Key Insights

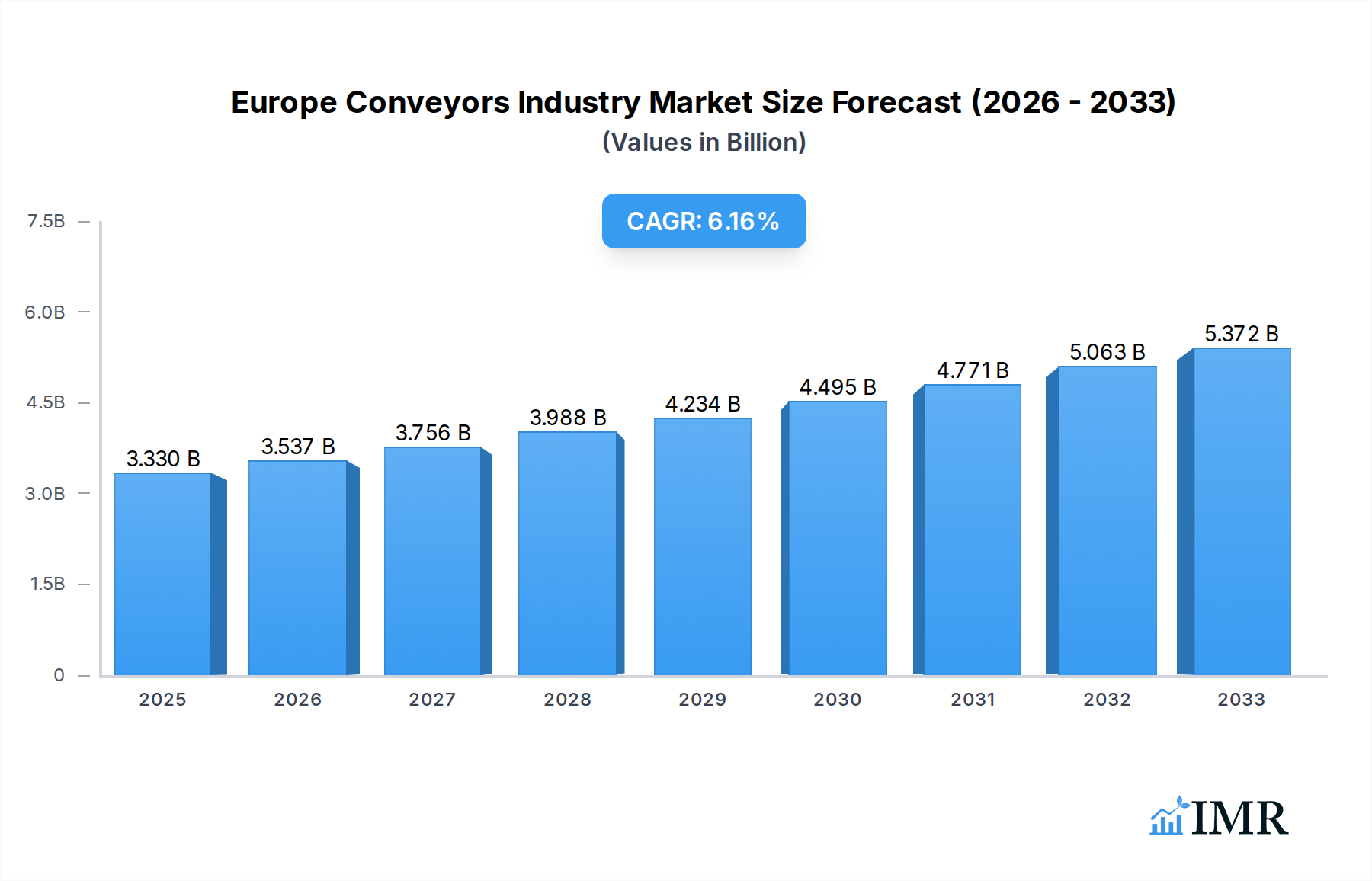

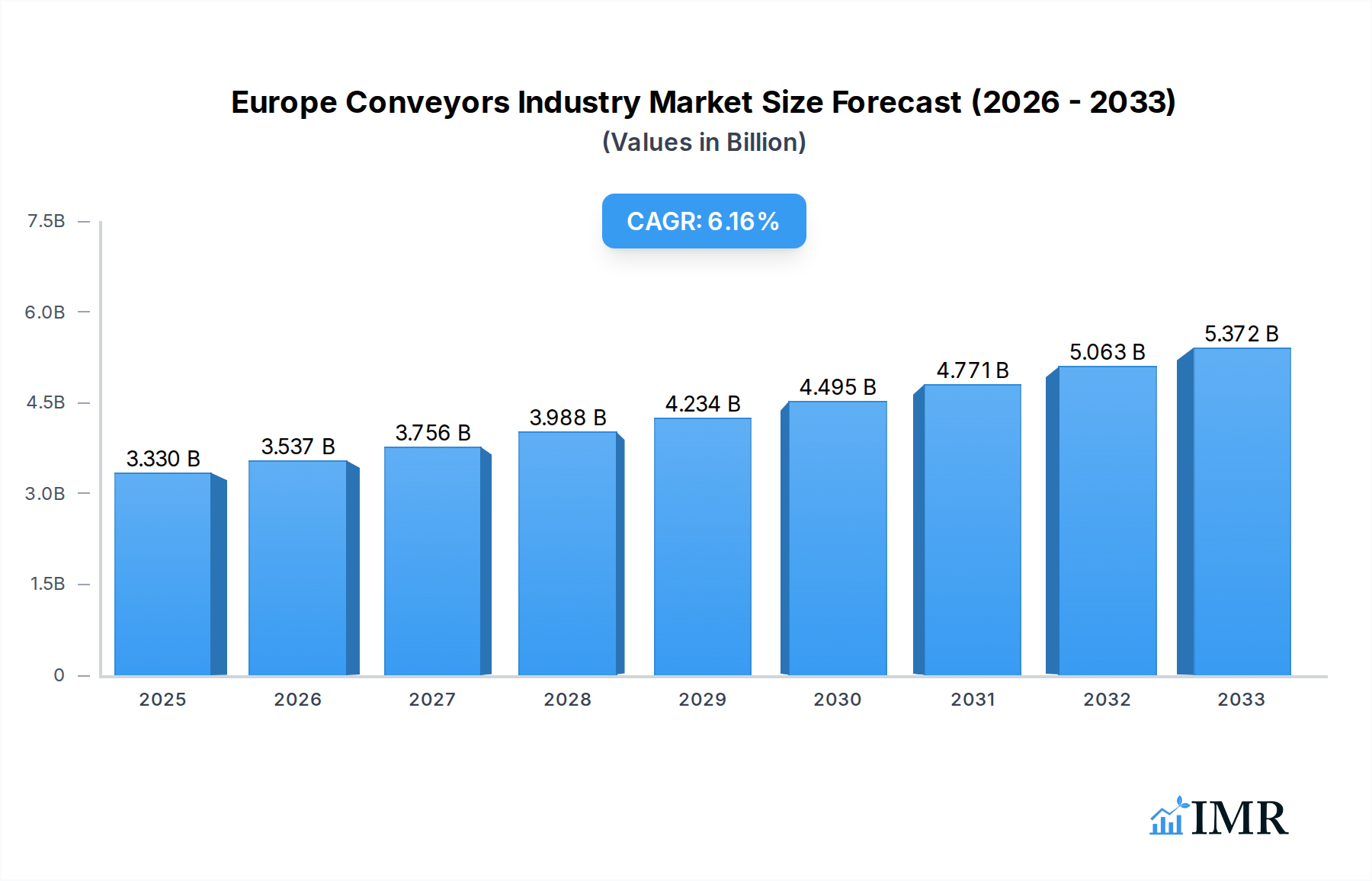

The European conveyor systems market is poised for significant expansion, projected to reach a value of $3.33 billion in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 6.26% anticipated over the forecast period of 2025-2033. The increasing adoption of automation across various industrial sectors, driven by the need for enhanced operational efficiency, reduced labor costs, and improved safety standards, is a primary catalyst. Industries such as manufacturing, automotive, and retail are heavily investing in advanced conveyor solutions to streamline their supply chains and logistics operations. Furthermore, the burgeoning e-commerce sector is creating sustained demand for sophisticated sorting and handling systems, especially in warehousing and distribution centers. The expansion of infrastructure projects, particularly in logistics hubs and airports, is also contributing to the market's upward trajectory, with a growing emphasis on integrated and intelligent conveyor technologies.

Europe Conveyors Industry Market Size (In Billion)

Key trends shaping the European conveyor market include the integration of Artificial Intelligence (AI) and the Internet of Things (IoT) for predictive maintenance and real-time performance monitoring, alongside a rise in flexible and modular conveyor designs that can be easily reconfigured to adapt to changing production needs. While the market enjoys strong growth drivers, certain restraints, such as the high initial investment cost for advanced systems and the complexity of integrating new technologies with legacy infrastructure, need to be addressed. However, the long-term benefits in terms of productivity and cost savings are expected to outweigh these challenges, driving widespread adoption. The diverse range of end-user industries, from food and beverage to pharmaceuticals and mining, further solidifies the market's resilience and growth potential. Prominent companies like KNAAP AG, Interroll Holding AG, and BEUMER Group are at the forefront, innovating and expanding their product portfolios to meet evolving market demands.

Europe Conveyors Industry Company Market Share

Here's a comprehensive, SEO-optimized report description for the Europe Conveyors Industry, designed for immediate use without modification:

Europe Conveyors Industry Market Dynamics & Structure

The Europe Conveyors Industry is characterized by a dynamic interplay of technological advancements, evolving end-user demands, and a concentrated competitive landscape. Market concentration is moderate, with key players like KNAAP AG, Interroll Holding AG, BEUMER Group GmbH & Co KG, KUKA AG (Swisslog AG), and Vanderlande Industries BV holding significant shares. Technological innovation is a primary driver, fueled by the need for increased efficiency, automation, and reduced operational costs across diverse sectors. Key innovations focus on smart conveyor systems, IoT integration for predictive maintenance, and advanced robotics for material handling. Regulatory frameworks, particularly concerning workplace safety and environmental standards, are influencing product design and implementation. Competitive product substitutes, such as automated guided vehicles (AGVs) and drones, are emerging, but traditional conveyor systems maintain dominance due to their proven reliability and scalability. End-user demographics are shifting, with a growing demand for customized solutions tailored to specific industry needs, particularly in the booming e-commerce and pharmaceutical sectors. Mergers and acquisitions (M&A) activity is moderate, often driven by strategic acquisitions to expand product portfolios or gain market access. For instance, the acquisition of Swisslog AG by KUKA AG significantly bolstered KUKA's automation capabilities within the logistics sector. The market is projected to reach approximately $28.5 billion in 2025, with steady growth anticipated.

- Market Concentration: Moderate, with a few dominant players and a growing number of niche providers.

- Technological Innovation: Driven by automation, IoT, AI integration, and smart logistics solutions.

- Regulatory Frameworks: Stringent safety and environmental regulations shaping product development.

- Competitive Substitutes: AGVs, drones, and advanced robotics posing emerging competition.

- End-User Demographics: Increasing demand for specialized, high-throughput, and integrated systems.

- M&A Trends: Strategic acquisitions focused on technology integration and market expansion.

Europe Conveyors Industry Growth Trends & Insights

The Europe Conveyors Industry is poised for robust growth over the forecast period, driven by an escalating demand for automated material handling solutions across a multitude of end-user industries. The market size is anticipated to expand from an estimated $27.1 billion in 2024 to approximately $41.8 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of around 4.9% during the forecast period (2025-2033). Adoption rates for advanced conveyor technologies are accelerating, propelled by the relentless pursuit of operational efficiency, labor cost optimization, and enhanced supply chain agility. Technological disruptions are at the forefront, with the integration of Artificial Intelligence (AI) and the Internet of Things (IoT) revolutionizing conveyor system capabilities. These advancements enable real-time monitoring, predictive maintenance, and dynamic route optimization, significantly reducing downtime and improving overall productivity. Consumer behavior shifts, particularly the surge in e-commerce and the increasing complexity of pharmaceutical supply chains, are directly impacting the demand for sophisticated conveyor solutions capable of handling higher volumes and diverse product types with greater precision. The need for faster order fulfillment, reduced return rates, and stringent product integrity in sectors like food and beverage and pharmaceuticals are compelling businesses to invest in cutting-edge conveyor systems. Furthermore, the ongoing trend towards industry 4.0 and smart manufacturing environments necessitates integrated automation solutions, where conveyors play a pivotal role as the backbone of internal logistics. The market penetration of automated conveyor systems is expected to deepen as businesses increasingly recognize their long-term return on investment and competitive advantages. The transition from manual handling to automated processes is no longer a luxury but a necessity for companies aiming to remain competitive in the evolving European market. The development of modular and flexible conveyor systems also caters to the changing needs of manufacturing and logistics, allowing for easy reconfiguration and adaptation to new production lines or warehouse layouts. This adaptability is a key growth driver in a market influenced by economic fluctuations and evolving business models. The continuous drive for sustainability is also influencing conveyor design, with an emphasis on energy-efficient motors and materials, further contributing to market expansion as companies seek to reduce their environmental footprint.

Dominant Regions, Countries, or Segments in Europe Conveyors Industry

Within the dynamic Europe Conveyors Industry, the Manufacturing end-user segment stands out as a primary growth engine, consistently driving significant market expansion. This dominance is underpinned by the pervasive need for efficient material flow, automation, and process optimization across a vast array of manufacturing sub-sectors. Germany, as a manufacturing powerhouse, spearheads this trend, exhibiting strong demand for advanced conveyor systems due to its established automotive, machinery, and chemical industries. Economic policies in Germany, which prioritize industrial competitiveness and innovation, further bolster the adoption of sophisticated material handling solutions. The automotive sector within manufacturing, in particular, relies heavily on automated assembly lines and just-in-time production, making robust and reliable conveyor systems indispensable. The market share for conveyor solutions in the manufacturing sector is estimated to represent approximately 25% of the total European market in 2025, with a projected CAGR of 5.2% during the forecast period.

- Dominant Segment: Manufacturing End-User Industry.

- Key Drivers in Manufacturing:

- Need for increased production efficiency and throughput.

- Reduction of labor costs and improved worker safety.

- Adoption of Industry 4.0 and smart manufacturing principles.

- Demand for highly automated and integrated production lines.

- Just-in-time and lean manufacturing practices.

- Leading Country: Germany, due to its strong industrial base, particularly in automotive and machinery.

- Economic Policies Supporting Growth: Government incentives for automation, investment in R&D, and trade policies favoring industrial exports.

- Growth Potential: High, driven by ongoing automation initiatives and the need to maintain global competitiveness.

Another significant contributor to market growth is the Airport segment, driven by the increasing volume of air travel and the necessity for efficient baggage handling and cargo logistics. Europe's extensive network of international airports necessitates sophisticated and high-speed conveyor systems to manage passenger flow, baggage screening, and cargo operations. The ongoing modernization of airport infrastructure across the continent, coupled with the expansion of air cargo services, further fuels demand. Market share for airport conveyors is estimated at 18% in 2025, with a projected CAGR of 4.7%.

- Key Drivers in Airports:

- Rising passenger and cargo traffic volumes.

- Need for efficient baggage handling and sorting systems.

- Implementation of advanced security screening technologies.

- Airport infrastructure upgrades and expansions.

- Focus on passenger experience and operational efficiency.

- Growth Potential: Significant, tied to global aviation trends and airport development projects.

The Retail sector, particularly driven by the e-commerce boom, is also a critical segment. Online retail growth necessitates efficient warehousing and distribution operations, with automated conveyor systems playing a crucial role in order fulfillment and returns processing. The demand for rapid delivery services is a key catalyst. Market share for retail conveyors is estimated at 15% in 2025, with a projected CAGR of 5.1%.

- Key Drivers in Retail:

- Explosive growth of e-commerce and online retail.

- Demand for faster order picking and packing.

- Need for efficient warehouse and distribution center operations.

- Management of increasing returns volumes.

- Personalization and customization of deliveries.

- Growth Potential: Very high, directly correlated with e-commerce penetration and consumer purchasing habits.

Furthermore, the Food and Beverage and Pharmaceuticals sectors are vital, characterized by stringent hygiene requirements, specialized handling needs, and the imperative for traceability and regulatory compliance. These industries demand hygienic, robust, and often integrated conveyor solutions to ensure product safety and quality. Market share for Food & Beverage is approximately 12% and for Pharmaceuticals is 10% in 2025, with respective CAGRs of 4.5% and 5.0%.

- Key Drivers in Food & Beverage:

- Demand for automated processing and packaging.

- Strict hygiene and safety regulations.

- Need for efficient product handling and sorting.

- Traceability requirements throughout the supply chain.

- Key Drivers in Pharmaceuticals:

- Stringent regulatory compliance and quality control.

- Demand for sterile and contamination-free environments.

- Need for precise and gentle product handling.

- Growth of biologics and personalized medicine.

Europe Conveyors Industry Product Landscape

The Europe Conveyors Industry product landscape is characterized by a diverse range of technologies designed to meet specific material handling needs. Belt conveyors remain a cornerstone, offering versatile solutions for transporting bulk materials and individual items, with innovations focusing on increased durability, energy efficiency, and specialized coatings for food-grade or high-temperature applications. Roller conveyors are widely adopted for package and unit handling, featuring powered and gravity-driven options, with advancements in modularity for flexible warehouse layouts. Pallet conveyors are crucial for logistics and warehousing, designed for heavy loads and integrated into automated storage and retrieval systems (AS/RS). Overhead conveyors are utilized in manufacturing and assembly lines for continuous flow and efficient space utilization, often integrated with robotics. Product innovations are centered on smart integration, including IoT sensors for real-time performance monitoring, predictive maintenance capabilities, and improved safety features. Performance metrics such as throughput capacity, energy consumption, and uptime are key considerations, driving the development of more efficient and reliable systems.

Key Drivers, Barriers & Challenges in Europe Conveyors Industry

The Europe Conveyors Industry is propelled by several key drivers, including the relentless pursuit of operational efficiency and cost reduction through automation, the burgeoning e-commerce sector demanding faster and more accurate order fulfillment, and the increasing adoption of Industry 4.0 principles for smart manufacturing. Technological advancements in AI, IoT, and robotics are enabling more sophisticated and integrated conveyor solutions.

However, significant barriers and challenges exist. High initial investment costs for advanced automated systems can be a restraint, particularly for small and medium-sized enterprises. Stringent regulatory compliance, especially concerning safety standards and environmental impact, requires continuous adaptation and can increase development costs. Supply chain disruptions and the volatility of raw material prices, such as steel and specialized components, can impact production and pricing. Intense competition from both established players and new entrants, as well as the emergence of alternative material handling solutions like AGVs, also pose challenges.

Emerging Opportunities in Europe Conveyors Industry

Emerging opportunities in the Europe Conveyors Industry lie in the expansion of smart warehousing solutions, driven by the increasing complexity of omnichannel retail logistics. The growing demand for sustainable and energy-efficient conveyor systems presents a significant growth avenue, aligned with European Union climate goals. Furthermore, the integration of AI and machine learning for predictive maintenance and real-time optimization of conveyor networks offers untapped potential. The development of highly specialized conveyor systems for niche applications within the pharmaceuticals and food & beverage sectors, focusing on extreme hygiene and precision handling, also represents a promising frontier.

Growth Accelerators in the Europe Conveyors Industry Industry

Several factors are acting as significant growth accelerators for the Europe Conveyors Industry. The ongoing digital transformation across industries, leading to the widespread adoption of automation and smart factory concepts, is a primary catalyst. Strategic partnerships between conveyor manufacturers and software providers are enabling the development of more integrated and intelligent material handling solutions. Market expansion initiatives, particularly into emerging European economies and the development of customized solutions for diverse end-user needs, are further fueling growth. The continuous drive for enhanced productivity and reduced operational costs across all sectors of the economy will sustain demand for advanced conveyor technologies.

Key Players Shaping the Europe Conveyors Industry Market

- KNAAP AG

- Interroll Holding AG

- BEUMER Group GmbH & Co KG

- KUKA AG (Swisslog AG)

- Vanderlande Industries BV

- SSI Schaefer AG

- Kardex Group

- Honeywell Intelligrated Inc

- Daifuku Co Ltd

- Viastrore Systems GmbH

- Mecalux SA

Notable Milestones in Europe Conveyors Industry Sector

- 2019: BEUMER Group expands its airport baggage handling solutions portfolio with new intelligent sorting technologies.

- 2020: KUKA AG (Swisslog AG) announces strategic investment in AI-driven warehouse automation, enhancing conveyor integration.

- 2021: Interroll Holding AG launches a new generation of high-performance drum motors for belt conveyors, focusing on energy efficiency.

- 2022: Vanderlande Industries BV secures a major contract for an advanced baggage handling system at a key European airport.

- 2023: SSI Schaefer AG introduces modular and flexible conveyor systems designed for rapid adaptation in e-commerce fulfillment centers.

- 2024: KNAAP AG unveils new smart conveyor technology with integrated IoT sensors for predictive maintenance and enhanced operational visibility.

In-Depth Europe Conveyors Industry Market Outlook

The future outlook for the Europe Conveyors Industry is exceptionally positive, with sustained growth driven by powerful accelerators. The escalating demand for automation in logistics and manufacturing, coupled with the continuous expansion of e-commerce, will remain primary growth engines. The integration of advanced technologies like AI and IoT into conveyor systems will unlock new levels of efficiency and predictive capabilities. Strategic market expansion, particularly in sectors prioritizing operational excellence and supply chain resilience, will open new revenue streams. The industry's commitment to developing sustainable and energy-efficient solutions aligns with global environmental trends and regulatory pressures, further solidifying its long-term growth trajectory and market potential.

Europe Conveyors Industry Segmentation

-

1. Product Type

- 1.1. Belt

- 1.2. Roller

- 1.3. Pallet

- 1.4. Overhead

-

2. End-User Industry

- 2.1. Airport

- 2.2. Retail

- 2.3. Automotive

- 2.4. Manufacturing

- 2.5. Food and Beverage

- 2.6. Pharmaceuticals

- 2.7. Mining

Europe Conveyors Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

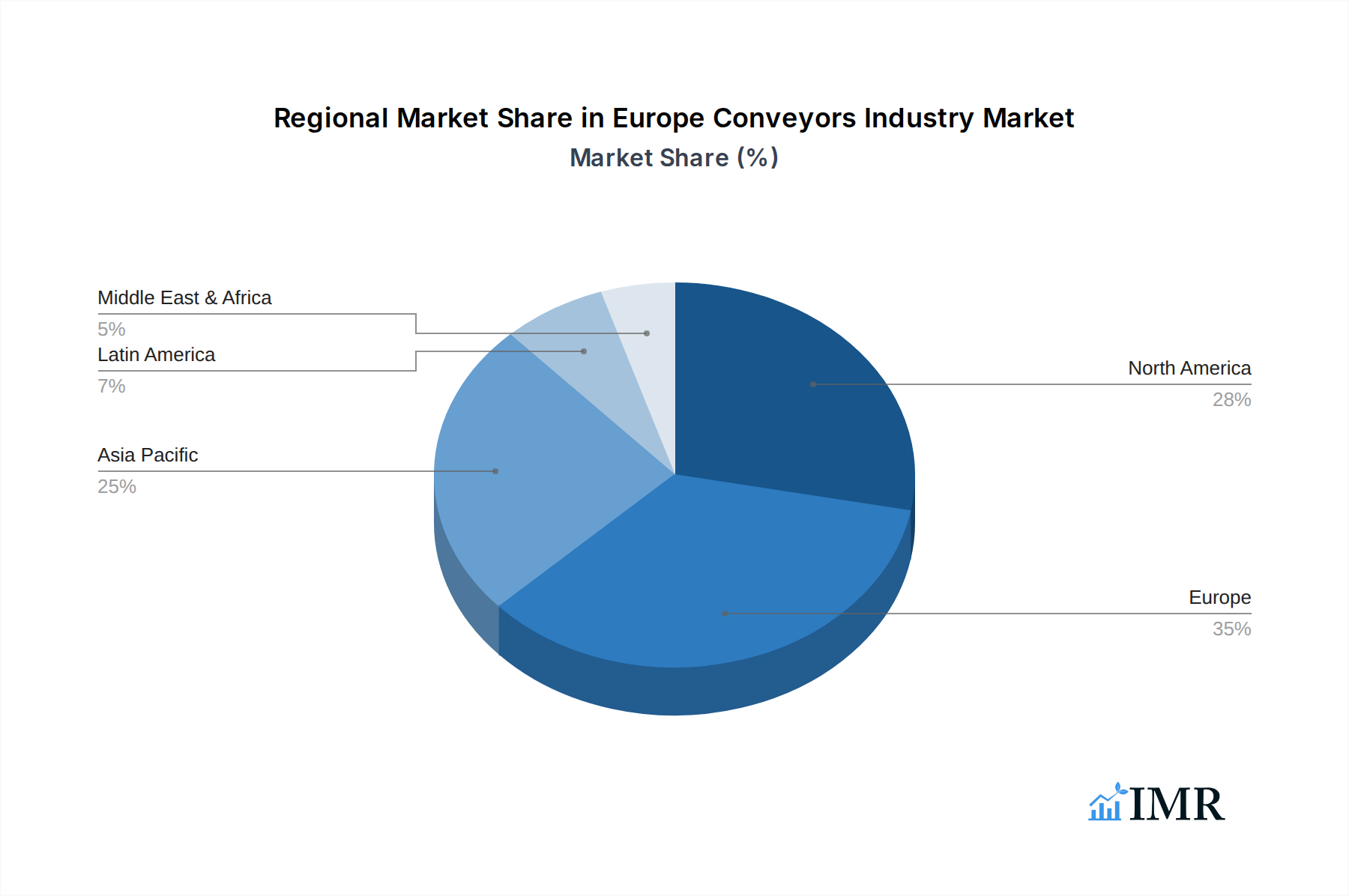

Europe Conveyors Industry Regional Market Share

Geographic Coverage of Europe Conveyors Industry

Europe Conveyors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.26% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Belt

- 5.1.2. Roller

- 5.1.3. Pallet

- 5.1.4. Overhead

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Airport

- 5.2.2. Retail

- 5.2.3. Automotive

- 5.2.4. Manufacturing

- 5.2.5. Food and Beverage

- 5.2.6. Pharmaceuticals

- 5.2.7. Mining

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Europe Conveyors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Belt

- 6.1.2. Roller

- 6.1.3. Pallet

- 6.1.4. Overhead

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Airport

- 6.2.2. Retail

- 6.2.3. Automotive

- 6.2.4. Manufacturing

- 6.2.5. Food and Beverage

- 6.2.6. Pharmaceuticals

- 6.2.7. Mining

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 KNAAP AG

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Interroll Holding AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BEUMER Group GmbH & Co KG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 KUKA AG (Swisslog AG)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Vanderlande Industries BV*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 SSI Schaefer AG

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kardex Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Honeywell Intelligrated Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Daifuku Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Viastrore Systems GmbH

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Mecalux SA

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 KNAAP AG

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Conveyors Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Conveyors Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Conveyors Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Europe Conveyors Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 3: Europe Conveyors Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Conveyors Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Europe Conveyors Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 6: Europe Conveyors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Conveyors Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Conveyors Industry?

The projected CAGR is approximately 6.26%.

2. Which companies are prominent players in the Europe Conveyors Industry?

Key companies in the market include KNAAP AG, Interroll Holding AG, BEUMER Group GmbH & Co KG, KUKA AG (Swisslog AG), Vanderlande Industries BV*List Not Exhaustive, SSI Schaefer AG, Kardex Group, Honeywell Intelligrated Inc, Daifuku Co Ltd, Viastrore Systems GmbH, Mecalux SA.

3. What are the main segments of the Europe Conveyors Industry?

The market segments include Product Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.33 billion as of 2022.

5. What are some drivers contributing to market growth?

; High Labor Wages in the European Region; Rapid Growth of E-commerce.

6. What are the notable trends driving market growth?

Airports are Expected to Hold Significant Growth.

7. Are there any restraints impacting market growth?

; High Cost of Implementation.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Conveyors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Conveyors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Conveyors Industry?

To stay informed about further developments, trends, and reports in the Europe Conveyors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence