Key Insights

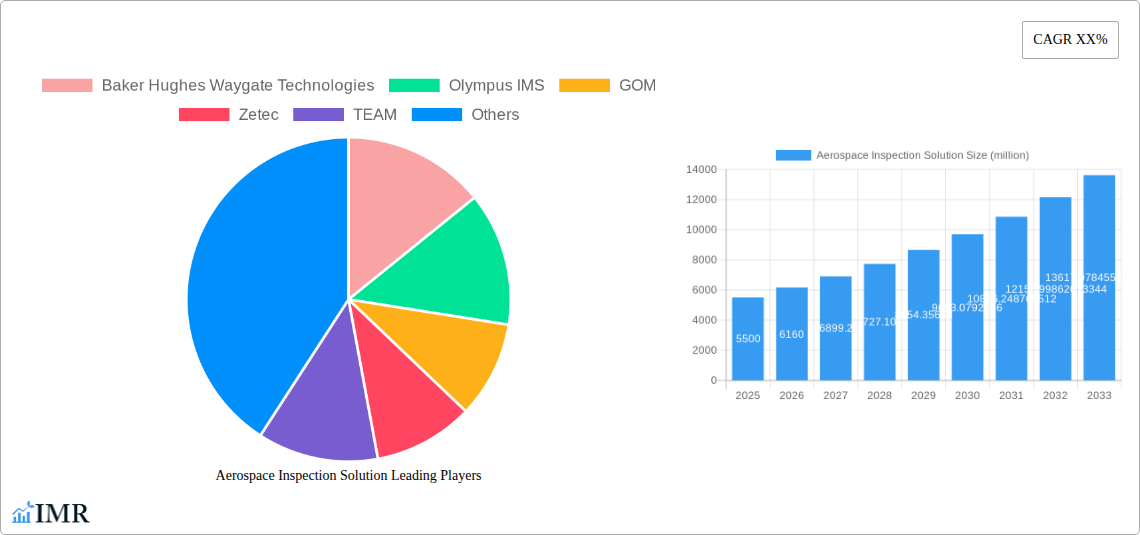

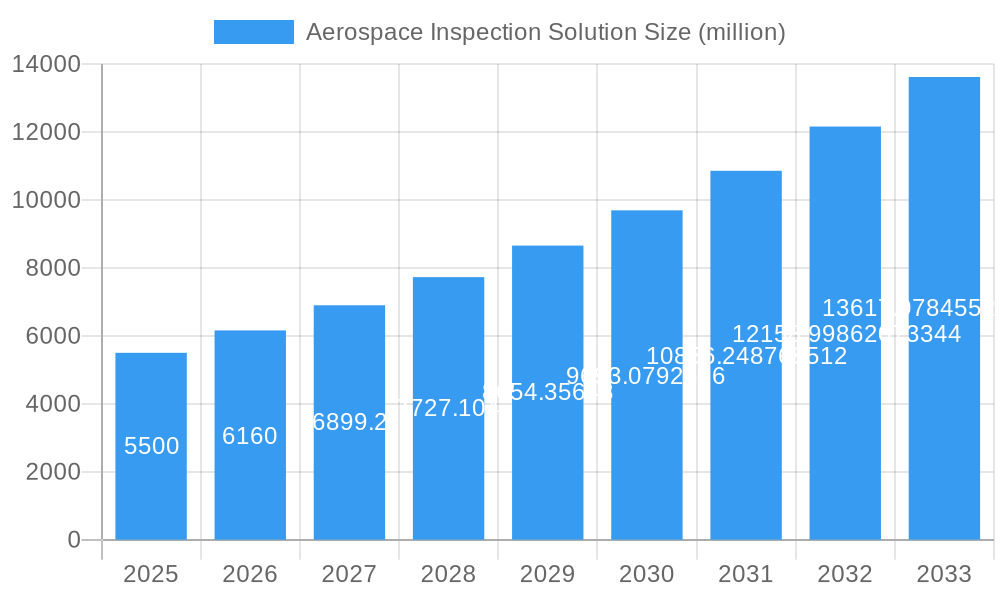

The global Aerospace Inspection Solution market is poised for robust growth, projected to reach an estimated USD 5,500 million by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 12% through 2033. This surge is primarily fueled by the increasing demand for advanced inspection techniques to ensure the safety and integrity of aircraft components, coupled with the growing fleet size and stringent regulatory requirements worldwide. The non-destructive testing (NDT) segment is expected to dominate, driven by its ability to detect defects without compromising the component's structural integrity. Visual inspection remains a foundational method, but its efficacy is being amplified by automated solutions that offer greater precision and efficiency. Structural health monitoring systems are gaining traction, offering real-time insights into an aircraft's condition, thereby enhancing predictive maintenance strategies and reducing operational downtime.

Aerospace Inspection Solution Market Size (In Billion)

The market is experiencing a significant shift towards automated inspection solutions, integrating artificial intelligence and machine learning to enhance accuracy and speed in defect detection. This trend is particularly evident in the aerospace sector, where the complexity and critical nature of components necessitate highly reliable inspection processes. Key players like Baker Hughes Waygate Technologies, Olympus IMS, and GOM are investing heavily in R&D to develop sophisticated technologies, including advanced ultrasonic, eddy current, and phased array systems, alongside robotic and drone-based inspection platforms. While the adoption of these advanced technologies presents a significant growth opportunity, potential restraints include the high initial investment costs associated with sophisticated equipment and the need for skilled personnel to operate and interpret the data. Geographically, North America and Europe are anticipated to lead the market share, driven by well-established aerospace manufacturing hubs and stringent aviation safety standards. However, the Asia Pacific region is expected to witness the fastest growth, propelled by the expanding aviation industry in China and India and increasing investments in modernizing MRO (Maintenance, Repair, and Overhaul) facilities.

Aerospace Inspection Solution Company Market Share

This in-depth report provides an indispensable look into the Aerospace Inspection Solution Market, meticulously detailing its current state, growth trajectory, and future potential. Spanning the historical period of 2019-2024, with a base year of 2025 and a comprehensive forecast extending to 2033, this analysis offers actionable insights for industry stakeholders seeking to navigate this dynamic sector. We delve into the intricate interplay of technological advancements, evolving regulatory landscapes, and shifting end-user demands that are shaping the global demand for advanced inspection solutions.

Aerospace Inspection Solution Market Dynamics & Structure

The Aerospace Inspection Solution market exhibits a moderate concentration, characterized by a few dominant players alongside a growing number of innovative niche providers. Technological innovation is the primary driver, with constant advancements in Non-destructive Testing (NDT) methodologies, artificial intelligence (AI) for automated analysis, and miniaturization of inspection equipment pushing the boundaries of what's possible. Regulatory frameworks, such as those mandated by the FAA and EASA, are instrumental in setting stringent safety and quality standards, thereby fueling the demand for reliable and certified inspection solutions. Competitive product substitutes, while present, are often surpassed by the superior accuracy, efficiency, and data integrity offered by advanced aerospace inspection solutions. End-user demographics are shifting towards a greater demand for predictive maintenance and condition-based monitoring, driven by cost-saving imperatives and a desire to minimize aircraft downtime. Mergers and acquisitions (M&A) are a recurring trend, as larger players seek to consolidate market share, acquire cutting-edge technologies, and expand their geographical reach.

- Market Concentration: Dominated by key players with significant R&D investments, alongside emerging innovators.

- Technological Innovation Drivers: Advancements in NDT techniques (ultrasonic, eddy current, phased array), AI/ML for data analysis, robotics, and drone-based inspections.

- Regulatory Frameworks: Strict adherence to FAA, EASA, and other aviation authority guidelines for safety and airworthiness.

- Competitive Product Substitutes: Traditional manual inspection methods, though increasingly being phased out by automated and NDT solutions.

- End-User Demographics: Airlines, MRO (Maintenance, Repair, and Overhaul) providers, aircraft manufacturers, and defense sectors.

- M&A Trends: Strategic acquisitions to gain market share, acquire proprietary technologies, and expand service offerings. Estimated 5-8 M&A deals annually within the broader industrial inspection sector, with a significant portion impacting aerospace.

Aerospace Inspection Solution Growth Trends & Insights

The global Aerospace Inspection Solution market is poised for substantial growth, projected to expand from an estimated $3,500 million in 2025 to over $6,200 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period. This robust expansion is fueled by an increasing global air passenger traffic, which in turn necessitates greater maintenance and inspection activities for existing fleets. The growing emphasis on aircraft safety and longevity, driven by both regulatory mandates and economic considerations, is a significant adoption rate accelerant for advanced inspection technologies. Technological disruptions, particularly the integration of AI and machine learning into automated inspection systems, are revolutionizing efficiency and accuracy, enabling faster defect detection and more comprehensive data analysis. Consumer behavior is shifting towards a preference for predictive maintenance strategies, moving away from time-based scheduled inspections towards condition-based monitoring, which reduces operational costs and minimizes unexpected failures. The increasing complexity of aircraft designs and materials also necessitates more sophisticated inspection methods.

The market penetration of automated inspection solutions is expected to witness a significant surge, driven by their ability to reduce human error, enhance consistency, and provide detailed digital records. Visual inspection, while foundational, is increasingly being augmented and sometimes replaced by high-resolution imaging, robotic cameras, and remote visual inspection (RVI) systems. Non-destructive Testing (NDT) remains the cornerstone of aerospace inspection, with continuous innovation in ultrasonic testing (UT), eddy current testing (ECT), phased array ultrasonic testing (PAUT), and computed radiography (CR) driving market demand. Structural Health Monitoring (SHM) systems, which continuously assess the integrity of aircraft structures, are gaining traction for their proactive approach to safety and maintenance. The demand for specialized inspection solutions for composite materials, critical for modern aircraft, is also on the rise. Furthermore, the burgeoning drone inspection market, offering efficient and safe access to hard-to-reach areas of aircraft, is a key growth driver. The growing defense aerospace sector, with its stringent requirements for aircraft readiness and safety, also contributes significantly to the market's upward trajectory. The integration of IoT (Internet of Things) for real-time data transmission from inspection sensors will further streamline maintenance processes. The rising demand for lightweight and fuel-efficient aircraft, often constructed with advanced composite materials, necessitates specialized and advanced inspection techniques to ensure structural integrity. The increasing lifespan of aircraft fleets also translates into a sustained demand for ongoing inspection and maintenance services.

Dominant Regions, Countries, or Segments in Aerospace Inspection Solution

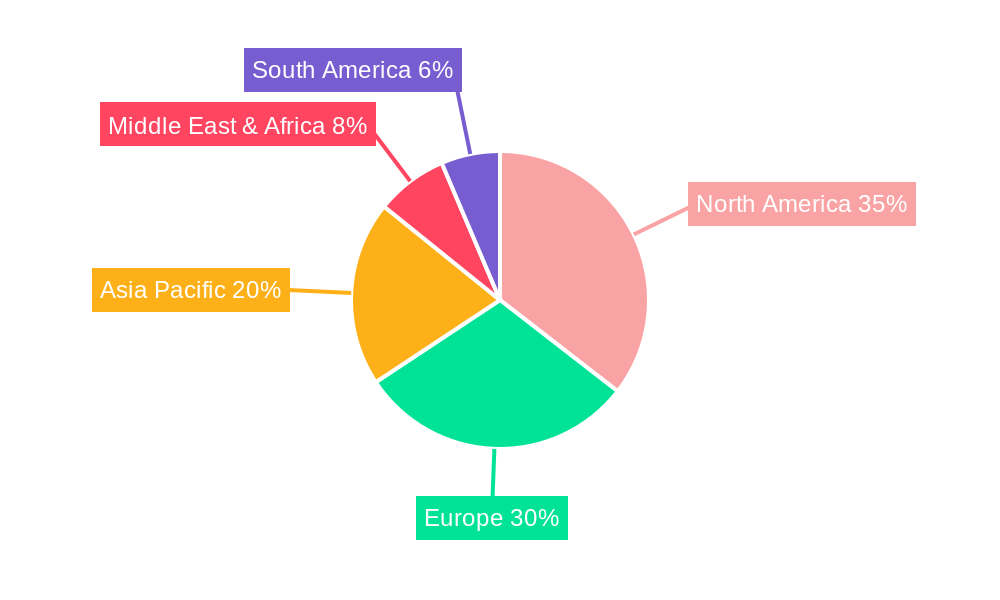

The Aerospace segment, within the broader Application category, is the undisputed dominant force driving growth in the Aerospace Inspection Solution market. This dominance is rooted in the inherently high safety standards and regulatory stringency of the aviation industry. Aircraft manufacturers and Maintenance, Repair, and Overhaul (MRO) providers are under immense pressure to ensure the airworthiness and structural integrity of aircraft, leading to a consistent and substantial demand for sophisticated inspection solutions. The Asia-Pacific region, particularly China and India, is emerging as a significant growth driver due to the rapid expansion of their domestic aviation industries and increasing investments in aerospace manufacturing and MRO capabilities. North America, with its established aerospace giants and a mature MRO network, continues to be a major market, driven by technological innovation and a high volume of aircraft operations. Europe also maintains a strong presence, fueled by leading aircraft manufacturers and a robust regulatory environment.

Within the Types of inspection solutions, Non-destructive Testing (NDT) holds the largest market share and is a primary growth engine. Advanced NDT techniques such as Phased Array Ultrasonic Testing (PAUT), Eddy Current Testing (ECT), and Computed Radiography (CR) are crucial for detecting internal flaws and material defects without damaging the aircraft structure. Automated Inspection is rapidly gaining prominence, driven by the need for increased efficiency, reduced human error, and enhanced data consistency. Robotic inspection systems and AI-powered defect analysis are transforming MRO operations. Visual Inspection, though a fundamental aspect, is increasingly enhanced by high-resolution cameras, drones, and endoscopes for detailed examination of aircraft components. Structural Health Monitoring (SHM) is a growing segment, offering continuous assessment of aircraft integrity, particularly for new composite materials. The increasing adoption of smart sensors and IoT integration in SHM systems is expected to further accelerate its growth. The market's growth is also influenced by government policies promoting domestic aerospace manufacturing and MRO hubs, as well as investments in advanced technological infrastructure. The rise of low-cost carriers globally also contributes to increased flight hours, thus escalating the need for regular and thorough aircraft inspections.

- Dominant Segment (Application): Aerospace

- Key Drivers: Stringent safety regulations, high maintenance requirements, growth in global air travel, increasing aircraft lifespans.

- Market Share: Estimated to constitute over 85% of the total Aerospace Inspection Solution market.

- Growth Potential: Continual innovation in inspection technologies to meet evolving aircraft materials and designs.

- Dominant Segment (Types): Non-destructive Testing (NDT)

- Key Drivers: Essential for flaw detection, regulatory mandates, advancements in UT, ECT, PAUT, and CR technologies.

- Market Share: Represents a substantial portion of the overall inspection solution market, estimated at over 50%.

- Growth Potential: Integration with AI for automated defect analysis, development of portable and advanced NDT equipment.

- Dominant Region: North America (continued strong market) and Asia-Pacific (rapid growth).

- Key Drivers (North America): Mature MRO infrastructure, technological innovation, significant defense spending.

- Key Drivers (Asia-Pacific): Rapidly expanding aviation sector, increasing domestic manufacturing, government initiatives to boost aerospace capabilities.

Aerospace Inspection Solution Product Landscape

The Aerospace Inspection Solution product landscape is characterized by a relentless pursuit of higher resolution, greater portability, enhanced automation, and superior data analytics capabilities. Innovations are focused on developing NDT equipment that can inspect complex geometries and composite materials with unprecedented accuracy. This includes advancements in phased array ultrasonic systems with multi-element transducers for comprehensive coverage, eddy current arrays for surface and near-surface flaw detection, and advanced radiographic solutions offering higher sensitivity and faster scanning times. The integration of AI and machine learning algorithms into these systems is a significant trend, enabling automated defect recognition, classification, and reporting, thereby reducing analysis time and human subjectivity. Robotic and drone-based inspection platforms are becoming increasingly sophisticated, offering safe, efficient, and cost-effective ways to inspect large aircraft structures, including wings, fuselages, and engines, in hard-to-reach areas. Visual inspection solutions are also evolving with high-definition cameras, specialized lighting, and augmented reality (AR) overlays to assist inspectors in identifying subtle defects. The development of portable and wireless inspection devices further enhances field service capabilities.

Key Drivers, Barriers & Challenges in Aerospace Inspection Solution

Key Drivers:

- Increasing Global Air Traffic: Rising passenger and cargo volumes necessitate more frequent and thorough aircraft inspections to ensure safety and operational efficiency.

- Stringent Regulatory Mandates: Aviation authorities worldwide impose strict safety and airworthiness standards, driving the adoption of advanced inspection solutions.

- Technological Advancements: Continuous innovation in NDT, AI, robotics, and data analytics offers more accurate, efficient, and cost-effective inspection methods.

- Aging Aircraft Fleets: The growing number of older aircraft in operation requires intensive maintenance and inspection to extend their service life.

- Emphasis on Predictive Maintenance: Shift from scheduled to condition-based maintenance, driven by cost savings and operational optimization, fuels demand for real-time monitoring and predictive capabilities.

Key Barriers & Challenges:

- High Initial Investment Costs: Advanced inspection equipment and software can represent a significant upfront capital expenditure for MROs and airlines.

- Skilled Workforce Shortage: A lack of trained and certified personnel to operate and interpret data from sophisticated inspection systems poses a challenge.

- Integration Complexity: Seamless integration of new inspection technologies with existing MRO workflows and IT infrastructure can be complex.

- Data Security and Management: Handling and securing vast amounts of inspection data requires robust cybersecurity measures and data management strategies.

- Resistance to Change: Some organizations may exhibit resistance to adopting new technologies due to established practices and training requirements, impacting the adoption rate. Estimated impact of these challenges could lead to a 5-10% slower adoption of cutting-edge technologies in less developed markets.

Emerging Opportunities in Aerospace Inspection Solution

Emerging opportunities in the Aerospace Inspection Solution market are abundant, driven by the continuous evolution of aircraft technology and the growing emphasis on sustainable aviation. The increasing use of advanced composite materials in aircraft construction presents a significant opportunity for specialized NDT techniques and phased array ultrasonics capable of detecting delamination and fiber breakage. The burgeoning market for unmanned aerial vehicles (UAVs) in aerospace inspection offers a cost-effective and safer alternative for inspecting large structures, creating demand for drone-integrated inspection solutions and data processing platforms. The development of "digital twin" technologies for aircraft, which require comprehensive and real-time inspection data for accurate modeling and simulation, presents a long-term growth avenue. Furthermore, the increasing focus on in-situ monitoring and the integration of sensors for Structural Health Monitoring (SHM) are opening up new markets for continuous assessment of aircraft integrity. The demand for lightweight and fuel-efficient aircraft, often incorporating novel materials and designs, will necessitate continuous innovation in inspection methodologies.

Growth Accelerators in the Aerospace Inspection Solution Industry

Several key catalysts are accelerating growth in the Aerospace Inspection Solution industry. Technological breakthroughs in areas like artificial intelligence for automated defect recognition and machine learning for predictive maintenance are significantly enhancing the capabilities and efficiency of inspection systems. Strategic partnerships between technology providers, aircraft manufacturers, and MROs are fostering innovation and accelerating the development and adoption of integrated solutions. Market expansion strategies, particularly in emerging economies with rapidly growing aviation sectors, are unlocking new customer bases and driving demand. The increasing regulatory pressure for enhanced safety and airworthiness standards globally also acts as a powerful growth accelerator, compelling organizations to invest in the most advanced inspection capabilities. Furthermore, the growing awareness and demand for proactive rather than reactive maintenance strategies are pushing the industry towards predictive and condition-based monitoring solutions.

Key Players Shaping the Aerospace Inspection Solution Market

- Baker Hughes Waygate Technologies

- Olympus IMS

- GOM

- Zetec

- TEAM

Notable Milestones in Aerospace Inspection Solution Sector

- 2021: Launch of advanced AI-powered phased array ultrasonic systems by major players, significantly improving defect detection speed and accuracy.

- 2022: Increased adoption of drone-based visual inspection for fuselage and wing inspections, improving safety and reducing turnaround times.

- 2023: Significant advancements in non-contact inspection techniques for composite materials, addressing a key challenge in modern aircraft manufacturing.

- 2023: Strategic collaborations between AI software developers and NDT equipment manufacturers to enhance data analysis capabilities.

- 2024: Expansion of automated inspection solutions into engine component inspections, further streamlining MRO processes.

- 2024: Introduction of enhanced Structural Health Monitoring (SHM) systems with real-time data transmission capabilities.

In-Depth Aerospace Inspection Solution Market Outlook

The outlook for the Aerospace Inspection Solution market remains exceptionally positive, driven by an unyielding commitment to safety, the relentless pace of technological innovation, and the sustained growth of the global aviation industry. Growth accelerators such as advancements in AI-driven analytics and the widespread adoption of automated inspection platforms will continue to enhance efficiency and precision. Strategic partnerships and collaborations are expected to foster further innovation, leading to integrated solutions that address the complex challenges of modern aircraft maintenance. As the aviation sector increasingly embraces predictive maintenance, the demand for real-time monitoring and intelligent data interpretation will surge. Emerging markets, coupled with the ongoing need to maintain and extend the lifespan of aging aircraft fleets, present significant untapped potential. The market is poised for continued expansion, with a strong emphasis on developing solutions that are not only accurate and reliable but also cost-effective and environmentally sustainable, creating a robust future for aerospace inspection technologies.

Aerospace Inspection Solution Segmentation

-

1. Application

- 1.1. Aerospace

- 1.2. Other

-

2. Types

- 2.1. Non-destructive Testing

- 2.2. Visual Inspection

- 2.3. Automated Inspection

- 2.4. Structural Health Monitoring

Aerospace Inspection Solution Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aerospace Inspection Solution Regional Market Share

Geographic Coverage of Aerospace Inspection Solution

Aerospace Inspection Solution REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aerospace

- 5.1.2. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Non-destructive Testing

- 5.2.2. Visual Inspection

- 5.2.3. Automated Inspection

- 5.2.4. Structural Health Monitoring

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Aerospace Inspection Solution Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aerospace

- 6.1.2. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Non-destructive Testing

- 6.2.2. Visual Inspection

- 6.2.3. Automated Inspection

- 6.2.4. Structural Health Monitoring

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Aerospace Inspection Solution Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aerospace

- 7.1.2. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Non-destructive Testing

- 7.2.2. Visual Inspection

- 7.2.3. Automated Inspection

- 7.2.4. Structural Health Monitoring

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Aerospace Inspection Solution Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aerospace

- 8.1.2. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Non-destructive Testing

- 8.2.2. Visual Inspection

- 8.2.3. Automated Inspection

- 8.2.4. Structural Health Monitoring

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Aerospace Inspection Solution Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aerospace

- 9.1.2. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Non-destructive Testing

- 9.2.2. Visual Inspection

- 9.2.3. Automated Inspection

- 9.2.4. Structural Health Monitoring

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Aerospace Inspection Solution Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aerospace

- 10.1.2. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Non-destructive Testing

- 10.2.2. Visual Inspection

- 10.2.3. Automated Inspection

- 10.2.4. Structural Health Monitoring

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Aerospace Inspection Solution Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Aerospace

- 11.1.2. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Non-destructive Testing

- 11.2.2. Visual Inspection

- 11.2.3. Automated Inspection

- 11.2.4. Structural Health Monitoring

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Baker Hughes Waygate Technologies

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Olympus IMS

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 GOM

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Zetec

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 TEAM

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.1 Baker Hughes Waygate Technologies

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aerospace Inspection Solution Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Aerospace Inspection Solution Revenue (million), by Application 2025 & 2033

- Figure 3: North America Aerospace Inspection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aerospace Inspection Solution Revenue (million), by Types 2025 & 2033

- Figure 5: North America Aerospace Inspection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aerospace Inspection Solution Revenue (million), by Country 2025 & 2033

- Figure 7: North America Aerospace Inspection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aerospace Inspection Solution Revenue (million), by Application 2025 & 2033

- Figure 9: South America Aerospace Inspection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aerospace Inspection Solution Revenue (million), by Types 2025 & 2033

- Figure 11: South America Aerospace Inspection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aerospace Inspection Solution Revenue (million), by Country 2025 & 2033

- Figure 13: South America Aerospace Inspection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aerospace Inspection Solution Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Aerospace Inspection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aerospace Inspection Solution Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Aerospace Inspection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aerospace Inspection Solution Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Aerospace Inspection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aerospace Inspection Solution Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aerospace Inspection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aerospace Inspection Solution Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aerospace Inspection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aerospace Inspection Solution Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aerospace Inspection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aerospace Inspection Solution Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Aerospace Inspection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aerospace Inspection Solution Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Aerospace Inspection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aerospace Inspection Solution Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Aerospace Inspection Solution Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aerospace Inspection Solution Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Aerospace Inspection Solution Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Aerospace Inspection Solution Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Aerospace Inspection Solution Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Aerospace Inspection Solution Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Aerospace Inspection Solution Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Aerospace Inspection Solution Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Aerospace Inspection Solution Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Aerospace Inspection Solution Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Aerospace Inspection Solution Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Aerospace Inspection Solution Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Aerospace Inspection Solution Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Aerospace Inspection Solution Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Aerospace Inspection Solution Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Aerospace Inspection Solution Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Aerospace Inspection Solution Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Aerospace Inspection Solution Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Aerospace Inspection Solution Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aerospace Inspection Solution Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Inspection Solution?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Aerospace Inspection Solution?

Key companies in the market include Baker Hughes Waygate Technologies, Olympus IMS, GOM, Zetec, TEAM.

3. What are the main segments of the Aerospace Inspection Solution?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aerospace Inspection Solution," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aerospace Inspection Solution report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aerospace Inspection Solution?

To stay informed about further developments, trends, and reports in the Aerospace Inspection Solution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence