Key Insights

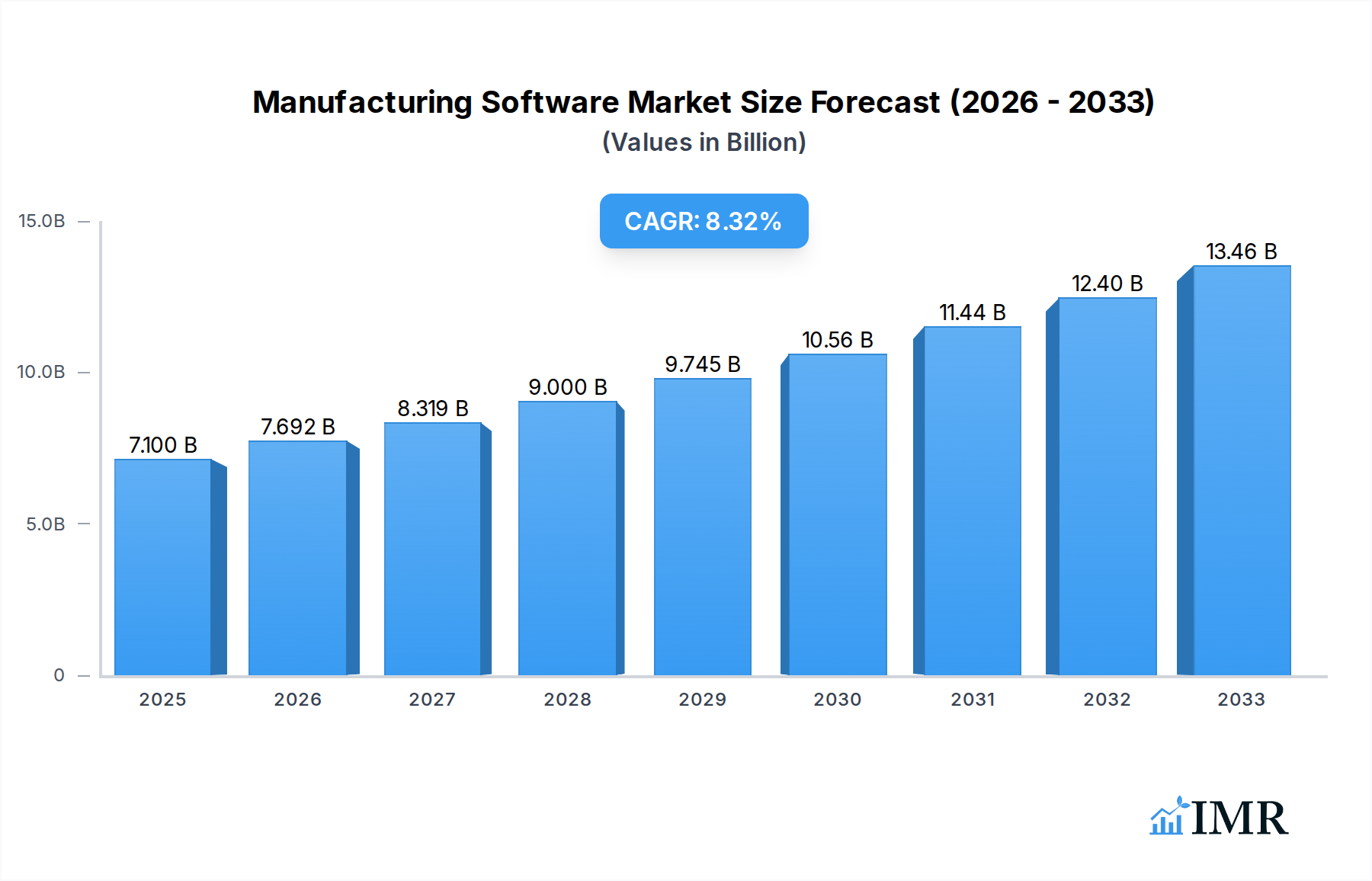

The global Manufacturing Software market is poised for substantial growth, projected to reach $7.1 billion in 2025, driven by a compelling CAGR of 8.15%. This robust expansion is fueled by the increasing adoption of advanced technologies aimed at optimizing production processes, enhancing efficiency, and improving product quality across diverse industries. Key drivers include the growing demand for automation, the implementation of Industry 4.0 principles, and the need for enhanced data analytics to inform strategic decision-making. Sectors such as Automotive & Aerospace, Electronic & Semiconductor, and Food & Beverage are leading the charge, leveraging manufacturing software to streamline operations, reduce waste, and meet stringent regulatory requirements. The continuous evolution of software solutions, offering features like real-time monitoring, predictive maintenance, and integrated supply chain management, further bolsters market momentum.

Manufacturing Software Market Size (In Billion)

Emerging trends such as the rise of the Internet of Things (IoT) in manufacturing, the increasing adoption of cloud-based solutions for scalability and accessibility, and the growing emphasis on cybersecurity within manufacturing environments are shaping the market landscape. While the integration of complex systems and the initial investment costs can present some challenges, the long-term benefits of improved productivity, reduced operational expenses, and enhanced competitiveness are outweighing these restraints. The market is segmented by type into Custom Manufacturing Software, Lean Manufacturing Software, and Project-Based Manufacturing Software, each catering to specific operational needs. Leading companies like Autodesk, Rockwell, SAP, PTC, and Siemens PLM Software are at the forefront of innovation, offering sophisticated solutions that empower manufacturers to navigate the complexities of modern production.

Manufacturing Software Company Market Share

Here is the SEO-optimized report description for Manufacturing Software, integrating high-traffic keywords and structured as requested.

Manufacturing Software Market Dynamics & Structure

The global manufacturing software market is characterized by a moderate to high level of concentration, with leading players like Siemens PLM Software, Dassault Systemes, SAP, Autodesk, and Rockwell Automation holding significant market share. Technological innovation remains a primary driver, fueled by advancements in AI, IoT, cloud computing, and digital twins, enabling greater automation, predictive maintenance, and real-time data analytics. Regulatory frameworks, particularly concerning data security and industry-specific compliance (e.g., FDA regulations for Food & Beverage, safety standards for Automotive & Aerospace), are shaping software development and deployment. Competitive product substitutes, such as off-the-shelf ERP systems versus highly customized solutions, present strategic choices for manufacturers. End-user demographics are shifting towards digitally-savvy workforces seeking intuitive and integrated platforms. Mergers and Acquisitions (M&A) activity is a consistent trend, with companies like PTC and Digitronik Labs actively pursuing inorganic growth to expand their portfolios and market reach.

- Market Concentration: Dominated by a few key vendors, but with increasing fragmentation in niche segments.

- Innovation Drivers: AI-powered analytics, IoT integration for real-time monitoring, cloud-based accessibility, and the rise of Industry 4.0 solutions.

- Regulatory Impact: Growing importance of cybersecurity standards, data privacy laws, and sector-specific compliance.

- Competitive Substitutes: Balancing specialized custom software with broader enterprise solutions.

- M&A Trends: Strategic acquisitions to enhance capabilities in areas like PLM, MES, and ERP.

Manufacturing Software Growth Trends & Insights

The manufacturing software market is poised for robust growth, projected to reach $XXX billion by 2033. This expansion is driven by a projected Compound Annual Growth Rate (CAGR) of XX.XX% during the forecast period of 2025–2033. The historical period (2019–2024) witnessed steady adoption, laying the groundwork for accelerated growth in the coming decade. Key trends influencing this trajectory include the escalating demand for smart manufacturing solutions, the pervasive adoption of Industry 4.0 technologies, and the increasing need for operational efficiency and supply chain optimization. Manufacturers are increasingly investing in software that facilitates real-time data capture, analysis, and decision-making, leading to significant improvements in productivity, quality control, and cost reduction. The shift towards digital transformation across all manufacturing segments, from Automotive & Aerospace to Food & Beverage and Electronic & Semiconductor, is a primary growth accelerator. Furthermore, the increasing complexity of global supply chains and the need for greater resilience are driving the adoption of integrated manufacturing execution systems (MES) and enterprise resource planning (ERP) solutions. The evolution of consumer preferences towards customized products is also fostering the growth of Project-Based Manufacturing Software and flexible production environments.

The adoption rates for advanced manufacturing software are climbing as businesses recognize the competitive advantages. Technological disruptions, such as the widespread implementation of machine learning algorithms for predictive maintenance and the integration of augmented reality (AR) for training and remote assistance, are revolutionizing operational paradigms. Consumer behavior shifts, characterized by a demand for greater product personalization and faster delivery times, are compelling manufacturers to adopt more agile and responsive software solutions. The proliferation of cloud-based manufacturing software has democratized access to sophisticated tools, particularly for small and medium-sized enterprises (SMEs), further fueling market penetration. The increasing emphasis on sustainability and green manufacturing practices is also creating demand for software that can monitor and optimize resource utilization and waste reduction.

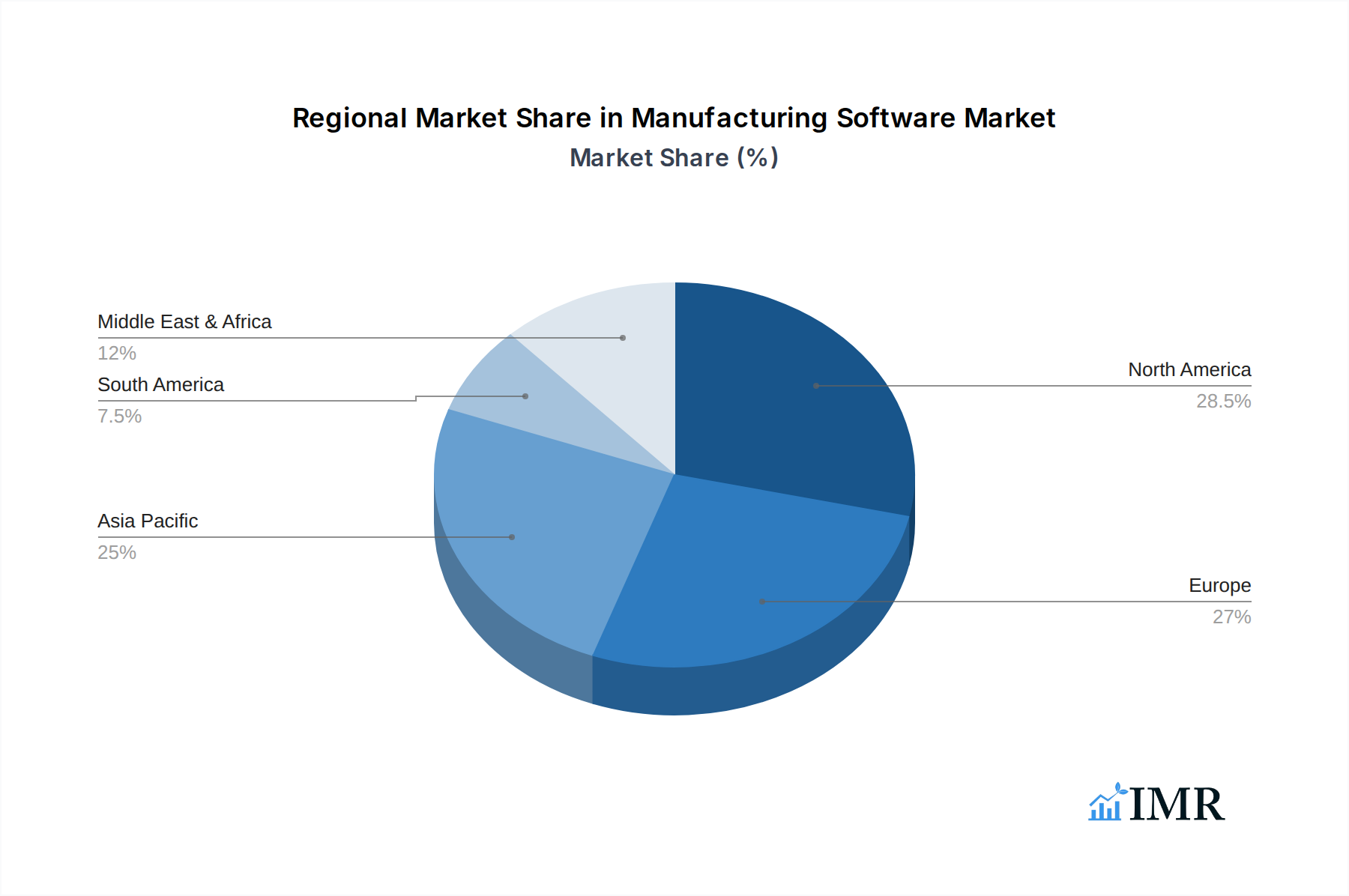

Dominant Regions, Countries, or Segments in Manufacturing Software

The Automotive & Aerospace application segment is emerging as a dominant force in the global manufacturing software market, driven by its inherent complexity, stringent quality requirements, and high value of output. This sector's reliance on advanced technologies for design, simulation, production planning, and quality assurance positions it at the forefront of software adoption. The forecast period of 2025–2033 is expected to see significant investment in Product Lifecycle Management (PLM), Manufacturing Execution Systems (MES), and Enterprise Resource Planning (ERP) solutions within Automotive & Aerospace. The projected market share for this segment is anticipated to reach XX.XX% by 2033, underscoring its substantial contribution to overall market growth.

Key drivers within the Automotive & Aerospace sector include:

- Technological Advancements: Rapid innovation in vehicle and aircraft design, requiring sophisticated simulation and modeling software.

- Supply Chain Integration: The need for seamless collaboration across a vast and complex global supply chain.

- Quality and Safety Standards: Rigorous regulatory requirements necessitate advanced quality control and traceability software.

- Electrification and Autonomous Driving: These megatrends are driving demand for new software capabilities in design, testing, and production.

North America and Europe are expected to remain leading regions for manufacturing software adoption, with the United States and Germany leading in innovation and implementation, respectively. However, the Asia-Pacific region, particularly countries like China and India, is exhibiting rapid growth due to industrial expansion and increasing investments in advanced manufacturing technologies. The Electronic & Semiconductor segment also shows strong growth potential, fueled by the ongoing digital transformation and the increasing demand for sophisticated electronic components across various industries. The market for Lean Manufacturing Software is expected to see consistent growth across all segments as companies strive for operational excellence and waste reduction.

Manufacturing Software Product Landscape

The manufacturing software product landscape is rapidly evolving with innovations focused on enhancing operational efficiency, improving decision-making, and fostering greater connectivity. Siemens PLM Software's comprehensive suite, Dassault Systemes' 3DEXPERIENCE platform, and SAP's S/4HANA are prime examples of integrated solutions offering capabilities from design and simulation to production and maintenance. Autodesk's focus on cloud-based design and engineering tools, alongside Rockwell Automation's strength in industrial control and automation software, highlights a trend towards digital thread integration. Emerging players like Digitronik Labs are pushing boundaries in niche areas like AI-driven optimization. Product innovations are increasingly incorporating AI for predictive analytics, IoT for real-time monitoring, and cloud-native architectures for scalability and accessibility. Unique selling propositions often revolve around seamless integration, user-friendliness, and the ability to provide actionable insights from vast data streams.

Key Drivers, Barriers & Challenges in Manufacturing Software

Key Drivers:

- Industry 4.0 Adoption: The push for smart factories and connected production lines is a primary growth catalyst.

- Demand for Automation: Increasing labor costs and the need for higher precision are driving automation software adoption.

- Data-Driven Decision Making: The recognition of data as a strategic asset fuels investment in analytics and reporting tools.

- Globalization and Supply Chain Complexity: The need for integrated, global supply chain management solutions.

Barriers & Challenges:

- High Implementation Costs: The initial investment in software and integration can be substantial.

- Resistance to Change: Overcoming ingrained operational practices and workforce reluctance to adopt new technologies.

- Cybersecurity Threats: Protecting sensitive manufacturing data from breaches and ensuring operational continuity.

- Skills Gap: A shortage of skilled personnel to implement, manage, and leverage advanced manufacturing software.

- Integration Complexity: Ensuring seamless interoperability between disparate legacy systems and new software solutions.

Emerging Opportunities in Manufacturing Software

Emerging opportunities lie in the development of AI-powered autonomous production systems that can self-optimize and adapt to changing demands. The integration of extended reality (XR) technologies for immersive training, remote assistance, and digital twin visualization presents significant potential. Furthermore, the growing emphasis on sustainability and circular economy principles is creating demand for software that can track material provenance, optimize resource usage, and facilitate product lifecycle management with an environmental focus. The expansion of manufacturing software into smaller and medium-sized enterprises (SMEs) through more affordable and scalable cloud-based solutions also represents a vast untapped market.

Growth Accelerators in the Manufacturing Software Industry

Long-term growth in the manufacturing software industry will be significantly accelerated by breakthroughs in artificial intelligence and machine learning, enabling more sophisticated predictive maintenance, anomaly detection, and process optimization. Strategic partnerships between software vendors and hardware manufacturers are crucial for creating seamless, end-to-end solutions. Market expansion into emerging economies and the development of specialized software for niche industries, such as advanced materials and biotechnology, will further fuel growth. The increasing adoption of digital twins for simulating and optimizing entire production lifecycles is another key growth accelerator.

Key Players Shaping the Manufacturing Software Market

- Autodesk

- Rockwell Automation

- SAP

- PTC

- Dassault Systemes

- Siemens PLM Software

- Digitronik Labs

- Schleuniger, Inc.

- ISGUS America

- CAMWorks

Notable Milestones in Manufacturing Software Sector

- 2019: Increased adoption of cloud-based MES solutions for enhanced flexibility.

- 2020: Significant investment in cybersecurity features for manufacturing software amid rising threats.

- 2021: Growth in the adoption of AI-driven predictive maintenance software across industries.

- 2022: Major vendors like Siemens and Dassault Systemes enhance their digital twin capabilities.

- 2023: Growing focus on sustainable manufacturing software solutions for resource optimization.

- 2024: Emergence of more integrated PLM, ERP, and MES platforms for end-to-end visibility.

In-Depth Manufacturing Software Market Outlook

The manufacturing software market is set for a period of sustained and significant expansion, driven by the relentless pursuit of efficiency, agility, and data-driven insights. The integration of advanced technologies like AI, IoT, and digital twins will continue to revolutionize manufacturing operations, enabling hyper-personalization and optimized supply chains. Strategic partnerships and ongoing M&A activities will further consolidate the market, while also fostering innovation in specialized segments. The outlook suggests a future where manufacturing software is not just a tool, but an indispensable strategic asset for competitive advantage.

Manufacturing Software Segmentation

-

1. Application

- 1.1. Automotive & Aerospace

- 1.2. Food & Beverage

- 1.3. Electronic & Semiconductor

- 1.4. Mining, Oil & Gas

- 1.5. Fiber & Textile

- 1.6. Paper & Pulp

- 1.7. Chemical

- 1.8. Others

-

2. Types

- 2.1. Custom Manufacturing Software

- 2.2. Lean Manufacturing Software

- 2.3. Project-Based Manufacturing Software

- 2.4. Other

Manufacturing Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Manufacturing Software Regional Market Share

Geographic Coverage of Manufacturing Software

Manufacturing Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.74% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive & Aerospace

- 5.1.2. Food & Beverage

- 5.1.3. Electronic & Semiconductor

- 5.1.4. Mining, Oil & Gas

- 5.1.5. Fiber & Textile

- 5.1.6. Paper & Pulp

- 5.1.7. Chemical

- 5.1.8. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Custom Manufacturing Software

- 5.2.2. Lean Manufacturing Software

- 5.2.3. Project-Based Manufacturing Software

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Manufacturing Software Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive & Aerospace

- 6.1.2. Food & Beverage

- 6.1.3. Electronic & Semiconductor

- 6.1.4. Mining, Oil & Gas

- 6.1.5. Fiber & Textile

- 6.1.6. Paper & Pulp

- 6.1.7. Chemical

- 6.1.8. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Custom Manufacturing Software

- 6.2.2. Lean Manufacturing Software

- 6.2.3. Project-Based Manufacturing Software

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Manufacturing Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive & Aerospace

- 7.1.2. Food & Beverage

- 7.1.3. Electronic & Semiconductor

- 7.1.4. Mining, Oil & Gas

- 7.1.5. Fiber & Textile

- 7.1.6. Paper & Pulp

- 7.1.7. Chemical

- 7.1.8. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Custom Manufacturing Software

- 7.2.2. Lean Manufacturing Software

- 7.2.3. Project-Based Manufacturing Software

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Manufacturing Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive & Aerospace

- 8.1.2. Food & Beverage

- 8.1.3. Electronic & Semiconductor

- 8.1.4. Mining, Oil & Gas

- 8.1.5. Fiber & Textile

- 8.1.6. Paper & Pulp

- 8.1.7. Chemical

- 8.1.8. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Custom Manufacturing Software

- 8.2.2. Lean Manufacturing Software

- 8.2.3. Project-Based Manufacturing Software

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Manufacturing Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive & Aerospace

- 9.1.2. Food & Beverage

- 9.1.3. Electronic & Semiconductor

- 9.1.4. Mining, Oil & Gas

- 9.1.5. Fiber & Textile

- 9.1.6. Paper & Pulp

- 9.1.7. Chemical

- 9.1.8. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Custom Manufacturing Software

- 9.2.2. Lean Manufacturing Software

- 9.2.3. Project-Based Manufacturing Software

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Manufacturing Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive & Aerospace

- 10.1.2. Food & Beverage

- 10.1.3. Electronic & Semiconductor

- 10.1.4. Mining, Oil & Gas

- 10.1.5. Fiber & Textile

- 10.1.6. Paper & Pulp

- 10.1.7. Chemical

- 10.1.8. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Custom Manufacturing Software

- 10.2.2. Lean Manufacturing Software

- 10.2.3. Project-Based Manufacturing Software

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Manufacturing Software Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Automotive & Aerospace

- 11.1.2. Food & Beverage

- 11.1.3. Electronic & Semiconductor

- 11.1.4. Mining, Oil & Gas

- 11.1.5. Fiber & Textile

- 11.1.6. Paper & Pulp

- 11.1.7. Chemical

- 11.1.8. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Custom Manufacturing Software

- 11.2.2. Lean Manufacturing Software

- 11.2.3. Project-Based Manufacturing Software

- 11.2.4. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Autodesk

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Rockwell

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SAP

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 PTC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Dassault Systemes

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Siemens PLM Software

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Digitronik Labs

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Schleuniger

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ISGUS America

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 CAMWorks

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Autodesk

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Manufacturing Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Manufacturing Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Manufacturing Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Manufacturing Software Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Manufacturing Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Manufacturing Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Manufacturing Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Manufacturing Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Manufacturing Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Manufacturing Software Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Manufacturing Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Manufacturing Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Manufacturing Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Manufacturing Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Manufacturing Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Manufacturing Software Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Manufacturing Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Manufacturing Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Manufacturing Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Manufacturing Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Manufacturing Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Manufacturing Software Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Manufacturing Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Manufacturing Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Manufacturing Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Manufacturing Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Manufacturing Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Manufacturing Software Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Manufacturing Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Manufacturing Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Manufacturing Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Manufacturing Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Manufacturing Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Manufacturing Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Manufacturing Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Manufacturing Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Manufacturing Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Manufacturing Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Manufacturing Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Manufacturing Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Manufacturing Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Manufacturing Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Manufacturing Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Manufacturing Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Manufacturing Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Manufacturing Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Manufacturing Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Manufacturing Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Manufacturing Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Manufacturing Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Manufacturing Software?

The projected CAGR is approximately 17.74%.

2. Which companies are prominent players in the Manufacturing Software?

Key companies in the market include Autodesk, Rockwell, SAP, PTC, Dassault Systemes, Siemens PLM Software, Digitronik Labs, Schleuniger, Inc., ISGUS America, CAMWorks.

3. What are the main segments of the Manufacturing Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Manufacturing Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Manufacturing Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Manufacturing Software?

To stay informed about further developments, trends, and reports in the Manufacturing Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence