Key Insights

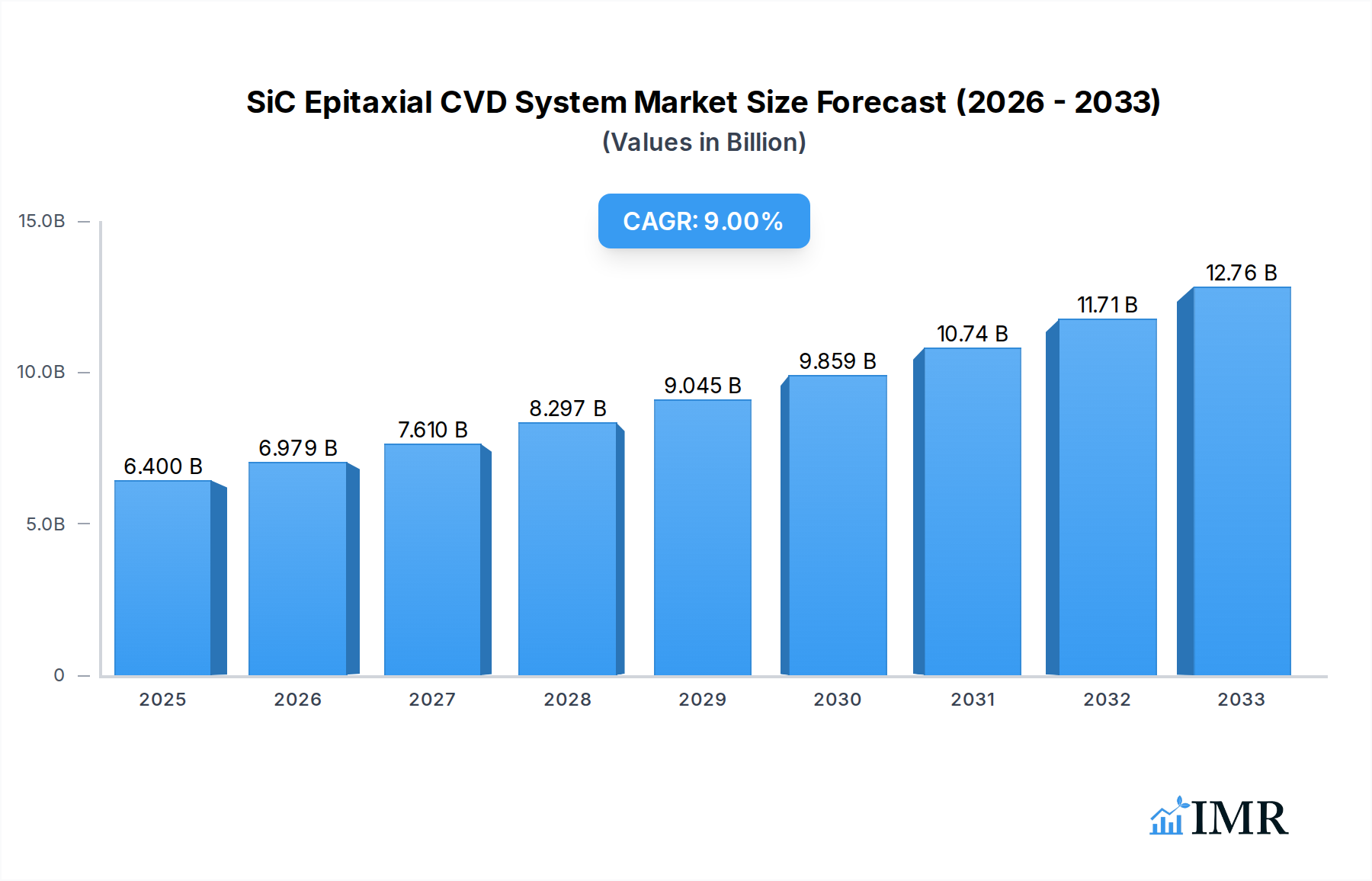

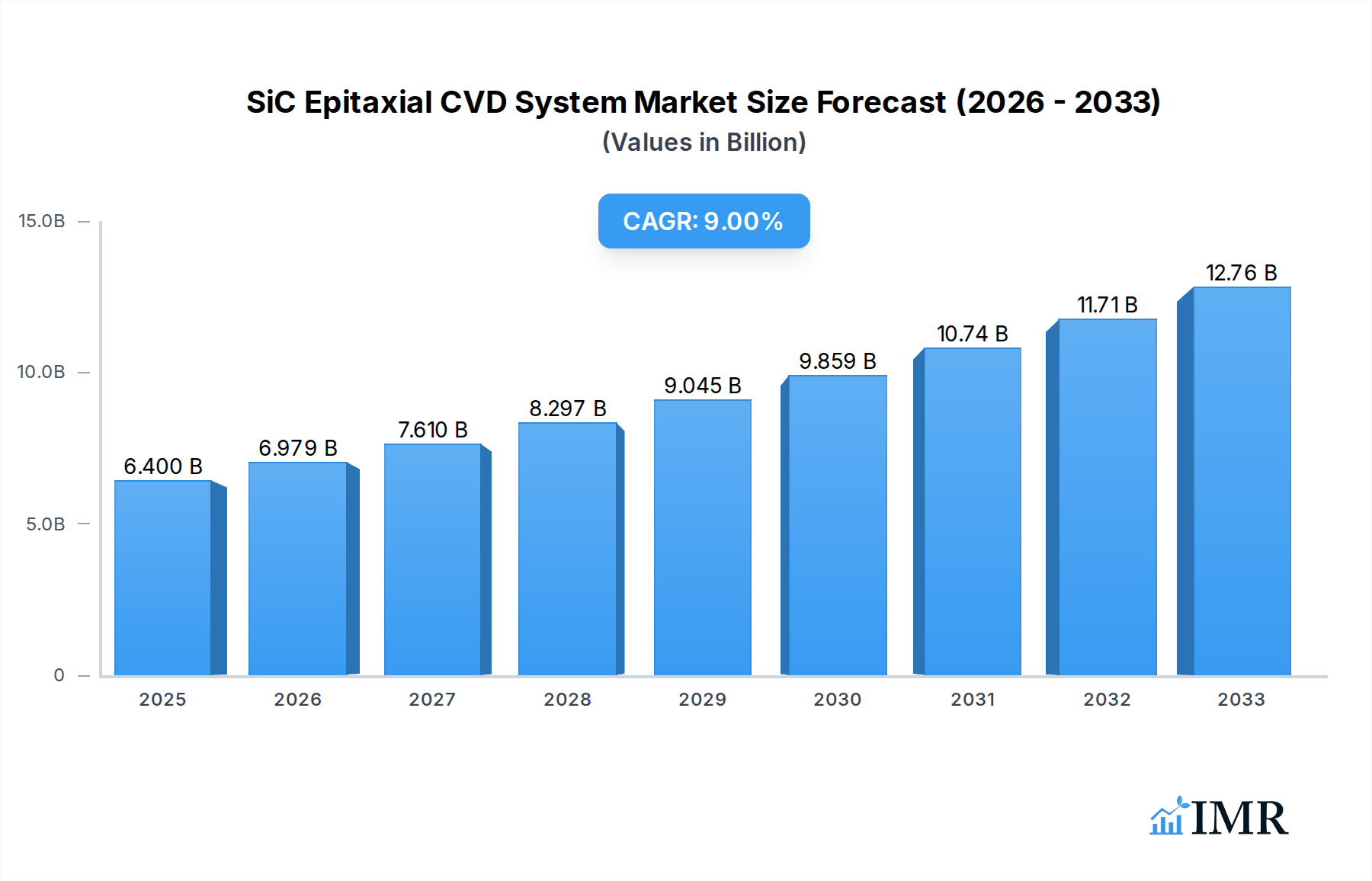

The SiC Epitaxial CVD System market is poised for substantial expansion, driven by the escalating demand for high-performance semiconductors in electric vehicles, renewable energy infrastructure, and advanced power electronics. With an estimated market size of USD 6.4 billion in 2025, the industry is projected to experience robust growth, evidenced by a compelling Compound Annual Growth Rate (CAGR) of 9.11% through 2033. This upward trajectory is primarily fueled by the superior properties of Silicon Carbide (SiC) substrates, including higher breakdown voltage, better thermal conductivity, and increased efficiency compared to traditional silicon. The burgeoning adoption of SiC-based power devices in applications like inverters, converters, and charging stations for electric vehicles is a significant catalyst, alongside their integration into grid-connected systems for enhanced energy management and renewable energy integration. Emerging applications in aerospace, defense, and high-frequency communication further underscore the market's inherent potential.

SiC Epitaxial CVD System Market Size (In Billion)

The market's dynamic landscape is shaped by key trends such as the increasing prevalence of dual wafer systems for improved throughput and efficiency in manufacturing, alongside advancements in epitaxial deposition techniques that enable finer control over wafer quality and performance. While the market benefits from strong growth drivers, it also faces certain restraints, including the high capital investment required for advanced CVD systems and the ongoing need for skilled labor to operate and maintain these sophisticated manufacturing lines. Geographically, Asia Pacific, led by China and Japan, is anticipated to be a dominant force in both production and consumption, owing to its established semiconductor manufacturing ecosystem and substantial investments in new energy technologies. North America and Europe are also demonstrating significant market penetration driven by their ambitious electrification targets and strong R&D capabilities in next-generation power semiconductors. Key players like Tokyo Electron Limited, ASM International, and AIXTRON are at the forefront of innovation, developing cutting-edge solutions to meet the evolving demands of this rapidly expanding sector.

SiC Epitaxial CVD System Company Market Share

Report Title: SiC Epitaxial CVD System Market: Global Forecast & Analysis 2019-2033

Report Description:

Dive deep into the burgeoning SiC Epitaxial CVD System market with our comprehensive report, a critical resource for understanding the trajectory of high-power semiconductor manufacturing. This analysis covers the expansive market for Silicon Carbide (SiC) Epitaxial Chemical Vapor Deposition (CVD) systems, essential for producing advanced wafers used in electric vehicles, renewable energy, and high-frequency electronics. Explore the intricate dynamics of the parent market and its crucial child markets, providing a holistic view of growth drivers and opportunities. We meticulously analyze market concentration, technological innovation drivers, regulatory frameworks, competitive product substitutes, end-user demographics, and M&A trends, offering actionable insights for stakeholders. The report provides a detailed market size evolution, adoption rates, technological disruptions, and consumer behavior shifts, including projected market values in billion units.

The SiC Epitaxial CVD System market is segmented by application into 4 Inch Epitaxial Wafer, 6 Inch Epitaxial Wafer, and 8 Inch Epitaxial Wafer, and by type into Single Wafer Type and Dual Wafer Type systems. Industry developments are scrutinized throughout the study period of 2019–2033, with a base year of 2025, estimated year of 2025, and a comprehensive forecast period of 2025–2033, informed by historical data from 2019–2024. Discover the dominant regions, countries, and segments driving market expansion, alongside a detailed product landscape featuring innovative applications and performance metrics. Key drivers, barriers, challenges, and emerging opportunities are dissected, offering strategic foresight. The report also highlights growth accelerators and profiles the key players shaping this dynamic industry, including Tokyo Electron Limited, Equiluvac (Veeco), Nuflare, ASM International, AIXTRON, M. WATANABE, Naura, JSG, Sicentury, Xiamen Yunmao, and Shenzhen Naso Tech. Notable milestones from 2019–2033 are presented to contextualize market evolution. This report is your definitive guide to navigating the future of SiC epitaxy, providing an in-depth market outlook with strategic opportunities and future potential.

SiC Epitaxial CVD System Market Dynamics & Structure

The SiC Epitaxial CVD System market is characterized by a moderate to high concentration, with a few leading players dominating the technological landscape and production capacity. Technological innovation is the primary driver, fueled by the relentless demand for higher efficiency, lower power loss, and increased reliability in SiC-based power devices. Regulatory frameworks, particularly those supporting renewable energy adoption and electric vehicle production, indirectly bolster the demand for these advanced systems. Competitive product substitutes are limited, as SiC epitaxy offers unique performance advantages over traditional silicon-based technologies for high-power applications. End-user demographics are increasingly shifting towards automotive manufacturers, renewable energy project developers, and industrial electronics providers. Mergers and acquisitions (M&A) are prevalent as companies seek to consolidate their market position, acquire critical intellectual property, or expand their manufacturing capabilities. For instance, in 2023, a significant acquisition in the semiconductor equipment sector involved a deal valued at approximately $3.5 billion, aiming to bolster offerings in advanced materials processing. Innovation barriers include the high capital investment required for R&D and manufacturing, the complexity of SiC material science, and the need for stringent quality control.

- Market Concentration: Dominated by a few key global equipment manufacturers.

- Technological Innovation Drivers: Demand for higher voltage, lower resistance SiC devices.

- Regulatory Frameworks: Government incentives for EV adoption and clean energy.

- Competitive Product Substitutes: Limited, with SiC offering superior performance in niche applications.

- End-User Demographics: Automotive, renewable energy, industrial, and telecommunications sectors.

- M&A Trends: Strategic acquisitions for technology, market access, and capacity expansion.

- Innovation Barriers: High R&D costs, material complexity, and yield optimization.

SiC Epitaxial CVD System Growth Trends & Insights

The SiC Epitaxial CVD System market is poised for robust growth, driven by the accelerating adoption of wide-bandgap semiconductors across various high-performance applications. The market size, projected to reach $4.8 billion in 2025, is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 18.5% from 2025 to 2033, culminating in an estimated market value of $18.2 billion by the end of the forecast period. This remarkable expansion is underpinned by the increasing demand for electric vehicles (EVs), where SiC power modules offer significant advantages in terms of efficiency, range, and charging speed. The renewable energy sector, particularly solar power generation and wind energy conversion, also presents a substantial growth avenue, as SiC devices enable more efficient and compact inverters.

Technological disruptions are continuously refining the capabilities of SiC Epitaxial CVD systems. Advancements in epitaxy techniques, such as advanced reactor designs and process control, are leading to improved wafer quality, reduced defect densities, and enhanced uniformity, all critical for high-yield device fabrication. The transition from 4-inch to 6-inch and eventually to 8-inch SiC wafers is a significant trend, promising to reduce manufacturing costs per chip and further accelerate SiC adoption. Consumer behavior shifts are evident in the growing preference for EVs and the increasing integration of renewable energy sources into the global power grid, directly translating into higher demand for SiC-based power electronics. The market penetration of SiC technology is rapidly increasing, moving from niche applications to mainstream automotive and industrial power systems. The adoption rate for SiC Epitaxial CVD systems is directly correlated with the ramp-up in SiC wafer production capacity globally. Companies are investing heavily in expanding their SiC wafer manufacturing facilities, which in turn drives the demand for advanced CVD equipment.

Furthermore, the development of more sophisticated epitaxy processes capable of depositing thicker SiC layers with higher doping concentrations and lower defect levels is crucial for enabling next-generation SiC devices with even higher power handling capabilities. The increasing reliability and performance metrics of SiC power devices are making them increasingly attractive alternatives to traditional silicon-based components, particularly in demanding environments. The market is witnessing a steady increase in the average selling price of SiC Epitaxial CVD systems due to their sophisticated technology and increasing demand, though economies of scale are expected to moderate price increases over the long term. The integration of artificial intelligence (AI) and machine learning (ML) in process optimization and defect detection within CVD systems is also emerging as a key trend, promising to enhance throughput and wafer quality further.

Dominant Regions, Countries, or Segments in SiC Epitaxial CVD System

The SiC Epitaxial CVD System market is experiencing significant growth and concentration across several key regions and segments. Among the Application segments, 8 Inch Epitaxial Wafer production is emerging as a critical growth frontier, driven by its potential to significantly reduce manufacturing costs per chip, thereby accelerating the widespread adoption of SiC technology. While 6 Inch Epitaxial Wafer production currently represents a substantial portion of the market due to established infrastructure and ongoing high demand, the strategic importance of transitioning to 8 Inch Epitaxial Wafer capabilities cannot be overstated for future market leadership. The 4 Inch Epitaxial Wafer segment, while still relevant for certain legacy applications and specific device types, is gradually being superseded by larger wafer diameters for cost efficiencies.

From the Types perspective, the Dual Wafer Type SiC Epitaxial CVD systems are gaining prominence. These systems offer increased throughput and better utilization of reactor space, directly contributing to higher production volumes and lower manufacturing costs. The ability to process two wafers simultaneously significantly enhances the efficiency of epitaxy processes, which are often time-consuming. The Single Wafer Type systems, while offering precise process control and flexibility for research and development or low-volume production of highly specialized devices, are less efficient for mass production compared to their dual-wafer counterparts.

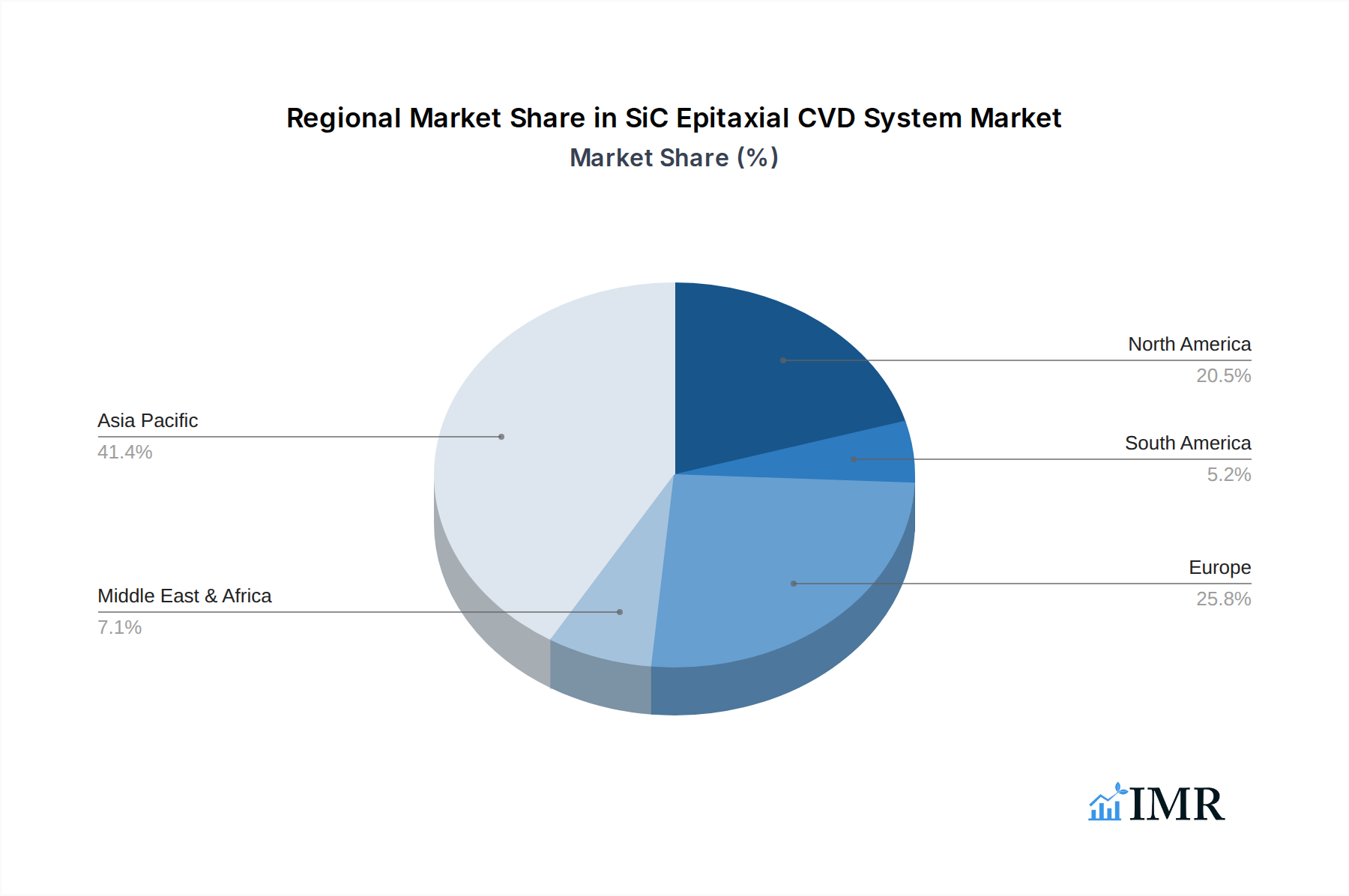

Geographically, Asia Pacific, particularly China, is emerging as a dominant region in the SiC Epitaxial CVD System market. This dominance is fueled by substantial government investments in the semiconductor industry, aggressive expansion of SiC wafer manufacturing capacity, and a rapidly growing domestic demand for electric vehicles and renewable energy infrastructure. China's ambitious "Made in China 2025" initiative has prioritized the development of advanced semiconductor materials and equipment, leading to significant investments in SiC technology. The presence of major SiC wafer manufacturers and foundries in the region further solidifies its leading position.

Key drivers for this regional dominance include supportive economic policies, such as tax incentives and subsidies for semiconductor manufacturing, and the continuous expansion of infrastructure for high-power electronics. Market share within the 8 Inch Epitaxial Wafer application segment is increasingly being contested, with leading equipment manufacturers heavily investing in developing and refining their dual-wafer systems to meet this demand. The growth potential in this segment is enormous, as the industry aims to scale up production to meet projected demand from the automotive sector for SiC power modules.

SiC Epitaxial CVD System Product Landscape

The SiC Epitaxial CVD System product landscape is defined by continuous innovation focused on enhancing throughput, uniformity, and defect control for higher-quality SiC wafers. Leading systems, such as those offered by Tokyo Electron Limited and AIXTRON, employ advanced reactor designs and sophisticated process chemistries to achieve high-quality epitaxial growth. Key product innovations include the development of multi-chambered reactors for increased efficiency and specialized deposition techniques that minimize crystal defects, such as threading dislocations. Performance metrics are rigorously tested, with companies striving for uniformity across the wafer and from wafer-to-wafer, crucial for consistent device performance. Unique selling propositions often revolve around proprietary process technologies that enable lower defect densities (e.g., <0.5 defects/cm²) and higher growth rates, reducing cycle times.

Key Drivers, Barriers & Challenges in SiC Epitaxial CVD System

Key Drivers:

The SiC Epitaxial CVD System market is propelled by several potent forces. The burgeoning electric vehicle (EV) market is a primary catalyst, as SiC power devices enable higher efficiency and faster charging. The expanding renewable energy sector, including solar and wind power, further amplifies demand for SiC's superior performance in inverters and power converters. Government initiatives promoting clean energy transition and semiconductor self-sufficiency also play a crucial role. Technological advancements in higher voltage and lower resistance SiC devices necessitate advanced epitaxy systems. The increasing adoption of 8-inch wafer technology promises cost reductions and higher production volumes.

Barriers & Challenges:

Despite the strong growth, the market faces significant hurdles. The high capital expenditure required for sophisticated SiC epitaxy equipment, often exceeding $10 million per system, is a major barrier. The complexity of SiC material science and epitaxy processes demands specialized expertise and can lead to longer development cycles. Achieving ultra-low defect densities consistently across large wafers remains a technical challenge. Supply chain constraints for critical raw materials and components can impact production timelines. Intense competition among equipment manufacturers puts pressure on pricing and necessitates continuous innovation. Regulatory hurdles related to environmental impact and safety standards also need to be navigated.

Emerging Opportunities in SiC Epitaxial CVD System

Emerging opportunities in the SiC Epitaxial CVD System sector lie in the development of advanced epitaxy techniques for higher performance devices, such as those operating at even higher voltages (e.g., 3.3kV and beyond). The transition to 8-inch SiC wafer manufacturing presents a significant opportunity for equipment suppliers to capture market share by offering leading-edge solutions. Untapped markets in aerospace, high-speed rail, and advanced industrial automation are beginning to explore the benefits of SiC technology. Innovative applications in 5G infrastructure and data centers are also creating new demand. Furthermore, the increasing focus on sustainability and energy efficiency globally will continue to drive the adoption of SiC-based solutions.

Growth Accelerators in the SiC Epitaxial CVD System Industry

The long-term growth of the SiC Epitaxial CVD System industry is being significantly accelerated by several key factors. Technological breakthroughs in achieving higher crystal quality and reducing epitaxy cycle times are crucial. The ongoing ramp-up of SiC wafer production capacity by major players, often involving multi-billion dollar investments, directly fuels demand for new equipment. Strategic partnerships between SiC wafer manufacturers and equipment suppliers facilitate the co-development of optimized epitaxy processes and systems. Furthermore, the increasing standardization of SiC wafer sizes and specifications, particularly the move towards 8-inch wafers, streamlines production and drives economies of scale. The continuous performance improvements and cost reductions in SiC devices make them increasingly competitive against traditional silicon technologies.

Key Players Shaping the SiC Epitaxial CVD System Market

- Tokyo Electron Limited

- Equiluvac (Veeco)

- Nuflare

- ASM International

- AIXTRON

- M. WATANABE

- Naura

- JSG

- Sicentury

- Xiamen Yunmao

- Shenzhen Naso Tech

Notable Milestones in SiC Epitaxial CVD System Sector

- 2019: Increased focus on 6-inch SiC wafer production and initial R&D for 8-inch systems.

- 2020: Major equipment manufacturers announce significant investments in SiC CVD R&D and capacity expansion.

- 2021: Growing demand for SiC in EVs leads to record orders for SiC Epitaxial CVD systems.

- 2022: Companies begin showcasing prototype 8-inch SiC Epitaxial CVD systems.

- 2023: Significant M&A activity aimed at consolidating market positions and acquiring intellectual property in SiC technology. First commercial shipments of 8-inch SiC Epitaxial CVD systems commence.

- 2024: Further acceleration in the adoption of 8-inch wafer technology; increased focus on defect reduction in epitaxy.

In-Depth SiC Epitaxial CVD System Market Outlook

The outlook for the SiC Epitaxial CVD System market remains exceptionally strong, driven by persistent demand from high-growth sectors like electric mobility and renewable energy. The strategic pivot towards 8-inch wafer technology represents a significant growth accelerator, promising to unlock further cost efficiencies and enable broader market penetration. Continued investment in advanced epitaxy processes to achieve superior wafer quality and reduced defect densities will be critical for maintaining competitive advantage. Emerging opportunities in sectors such as advanced power grids, industrial automation, and even defense applications will contribute to sustained market expansion. The future of SiC epitaxy is intrinsically linked to the global push for electrification and decarbonization, creating a robust and enduring demand for these sophisticated manufacturing systems.

SiC Epitaxial CVD System Segmentation

-

1. Application

- 1.1. 4 Inch Epitaxial Wafer

- 1.2. 6 Inch Epitaxial Wafer

- 1.3. 8 Inch Epitaxial Wafer

-

2. Types

- 2.1. Single Wafer Type

- 2.2. Dual Wafer Type

SiC Epitaxial CVD System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

SiC Epitaxial CVD System Regional Market Share

Geographic Coverage of SiC Epitaxial CVD System

SiC Epitaxial CVD System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global SiC Epitaxial CVD System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. 4 Inch Epitaxial Wafer

- 5.1.2. 6 Inch Epitaxial Wafer

- 5.1.3. 8 Inch Epitaxial Wafer

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Single Wafer Type

- 5.2.2. Dual Wafer Type

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America SiC Epitaxial CVD System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. 4 Inch Epitaxial Wafer

- 6.1.2. 6 Inch Epitaxial Wafer

- 6.1.3. 8 Inch Epitaxial Wafer

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Single Wafer Type

- 6.2.2. Dual Wafer Type

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America SiC Epitaxial CVD System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. 4 Inch Epitaxial Wafer

- 7.1.2. 6 Inch Epitaxial Wafer

- 7.1.3. 8 Inch Epitaxial Wafer

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Single Wafer Type

- 7.2.2. Dual Wafer Type

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe SiC Epitaxial CVD System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. 4 Inch Epitaxial Wafer

- 8.1.2. 6 Inch Epitaxial Wafer

- 8.1.3. 8 Inch Epitaxial Wafer

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Single Wafer Type

- 8.2.2. Dual Wafer Type

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa SiC Epitaxial CVD System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. 4 Inch Epitaxial Wafer

- 9.1.2. 6 Inch Epitaxial Wafer

- 9.1.3. 8 Inch Epitaxial Wafer

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Single Wafer Type

- 9.2.2. Dual Wafer Type

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific SiC Epitaxial CVD System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. 4 Inch Epitaxial Wafer

- 10.1.2. 6 Inch Epitaxial Wafer

- 10.1.3. 8 Inch Epitaxial Wafer

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Single Wafer Type

- 10.2.2. Dual Wafer Type

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Tokyo Electron Limited

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Equiluvac (Veeco)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nuflare

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ASM International

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 AIXTRON

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 M.WATANABE

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Naura

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 JSG

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Sicentury

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Xiamen Yunmao

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shenzhen Naso Tech

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Tokyo Electron Limited

List of Figures

- Figure 1: Global SiC Epitaxial CVD System Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America SiC Epitaxial CVD System Revenue (billion), by Application 2025 & 2033

- Figure 3: North America SiC Epitaxial CVD System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America SiC Epitaxial CVD System Revenue (billion), by Types 2025 & 2033

- Figure 5: North America SiC Epitaxial CVD System Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America SiC Epitaxial CVD System Revenue (billion), by Country 2025 & 2033

- Figure 7: North America SiC Epitaxial CVD System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America SiC Epitaxial CVD System Revenue (billion), by Application 2025 & 2033

- Figure 9: South America SiC Epitaxial CVD System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America SiC Epitaxial CVD System Revenue (billion), by Types 2025 & 2033

- Figure 11: South America SiC Epitaxial CVD System Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America SiC Epitaxial CVD System Revenue (billion), by Country 2025 & 2033

- Figure 13: South America SiC Epitaxial CVD System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe SiC Epitaxial CVD System Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe SiC Epitaxial CVD System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe SiC Epitaxial CVD System Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe SiC Epitaxial CVD System Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe SiC Epitaxial CVD System Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe SiC Epitaxial CVD System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa SiC Epitaxial CVD System Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa SiC Epitaxial CVD System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa SiC Epitaxial CVD System Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa SiC Epitaxial CVD System Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa SiC Epitaxial CVD System Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa SiC Epitaxial CVD System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific SiC Epitaxial CVD System Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific SiC Epitaxial CVD System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific SiC Epitaxial CVD System Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific SiC Epitaxial CVD System Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific SiC Epitaxial CVD System Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific SiC Epitaxial CVD System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global SiC Epitaxial CVD System Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global SiC Epitaxial CVD System Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global SiC Epitaxial CVD System Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global SiC Epitaxial CVD System Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global SiC Epitaxial CVD System Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global SiC Epitaxial CVD System Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global SiC Epitaxial CVD System Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global SiC Epitaxial CVD System Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global SiC Epitaxial CVD System Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global SiC Epitaxial CVD System Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global SiC Epitaxial CVD System Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global SiC Epitaxial CVD System Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global SiC Epitaxial CVD System Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global SiC Epitaxial CVD System Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global SiC Epitaxial CVD System Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global SiC Epitaxial CVD System Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global SiC Epitaxial CVD System Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global SiC Epitaxial CVD System Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific SiC Epitaxial CVD System Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the SiC Epitaxial CVD System?

The projected CAGR is approximately 9.11%.

2. Which companies are prominent players in the SiC Epitaxial CVD System?

Key companies in the market include Tokyo Electron Limited, Equiluvac (Veeco), Nuflare, ASM International, AIXTRON, M.WATANABE, Naura, JSG, Sicentury, Xiamen Yunmao, Shenzhen Naso Tech.

3. What are the main segments of the SiC Epitaxial CVD System?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "SiC Epitaxial CVD System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the SiC Epitaxial CVD System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the SiC Epitaxial CVD System?

To stay informed about further developments, trends, and reports in the SiC Epitaxial CVD System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence