Key Insights

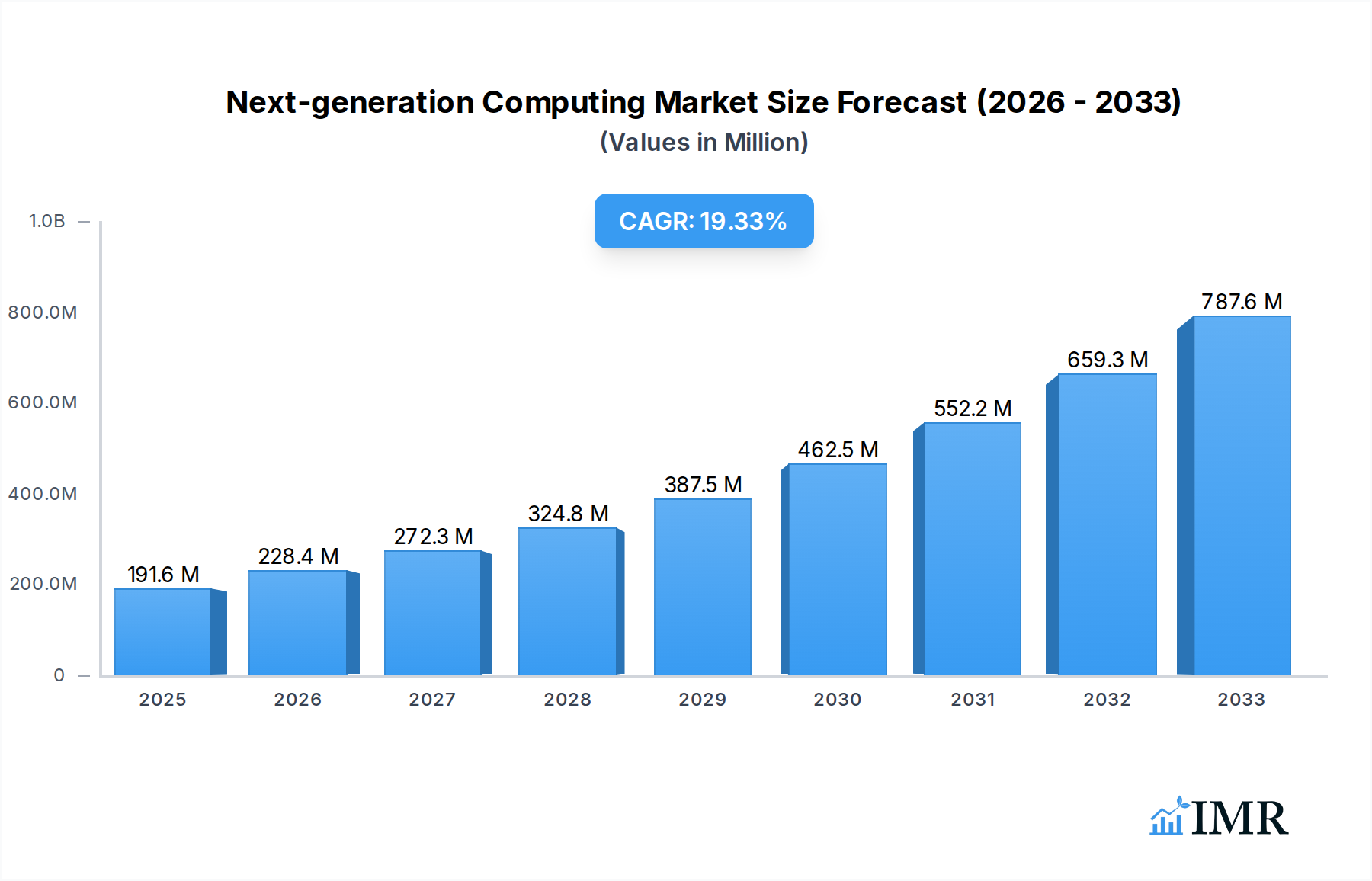

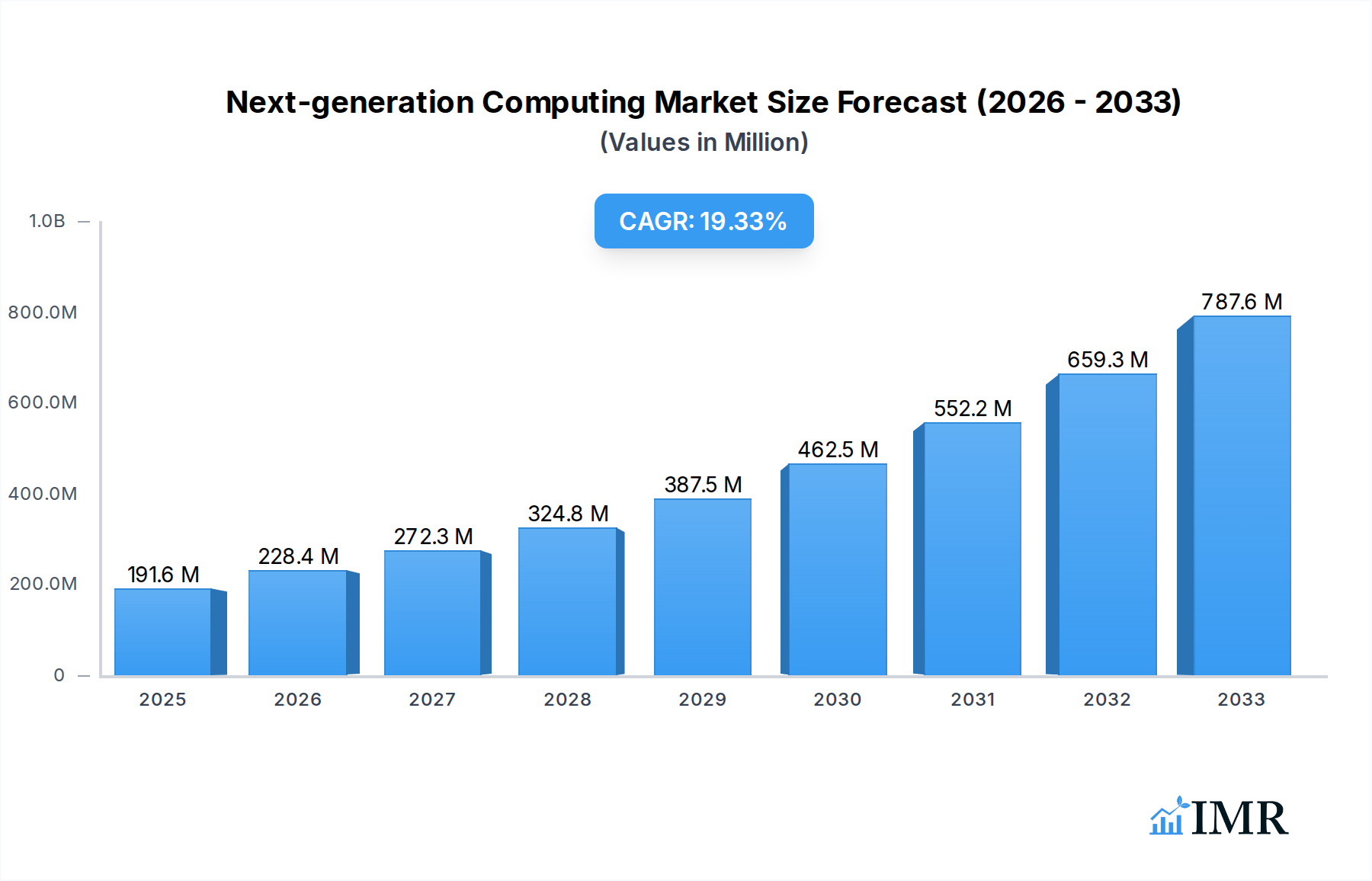

The Next-generation Computing Market is poised for explosive growth, projected to reach $191.62 million by 2025, with a remarkable Compound Annual Growth Rate (CAGR) of 19.38% through 2033. This expansion is fueled by a confluence of powerful drivers, including the increasing demand for advanced computational capabilities to tackle complex problems in areas like artificial intelligence, scientific research, and data analytics. The insatiable appetite for faster processing, enhanced efficiency, and the ability to handle massive datasets is propelling innovation across hardware, software, and services within the next-generation computing ecosystem. Emerging technologies like quantum computing, optical computing, and advanced edge computing are no longer theoretical concepts but are rapidly maturing into viable solutions that promise to revolutionize industries. The integration of high-performance computing (HPC) with these nascent technologies is creating a powerful synergy, enabling breakthroughs previously unimaginable.

Next-generation Computing Market Market Size (In Million)

The market is characterized by significant trends such as the widespread adoption of cloud-based deployments, offering scalability and accessibility, and the continued development of on-premise solutions for sensitive data and specialized applications. The strategic importance of next-generation computing is evident in its penetration across diverse end-user industries, including Automotive & Transportation, Energy & Utilities, Healthcare, BFSI, Aerospace & Defense, Media & Entertainment, IT & Telecom, Retail, and Manufacturing. These sectors are leveraging next-generation computing to gain competitive advantages, optimize operations, and drive innovation. While the immense potential is clear, certain restraints, such as the high cost of implementation and the need for specialized expertise, could temper the pace of adoption in some segments. However, the ongoing technological advancements and increasing industry investment are expected to mitigate these challenges, paving the way for sustained and robust market expansion.

Next-generation Computing Market Company Market Share

Next-generation Computing Market: Unlocking Future Digital Capabilities | Comprehensive Report 2019–2033

This definitive report offers an in-depth analysis of the global Next-generation Computing Market, exploring its transformative potential across various industries. We delve into High-Performance Computing (HPC), Quantum Computing, Optical Computing, and Edge Computing, examining their intricate interplay and projected growth. With a study period spanning 2019–2033, a base year of 2025, and a forecast period of 2025–2033, this report provides unparalleled strategic insights for stakeholders. Discover the key players, market dynamics, growth drivers, and emerging opportunities that are shaping the future of computation, with all values presented in Million units.

Next-generation Computing Market Market Dynamics & Structure

The Next-generation Computing Market is characterized by dynamic forces shaping its structure and trajectory. Market concentration is gradually shifting as established tech giants like IBM Corporation, Alibaba Group Holding Limited, Google LLC, Microsoft Corporation, and Amazon Web Services Inc. invest heavily in cutting-edge research and development, alongside specialized players such as NVIDIA Corp, NEC Corporation, Oracle Corporation, Cisco Systems, and Intel Corporation. Technological innovation remains the primary driver, with breakthroughs in AI, machine learning, and advanced algorithms fueling the demand for more powerful and efficient computing solutions. Regulatory frameworks, while still evolving, are becoming increasingly important, particularly concerning data privacy and ethical AI development. Competitive product substitutes are emerging, but the unique capabilities of next-generation computing offer distinct advantages in complex problem-solving. End-user demographics are diversifying, with significant adoption across Automotive & Transportation, Energy & Utilities, Healthcare, BFSI, Aerospace & Defense, Media & Entertainment, IT & Telecom, Retail, and Manufacturing. Mergers and acquisitions (M&A) are a significant trend, consolidating market share and fostering innovation. For instance, the sector has witnessed numerous strategic alliances aimed at accelerating product development and market penetration. Barriers to innovation include the immense capital investment required for R&D, the long development cycles for certain technologies like quantum computing, and the need for specialized talent.

- Market Concentration: Moderate to high, with key players investing heavily in R&D.

- Technological Innovation Drivers: AI, machine learning, advanced algorithms, hardware miniaturization, energy efficiency.

- Regulatory Frameworks: Evolving data privacy laws, AI ethics guidelines.

- Competitive Product Substitutes: Advanced traditional computing, specialized hardware accelerators.

- End-User Demographics: Broad adoption across sectors, with increasing demand from data-intensive industries.

- M&A Trends: Strategic acquisitions and partnerships to enhance technological capabilities and market reach.

- Innovation Barriers: High R&D costs, long development cycles, talent shortages.

Next-generation Computing Market Growth Trends & Insights

The Next-generation Computing Market is poised for substantial growth, driven by an escalating need for processing power and advanced analytical capabilities. Market size evolution is marked by a consistent upward trend, with significant expansion anticipated in the forecast period. Adoption rates for key technologies like High-Performance Computing are steadily increasing across research institutions and enterprise environments for complex simulations and data analysis. The advent of Quantum Computing presents a revolutionary shift, promising to solve problems currently intractable for even the most powerful supercomputers, albeit with a longer adoption horizon. Optical Computing and Edge Computing are also gaining momentum, offering distinct advantages in speed, efficiency, and localized processing, respectively.

Technological disruptions are at the heart of this market's dynamism. The integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is a primary catalyst, enabling sophisticated data analytics, predictive modeling, and intelligent automation. These advancements are transforming industries by enhancing decision-making, optimizing operations, and fostering innovation. Consumer behavior shifts are also playing a crucial role. Businesses are increasingly leveraging next-generation computing to gain a competitive edge, improve customer experiences through personalized services, and develop groundbreaking products. The demand for real-time data processing and insights at the edge is fueling the growth of Edge Computing solutions, particularly in sectors like autonomous vehicles and smart manufacturing.

The growth is not uniform; specific segments are experiencing accelerated adoption. Cloud deployments continue to be a dominant model due to scalability and cost-effectiveness, but On-Premise solutions are seeing resurgence for sensitive data and highly regulated environments. The market penetration of these advanced computing paradigms is projected to deepen significantly as the underlying technologies mature and become more accessible. The CAGR for the next-generation computing market is estimated to be robust, reflecting the immense potential and ongoing technological advancements. This growth trajectory is indicative of a fundamental shift in how computation is perceived and utilized, moving beyond mere data processing to intelligent problem-solving and discovery. The evolving digital landscape, with its ever-increasing data volumes and complexity, necessitates the adoption of these advanced computing paradigms to unlock future capabilities.

Dominant Regions, Countries, or Segments in Next-generation Computing Market

The Next-generation Computing Market exhibits varied dominance across its constituent segments and geographical landscapes. From a Component perspective, Hardware remains a foundational pillar, encompassing advanced processors, accelerators, and specialized chips crucial for enabling next-generation capabilities. The Software segment, including AI/ML frameworks, quantum algorithms, and specialized operating systems, is rapidly expanding in importance, providing the intelligence and control for these powerful systems. Services, such as cloud computing, managed services, and consulting, are integral to the adoption and effective utilization of next-generation computing solutions.

In terms of Computing Type, High-Performance Computing (HPC) currently dominates due to its established presence in scientific research, weather forecasting, and complex simulations. However, Quantum Computing represents the frontier, with significant long-term growth potential and the capacity to revolutionize fields like drug discovery and materials science. Optical Computing offers immense promise in terms of speed and energy efficiency, while Edge Computing is rapidly expanding its footprint in applications requiring real-time data processing at the source, such as IoT devices and autonomous systems.

Deployment models are predominantly driven by Cloud solutions, offering scalability, flexibility, and reduced upfront investment for many organizations. Nevertheless, On-Premise deployments remain critical for sectors with stringent data security and compliance requirements.

Across End-Users, the IT & Telecom sector leads in adoption due to its inherent need for advanced data processing and network capabilities. The Automotive & Transportation industry is a significant growth driver, particularly with the rise of autonomous vehicles and connected car technologies. Healthcare is witnessing increased adoption for drug discovery, personalized medicine, and advanced diagnostics. The BFSI sector leverages next-generation computing for fraud detection, risk management, and algorithmic trading. Aerospace & Defense, Energy & Utilities, Retail, and Manufacturing are also increasingly integrating these technologies to optimize operations, enhance security, and drive innovation.

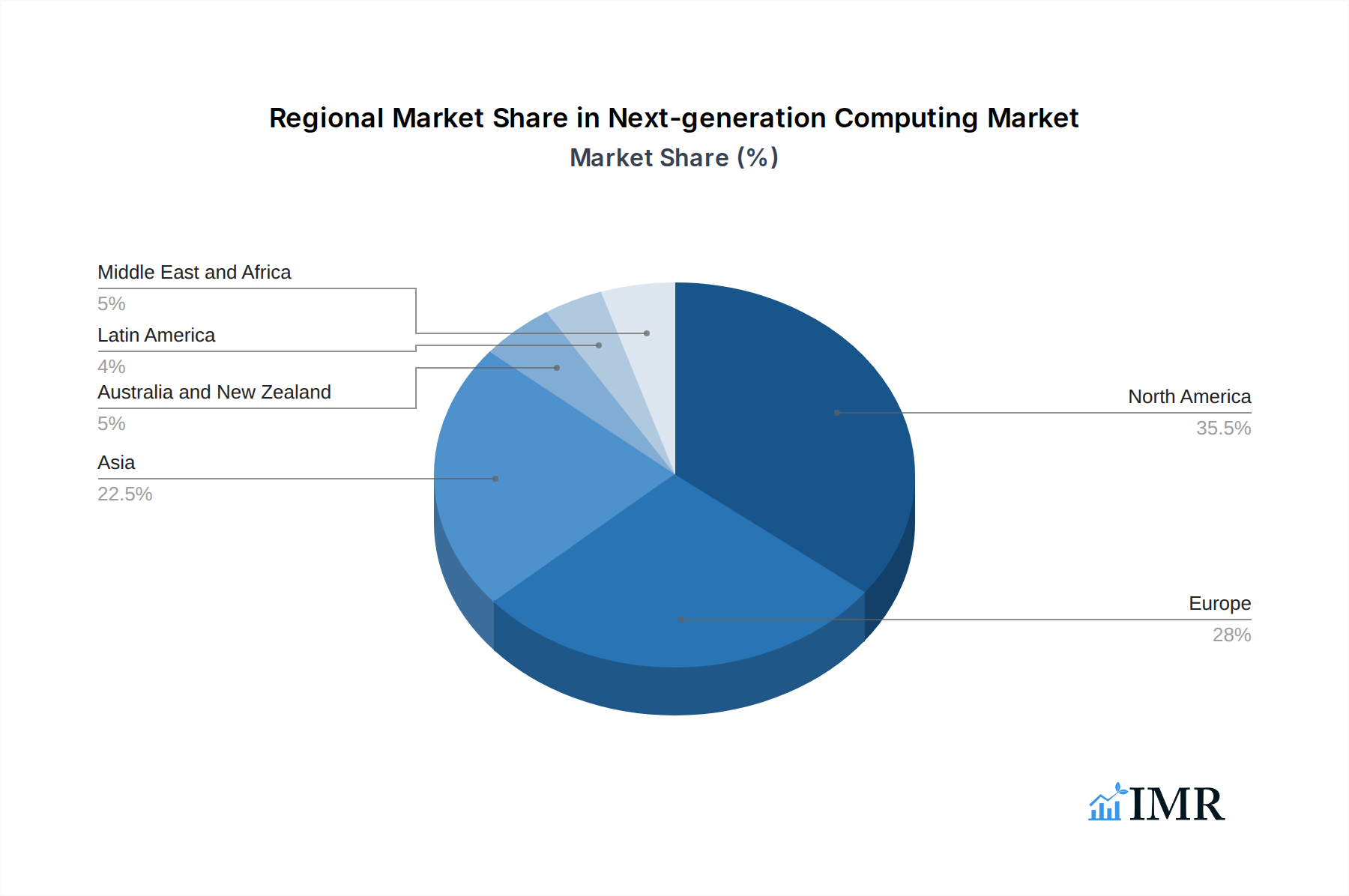

Geographically, North America and Europe are currently leading regions, driven by robust R&D investments, established technological ecosystems, and significant government support for advanced computing initiatives. However, the Asia Pacific region is rapidly emerging as a major growth hub, fueled by increasing investments from countries like China and India, a burgeoning tech industry, and a vast potential market. Key drivers for regional dominance include favorable economic policies, strong academic-industry collaborations, and the availability of skilled workforces. Market share in these dominant segments and regions is expected to continue shifting as new technologies mature and adoption curves steepen.

Next-generation Computing Market Product Landscape

The Next-generation Computing Market product landscape is defined by groundbreaking innovations aimed at pushing the boundaries of computational power, speed, and efficiency. Companies are actively developing specialized hardware such as quantum processors, photonic chips, and advanced GPUs designed for parallel processing and AI workloads. Software innovations include sophisticated algorithms for quantum computing, optimized AI frameworks, and secure, distributed ledger technologies that underpin many next-generation applications. Services are evolving to support the complex deployment and management of these cutting-edge solutions, with a focus on cloud-native architectures and managed edge deployments. These products are finding critical applications in scientific research, complex simulations, advanced data analytics, artificial intelligence development, and solving previously intractable problems. Unique selling propositions revolve around unprecedented processing speeds, the ability to tackle highly complex problems, and the potential for transformative scientific and industrial breakthroughs.

Key Drivers, Barriers & Challenges in Next-generation Computing Market

The Next-generation Computing Market is propelled by several key drivers. The exponential growth of data generation necessitates more powerful processing capabilities for analysis and insight extraction. Advancements in Artificial Intelligence and Machine Learning are creating a demand for computing architectures that can handle complex model training and inference. The pursuit of scientific discovery, from drug development to climate modeling, relies heavily on the computational power offered by these technologies. Furthermore, the increasing adoption of IoT devices and the growing need for real-time data processing at the edge are driving the development of distributed and intelligent computing solutions.

However, significant barriers and challenges exist. The immense capital investment required for research, development, and manufacturing of next-generation hardware, particularly quantum computers, is substantial. The nascent stage of some technologies, such as quantum computing, means that their practical applications and widespread adoption are still some years away. Talent shortages for highly specialized professionals in areas like quantum physics and advanced AI development pose a significant constraint. Regulatory hurdles related to data privacy, security, and the ethical implications of advanced AI can also impede market growth. Supply chain issues for specialized components, and the interoperability challenges between different next-generation computing platforms, further contribute to the complexities. Competitive pressures from established computing paradigms, though diminishing, still exist, requiring continuous innovation and demonstration of clear value propositions.

Emerging Opportunities in Next-generation Computing Market

Emerging opportunities within the Next-generation Computing Market are abundant and ripe for exploration. The untapped potential of Quantum Computing in drug discovery, materials science, and financial modeling presents a revolutionary avenue for innovation. The rapid expansion of Edge Computing in response to the proliferation of IoT devices and the demand for low-latency processing opens doors for specialized hardware and software solutions in smart cities, industrial automation, and autonomous systems. The integration of AI with next-generation computing is creating opportunities for hyper-personalized customer experiences, predictive maintenance in manufacturing, and advanced cybersecurity solutions. Furthermore, the growing need for sustainable and energy-efficient computing is driving innovation in optical computing and novel processor architectures. Evolving consumer preferences towards data-driven insights and hyper-personalized services will continue to fuel demand for these advanced capabilities across all sectors.

Growth Accelerators in the Next-generation Computing Market Industry

Several key catalysts are accelerating long-term growth in the Next-generation Computing Market. Technological breakthroughs, particularly in quantum entanglement, qubit stability, and error correction, are rapidly advancing the feasibility of practical quantum computers. Strategic partnerships between hardware manufacturers, software developers, and end-user industries are crucial for co-creating solutions tailored to specific needs and accelerating adoption. Market expansion strategies, including the development of accessible cloud-based platforms for quantum computing and edge AI, are lowering the barrier to entry for businesses of all sizes. Furthermore, significant government investments in national quantum initiatives and advanced research programs are fostering a robust innovation ecosystem and driving foundational research. The continuous refinement of algorithms and the development of new use cases for existing technologies like HPC are also contributing to sustained growth.

Key Players Shaping the Next-generation Computing Market Market

- IBM Corporation

- Alibaba Group Holding Limited

- Google LLC

- Microsoft Corporation

- Amazon Web Services Inc.

- NVIDIA Corp

- NEC Corporation

- Oracle Corporation

- Cisco Systems

- Intel Corporation

Notable Milestones in Next-generation Computing Market Sector

- July 2023: Moody's and Microsoft announced a strategic partnership to co-create next-generation data, analytics, research, collaboration, and risk solutions for the financial services industry. This collaboration aims to leverage Microsoft's Azure OpenAI Service, Fabric, and Teams with Moody's proprietary data and analytics to enhance corporate intelligence and risk assessment.

- September 2022: General Atomics Aeronautical Systems, in partnership with Indian start-up 3rdiTech, announced their intention to develop next-generation integrated circuits, other semiconductor technologies, and computer chips, signaling advancements in the hardware crucial for future computing.

In-Depth Next-generation Computing Market Market Outlook

The Next-generation Computing Market is characterized by a highly promising future, with growth accelerators poised to unlock unprecedented potential. The ongoing advancements in Quantum Computing are expected to move from theoretical possibilities to tangible applications in complex problem-solving, revolutionizing fields such as medicine and materials science. The maturation and widespread adoption of Edge Computing will enable pervasive intelligence and real-time decision-making across industries, from autonomous vehicles to smart manufacturing. Strategic collaborations between leading technology providers and industry-specific enterprises will continue to foster innovation, driving the development of tailored solutions. Furthermore, the increasing focus on sustainable and energy-efficient computing paradigms will spur further research and development in areas like optical computing. The market's trajectory points towards a future where computation is not just about processing power but about intelligent, adaptive, and transformative capabilities across all aspects of human endeavor.

Next-generation Computing Market Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

- 1.3. Services

-

2. Computing Type

- 2.1. High-Performance Computing

- 2.2. Quantum Computing

- 2.3. Optical Computing

- 2.4. Edge Computing

- 2.5. Other Computing Types

-

3. Deployement

- 3.1. Cloud

- 3.2. On-Premise

-

4. End-user

- 4.1. Automotive & Transportation

- 4.2. Energy & Utilities

- 4.3. Healthcare

- 4.4. BFSI

- 4.5. Aerospace & Defense

- 4.6. Media & Entertainment

- 4.7. IT & Telecom

- 4.8. Retail

- 4.9. Manufacturing

- 4.10. Other End Users

Next-generation Computing Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Next-generation Computing Market Regional Market Share

Geographic Coverage of Next-generation Computing Market

Next-generation Computing Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Services

- 5.2. Market Analysis, Insights and Forecast - by Computing Type

- 5.2.1. High-Performance Computing

- 5.2.2. Quantum Computing

- 5.2.3. Optical Computing

- 5.2.4. Edge Computing

- 5.2.5. Other Computing Types

- 5.3. Market Analysis, Insights and Forecast - by Deployement

- 5.3.1. Cloud

- 5.3.2. On-Premise

- 5.4. Market Analysis, Insights and Forecast - by End-user

- 5.4.1. Automotive & Transportation

- 5.4.2. Energy & Utilities

- 5.4.3. Healthcare

- 5.4.4. BFSI

- 5.4.5. Aerospace & Defense

- 5.4.6. Media & Entertainment

- 5.4.7. IT & Telecom

- 5.4.8. Retail

- 5.4.9. Manufacturing

- 5.4.10. Other End Users

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia

- 5.5.4. Australia and New Zealand

- 5.5.5. Latin America

- 5.5.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Next-generation Computing Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Services

- 6.2. Market Analysis, Insights and Forecast - by Computing Type

- 6.2.1. High-Performance Computing

- 6.2.2. Quantum Computing

- 6.2.3. Optical Computing

- 6.2.4. Edge Computing

- 6.2.5. Other Computing Types

- 6.3. Market Analysis, Insights and Forecast - by Deployement

- 6.3.1. Cloud

- 6.3.2. On-Premise

- 6.4. Market Analysis, Insights and Forecast - by End-user

- 6.4.1. Automotive & Transportation

- 6.4.2. Energy & Utilities

- 6.4.3. Healthcare

- 6.4.4. BFSI

- 6.4.5. Aerospace & Defense

- 6.4.6. Media & Entertainment

- 6.4.7. IT & Telecom

- 6.4.8. Retail

- 6.4.9. Manufacturing

- 6.4.10. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.2. Software

- 7.1.3. Services

- 7.2. Market Analysis, Insights and Forecast - by Computing Type

- 7.2.1. High-Performance Computing

- 7.2.2. Quantum Computing

- 7.2.3. Optical Computing

- 7.2.4. Edge Computing

- 7.2.5. Other Computing Types

- 7.3. Market Analysis, Insights and Forecast - by Deployement

- 7.3.1. Cloud

- 7.3.2. On-Premise

- 7.4. Market Analysis, Insights and Forecast - by End-user

- 7.4.1. Automotive & Transportation

- 7.4.2. Energy & Utilities

- 7.4.3. Healthcare

- 7.4.4. BFSI

- 7.4.5. Aerospace & Defense

- 7.4.6. Media & Entertainment

- 7.4.7. IT & Telecom

- 7.4.8. Retail

- 7.4.9. Manufacturing

- 7.4.10. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.2. Software

- 8.1.3. Services

- 8.2. Market Analysis, Insights and Forecast - by Computing Type

- 8.2.1. High-Performance Computing

- 8.2.2. Quantum Computing

- 8.2.3. Optical Computing

- 8.2.4. Edge Computing

- 8.2.5. Other Computing Types

- 8.3. Market Analysis, Insights and Forecast - by Deployement

- 8.3.1. Cloud

- 8.3.2. On-Premise

- 8.4. Market Analysis, Insights and Forecast - by End-user

- 8.4.1. Automotive & Transportation

- 8.4.2. Energy & Utilities

- 8.4.3. Healthcare

- 8.4.4. BFSI

- 8.4.5. Aerospace & Defense

- 8.4.6. Media & Entertainment

- 8.4.7. IT & Telecom

- 8.4.8. Retail

- 8.4.9. Manufacturing

- 8.4.10. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.2. Software

- 9.1.3. Services

- 9.2. Market Analysis, Insights and Forecast - by Computing Type

- 9.2.1. High-Performance Computing

- 9.2.2. Quantum Computing

- 9.2.3. Optical Computing

- 9.2.4. Edge Computing

- 9.2.5. Other Computing Types

- 9.3. Market Analysis, Insights and Forecast - by Deployement

- 9.3.1. Cloud

- 9.3.2. On-Premise

- 9.4. Market Analysis, Insights and Forecast - by End-user

- 9.4.1. Automotive & Transportation

- 9.4.2. Energy & Utilities

- 9.4.3. Healthcare

- 9.4.4. BFSI

- 9.4.5. Aerospace & Defense

- 9.4.6. Media & Entertainment

- 9.4.7. IT & Telecom

- 9.4.8. Retail

- 9.4.9. Manufacturing

- 9.4.10. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Australia and New Zealand Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.2. Software

- 10.1.3. Services

- 10.2. Market Analysis, Insights and Forecast - by Computing Type

- 10.2.1. High-Performance Computing

- 10.2.2. Quantum Computing

- 10.2.3. Optical Computing

- 10.2.4. Edge Computing

- 10.2.5. Other Computing Types

- 10.3. Market Analysis, Insights and Forecast - by Deployement

- 10.3.1. Cloud

- 10.3.2. On-Premise

- 10.4. Market Analysis, Insights and Forecast - by End-user

- 10.4.1. Automotive & Transportation

- 10.4.2. Energy & Utilities

- 10.4.3. Healthcare

- 10.4.4. BFSI

- 10.4.5. Aerospace & Defense

- 10.4.6. Media & Entertainment

- 10.4.7. IT & Telecom

- 10.4.8. Retail

- 10.4.9. Manufacturing

- 10.4.10. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Latin America Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Hardware

- 11.1.2. Software

- 11.1.3. Services

- 11.2. Market Analysis, Insights and Forecast - by Computing Type

- 11.2.1. High-Performance Computing

- 11.2.2. Quantum Computing

- 11.2.3. Optical Computing

- 11.2.4. Edge Computing

- 11.2.5. Other Computing Types

- 11.3. Market Analysis, Insights and Forecast - by Deployement

- 11.3.1. Cloud

- 11.3.2. On-Premise

- 11.4. Market Analysis, Insights and Forecast - by End-user

- 11.4.1. Automotive & Transportation

- 11.4.2. Energy & Utilities

- 11.4.3. Healthcare

- 11.4.4. BFSI

- 11.4.5. Aerospace & Defense

- 11.4.6. Media & Entertainment

- 11.4.7. IT & Telecom

- 11.4.8. Retail

- 11.4.9. Manufacturing

- 11.4.10. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Middle East and Africa Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Component

- 12.1.1. Hardware

- 12.1.2. Software

- 12.1.3. Services

- 12.2. Market Analysis, Insights and Forecast - by Computing Type

- 12.2.1. High-Performance Computing

- 12.2.2. Quantum Computing

- 12.2.3. Optical Computing

- 12.2.4. Edge Computing

- 12.2.5. Other Computing Types

- 12.3. Market Analysis, Insights and Forecast - by Deployement

- 12.3.1. Cloud

- 12.3.2. On-Premise

- 12.4. Market Analysis, Insights and Forecast - by End-user

- 12.4.1. Automotive & Transportation

- 12.4.2. Energy & Utilities

- 12.4.3. Healthcare

- 12.4.4. BFSI

- 12.4.5. Aerospace & Defense

- 12.4.6. Media & Entertainment

- 12.4.7. IT & Telecom

- 12.4.8. Retail

- 12.4.9. Manufacturing

- 12.4.10. Other End Users

- 12.1. Market Analysis, Insights and Forecast - by Component

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 IBM Corporation

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Alibaba Group Holding Limited

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Google LLC

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Microsoft Corporation

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Amazon Web Services Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 NVIDIA Corp

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 NEC Corporation

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Oracle Corporation

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Cisco Systems

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Intel Corporation

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 IBM Corporation

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Next-generation Computing Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Next-generation Computing Market Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 4: North America Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 5: North America Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 7: North America Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 8: North America Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 9: North America Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 10: North America Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 11: North America Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 12: North America Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 13: North America Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 14: North America Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 15: North America Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 16: North America Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 17: North America Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 18: North America Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 19: North America Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 20: North America Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 21: North America Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 22: North America Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 23: Europe Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 24: Europe Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 25: Europe Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 26: Europe Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 27: Europe Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 28: Europe Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 29: Europe Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 30: Europe Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 31: Europe Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 32: Europe Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 33: Europe Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 34: Europe Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 35: Europe Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 36: Europe Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 37: Europe Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 38: Europe Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 39: Europe Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 40: Europe Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 41: Europe Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 42: Europe Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 43: Asia Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 44: Asia Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 45: Asia Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 46: Asia Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 47: Asia Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 48: Asia Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 49: Asia Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 50: Asia Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 51: Asia Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 52: Asia Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 53: Asia Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 54: Asia Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 55: Asia Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 56: Asia Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 57: Asia Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 58: Asia Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 59: Asia Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 60: Asia Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 61: Asia Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 63: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 64: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 65: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 66: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 67: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 68: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 69: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 70: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 71: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 72: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 73: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 74: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 75: Australia and New Zealand Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 76: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 77: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 78: Australia and New Zealand Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 79: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 80: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 81: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 82: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 83: Latin America Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 84: Latin America Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 85: Latin America Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 86: Latin America Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 87: Latin America Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 88: Latin America Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 89: Latin America Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 90: Latin America Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 91: Latin America Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 92: Latin America Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 93: Latin America Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 94: Latin America Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 95: Latin America Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 96: Latin America Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 97: Latin America Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 98: Latin America Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 99: Latin America Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 100: Latin America Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 101: Latin America Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 102: Latin America Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 103: Middle East and Africa Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 104: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 105: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 106: Middle East and Africa Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 107: Middle East and Africa Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 108: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 109: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 110: Middle East and Africa Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 111: Middle East and Africa Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 112: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 113: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 114: Middle East and Africa Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 115: Middle East and Africa Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 116: Middle East and Africa Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 117: Middle East and Africa Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 118: Middle East and Africa Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 119: Middle East and Africa Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 120: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 121: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 122: Middle East and Africa Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 4: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 5: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 6: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 7: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 8: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 9: Global Next-generation Computing Market Revenue Million Forecast, by Region 2020 & 2033

- Table 10: Global Next-generation Computing Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 12: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 13: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 14: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 15: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 16: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 17: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 18: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 19: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 21: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 22: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 23: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 24: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 25: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 26: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 27: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 28: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 29: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 32: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 33: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 34: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 35: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 36: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 37: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 38: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 39: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 42: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 43: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 44: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 45: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 46: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 47: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 48: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 49: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 52: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 53: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 54: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 55: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 56: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 57: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 58: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 59: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 62: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 63: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 64: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 65: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 66: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 67: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 68: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 69: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Next-generation Computing Market?

The projected CAGR is approximately 19.38%.

2. Which companies are prominent players in the Next-generation Computing Market?

Key companies in the market include IBM Corporation, Alibaba Group Holding Limited, Google LLC, Microsoft Corporation, Amazon Web Services Inc, NVIDIA Corp, NEC Corporation, Oracle Corporation, Cisco Systems, Intel Corporation.

3. What are the main segments of the Next-generation Computing Market?

The market segments include Component, Computing Type, Deployement, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD 191.62 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth in demand for high performance computing; Adoption of Advanced Analytics in SMEs.

6. What are the notable trends driving market growth?

The Cloud Deployment of The Solutions Significantly Contributes to The Market Growth.

7. Are there any restraints impacting market growth?

Risk of Data Breach in Storing and Processing Large Data in Next-gen Computing; High operational challenges in Implementing the Solution.

8. Can you provide examples of recent developments in the market?

July 2023: Moody's and Microsoft have partnered strategically to co-create next-generation data, analytics, research, collaboration, and risk solutions for financial services, which would be built by combining Microsoft's Azure OpenAI Service, Fabric, and Teams with Moody's proprietary data, analytics, and research and has been designed to enhance insights into corporate intelligence and risk assessment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Next-generation Computing Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Next-generation Computing Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Next-generation Computing Market?

To stay informed about further developments, trends, and reports in the Next-generation Computing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence