Key Insights

The cloud computing chip market is experiencing significant expansion, propelled by the increasing demand for high-performance computing in data centers and the rapid adoption of Artificial Intelligence (AI) and Machine Learning (ML) technologies. With a current market size of $723 billion in 2025, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% from 2025 to 2033. Key growth drivers include the widespread adoption of cloud services across industries, the necessity for enhanced data center processing speeds and energy efficiency, and the escalating complexity of AI workloads requiring specialized hardware. Leading semiconductor manufacturers are making substantial R&D investments to advance chip capabilities and meet evolving market demands, fostering a competitive yet innovative ecosystem.

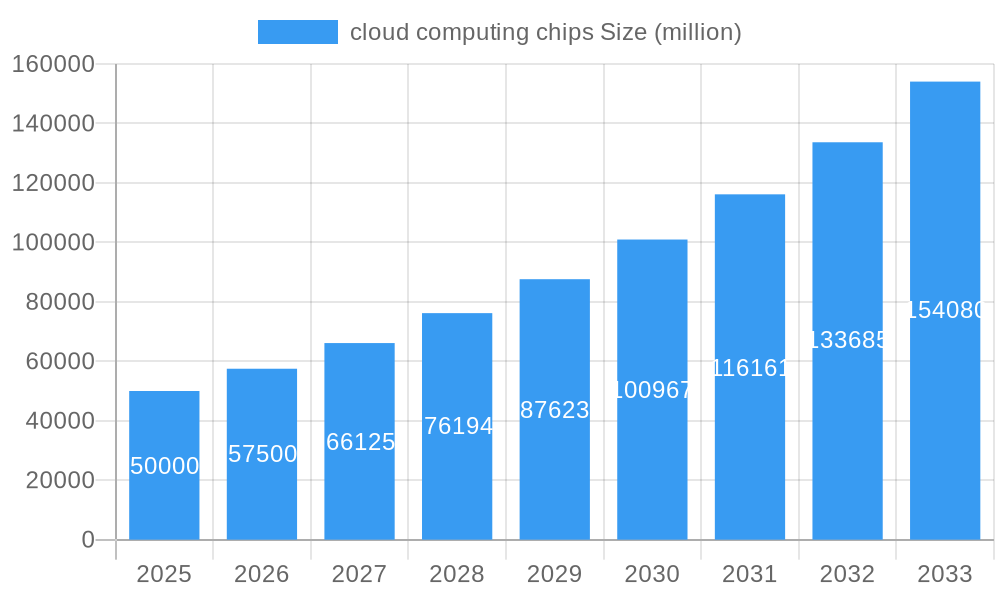

cloud computing chips Market Size (In Billion)

This dynamic environment is further shaped by emerging specialized chip providers focusing on AI acceleration. While challenges such as high development costs and supply chain vulnerabilities exist, industry-wide investments and collaborations are actively mitigating these concerns. The market is segmented by chip type (CPUs, GPUs, FPGAs, ASICs), application (AI/ML, cloud computing, high-performance computing), and geography. North America and Asia-Pacific currently lead the market, with other regions demonstrating considerable growth potential. The forecast period from 2025 to 2033 indicates sustained market expansion.

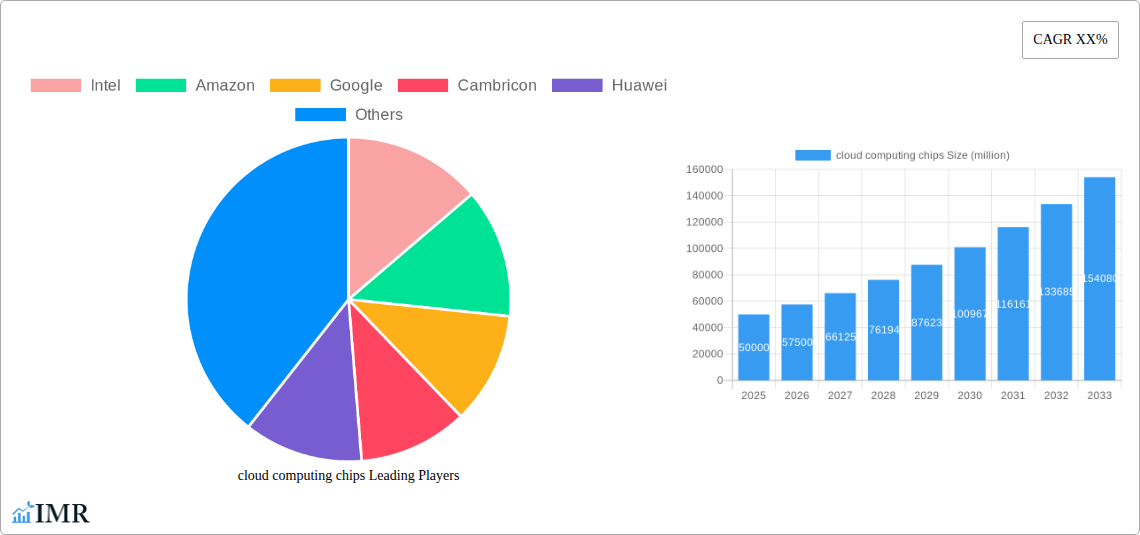

cloud computing chips Company Market Share

Cloud Computing Chips Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the global cloud computing chips market, encompassing market dynamics, growth trends, regional dominance, product landscape, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report utilizes a robust methodology, combining extensive primary and secondary research to deliver actionable insights for industry professionals, investors, and strategists. The market is segmented by key players such as Intel, Amazon, Google, and others, offering a granular understanding of the competitive landscape and market share distribution. The parent market is the overall semiconductor industry, while the child market is specifically cloud-based data centers and servers.

Cloud Computing Chips Market Dynamics & Structure

The cloud computing chips market is characterized by intense competition among major players, driving rapid technological innovation and continuous product improvements. Market concentration is high, with a few dominant players controlling a significant portion of the market share. Intel, AMD, and NVIDIA hold substantial market share, estimated at xx%, xx%, and xx% respectively in 2025. However, emerging players like Cambricon and Alibaba are rapidly gaining traction, increasing competitive intensity. Regulatory frameworks, particularly concerning data privacy and security, significantly influence market dynamics. The increasing demand for high-performance computing (HPC) in cloud environments is a key driver, while the emergence of alternative technologies, such as specialized AI accelerators, presents a challenge. M&A activity is significant, with xx major deals recorded during the historical period (2019-2024), primarily focused on acquiring specialized chip design companies and strengthening technological capabilities.

- Market Concentration: High, with top 5 players controlling approximately xx% of the market in 2025.

- Technological Innovation Drivers: Demand for higher processing power, AI acceleration, and energy efficiency.

- Regulatory Frameworks: Data privacy regulations (GDPR, CCPA) influence chip design and deployment.

- Competitive Product Substitutes: Specialized AI accelerators, FPGAs, and ASICs pose a competitive threat.

- End-User Demographics: Primarily large hyperscale cloud providers (Amazon, Google, Microsoft, etc.), followed by enterprise clients.

- M&A Trends: Focus on acquiring specialized chip design companies and strengthening technology portfolios. Average deal value in 2024 was approximately $xx million.

Cloud Computing Chips Growth Trends & Insights

The global cloud computing chips market experienced robust growth during the historical period (2019-2024), primarily driven by the exponential growth of cloud computing adoption across diverse sectors. The market size expanded from approximately $xx million in 2019 to $xx million in 2024, exhibiting a Compound Annual Growth Rate (CAGR) of xx%. This growth is projected to continue, reaching $xx million by 2025 and $xx million by 2033, driven by increasing data center deployments, rising demand for AI and machine learning applications, and the ongoing expansion of the Internet of Things (IoT). Market penetration within the enterprise segment is expected to increase from xx% in 2024 to xx% by 2033, fueled by the increasing adoption of cloud-native applications and hybrid cloud strategies. Technological disruptions, such as the rise of chiplets and 3D packaging, are further propelling market growth, enabling higher performance and density while reducing manufacturing costs.

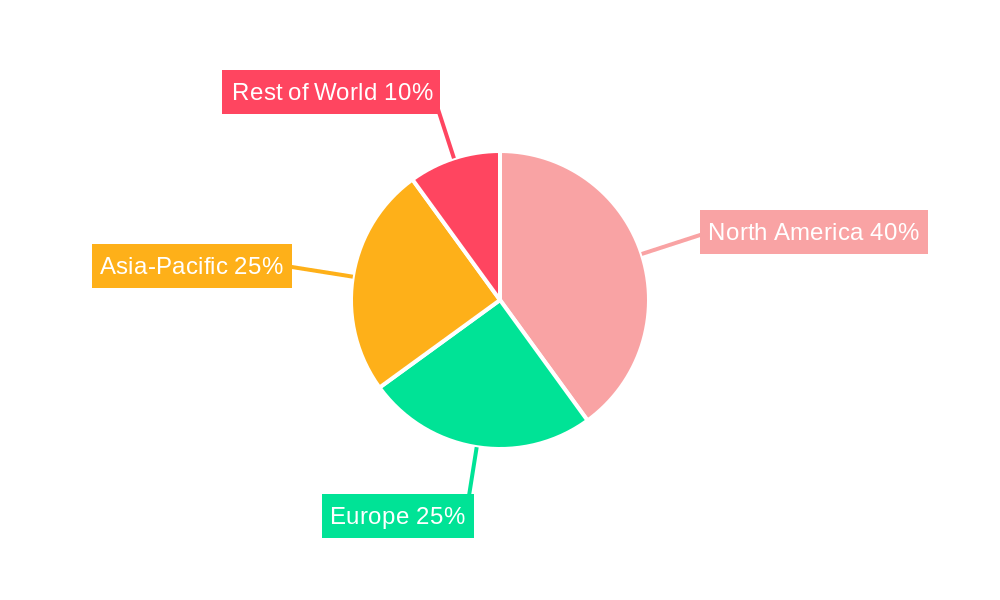

Dominant Regions, Countries, or Segments in Cloud Computing Chips

North America currently holds the largest market share in cloud computing chips, driven by the presence of major hyperscale data centers and a strong technological ecosystem. This region is estimated to account for approximately xx% of the global market in 2025. However, the Asia-Pacific region is exhibiting the fastest growth rate, projected to expand at a CAGR of xx% during the forecast period (2025-2033). This rapid growth is primarily fueled by burgeoning cloud infrastructure investments in countries like China and India, coupled with supportive government policies promoting digital transformation initiatives. Within segments, high-performance computing (HPC) and AI accelerators are experiencing the most significant growth, fueled by increasing adoption in areas such as scientific research, financial modeling, and autonomous driving.

- North America Dominance: Strong presence of hyperscale data centers and technological innovation.

- Asia-Pacific Growth: Rapid expansion of cloud infrastructure and government support for digital transformation.

- Europe's Steady Growth: Driven by increasing adoption of cloud services across various sectors.

- High-Performance Computing (HPC) and AI Accelerators: Fastest-growing segments, propelled by demand in various industries.

- Market Share Distribution (2025): North America (xx%), Asia-Pacific (xx%), Europe (xx%), Rest of World (xx%).

Cloud Computing Chips Product Landscape

Cloud computing chips encompass a broad range of products, including CPUs, GPUs, FPGAs, and specialized AI accelerators. Continuous innovation focuses on enhancing performance, energy efficiency, and security. Unique selling propositions often center around specialized architectures optimized for specific workloads, such as AI inference or high-performance computing. Advancements in chip manufacturing technologies, such as 3D packaging and EUV lithography, are enabling higher transistor densities and improved performance.

Key Drivers, Barriers & Challenges in Cloud Computing Chips

Key Drivers: The increasing demand for cloud computing services, fueled by digital transformation across industries, is a primary driver. The rising adoption of AI/ML workloads demanding substantial processing power is another significant factor. Government initiatives supporting cloud infrastructure development also contribute.

Challenges: Supply chain disruptions, particularly concerning semiconductor manufacturing, can impact production and lead times. Regulatory hurdles concerning data privacy and security can limit market expansion. Intense competition among chip vendors creates price pressures and necessitates continuous innovation. The high cost of research and development poses a significant barrier to entry for new players.

Emerging Opportunities in Cloud Computing Chips

Untapped markets in developing economies present significant opportunities for growth. The increasing demand for edge computing, requiring specialized low-power chips, is creating new avenues for innovation. The rising adoption of serverless computing and containerization technologies also opens new market possibilities.

Growth Accelerators in the cloud computing chips Industry

Technological breakthroughs in chip design and manufacturing, such as advanced packaging techniques and innovative memory architectures, are pivotal for accelerating market growth. Strategic partnerships between chip manufacturers and cloud providers can drive adoption and optimize performance. Expansion into new geographic markets and developing applications for emerging technologies (e.g., quantum computing) also contribute to market growth.

Notable Milestones in cloud computing chips Sector

- 2020, Q3: AMD launched its EPYC Milan processors, significantly boosting performance in cloud data centers.

- 2021, Q1: NVIDIA announced its A100 GPU, a significant leap in AI processing capabilities for cloud deployments.

- 2022, Q2: Intel and Qualcomm announced a strategic partnership for developing cloud-based solutions.

- 2023, Q4: Amazon launched a new line of custom-designed chips for its cloud infrastructure. (Specific examples of other milestones can be added depending on available data)

In-Depth cloud computing chips Market Outlook

The cloud computing chips market is poised for sustained growth, driven by continued cloud adoption and innovation in chip architectures. Strategic opportunities lie in developing specialized chips for emerging technologies like quantum computing and edge AI, as well as expanding into new geographical markets. The ongoing evolution of cloud computing architectures, along with the increasing demand for high-performance and energy-efficient chips, will shape the future market landscape. Companies focusing on innovation, strategic partnerships, and efficient supply chain management will be well-positioned to capitalize on the immense growth potential.

cloud computing chips Segmentation

-

1. Application

- 1.1. BFSI

- 1.2. Manufacturing

- 1.3. Government

- 1.4. IT & Telecom

- 1.5. Retail

- 1.6. Transportation

- 1.7. Energy & Utilities

- 1.8. Others

-

2. Types

- 2.1. Graphics Processing Unit (GPU)

- 2.2. Field Programmable Gate Array (FPGA)

- 2.3. Application-Specific Integrated Circuit (ASIC)

cloud computing chips Segmentation By Geography

- 1. CA

cloud computing chips Regional Market Share

Geographic Coverage of cloud computing chips

cloud computing chips REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. BFSI

- 5.1.2. Manufacturing

- 5.1.3. Government

- 5.1.4. IT & Telecom

- 5.1.5. Retail

- 5.1.6. Transportation

- 5.1.7. Energy & Utilities

- 5.1.8. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Graphics Processing Unit (GPU)

- 5.2.2. Field Programmable Gate Array (FPGA)

- 5.2.3. Application-Specific Integrated Circuit (ASIC)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. cloud computing chips Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. BFSI

- 6.1.2. Manufacturing

- 6.1.3. Government

- 6.1.4. IT & Telecom

- 6.1.5. Retail

- 6.1.6. Transportation

- 6.1.7. Energy & Utilities

- 6.1.8. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Graphics Processing Unit (GPU)

- 6.2.2. Field Programmable Gate Array (FPGA)

- 6.2.3. Application-Specific Integrated Circuit (ASIC)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Intel

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Amazon

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Google

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Cambricon

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Huawei

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Microsoft

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Baidu

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 AMD

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 NVIDIA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Xilinx

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Alibaba

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Unisoc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Samsung Electronics

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Intel

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: cloud computing chips Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: cloud computing chips Share (%) by Company 2025

List of Tables

- Table 1: cloud computing chips Revenue billion Forecast, by Application 2020 & 2033

- Table 2: cloud computing chips Revenue billion Forecast, by Types 2020 & 2033

- Table 3: cloud computing chips Revenue billion Forecast, by Region 2020 & 2033

- Table 4: cloud computing chips Revenue billion Forecast, by Application 2020 & 2033

- Table 5: cloud computing chips Revenue billion Forecast, by Types 2020 & 2033

- Table 6: cloud computing chips Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the cloud computing chips?

The projected CAGR is approximately 21.5%.

2. Which companies are prominent players in the cloud computing chips?

Key companies in the market include Intel, Amazon, Google, Cambricon, Huawei, Microsoft, Baidu, AMD, NVIDIA, Xilinx, Alibaba, Unisoc, Samsung Electronics.

3. What are the main segments of the cloud computing chips?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 723 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "cloud computing chips," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the cloud computing chips report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the cloud computing chips?

To stay informed about further developments, trends, and reports in the cloud computing chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence