Key Insights

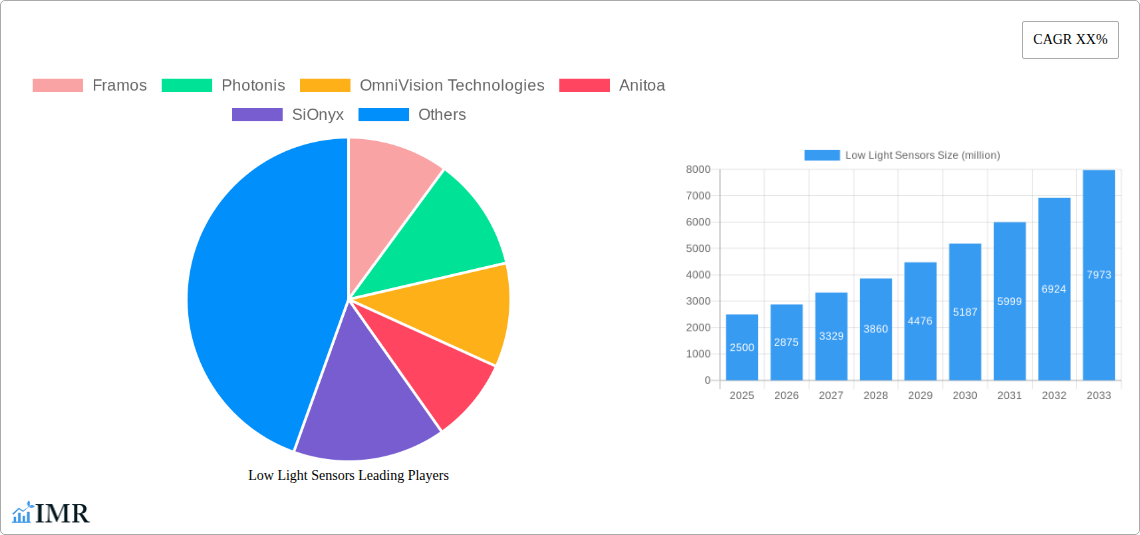

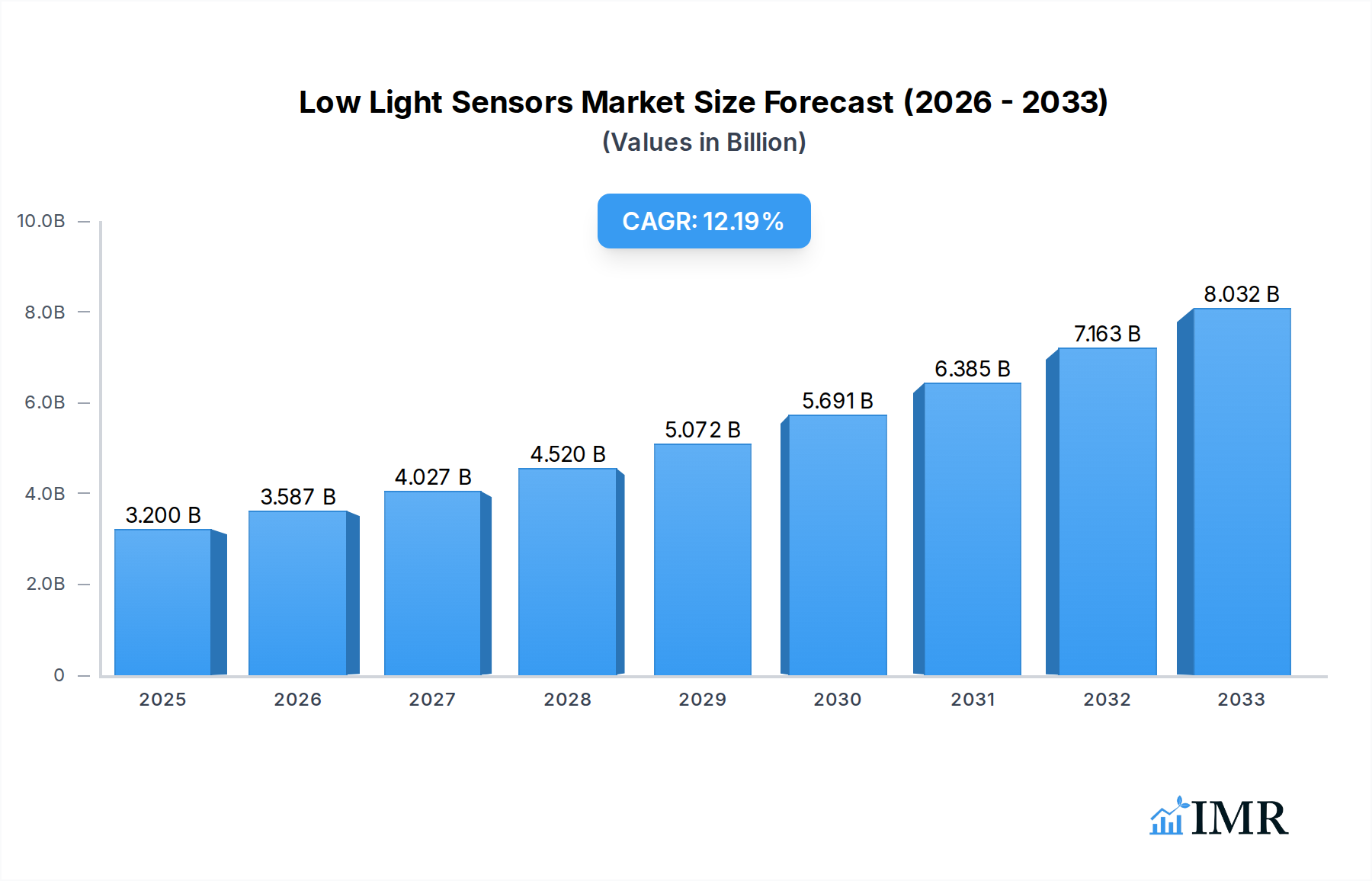

The global Low Light Sensors market is poised for substantial growth, projected to reach $3.2 billion in 2025 and expand at an impressive Compound Annual Growth Rate (CAGR) of 12.1% through 2033. This robust expansion is primarily fueled by escalating demand across critical sectors such as national defense and surveillance, where advanced imaging capabilities are paramount for operational effectiveness. The medical and scientific fields are also significant contributors, leveraging low-light sensor technology for enhanced diagnostic tools and research applications. Furthermore, the burgeoning astronomy sector, with its insatiable need for sensitive imaging of celestial bodies, and a diverse range of other niche applications are collectively driving market momentum. The ongoing evolution from analog to more sophisticated digital sensor technologies is a key trend, offering improved performance, accuracy, and data processing capabilities.

Low Light Sensors Market Size (In Billion)

While the market demonstrates strong growth potential, certain factors could temper its trajectory. Intensifying price competition among key players, including established giants like Sony, Canon, and On Semiconductor, alongside innovative firms such as Photonis and SiOnyx, could impact profit margins. Additionally, the high cost associated with research and development for cutting-edge low-light sensor technology, coupled with the complexities of manufacturing, may present challenges for widespread adoption, particularly in price-sensitive markets. Despite these restraints, the undeniable advantages offered by low-light sensors in improving visibility in challenging conditions are expected to sustain a healthy growth trajectory, with digital sensors gaining increasing prominence over their analog counterparts.

Low Light Sensors Company Market Share

Here is the SEO-optimized report description for Low Light Sensors, incorporating your specified requirements:

Report Title: Global Low Light Sensors Market Analysis & Forecast: Unveiling Growth Opportunities (2019-2033)

Report Description:

Dive deep into the rapidly evolving global low light sensors market with this comprehensive report. Examining the period from 2019 to 2033, with a base year of 2025, this analysis provides critical insights into market dynamics, growth trends, and future outlook. Explore the impact of key low light camera sensor technologies, night vision sensors, and CMOS low light performance across diverse applications including National Defence & Surveillance, Medical & Scientific, and Astronomy. Understand the competitive landscape, driven by innovations from industry leaders such as Framos, Photonis, OmniVision Technologies, Anitoa, SiOnyx, On Semiconductor, Teledyne, Sony, and Canon. This report is essential for stakeholders seeking to capitalize on the burgeoning demand for superior imaging in challenging lighting conditions, offering actionable intelligence on market size, CAGR, and segment-specific growth drivers.

Low Light Sensors Market Dynamics & Structure

The low light sensor market is characterized by a moderate to high concentration, with a few key players dominating technological advancements and market share. Driven by relentless technological innovation, particularly in image sensor technology and low light sensitivity, the market is poised for significant expansion. Regulatory frameworks, especially in defense and medical sectors, often dictate stringent performance standards, acting as both a barrier and an innovation catalyst. Competitive product substitutes, while emerging, are yet to fully match the performance benchmarks set by specialized low light sensors. End-user demographics are increasingly sophisticated, demanding higher resolution and lower noise performance even in near-dark environments. Mergers and acquisitions (M&A) are actively shaping the landscape, with an estimated volume of 5-8 deals annually in the historical period (2019-2024), reflecting a drive for market consolidation and technology acquisition. For instance, the acquisition of niche players by larger entities aims to integrate advanced night vision technology and broaden product portfolios. Innovation barriers include the high cost of R&D for quantum efficiency improvements and the inherent physics limitations of light capture.

- Market concentration: Moderate to High

- Key innovation drivers: Improved quantum efficiency, reduced read noise, higher frame rates, advanced signal processing.

- Regulatory influence: Significant in defense (e.g., night vision standards) and medical (e.g., imaging diagnostics).

- Competitive substitutes: Less prevalent in high-performance niche applications; broader adoption in consumer electronics.

- End-user trends: Demand for enhanced detail, color fidelity, and reduced noise in low light.

- M&A activity: Strategic acquisitions for technology integration and market expansion.

Low Light Sensors Growth Trends & Insights

The global low light sensors market is experiencing robust growth, projected to reach an estimated $15.5 billion in 2025, driven by escalating demand across various high-value sectors. The historical period (2019-2024) saw a compounded annual growth rate (CAGR) of approximately 8.5%, with projections indicating a sustained CAGR of 9.2% during the forecast period (2025-2033). This trajectory is fueled by critical advancements in digital low light sensors and analog low light sensors, offering enhanced performance and cost-effectiveness. Market penetration is deepening, especially in the National Defence & Surveillance segment, where the need for round-the-clock operational capabilities is paramount. In Medical & Scientific applications, the ability of low light sensors to capture subtle biological signals without invasive procedures is revolutionizing diagnostics and research. Furthermore, the burgeoning field of astronomy relies heavily on these sensors for capturing faint celestial objects, pushing the boundaries of scientific discovery. Consumer behavior is also shifting, with an increasing appreciation for smartphone cameras capable of exceptional low-light photography and videography, further boosting adoption. Technological disruptions, such as the integration of AI and machine learning for image enhancement, are augmenting the value proposition of low light sensors. The evolution from traditional CCD to advanced CMOS technologies continues to drive down costs and improve performance, making these sensors accessible to a wider array of applications and markets. The increasing resolution and sensitivity of these devices are enabling new use cases in areas like autonomous driving, industrial inspection, and advanced security systems. As the world becomes more interconnected and reliant on visual data, the demand for sensors that can perform reliably under all lighting conditions will only intensify. The parent market for imaging sensors is also expanding, with low light sensors representing a significant and rapidly growing sub-segment. This growth is further amplified by the "child markets" that emerge from these advancements, such as specialized industrial vision systems and advanced robotics requiring sophisticated perception capabilities. The overall market size for imaging sensors, which forms the parent market, is estimated to reach over $50 billion by 2025, with low light sensors contributing a substantial and growing portion.

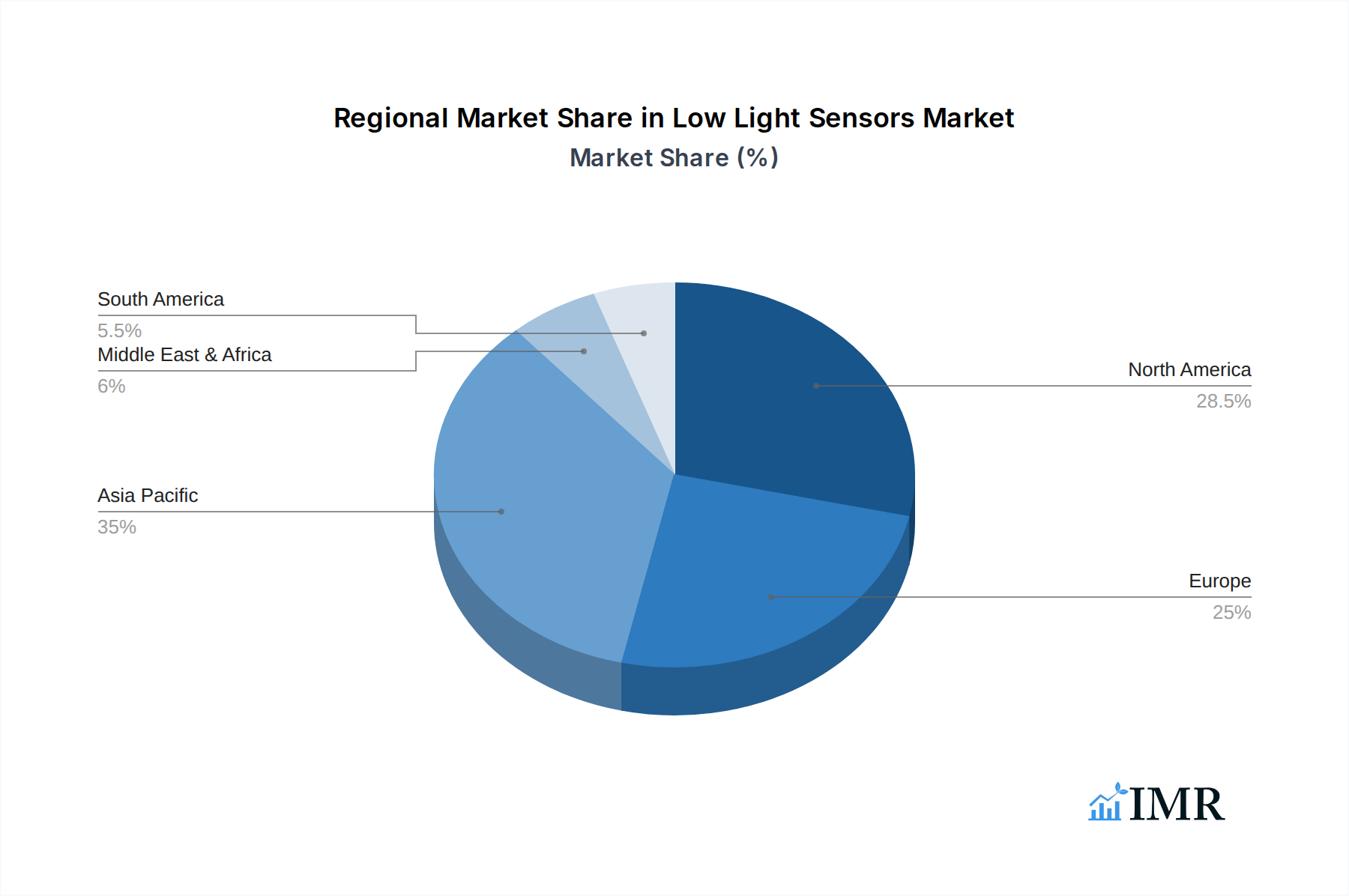

Dominant Regions, Countries, or Segments in Low Light Sensors

The global low light sensors market is witnessing significant dominance from the Asia Pacific region, primarily driven by the robust manufacturing capabilities and increasing R&D investments in countries like China, Japan, and South Korea. This region's influence is further amplified by its substantial contribution to the consumer electronics and automotive industries, both of which are increasingly integrating advanced imaging solutions. In terms of applications, National Defence & Surveillance stands out as a dominant segment, accounting for an estimated 38% of the market share in 2025. This dominance is fueled by escalating geopolitical tensions, the need for enhanced border security, and the growing adoption of surveillance systems by law enforcement agencies worldwide. The market for these sensors in defense applications is projected to reach $5.8 billion by 2025, with a projected CAGR of 9.5% during the forecast period. Leading countries within this segment include the United States, with its significant defense spending, and a growing number of nations investing in sophisticated imaging technologies for military and security purposes.

In the Medical & Scientific segment, the market is expected to reach $3.1 billion by 2025, with a CAGR of 8.8%. The demand here is driven by the need for non-invasive diagnostic tools, advanced microscopy for biological research, and high-resolution imaging for medical procedures. Countries with advanced healthcare infrastructures and strong R&D ecosystems, such as the United States, Germany, and Japan, are key players in this segment. The Astronomy segment, while smaller in terms of market size (estimated at $0.8 billion in 2025), is a crucial area for technological innovation, with a CAGR of 7.9%. This segment is characterized by a demand for ultra-sensitive sensors capable of detecting faint light signals from distant celestial objects, driving cutting-edge research and development. The 'Others' application segment, which includes industrial inspection, autonomous vehicles, and consumer electronics beyond general surveillance, is also showing considerable growth potential, with a projected market size of $5.8 billion by 2025 and a CAGR of 9.0%. Within the types of low light sensors, Digital sensors are increasingly dominating the market, accounting for over 70% of the market share due to their superior performance, ease of integration, and advanced signal processing capabilities compared to their analog counterparts. The market for digital low light sensors is estimated to reach $10.8 billion in 2025.

Low Light Sensors Product Landscape

The low light sensors product landscape is continuously being reshaped by innovations focused on maximizing quantum efficiency and minimizing noise. Key advancements include the development of back-illuminated CMOS sensors, enabling superior light capture, and the integration of advanced noise reduction algorithms, resulting in clearer images even at extreme low light levels. Products are tailored for diverse applications, offering enhanced spectral sensitivity and higher dynamic range. Unique selling propositions revolve around achieving near-perfect image quality in challenging conditions, enabling unprecedented detail in surveillance, medical imaging, and scientific observation. Technological advancements are also enabling smaller form factors and lower power consumption, making these sensors ideal for mobile and portable devices.

Key Drivers, Barriers & Challenges in Low Light Sensors

Key Drivers:

- Technological Advancements: Continuous improvements in sensor technology, such as higher quantum efficiency, lower read noise, and enhanced sensitivity, are primary growth accelerators. The evolution of CMOS technology is a significant driver, offering better performance and cost-effectiveness.

- Increasing Demand in Defence and Surveillance: The global need for enhanced security, border monitoring, and battlefield situational awareness fuels the demand for advanced low light imaging solutions.

- Growth in Medical Imaging: The expanding applications of low light sensors in diagnostics, surgery, and biological research are creating new market opportunities.

- Rise of IoT and Smart Devices: The proliferation of connected devices requiring visual sensing capabilities in various lighting conditions is a key growth factor.

Barriers & Challenges:

- High R&D Costs: Developing next-generation low light sensors requires substantial investment in research and development, posing a barrier for smaller companies.

- Manufacturing Complexity: Achieving high yields and consistent performance in mass production of advanced low light sensors can be challenging.

- Competition from Conventional Sensors: In less demanding applications, conventional sensors might still offer a more cost-effective solution, limiting the penetration of specialized low light sensors.

- Supply Chain Vulnerabilities: Global supply chain disruptions can impact the availability and cost of critical components, affecting production schedules.

Emerging Opportunities in Low Light Sensors

Emerging opportunities in the low light sensors market lie in the burgeoning fields of autonomous vehicles, where robust night-time perception is critical, and advanced robotics requiring precise object recognition in varied lighting. The expansion of smart city initiatives, incorporating intelligent surveillance and infrastructure monitoring, presents another significant avenue. Furthermore, the demand for high-fidelity imaging in virtual and augmented reality experiences, especially in simulated low-light environments, is creating new avenues for specialized sensor development. The exploration of novel materials and quantum dot technologies for enhanced light absorption and conversion also promises to unlock new performance benchmarks.

Growth Accelerators in the Low Light Sensors Industry

The low light sensors industry is experiencing sustained growth acceleration driven by several key factors. Continued advancements in semiconductor manufacturing processes are enabling higher integration and performance at competitive price points. Strategic partnerships between sensor manufacturers and system integrators are crucial for tailoring solutions to specific end-user needs, especially in demanding sectors like defense and medical diagnostics. The increasing adoption of AI and machine learning algorithms for image processing is further enhancing the capabilities of low light sensors, enabling more sophisticated analysis and interpretation of visual data. Market expansion into developing economies, where the adoption of advanced security and monitoring systems is on the rise, also serves as a significant growth accelerator.

Key Players Shaping the Low Light Sensors Market

- Framos

- Photonis

- OmniVision Technologies

- Anitoa

- SiOnyx

- On Semiconductor

- Teledyne

- Sony

- Canon

Notable Milestones in Low Light Sensors Sector

- 2019: Introduction of new back-illuminated CMOS sensors with significantly improved low-light sensitivity by leading manufacturers.

- 2020: Advancements in AI-driven noise reduction algorithms further enhance image quality in low-light conditions.

- 2021: Increased adoption of silicon photomultiplier (SiPM) technology in medical and scientific applications for enhanced photon detection.

- 2022: Development of specialized sensors for autonomous driving requiring robust performance across all lighting and weather conditions.

- 2023: Emergence of novel materials and quantum technologies promising breakthrough performance in light capture.

- 2024: Strategic acquisitions and collaborations focusing on integrating advanced low-light capabilities into broader imaging systems.

In-Depth Low Light Sensors Market Outlook

The future of the low light sensors market is exceptionally bright, projected for sustained and robust growth driven by an confluence of technological innovation and escalating demand across critical sectors. The anticipated $15.5 billion market size in 2025 is just the beginning, with the forecast period (2025-2033) poised to witness significant expansion. Strategic opportunities abound in areas such as advanced autonomous systems, next-generation medical imaging technologies, and enhanced scientific exploration. The continued evolution of CMOS technology, coupled with breakthroughs in material science and computational imaging, will unlock unprecedented levels of performance and accessibility, further solidifying the indispensable role of low light sensors in shaping our visual future.

Low Light Sensors Segmentation

-

1. Application

- 1.1. National Defence & Surveillance

- 1.2. Medical & Scientific

- 1.3. Astronomy

- 1.4. Others

-

2. Types

- 2.1. Analog

- 2.2. Digital

Low Light Sensors Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Low Light Sensors Regional Market Share

Geographic Coverage of Low Light Sensors

Low Light Sensors REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Low Light Sensors Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. National Defence & Surveillance

- 5.1.2. Medical & Scientific

- 5.1.3. Astronomy

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Analog

- 5.2.2. Digital

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Low Light Sensors Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. National Defence & Surveillance

- 6.1.2. Medical & Scientific

- 6.1.3. Astronomy

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Analog

- 6.2.2. Digital

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Low Light Sensors Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. National Defence & Surveillance

- 7.1.2. Medical & Scientific

- 7.1.3. Astronomy

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Analog

- 7.2.2. Digital

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Low Light Sensors Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. National Defence & Surveillance

- 8.1.2. Medical & Scientific

- 8.1.3. Astronomy

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Analog

- 8.2.2. Digital

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Low Light Sensors Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. National Defence & Surveillance

- 9.1.2. Medical & Scientific

- 9.1.3. Astronomy

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Analog

- 9.2.2. Digital

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Low Light Sensors Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. National Defence & Surveillance

- 10.1.2. Medical & Scientific

- 10.1.3. Astronomy

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Analog

- 10.2.2. Digital

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Framos

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Photonis

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 OmniVision Technologies

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Anitoa

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SiOnyx

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 On Semiconductor

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Teledyne

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sony

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Canon

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Framos

List of Figures

- Figure 1: Global Low Light Sensors Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Low Light Sensors Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Low Light Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Low Light Sensors Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Low Light Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Low Light Sensors Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Low Light Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Low Light Sensors Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Low Light Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Low Light Sensors Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Low Light Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Low Light Sensors Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Low Light Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Low Light Sensors Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Low Light Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Low Light Sensors Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Low Light Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Low Light Sensors Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Low Light Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Low Light Sensors Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Low Light Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Low Light Sensors Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Low Light Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Low Light Sensors Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Low Light Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Low Light Sensors Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Low Light Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Low Light Sensors Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Low Light Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Low Light Sensors Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Low Light Sensors Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Low Light Sensors Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Low Light Sensors Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Low Light Sensors Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Low Light Sensors Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Low Light Sensors Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Low Light Sensors Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Low Light Sensors Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Low Light Sensors Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Low Light Sensors Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Low Light Sensors Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Low Light Sensors Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Low Light Sensors Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Low Light Sensors Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Low Light Sensors Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Low Light Sensors Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Low Light Sensors Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Low Light Sensors Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Low Light Sensors Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Low Light Sensors Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Low Light Sensors?

The projected CAGR is approximately 12.1%.

2. Which companies are prominent players in the Low Light Sensors?

Key companies in the market include Framos, Photonis, OmniVision Technologies, Anitoa, SiOnyx, On Semiconductor, Teledyne, Sony, Canon.

3. What are the main segments of the Low Light Sensors?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Low Light Sensors," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Low Light Sensors report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Low Light Sensors?

To stay informed about further developments, trends, and reports in the Low Light Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence