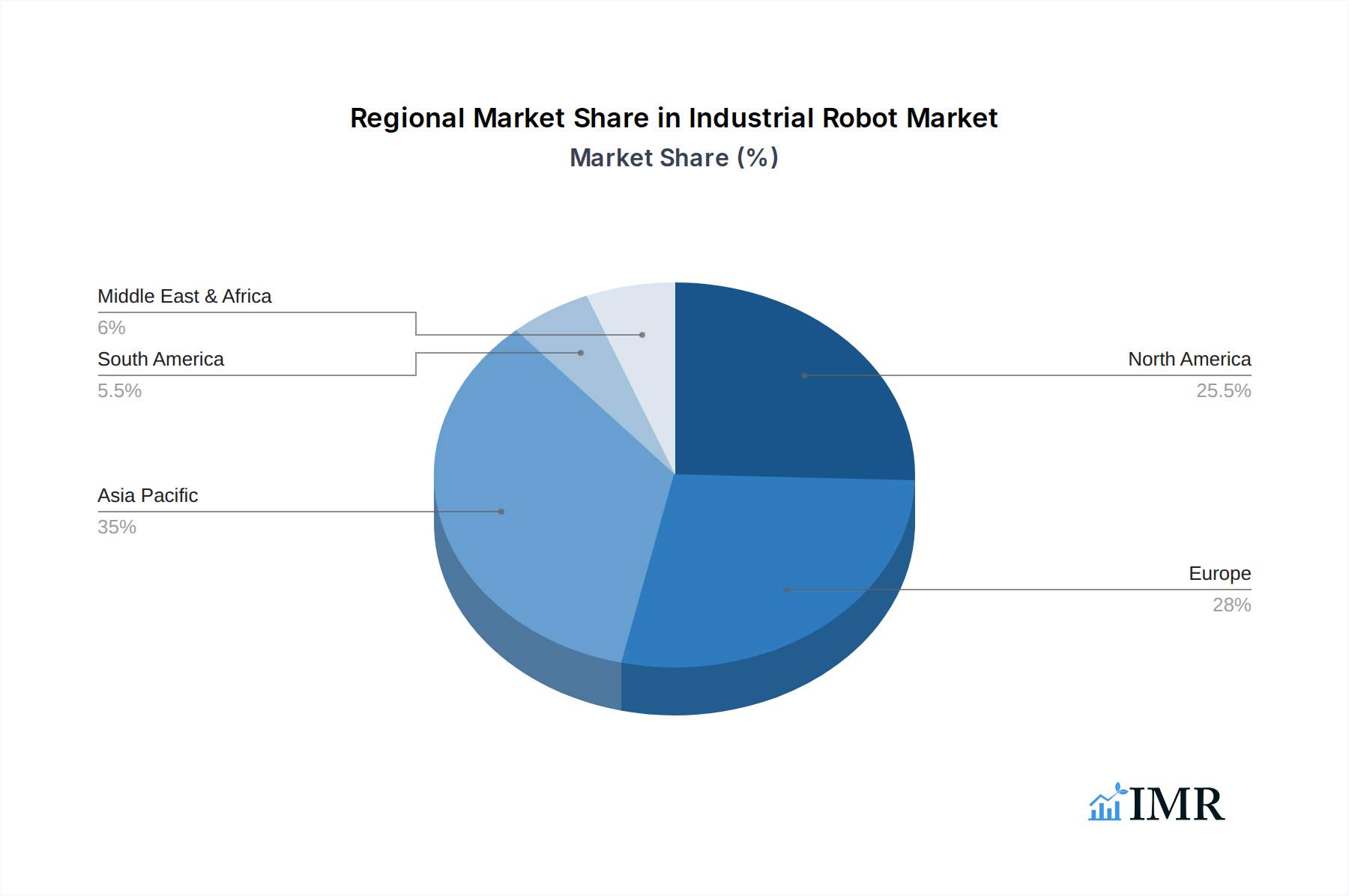

Regional Dominance: Asia-Pacific, particularly China, stands out as a dominant region in the industrial robot market. This leadership is propelled by its status as a global manufacturing hub for electronics and a strong push from the Chinese government to develop its domestic robotics industry through initiatives like "Made in China 2025." The sheer scale of manufacturing operations and the increasing adoption of advanced automation technologies in countries like South Korea and Japan further solidify Asia-Pacific's leading position. The region's substantial market share, estimated at over 50%, is attributed to a combination of factors including a large manufacturing base, supportive government policies, and a growing focus on smart manufacturing.

- Electrical and Electronics Segment: Dominant due to demand for precision, high volume, and rapid product cycles.

- Dominant Robot Types: Articulated Robots (for complex tasks) and SCARA Robots (for pick-and-place).

- Leading Region: Asia-Pacific, driven by China's manufacturing prowess and government support for automation.

- Key Drivers in Asia-Pacific: Large manufacturing base, government incentives, growing adoption of Industry 4.0, and cost-competitiveness.

- Market Share within Asia-Pacific: Estimated at 50.xx% of the global industrial robot market.

- Growth Potential: Significant untapped potential in emerging economies within the region.

Industrial Robot Product Landscape

The industrial robot product landscape is characterized by continuous innovation, with a focus on enhanced dexterity, improved human-robot collaboration, and greater intelligence. Newer models boast higher payloads, increased reach, and more sophisticated end-of-arm tooling, expanding their applicability in the Metal and Machinery and Automotive sectors for tasks like heavy-duty welding and intricate assembly. The integration of advanced AI and machine learning capabilities allows robots to perform adaptive tasks, optimize movements in real-time, and even predict potential maintenance needs. For instance, the development of robots with improved force sensing enables them to handle delicate materials with precision, opening new avenues in the Food, Beverages, and Pharmaceuticals industry for tasks requiring aseptic handling. The performance metrics are consistently being pushed with faster cycle times, increased accuracy (down to xx microns), and enhanced energy efficiency becoming standard expectations.

Key Drivers, Barriers & Challenges in Industrial Robot

Key Drivers:

- Increased Demand for Automation: Driven by labor shortages, rising wages, and the need for enhanced productivity and quality across industries.

- Technological Advancements: AI, IoT integration, advanced sensors, and collaborative robotics (cobots) are expanding capabilities and lowering adoption barriers.

- Industry 4.0 Adoption: The push for smart manufacturing and connected factories necessitates sophisticated robotic solutions.

- Government Initiatives: Supportive policies, subsidies, and R&D funding in many countries are accelerating market growth.

- Cost Reduction: Falling robot prices and the rise of RaaS models make automation more accessible.

Barriers & Challenges:

- High Initial Investment: Despite falling prices, the upfront cost can still be a hurdle for some SMEs.

- Integration Complexity: Integrating robots into existing factory infrastructure and IT systems can be complex and require specialized expertise.

- Skill Gap: A shortage of skilled personnel to program, operate, and maintain robotic systems.

- Cybersecurity Threats: The increasing connectivity of robots raises concerns about data security and potential cyberattacks.

- Regulatory Hurdles: Evolving safety standards and compliance requirements can create challenges.

- Supply Chain Disruptions: Global supply chain issues can impact the availability of components and lead to longer lead times. Estimated impact: 15.xx% increase in lead times for critical components.

- Resistance to Change: Cultural and organizational resistance to adopting new technologies can slow down implementation.

Emerging Opportunities in Industrial Robot

Emerging opportunities in the industrial robot market lie in the expansion into new application domains and the development of more specialized robotic solutions. The Food, Beverages, and Pharmaceuticals sector presents a significant growth area, driven by the need for enhanced hygiene, precision in packaging and palletizing, and the ability to handle delicate products. The burgeoning e-commerce industry also fuels demand for advanced robotics in logistics and warehousing for automated order picking, sorting, and inventory management. Furthermore, the development of AI-powered robots capable of autonomous decision-making and adaptable learning is opening doors for applications in unpredictable environments, such as agriculture and construction. The increasing focus on sustainability is also creating opportunities for robots that can optimize energy consumption and reduce waste in manufacturing processes.

Growth Accelerators in the Industrial Robot Industry

Several catalysts are accelerating growth in the industrial robot industry. The continuous miniaturization and improved efficiency of robotic components are making robots more versatile and cost-effective. Strategic partnerships between robot manufacturers and software developers are leading to the creation of integrated automation solutions that offer enhanced functionality and ease of use. Market expansion strategies, including the targeting of SMEs with flexible RaaS models and tailored solutions, are broadening the customer base. Furthermore, breakthroughs in areas like advanced gripping technologies and intuitive programming interfaces are significantly reducing the barriers to entry, enabling a wider range of businesses to leverage the benefits of industrial automation. The increasing focus on data analytics and AI integration within robotic systems is also a key growth accelerator, enabling predictive maintenance and optimizing production processes.

Key Players Shaping the Industrial Robot Market

- FANUC

- KUKA

- ABB

- Yaskawa (Motoman)

- Nachi

- Kawasaki Robotics

- Comau

- EPSON Robots

- Staubli

- Omron (Adept)

- DENSO Robotics

- OTC Daihen

- Panasonic

- Shibaura Machine

- Mitsubishi Electric

- Yamaha

- Universal Robots

- Hyundai Robotics

- Robostar

- Star Seiki

- JEL Corporation

- Techman

- Siasun

- EFORT Intelligent Equipment

- Estun Automation

- STEP Electric Corporation

- Guangdong Topstar Technology

- Inovance Group

- Nidec (Genmark Automation)

- Hirata

- Brooks Automation

- RORZE Corporation

- Tianji Intelligent System

- Delta Group

- Chengdu CRP Robot Technology

- AUBO Robotics

- Huashu Robot Co.,Ltd.

- Zhejiang Qianjiang Robot

- Peitian Robotics

- Shanghai TURIN Chi Robot

- Chenxing (Tianjin) Automation Equipment Co.,Ltd.

- QKM Technology

- Guangzhou CNC Equipment

- Robotphoenix LLC

- warsonco Corporation

- Sanwa Engineering Corporation

- Bekannter Robot Technology

- ROKAE

Notable Milestones in Industrial Robot Sector

- 2019: Increased adoption of collaborative robots (cobots) in SMEs, offering safer human-robot interaction.

- 2020: Significant surge in automation demand driven by supply chain disruptions and the need for resilient manufacturing.

- 2021: Advancements in AI and machine learning leading to more intelligent and adaptive robotic systems.

- 2022: Growth of Robotics as a Service (RaaS) models, lowering upfront costs and increasing accessibility.

- 2023: Expansion of industrial robots into new sectors like food & beverage and pharmaceuticals due to hygiene and precision requirements.

- 2024: Enhanced focus on robot mobility and autonomous navigation in warehousing and logistics applications.

- 2025 (Estimated): Widespread integration of advanced vision systems for complex quality control and inspection tasks.

In-Depth Industrial Robot Market Outlook

The industrial robot market is poised for sustained and accelerated growth, driven by an ever-increasing demand for automation across global manufacturing landscapes. The strategic integration of AI, enhanced sensor technologies, and the burgeoning acceptance of collaborative robotics will continue to expand the application scope of robots into more complex and sensitive tasks. Emerging markets present significant untapped potential, while developed economies will continue to invest in upgrading existing automation infrastructure. The shift towards smart manufacturing and Industry 4.0 principles will further solidify the pivotal role of industrial robots in creating efficient, agile, and competitive production environments. The market's outlook is exceptionally positive, with continuous innovation and strategic market expansion paving the way for a future where robots are integral to virtually every facet of industrial production, aiming for a market size of over 120 million units by 2033.

Industrial Robot Segmentation

-

1. Application

- 1.1. Automotive

- 1.2. Electrical and Electronics

- 1.3. Chemical, Rubber and Plastic

- 1.4. Metal and Machinery

- 1.5. Food, Beverages and Pharmaceuticals

- 1.6. Others

-

2. Types

- 2.1. Articulated Robots

- 2.2. Parallel Robots

- 2.3. SCARA Robots

- 2.4. Cylindrical Robots

- 2.5. Cartesian Robots

Industrial Robot Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Industrial Robot Regional Market Share

Geographic Coverage of Industrial Robot

Industrial Robot REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Industrial Robot Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive

- 5.1.2. Electrical and Electronics

- 5.1.3. Chemical, Rubber and Plastic

- 5.1.4. Metal and Machinery

- 5.1.5. Food, Beverages and Pharmaceuticals

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Articulated Robots

- 5.2.2. Parallel Robots

- 5.2.3. SCARA Robots

- 5.2.4. Cylindrical Robots

- 5.2.5. Cartesian Robots

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Industrial Robot Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive

- 6.1.2. Electrical and Electronics

- 6.1.3. Chemical, Rubber and Plastic

- 6.1.4. Metal and Machinery

- 6.1.5. Food, Beverages and Pharmaceuticals

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Articulated Robots

- 6.2.2. Parallel Robots

- 6.2.3. SCARA Robots

- 6.2.4. Cylindrical Robots

- 6.2.5. Cartesian Robots

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Industrial Robot Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive

- 7.1.2. Electrical and Electronics

- 7.1.3. Chemical, Rubber and Plastic

- 7.1.4. Metal and Machinery

- 7.1.5. Food, Beverages and Pharmaceuticals

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Articulated Robots

- 7.2.2. Parallel Robots

- 7.2.3. SCARA Robots

- 7.2.4. Cylindrical Robots

- 7.2.5. Cartesian Robots

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Industrial Robot Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive

- 8.1.2. Electrical and Electronics

- 8.1.3. Chemical, Rubber and Plastic

- 8.1.4. Metal and Machinery

- 8.1.5. Food, Beverages and Pharmaceuticals

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Articulated Robots

- 8.2.2. Parallel Robots

- 8.2.3. SCARA Robots

- 8.2.4. Cylindrical Robots

- 8.2.5. Cartesian Robots

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Industrial Robot Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive

- 9.1.2. Electrical and Electronics

- 9.1.3. Chemical, Rubber and Plastic

- 9.1.4. Metal and Machinery

- 9.1.5. Food, Beverages and Pharmaceuticals

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Articulated Robots

- 9.2.2. Parallel Robots

- 9.2.3. SCARA Robots

- 9.2.4. Cylindrical Robots

- 9.2.5. Cartesian Robots

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Industrial Robot Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive

- 10.1.2. Electrical and Electronics

- 10.1.3. Chemical, Rubber and Plastic

- 10.1.4. Metal and Machinery

- 10.1.5. Food, Beverages and Pharmaceuticals

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Articulated Robots

- 10.2.2. Parallel Robots

- 10.2.3. SCARA Robots

- 10.2.4. Cylindrical Robots

- 10.2.5. Cartesian Robots

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 FANUC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 KUKA

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ABB

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Yaskawa (Motoman)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Nachi

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Kawasaki Robotics

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Comau

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 EPSON Robots

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Staubli

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Omron (Adept)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 DENSO Robotics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 OTC Daihen

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Panasonic

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shibaura Machine

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Mitsubishi Electric

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Yamaha

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Universal Robots

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Hyundai Robotics

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Robostar

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Star Seiki

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 JEL Corporation

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Techman

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Siasun

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 EFORT Intelligent Equipment

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Estun Automation

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 STEP Electric Corporation

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Guangdong Topstar Technology

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 Inovance Group

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 Nidec (Genmark Automation)

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Hirata

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 Brooks Automation

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.32 RORZE Corporation

- 11.2.32.1. Overview

- 11.2.32.2. Products

- 11.2.32.3. SWOT Analysis

- 11.2.32.4. Recent Developments

- 11.2.32.5. Financials (Based on Availability)

- 11.2.33 Tianji Intelligent System

- 11.2.33.1. Overview

- 11.2.33.2. Products

- 11.2.33.3. SWOT Analysis

- 11.2.33.4. Recent Developments

- 11.2.33.5. Financials (Based on Availability)

- 11.2.34 Delta Group

- 11.2.34.1. Overview

- 11.2.34.2. Products

- 11.2.34.3. SWOT Analysis

- 11.2.34.4. Recent Developments

- 11.2.34.5. Financials (Based on Availability)

- 11.2.35 Chengdu CRP Robot Technology

- 11.2.35.1. Overview

- 11.2.35.2. Products

- 11.2.35.3. SWOT Analysis

- 11.2.35.4. Recent Developments

- 11.2.35.5. Financials (Based on Availability)

- 11.2.36 AUBO Robotics

- 11.2.36.1. Overview

- 11.2.36.2. Products

- 11.2.36.3. SWOT Analysis

- 11.2.36.4. Recent Developments

- 11.2.36.5. Financials (Based on Availability)

- 11.2.37 Huashu Robot Co.

- 11.2.37.1. Overview

- 11.2.37.2. Products

- 11.2.37.3. SWOT Analysis

- 11.2.37.4. Recent Developments

- 11.2.37.5. Financials (Based on Availability)

- 11.2.38 Ltd.

- 11.2.38.1. Overview

- 11.2.38.2. Products

- 11.2.38.3. SWOT Analysis

- 11.2.38.4. Recent Developments

- 11.2.38.5. Financials (Based on Availability)

- 11.2.39 Zhejiang Qianjiang Robot

- 11.2.39.1. Overview

- 11.2.39.2. Products

- 11.2.39.3. SWOT Analysis

- 11.2.39.4. Recent Developments

- 11.2.39.5. Financials (Based on Availability)

- 11.2.40 Peitian Robotics

- 11.2.40.1. Overview

- 11.2.40.2. Products

- 11.2.40.3. SWOT Analysis

- 11.2.40.4. Recent Developments

- 11.2.40.5. Financials (Based on Availability)

- 11.2.41 Shanghai TURIN Chi Robot

- 11.2.41.1. Overview

- 11.2.41.2. Products

- 11.2.41.3. SWOT Analysis

- 11.2.41.4. Recent Developments

- 11.2.41.5. Financials (Based on Availability)

- 11.2.42 Chenxing (Tianjin) Automation Equipment Co.

- 11.2.42.1. Overview

- 11.2.42.2. Products

- 11.2.42.3. SWOT Analysis

- 11.2.42.4. Recent Developments

- 11.2.42.5. Financials (Based on Availability)

- 11.2.43 Ltd.

- 11.2.43.1. Overview

- 11.2.43.2. Products

- 11.2.43.3. SWOT Analysis

- 11.2.43.4. Recent Developments

- 11.2.43.5. Financials (Based on Availability)

- 11.2.44 QKM Technology

- 11.2.44.1. Overview

- 11.2.44.2. Products

- 11.2.44.3. SWOT Analysis

- 11.2.44.4. Recent Developments

- 11.2.44.5. Financials (Based on Availability)

- 11.2.45 Guangzhou CNC Equipment

- 11.2.45.1. Overview

- 11.2.45.2. Products

- 11.2.45.3. SWOT Analysis

- 11.2.45.4. Recent Developments

- 11.2.45.5. Financials (Based on Availability)

- 11.2.46 Robotphoenix LLC

- 11.2.46.1. Overview

- 11.2.46.2. Products

- 11.2.46.3. SWOT Analysis

- 11.2.46.4. Recent Developments

- 11.2.46.5. Financials (Based on Availability)

- 11.2.47 warsonco Corporation

- 11.2.47.1. Overview

- 11.2.47.2. Products

- 11.2.47.3. SWOT Analysis

- 11.2.47.4. Recent Developments

- 11.2.47.5. Financials (Based on Availability)

- 11.2.48 Sanwa Engineering Corporation

- 11.2.48.1. Overview

- 11.2.48.2. Products

- 11.2.48.3. SWOT Analysis

- 11.2.48.4. Recent Developments

- 11.2.48.5. Financials (Based on Availability)

- 11.2.49 Bekannter Robot Technology

- 11.2.49.1. Overview

- 11.2.49.2. Products

- 11.2.49.3. SWOT Analysis

- 11.2.49.4. Recent Developments

- 11.2.49.5. Financials (Based on Availability)

- 11.2.50 ROKAE

- 11.2.50.1. Overview

- 11.2.50.2. Products

- 11.2.50.3. SWOT Analysis

- 11.2.50.4. Recent Developments

- 11.2.50.5. Financials (Based on Availability)

- 11.2.1 FANUC

List of Figures

- Figure 1: Global Industrial Robot Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Industrial Robot Revenue (million), by Application 2025 & 2033

- Figure 3: North America Industrial Robot Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Industrial Robot Revenue (million), by Types 2025 & 2033

- Figure 5: North America Industrial Robot Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Industrial Robot Revenue (million), by Country 2025 & 2033

- Figure 7: North America Industrial Robot Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Industrial Robot Revenue (million), by Application 2025 & 2033

- Figure 9: South America Industrial Robot Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Industrial Robot Revenue (million), by Types 2025 & 2033

- Figure 11: South America Industrial Robot Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Industrial Robot Revenue (million), by Country 2025 & 2033

- Figure 13: South America Industrial Robot Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Industrial Robot Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Industrial Robot Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Industrial Robot Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Industrial Robot Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Industrial Robot Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Industrial Robot Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Industrial Robot Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Industrial Robot Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Industrial Robot Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Industrial Robot Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Industrial Robot Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Industrial Robot Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Industrial Robot Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Industrial Robot Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Industrial Robot Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Industrial Robot Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Industrial Robot Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Industrial Robot Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Industrial Robot Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Industrial Robot Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Industrial Robot Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Industrial Robot Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Industrial Robot Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Industrial Robot Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Industrial Robot Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Industrial Robot Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Industrial Robot Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Industrial Robot Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Industrial Robot Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Industrial Robot Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Industrial Robot Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Industrial Robot Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Industrial Robot Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Industrial Robot Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Industrial Robot Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Industrial Robot Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Industrial Robot Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Robot?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Industrial Robot?

Key companies in the market include FANUC, KUKA, ABB, Yaskawa (Motoman), Nachi, Kawasaki Robotics, Comau, EPSON Robots, Staubli, Omron (Adept), DENSO Robotics, OTC Daihen, Panasonic, Shibaura Machine, Mitsubishi Electric, Yamaha, Universal Robots, Hyundai Robotics, Robostar, Star Seiki, JEL Corporation, Techman, Siasun, EFORT Intelligent Equipment, Estun Automation, STEP Electric Corporation, Guangdong Topstar Technology, Inovance Group, Nidec (Genmark Automation), Hirata, Brooks Automation, RORZE Corporation, Tianji Intelligent System, Delta Group, Chengdu CRP Robot Technology, AUBO Robotics, Huashu Robot Co., Ltd., Zhejiang Qianjiang Robot, Peitian Robotics, Shanghai TURIN Chi Robot, Chenxing (Tianjin) Automation Equipment Co., Ltd., QKM Technology, Guangzhou CNC Equipment, Robotphoenix LLC, warsonco Corporation, Sanwa Engineering Corporation, Bekannter Robot Technology, ROKAE.

3. What are the main segments of the Industrial Robot?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 13580 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Industrial Robot," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Industrial Robot report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Industrial Robot?

To stay informed about further developments, trends, and reports in the Industrial Robot, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence