Key Insights

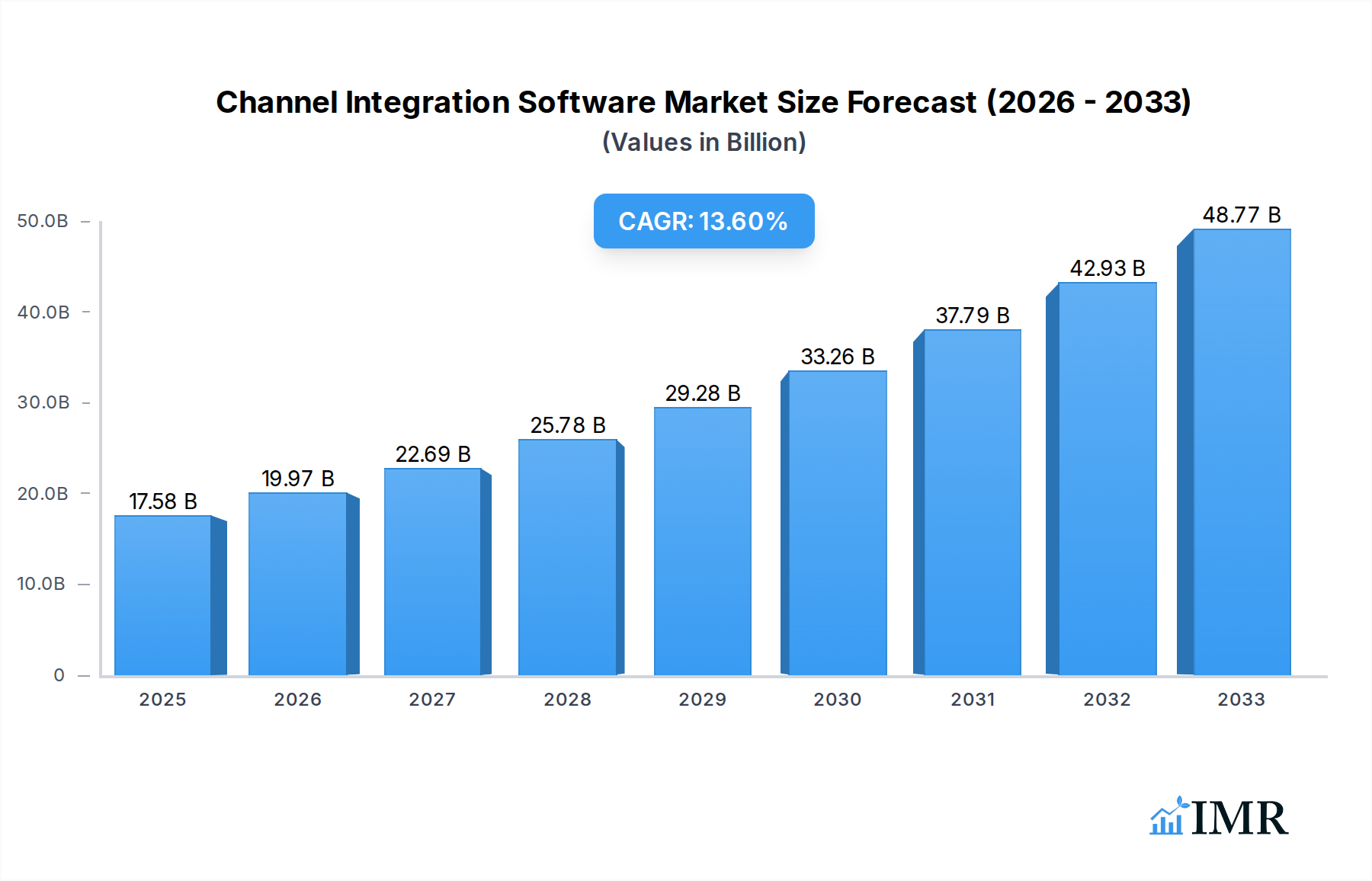

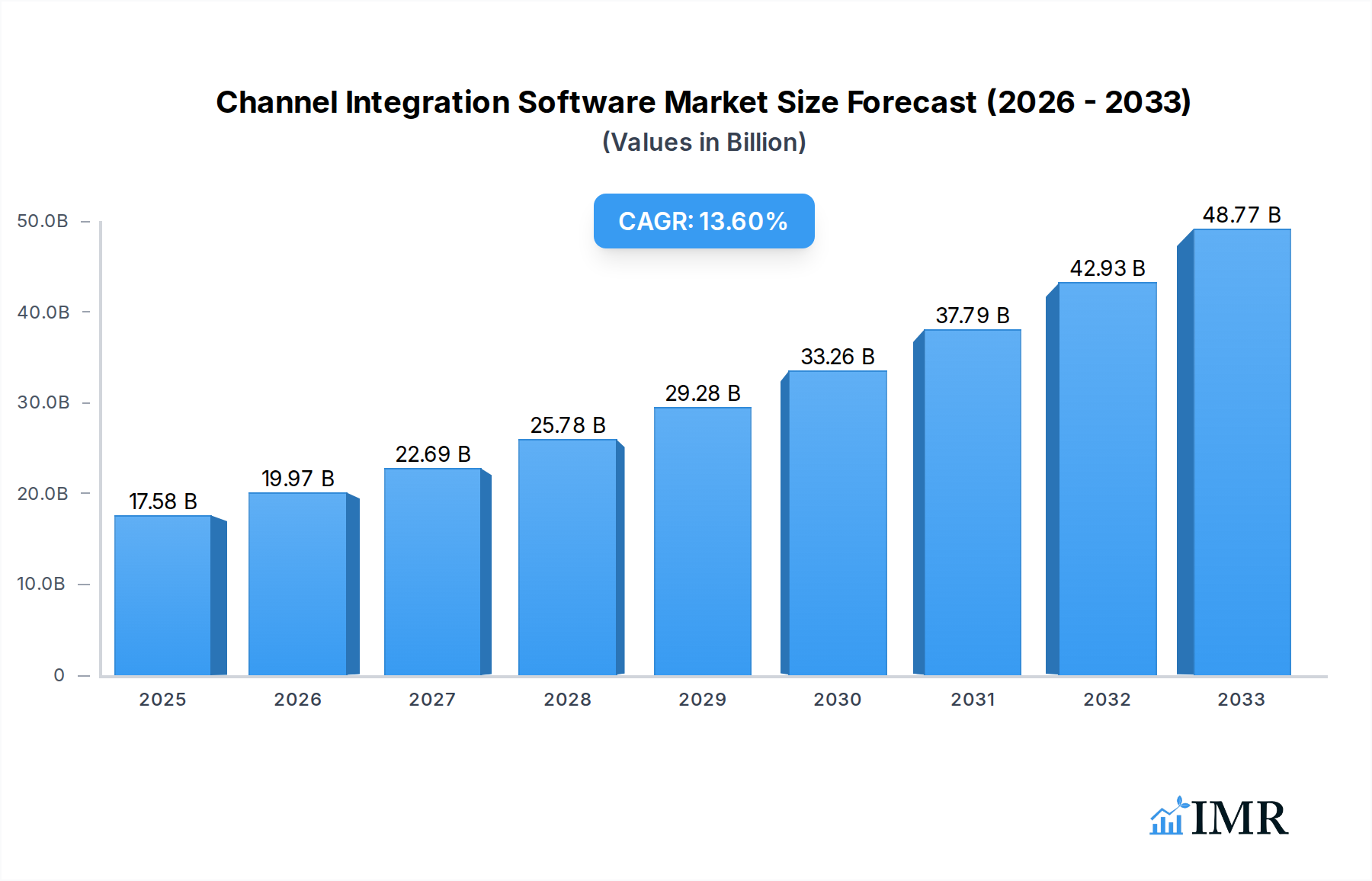

The Channel Integration Software market is poised for robust expansion, driven by the accelerating pace of digital transformation and the imperative for businesses to maintain a cohesive omnichannel presence. Valued at $17.58 billion in 2025, the market is projected to grow at an impressive Compound Annual Growth Rate (CAGR) of 13.6% through the forecast period (2025-2033). This growth is fundamentally fueled by the explosive growth of e-commerce, the increasing complexity of sales and marketing channels, and the critical need for unified data insights across disparate platforms. Both Small and Medium-sized Enterprises (SMEs) and large enterprises are increasingly adopting these solutions to streamline operations, enhance customer experiences, and optimize their go-to-market strategies. The shift towards cloud-based deployments is a significant driver, offering enhanced scalability, flexibility, and reduced infrastructure costs, making advanced integration accessible to a broader range of businesses.

Channel Integration Software Market Size (In Billion)

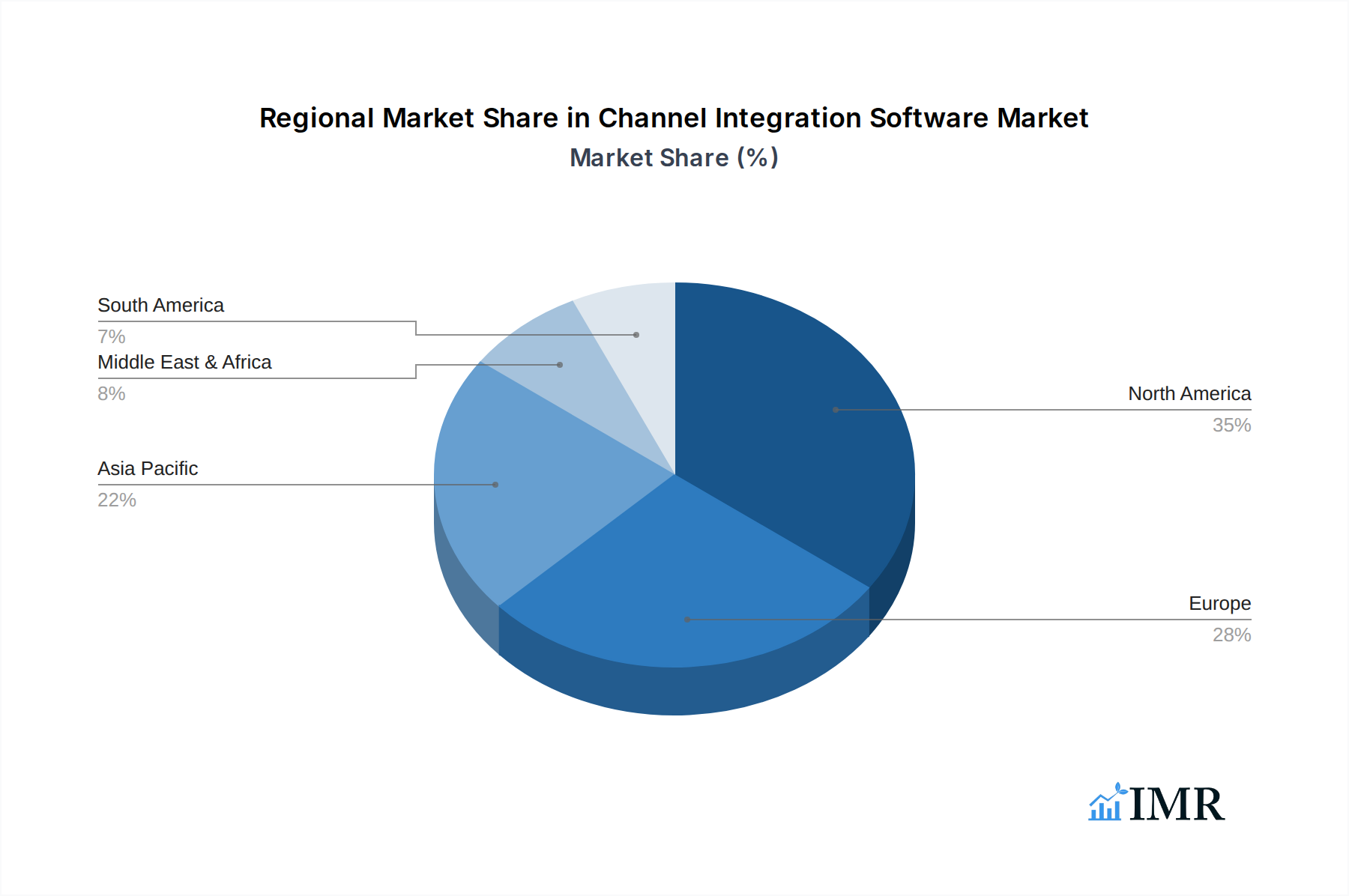

Key market trends include the deeper integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive analytics, personalized customer engagement, and automated workflow optimization. The adoption of API-first architectures is also gaining traction, enabling seamless connectivity and data exchange between various applications, from CRM and ERP systems to e-commerce platforms and social media channels. While the benefits are substantial, the market also navigates challenges such as the inherent complexity of integrating legacy systems, data security concerns, and the initial investment costs associated with advanced solutions. Leading companies like Salesforce, Adobe, Shopify, and SAP are continuously innovating to offer more intuitive, secure, and comprehensive platforms. Geographically, North America and Europe continue to hold significant market shares, while the Asia Pacific region is expected to witness the fastest growth, propelled by rapid digitalization and the burgeoning e-commerce landscape in emerging economies.

Channel Integration Software Company Market Share

This comprehensive report offers an unparalleled deep dive into the Channel Integration Software Market, a critical enabler of digital transformation and unified commerce. As businesses increasingly navigate complex multi-channel environments, the demand for robust API Integration, E-commerce Integration, and B2B Integration solutions has never been higher. This study meticulously analyzes the global landscape, providing strategic insights for industry professionals, investors, and technology leaders.

The Global Enterprise Software Market, the parent market, was valued at an estimated $650.0 billion in 2025, projected to reach $1,100.0 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 6.8%. Within this expansive ecosystem, the Global Channel Integration Software Market, the child market, is experiencing accelerated growth. Valued at $12.5 billion in 2025, it is forecast to expand significantly to $32.0 billion by 2033, demonstrating an impressive CAGR of 12.5% during the forecast period.

Our analysis spans a Study Period of 2019–2033, with 2025 serving as both the Base Year and Estimated Year, and a Forecast Period extending from 2025–2033. The Historical Period covers 2019–2024, offering a foundational understanding of market evolution. Key players like Salesforce, Adobe, Shopify, ChannelAdvisor, BigCommerce, NetSuite, Zoho, WooCommerce (Automattic), IBM, and SAP are meticulously examined, alongside crucial segments including Application (SMEs, Large Enterprises) and Types (Cloud-Based, On-Premises). Discover the driving forces behind Unified Commerce, Supply Chain Integration, and Digital Business Automation, and equip your strategy with foresight into the future of enterprise connectivity.

Channel Integration Software Market Dynamics & Structure

The Channel Integration Software Market is characterized by a dynamic structure influenced by rapid technological advancements, evolving regulatory landscapes, and a highly competitive environment. Market concentration is moderate, with the top five players collectively holding an estimated 48% of the global market share in 2025, indicating both established leadership and significant room for niche innovators. Technological innovation, particularly in AI, Machine Learning (ML), and blockchain, serves as a primary driver, enabling more intelligent data routing, predictive analytics for integration workflows, and enhanced security protocols for cross-channel transactions. These innovations address core pain points like data silos and latency, pushing the market towards real-time, event-driven architectures.

Regulatory frameworks, such as GDPR, CCPA, and emerging data sovereignty laws, significantly impact how data flows across integrated channels. Compliance requirements necessitate robust governance features within integration platforms, influencing product development and market adoption, particularly in regions with stringent data protection policies. Competitive product substitutes, ranging from custom-built API solutions to open-source integration tools, offer alternatives, yet often lack the scalability, comprehensive features, and support provided by dedicated commercial software. This keeps pressure on vendors to continuously enhance their offerings.

End-user demographics reveal a growing preference for cloud-based, flexible solutions among Small and Medium-sized Enterprises (SMEs) and a strong demand for enterprise-grade, scalable platforms from Large Enterprises seeking to unify complex ERP, CRM, and e-commerce systems. The shift towards omnichannel customer experiences and the proliferation of digital sales channels are significant demographic trends fueling demand. Mergers and acquisitions (M&A) are a prevalent trend, with over $18.5 billion in deals recorded between 2019 and 2024. Larger players acquire specialized integration capabilities, regional market presence, or customer bases, leading to market consolidation and the expansion of integrated platform offerings. Innovation barriers, such as the complexity of integrating legacy systems and overcoming interoperability challenges, remain, but are increasingly mitigated by low-code/no-code platforms and AI-assisted mapping tools.

Channel Integration Software Growth Trends & Insights

Leveraging in-depth market analysis and proprietary data, the Channel Integration Software market is poised for robust growth, driven by an escalating need for seamless digital operations. The market size has evolved significantly, expanding from $7.0 billion in 2019 to an estimated $12.5 billion in 2025, and is projected to reach $32.0 billion by 2033, reflecting an impressive CAGR of 12.5% during the forecast period. This trajectory is fueled by increasing adoption rates across diverse industries. Currently, an estimated 38% of global businesses are actively leveraging channel integration software, a figure expected to surpass 60% by the end of the forecast period as digital transformation initiatives mature.

Technological disruptions are a cornerstone of this growth. The pervasive adoption of API-first strategies, where organizations build their digital ecosystems around modular, interconnected APIs, is making integration a core business capability rather than an IT afterthought. Furthermore, the rise of Integration Platform as a Service (iPaaS) solutions offers flexible, scalable, and cloud-native integration capabilities, significantly lowering the barrier to entry for many businesses. Low-code/no-code integration platforms are democratizing access, allowing business users to configure integrations without extensive coding expertise, thereby accelerating deployment and innovation cycles.

Consumer behavior shifts are equally impactful. The modern consumer expects a unified, consistent, and personalized experience across all touchpoints, whether engaging via a website, mobile app, social media, or in-store. This demand for omnichannel interactions compels businesses to integrate their front-end and back-end systems, ensuring data consistency and real-time synchronization. The ability to track customer journeys, personalize recommendations, and streamline order fulfillment across disparate channels is now a competitive imperative. Businesses failing to adapt risk customer churn and diminished market relevance. The continuous evolution of e-commerce, the emergence of social commerce, and the increasing reliance on digital supply chains further underscore the critical role of channel integration software in enabling resilient and customer-centric operations.

Dominant Regions, Countries, or Segments in Channel Integration Software

The Cloud-Based segment and Large Enterprises application segment currently dominate the Channel Integration Software Market, with North America leading as the primary regional driver. In 2025, Cloud-Based solutions account for an estimated 72% of the market share, projected to grow to 85% by 2033, while Large Enterprises represent approximately 60% of the application market. North America holds about 40% of the global market share, with the Asia-Pacific (APAC) region emerging as the fastest-growing market with a projected CAGR of 14.8%.

Cloud-Based Dominance:

- Key Drivers:

- Scalability & Flexibility: Cloud-based platforms offer unparalleled scalability, allowing businesses to adapt quickly to fluctuating demands without significant capital expenditure.

- Reduced TCO: Lower total cost of ownership due to minimized infrastructure and maintenance requirements.

- Accessibility: Enables remote access and collaboration, crucial for distributed teams and global operations.

- Faster Deployment: Quick setup and integration with other cloud services accelerate time-to-market for new digital initiatives.

- Continuous Updates: Vendors provide regular updates and security patches, ensuring platforms remain current and secure.

- Dominance Factors: The inherent advantages of cloud technology align perfectly with the dynamic needs of channel integration, where agility, real-time data exchange, and seamless connectivity across diverse applications are paramount. The shift from monolithic on-premises systems to modular cloud services has made cloud-based integration a natural evolution, fostering a vibrant ecosystem of iPaaS and SaaS integration tools.

- Key Drivers:

Large Enterprises Segment:

- Key Drivers:

- Complex Ecosystems: Large enterprises typically manage vast, heterogeneous IT landscapes, necessitating robust integration to connect ERP, CRM, HR, supply chain, and e-commerce platforms.

- Digital Transformation Mandates: Significant investments in digital transformation initiatives drive the need for comprehensive integration to unlock data insights and automate processes.

- Omnichannel Strategies: Advanced omnichannel customer engagement and supply chain optimization strategies demand sophisticated, real-time data synchronization across numerous channels.

- Regulatory Compliance: The need to maintain data integrity and compliance across complex systems requires centralized integration governance.

- Dominance Factors: Large enterprises have the resources and strategic imperative to invest in sophisticated integration solutions that provide a unified view of their operations and customers. Their complex data environments and global presence necessitate robust, scalable, and secure integration platforms capable of handling high transaction volumes and diverse data types.

- Key Drivers:

North America's Leadership:

- Key Drivers:

- Technological Readiness: High adoption rates of cloud computing, advanced analytics, and enterprise software.

- Strong Economic Policies: Supportive regulatory environments and significant corporate IT spending.

- Innovation Hub: Presence of major technology players and a strong startup ecosystem fostering innovation in integration solutions.

- Mature Digital Economy: High penetration of e-commerce and advanced digital consumer behaviors driving the demand for seamless channel experiences.

- Dominance Factors: North America benefits from a mature digital infrastructure, early adoption of advanced business technologies, and a highly competitive market that encourages continuous innovation in channel integration. The region's large enterprise base and dynamic startup culture continue to drive investment and deployment of cutting-edge integration solutions.

- Key Drivers:

Channel Integration Software Product Landscape

The Channel Integration Software product landscape is rapidly evolving, characterized by innovation aimed at simplifying complex data flows and enhancing real-time connectivity. Key innovations include AI-driven mapping and automation tools that intelligently suggest data transformations and orchestrate workflows, significantly reducing manual effort. Platforms are increasingly offering pre-built connectors for popular business applications like Salesforce, Shopify, and SAP, enabling rapid deployment and seamless data synchronization. Unique selling propositions often center on low-code/no-code interfaces, empowering business users to manage integrations, and robust API management capabilities for secure and scalable external connections. Performance metrics highlight solutions that offer high throughput, minimal latency for real-time data exchange, and enterprise-grade security features like end-to-end encryption and compliance certifications. Technological advancements are focused on event-driven architectures, ensuring that data updates are immediately reflected across all integrated channels, crucial for achieving true unified commerce and efficient supply chain management.

Key Drivers, Barriers & Challenges in Channel Integration Software

Key Drivers:

- Technological Advancement: The explosion of APIs, the widespread adoption of cloud computing, and the growing demand for data analytics are primary drivers. Businesses require seamless data flow between SaaS applications, on-premises systems, and external partners to derive actionable insights.

- Economic Imperatives: Digital transformation initiatives, driven by the need for operational efficiency and cost savings through automation, propel market growth. Integrated channels reduce manual errors, optimize workflows, and enhance customer satisfaction, directly impacting profitability.

- Policy & Consumer Demand: The imperative for unified customer experiences across multiple touchpoints (web, mobile, social, in-store) and regulatory pressures for data governance and privacy drive the adoption of integrated platforms. Organizations must consolidate data to meet compliance and personalization demands.

Barriers & Challenges:

- Legacy System Interoperability: Integrating modern cloud-native solutions with entrenched, often proprietary, legacy systems presents significant technical hurdles and resource demands, leading to complex and costly migration or integration projects.

- Data Security & Governance: Managing data privacy, security, and compliance across diverse channels and geographical boundaries poses substantial regulatory and technical challenges. Breaches or non-compliance can have severe financial and reputational impacts.

- Skilled Talent Shortage: A scarcity of professionals with expertise in API management, data architecture, and integration platform implementation hampers adoption and effective utilization of advanced integration solutions, impacting project timelines and success rates.

- Competitive Pressure & Cost: The market faces pressure from custom development alternatives and open-source solutions, alongside the perceived high initial investment and ongoing maintenance costs of robust commercial integration software.

Emerging Opportunities in Channel Integration Software

Significant emerging opportunities in the Channel Integration Software market are driven by evolving technological landscapes and untapped market segments. Untapped markets include the vast number of small and medium-sized businesses (SMBs) in emerging economies that are rapidly digitizing but lack sophisticated integration solutions. These businesses seek affordable, easy-to-implement platforms to connect their e-commerce, CRM, and basic ERP systems. Innovative applications are expanding beyond traditional e-commerce and supply chain use cases to include IoT integration, enabling seamless data flow from connected devices to backend systems for smart factories, logistics, and retail. The rise of the metaverse commerce also presents a new frontier for integrating virtual and physical customer interactions. Evolving consumer preferences for hyper-personalization and seamless cross-channel experiences across all digital and physical touchpoints will continue to fuel demand for advanced, AI-driven integration capabilities that deliver a truly unified customer journey.

Growth Accelerators in the Channel Integration Software Industry

The Channel Integration Software industry is propelled by several key accelerators driving long-term growth and market expansion. Foremost among these are technological breakthroughs in artificial intelligence and machine learning, which are enhancing integration platforms with capabilities for predictive error detection, automated data mapping, and intelligent workflow orchestration, dramatically improving efficiency and reducing manual effort. The increasing adoption of blockchain for secure data exchange between disparate systems, particularly in supply chain and financial integrations, is also fostering trust and transparency. Strategic partnerships between integration platform providers and cloud hyperscalers (e.g., AWS, Azure, Google Cloud), as well as leading SaaS application vendors (e.g., Salesforce, SAP), are creating robust ecosystems of pre-built connectors and joint solutions, simplifying deployment and extending market reach. Furthermore, market expansion strategies targeting specific vertical industries (e.g., healthcare, finance, manufacturing) with tailored integration solutions, along with a focus on geographic expansion into rapidly digitizing regions like APAC and Latin America, are opening up vast new revenue streams and fostering widespread adoption. These catalysts collectively ensure sustained innovation and broader market penetration for channel integration software.

Key Players Shaping the Channel Integration Software Market

- Salesforce

- Adobe

- Shopify

- ChannelAdvisor

- BigCommerce

- NetSuite

- Zoho

- WooCommerce (Automattic)

- IBM

- SAP

Notable Milestones in Channel Integration Software Sector

- 2020 Q2: Salesforce completes acquisition of MuleSoft, significantly enhancing its API integration and iPaaS capabilities, solidifying its position in the enterprise integration market.

- 2021 Q4: Adobe unveils its headless commerce API suite, empowering businesses with greater flexibility in frontend development and driving demand for robust backend channel integration.

- 2022 Q3: Shopify announces expanded B2B e-commerce functionalities, necessitating deeper integration with ERP and CRM systems for its merchant base.

- 2023 Q1: IBM introduces an AI-powered integration hub, leveraging advanced analytics to streamline complex enterprise application integrations and improve data flow efficiency.

- 2024 Q2: Major regulatory updates regarding cross-border data sharing (e.g., EU-US Data Privacy Framework) prompt significant platform enhancements focusing on compliant data transfer and governance for global integration solutions.

In-Depth Channel Integration Software Market Outlook

The Channel Integration Software Market is poised for continued robust growth, driven by an unwavering global commitment to digital transformation and the increasing complexity of multi-channel business operations. The growth accelerators—primarily AI/ML advancements, strategic ecosystem partnerships, and targeted vertical/geographic expansion—will significantly shape the future market potential. We anticipate sustained innovation in low-code/no-code platforms, making sophisticated integration accessible to a broader range of businesses, including SMEs in emerging markets. The strategic opportunities lie in developing highly specialized, industry-specific integration solutions, leveraging predictive analytics for proactive issue resolution, and building resilient, secure platforms that can adapt to evolving data privacy regulations. The trajectory indicates a shift towards truly intelligent, self-optimizing integration systems that will become indispensable for achieving competitive advantage and driving operational excellence in an interconnected global economy.

Channel Integration Software Segmentation

-

1. Application

- 1.1. SMEs

- 1.2. Large Enterprises

-

2. Types

- 2.1. Cloud-Based

- 2.2. On-Premises

Channel Integration Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Channel Integration Software Regional Market Share

Geographic Coverage of Channel Integration Software

Channel Integration Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. SMEs

- 5.1.2. Large Enterprises

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud-Based

- 5.2.2. On-Premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Channel Integration Software Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. SMEs

- 6.1.2. Large Enterprises

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud-Based

- 6.2.2. On-Premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Channel Integration Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. SMEs

- 7.1.2. Large Enterprises

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud-Based

- 7.2.2. On-Premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Channel Integration Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. SMEs

- 8.1.2. Large Enterprises

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud-Based

- 8.2.2. On-Premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Channel Integration Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. SMEs

- 9.1.2. Large Enterprises

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud-Based

- 9.2.2. On-Premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Channel Integration Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. SMEs

- 10.1.2. Large Enterprises

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud-Based

- 10.2.2. On-Premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Channel Integration Software Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. SMEs

- 11.1.2. Large Enterprises

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Cloud-Based

- 11.2.2. On-Premises

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Salesforce

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Adobe

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Shopify

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ChannelAdvisor

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BigCommerce

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NetSuite

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Zoho

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 WooCommerce (Automattic)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 IBM

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SAP

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Salesforce

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Channel Integration Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Channel Integration Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Channel Integration Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Channel Integration Software Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Channel Integration Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Channel Integration Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Channel Integration Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Channel Integration Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Channel Integration Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Channel Integration Software Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Channel Integration Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Channel Integration Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Channel Integration Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Channel Integration Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Channel Integration Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Channel Integration Software Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Channel Integration Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Channel Integration Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Channel Integration Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Channel Integration Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Channel Integration Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Channel Integration Software Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Channel Integration Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Channel Integration Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Channel Integration Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Channel Integration Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Channel Integration Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Channel Integration Software Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Channel Integration Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Channel Integration Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Channel Integration Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Channel Integration Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Channel Integration Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Channel Integration Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Channel Integration Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Channel Integration Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Channel Integration Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Channel Integration Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Channel Integration Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Channel Integration Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Channel Integration Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Channel Integration Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Channel Integration Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Channel Integration Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Channel Integration Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Channel Integration Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Channel Integration Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Channel Integration Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Channel Integration Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Channel Integration Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Channel Integration Software?

The projected CAGR is approximately 13.6%.

2. Which companies are prominent players in the Channel Integration Software?

Key companies in the market include Salesforce, Adobe, Shopify, ChannelAdvisor, BigCommerce, NetSuite, Zoho, WooCommerce (Automattic), IBM, SAP.

3. What are the main segments of the Channel Integration Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Channel Integration Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Channel Integration Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Channel Integration Software?

To stay informed about further developments, trends, and reports in the Channel Integration Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence